Business

SDB bank set to boost SMEs and women entrepreneurship nationwide

Securing LKR 7.5 billion term loan facility from U.S International Development Finance Corporation (DFC)

The United States International Development Finance Corporation (DFC) has approved a USD 40 Million (Rs. 7.5 Billion) term loan facility to SDB bank in a bid to promote financial inclusion, resulting in more support to SMEs, particularly female-owned Small and Medium Enterprises. This comes as part of the financing recently approved by the DFC board to advance development in emerging markets of African, Middle Eastern, Eastern European, Indo-pacific, and Latin American regions.

United States International Development Finance Corporation (DFC) is a U.S. Development Bank specializing in providing financial support to private sector partners in developing markets. Promoting financial support to SMEs and women entrepreneurs in these markets is a key focus area for the bank. SDB bank was selected for the loan primarily due to its innovative business model that takes a progressive approach to development, with an emphasis on financial empowerment and SME development. In fact, 40% of the loan facility is reserved exclusively for women with the remaining 60% being allocated to SMEs in general. The bank’s commitment to these forward-looking policies is evident in their specialized products for female-owned SMEs which include Uththamavi, a special investment scheme for women and a general SME loan offering.

The investment loan approval granted by DFC comes at a critical time and is the first in over 7 years. The loan also comes with a series of other value additions including a Capacity Development Programme, which gives bank employees access to modern technology and know-how. This invaluable resource is then passed on to the customer, which enables them to grow their enterprise, as their hard work is directed by strategic thinking and professional business insight.

Speaking about this monumental opportunity, Thilak Piyadigama, CEO, SDB bank had this to say, “DFC is known for financing solutions which have helped overcome some of the most critical problems across the developing world. This loan comes at a time when the country needs financial support and gives us the chance to get our economy back on track faster. As always we will be giving the SME sector our full support. This loan will go a long way towards ensuring a more self-sufficient country, where hardworking Sri Lankans, who are the engine of progress, realise their financial ambitions. We are also focused on utilising these funds to create a new era of financial freedom and empowerment for female entrepreneurs”.

By uplifting SMEs and encouraging the spirit of entrepreneurship SDB Bank continues to create opportunities all over the island. These initiatives create jobs, ensure local communities are uplifted, and enable Sri Lankans to enjoy a better quality of life by giving them access to higher wages. They help safeguard the rights of workers, the preservation of the environment, and continually support SME empowerment. This development is essential for the country to remain competitive on a global scale. These initiatives also guarantee critical investment happens at the right time for maximum developmental impact. SDB bank shares these developmental goals and is honoured to lead the way for a new era of progress and prosperity.

Business

Ambeon Securities hosts exclusive investor forum on Sri Lanka’s economic and market outlook

Ambeon Securities recently hosted an exclusive investor forum, bringing together clients, investors, business leaders, and market professionals for an insightful discussion on Sri Lanka’s economic outlook and investment opportunities amidst a challenging global landscape.

The event was organized with the objective of providing investors with valuable insights to make better-informed investment decisions while further strengthening the firm’s engagement with its growing client base.

The forum featured Baqar Zaidi, Director and Chief Economist for Sri Lanka and India at Citi Research, as the keynote speaker. Sharing his perspectives on the evolving global macroeconomic environment, Mr. Zaidi discussed key themes influencing emerging and frontier markets, Sri Lanka’s economic trajectory, and the opportunities lie ahead.

The keynote address was followed by an engaging panel discussion comprising Baqar Zaidi, Aravinda De Silva, respected investor, entrepreneur, and the Chairman of Arcasia Holdings. Hasitha Premaratne, Group Managing Director of Brandix and Asanka Herath, Chief Executive Officer – Unit Trusts and Head of Equities at LYNEAR Wealth Management.

Moderated by Imran Furkan, the panel explored a range of topics including Sri Lanka’s macroeconomic outlook, the future of the Colombo Stock Exchange, sectoral opportunities, capital allocation strategies, investor confidence, and the role of policy reforms in attracting investment and supporting long-term growth.

Speaking at the event, Charith Kamaladasa, Chief Executive Officer of Ambeon Securities, reaffirmed the company’s commitment to facilitate quality insights, informed perspectives, and meaningful dialogue to support their clients while building lasting relationships with them. He noted that in an environment where uncertainty has become the new normal, equipping investors with timely information and expert perspectives is essential for successful wealth creation.

The event was well attended by a distinguished gathering of institutional investors, high-net-worth investors, and business leaders. Among those present were members of the Ambeon Group Board, including Group Chairman Sujeewa Mudalige, Group CEO Dr. Sajeeva Narangoda, and Chairman of Ambeon Securities Mangala Boyagoda. Their presence, together with the participation of Ambeon Group shareholders and valued clients, enriched the discussions and contributed to a vibrant networking session, fostering meaningful dialogue and stronger connections within the investment community.

Through initiatives such as this, Ambeon Securities continues to reinforce its commitment to helping clients navigate evolving market conditions, make informed investment decisions, and achieve their long-term financial goals.

The Tata Group, in partnership with ChildFund and DIMO, has successfully implemented a humanitarian education support initiative for disaster-affected schoolchildren in Sri Lanka, reaffirming its commitment to helping communities recover from the impacts of Cyclone Ditwah and the subsequent floods.

Following a formal request for support from Sri Lanka, an on-ground assessment was conducted in December 2025. Recognizing the urgent need, several Tata companies joined forces to implement the response program.

As part of this initiative, the ‘Hope in a Backpack’ programme, which provides disaster-affected children with essential educational supplies, was launched by the Tata Group at Taj Samudra, Colombo, in the presence of the Chief Guest, Hon. Prime Minister Dr. Harini Amarasuriya; the Guest of Honour, Hon. Indian High Commissioner Santhosh Jha; Ranjith Pandithage, Chairman of DIMO; Chacko Thomas, Group Chief Sustainability Officer, Tata Sons; and Aditi Ghosh, Country Director, ChildFund.

This initiative is part of DIMO’s Social and Community Pillar, under the project theme ‘Lassana Hetak,’ which focuses on giving the future generation a helping hand towards a better future.

This collective effort was further strengthened by volunteers from Tata and DIMO, who actively mobilized on the ground to pack, distribute, and support affected communities. During the proceedings, specially invited schoolchildren received the backpacks with essential supplies as well.

Commenting on the partnership, Ranjith Pandithage, Chairman of DIMO, said: “DIMO is proud to collaborate on this meaningful initiative alongside the Tata Group and ChildFund as the local implementation and logistics partner. Our relationship with Tata spans more than six decades and has been built on a shared commitment to ethical business practices, trust, and creating lasting value for the communities we serve. These values have shaped our partnership over the years, extending beyond business to initiatives that make a meaningful difference in people’s lives.”

NovaNest Properties (Pvt) Ltd has officially launched Rainbow Apartments, a new residential development in Ratmalana. The announcement was made at an official launch event held at the Shangri-La Hotel, Colombo, marking the company’s latest addition to Sri Lanka’s growing apartment market.

The development is designed to cater to homebuyers seeking modern urban living, as well as investors looking for long-term value. Rainbow Apartments is located in Ratmalana, an area of increasing residential interest, and benefits from the suburb’s established social infrastructure, proximity to major transportation links, and accessibility to Colombo.

The project reflects NovaNest Properties’ commitment to delivering quality residential developments that combine contemporary design with practical living. Intended to satisfy the evolving lifestyle demands of today’s homeowners, Rainbow Apartments features thoughtfully designed living spaces supported by modern amenities. These include two infinity pools, a gym, fully functional workspaces, a mini theatre, stylish cafés, a mini-mart, and a children’s daycare. Additionally, it features a full time medical centre backed by Nawaloka Hospitals PLC Colombo, with a 24-hour ambulance service.

Commenting on the launch, the Chief Executive Officer of NovaNest Properties (Pvt) Ltd, Samitha Waidyasekera, said, “Today’s buyers are looking beyond square footage. In addition to providing long-term value, they want homes that are close to the places where they work, learn, and spend their time. With that shift in mind, Rainbow Apartments was created to bring together a strategic location, thoughtful design, and quality construction in a way that will continue to meet buyers’ needs for years to come. Through our promise of ‘Luxury Beyond Expectations,’ we are committed to delivering an elevated lifestyle experience that combines comfort, convenience, and modern living.

Can Argentina and Messi beat Spain and Yamal to defend World Cup?

Anushka Sanjeewani, Vishmi Gunaratne return for Pakistan ODIs

Lennox stars again as New Zealand take series lead after West Indies collapse

Former IGP C.D. Wickramaratne found dead at his residence

Venezuela earthquake: Number of known dead rises to nearly 5,000 victims

A few showers may occur in the Western, Sabaragamuwa and North-western provinces and in Kandy, Nuwara-Eliya, Galle and Matara districts

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features6 days ago

Features6 days agoPrison riots and politics: NPP’s biggest challenge and Sri Lanka’s biggest opportunity

-

Editorial7 days ago

Editorial7 days agoWhat’s the world coming to?

-

Features3 days ago

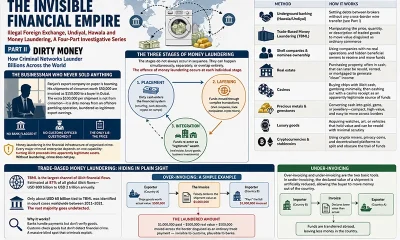

Features3 days agoDirty Money

-

Editorial6 days ago

Editorial6 days agoMuch ado about crime: Fish or cut bait

-

Features6 days ago

Features6 days agoMore on Saudi Arabia: ARAMCO and beyond

-

Midweek Review3 days ago

Midweek Review3 days agoThe sordid tale of theft and tragedy at Finance Ministry

-

Latest News3 days ago

Latest News3 days agoOil prices hit 1-month high as US-Iran attacks dim Strait of Hormuz outlook

-

Features5 days ago

Features5 days agoDeepening Democracy – Constitutions and Constitutionalism