Business

Special goods and services tax: Issues and concerns

By Dr Roshan Perera & Naqiya Shiraz

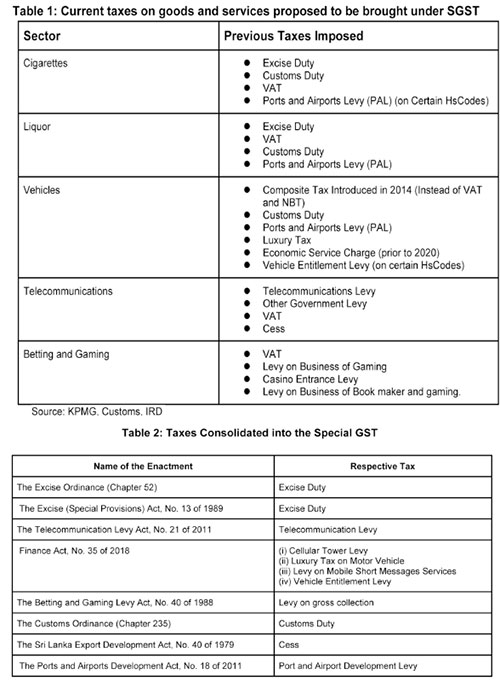

The new bill titled ‘Special Goods and Services Tax’ was published by gazette dated 07 January 2022.1 The Special Goods and Services Tax (SGST) was originally proposed in Budget speech 2021 but was not implemented. It has once again been presented in Budget 2022. The SGST aims to consolidate taxes on manufacturing and importing cigarettes, liquor, vehicles and assembly parts, while also consolidating taxes on telecommunication and betting and gaming (see table 1 for existing taxes on these products and table 2 for taxes consolidated into the SGST as per the schedule in the gazette). The rationale for this new tax as per the bill is “…to promote self-compliance in the payment of taxes in order to ensure greater efficiency in relation to the collection and administration on such taxes by avoiding the complexities associated with the application and administration of a multiple tax regime on specified goods and services.”

Given the multiplicity of taxes and the complexity of the current tax system as a whole, rationalising taxes is necessary to improve collection. However, whether the proposed SGST simplifies the tax system, while ensuring revenue neutrality or even improving revenue collection, needs to be carefully examined.

The SGST Bill is silent on the treatment of the existing VAT on these goods and services. However, according to the Value Added Tax (Amendment) Bill also gazetted on 07 January 2022,1 liquor, cigarettes and motor vehicles will be exempted from VAT while telecommunications and betting and gaming services will still be subject to VAT.

While the gazetted Bill sets out some of the features of the proposed SGST there are many important areas not covered in the Bill. These are expected to be gazetted as and when required by the Minister in charge.

Issues & Concerns

The motivation behind SGST is the simplification of the tax system. Although the objective of introducing the SGST is to improve efficiency by reducing the complexity of the tax system there are many issues and concerns with this proposed tax.

Revenue

Tax revenue which was 13% of GDP in 2010, declined to 8% in 2020. Ad hoc policy changes and weak administration contributed to the decline in tax revenue collection. This continuous decline in tax revenue has led to widening fiscal deficits and increasing debt. One of the main reasons for the current macroeconomic crisis is low tax revenue collection. Hence, any change to the existing tax system should be with the primary objective of raising more revenue.

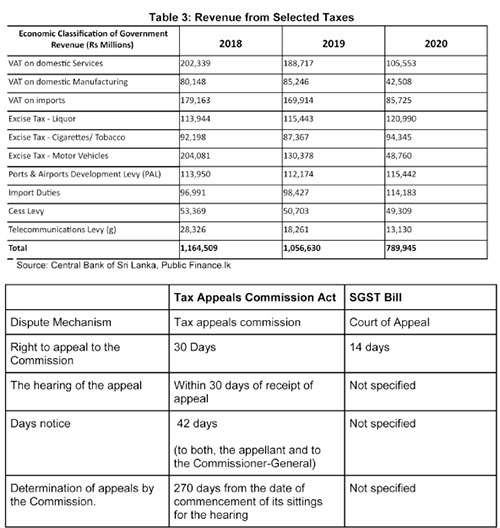

According to the budget speech the SGST is estimated to bring in an additional Rs. 50 billion in revenue in 2022.1 Revenue from taxes proposed to be consolidated under the SGST has significantly declined over the past 3 years. Given the already difficult macroeconomic environment, along with ad hoc tax policy changes raising the additional revenue estimated at Rs. 50 billion seems a difficult task.

Tax Base and Rate

For the SGST to raise taxes in excess of what is already being collected through the existing taxes, the rate and the base for the SGST needs to be carefully and methodically calculated. Further, the existing taxes have different bases of taxation. For instance the basis of taxation of motor vehicles is both on an ad valorem1 basis and a quantity basis while the basis of taxation of cigarettes and liquor is quantity.2 In light of this, the basis of taxation on which SGST isapplied becomes an issue. Having different bases and different rates for various goods and services would complicate the implementation of the tax These issues need to be carefully considered to ensure the new tax is revenue neutral or be able to enhance revenue collection.

Efficiency

One possible revenue benefit of this proposal is the inability to claim input tax credits on the sectors exempted from VAT. However, the issue is the cascading effect that would result where there would be a tax on tax with the end consumer paying taxes on already paid taxes. If the idea was to raise additional revenue by limiting tax credits, it would have been simpler to raise the tax rates on the existing taxes rather than introduce a new tax.

4. Administration

According to the bill, SGST will now be collected through a new unit set up under the General Treasury where a Designated Officer (DO) will be in charge of the administration, collection and accountability of the tax. The existing revenue collection agencies, such as the Inland Revenue Department (IRD) or the Excise Department will not be primarily responsible for the collection of this tax. By removing the IRD and Excise Department, a parallel bureaucracy will be created, at a time when public spending needs to be carefully managed. The General Treasury also has no previous experience and expertise in direct revenue collection. Weak administration is one of the key reasons for the low tax collection and success of this tax would depend on the strength of its administration.

In addition to the above mentioned concerns, as per the Bill the minister in charge of the SGST has been vested with the power to set the rates, the base and grant exemptions. Accordingly, Parliamentary oversight over fiscal matters is weakened under this proposed Bill.

It could also lead to a time lag between the gazetting and implementing of changes to the SGST (such as the rate, base etc) and obtaining Parliamentary approval for those changes.

Dispute resolution

The SGST Bill also focuses on the dispute resolution mechanism. Under the present tax system, with the enactment of the Tax Appeals Commission Act, No. 23 in 2011 the Tax Appeals Commission has the “responsibility of hearing all appeals in respect of matters relating to imposition of any tax, levy or duty”.1 The most recent amendment to the Tax Appeal

Commissions act (2013)1 seeks to address the large number (495) of cases pending before the Tax Appeals Commision2 by increasing the number of panels to hear the appeals.

Under the proposed SGST disputes will be handled through the court of appeal. However, the time period by which specific actions need to be taken is not provided in the bill. In addition, disputes have to be taken to the court of appeal. Hence, the entire process will be more time consuming. This could result in revenue lags and difficulties in revenue estimation until disputes are resolved.

Additionally, in the case that no valid appeal has been lodged within 14 days, any remaining payments would be considered to be in default. Thereafter, the responsibility is shifted to the Commissioner General of the IRD to recover the dues. Given the IRD is completely removed from the normal collection process, the rationale for bringing defaults under the IRD is not clear.

III. Policy Recommendations

As discussed, the SGST Bill has several limitations and much of this is due to the ambiguities in the Bill.

If the tax is implemented, the rate and basis of taxation needs to be revenue neutral to ensure tax collection is maximised and administrative costs minimised.

The rates, basis of taxation, exemptions etc should be specified in the Bill, as done in most other Acts. This would avoid the power for discretionary changes to the tax being placed in the hands of the minister in charge.

Given the already weak tax administration, it would be more sensible to strengthen the existing revenue collecting agencies and address the weaknesses in the existing system without creating a parallel bureaucracy.

In the case where VAT is consolidated into the proposed GST, the issue of cascading effect of input tax credits needs to be addressed. This is relevant particularly in the case of capital expenditure.

Given the critical state of revenue collection in the country the question to ask is whether this is the best time to introduce a new tax. Focus should be on fixing issues in the existing tax system to ensure revenue is maximised. The VAT is the least distortionary tax and it is the easiest to administer. Given these features it can be a very efficient revenue generator for a country. Therefore instead of introducing a new tax, capitalising on systems that are already in place and amending the VAT rate, threshold and exemptions may be a more practical solution to the revenue problem that the country is currently facing.

Dr. Roshan Perera is a Senior Research Fellow at the Advocata Institute and the former Director of the Central Bank of Sri Lanka.

Naqiya Shiraz is a Research Analyst at the Advocata Institute.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

Business

Sri Lanka Climate Summit flags need to ‘mainstream climate action into country’s growth story’

Sri Lanka has reached a critical juncture where climate action must evolve from policy discussions into tangible investments capable of driving economic growth, strengthening competitiveness and attracting international capital, speakers at the second Sri Lanka Climate Summit 2026 organised by the Ceylon Chamber of Commerce said.

Held under the theme “From Risk to Opportunity: Mainstreaming Climate Action into Sri Lanka’s Growth Story,” the summit at Taj Samudra yesterday brought together policymakers, multilateral agencies, financiers and private sector leaders to assess whether Sri Lanka is climate-ready for investment and how climate resilience can be transformed into an economic advantage.

Delivering the welcome address, Chairman of the Ceylon Chamber of Commerce, Krishan Balendra, said climate action could no longer be treated as a separate sustainability agenda.

“As Sri Lanka enters its next phase of economic growth and recovery, climate action must become part of our competitiveness agenda, our investment agenda and ultimately our national growth story, Balendra said.

He noted that since the inaugural Climate Summit in 2024, the Chamber had moved beyond advocacy to practical implementation through initiatives promoting Environmental, Social and Governance (ESG) practices, climate disclosures, green innovation and public-private collaboration.

The Chamber has also established a public-private working group jointly led by the Ministry of Environment and the Chamber to support implementation of Sri Lanka’s Nationally Determined Contributions (NDCs) and emerging carbon market frameworks.

Environment Minister Dr. Dhammika Patabendi, delivering the keynote address titled “Sri Lanka’s Climate State of the Nation 2026, said the government was positioning climate resilience as a cornerstone of economic transformation.

“We are working directly with the Chamber to transform global climate risks into Sri Lanka’s greatest competitive advantages, the minister said.

He highlighted landmark amendments to the National Environment Act aimed at modernising environmental governance while providing greater certainty to investors.

According to Patabendi, the reforms would shift environmental compliance from a reactive and punitive model to a proactive framework that provides businesses with greater operational clarity before projects commence.

The minister also stressed that environmental compliance is increasingly becoming a prerequisite for access to premium export markets.

“Enhanced environmental standards act as an economic shield for our exporters, validating the ‘Made in Sri Lanka’ brand as an ethically secure, low-carbon choice, he said.

Patabendi reaffirmed Sri Lanka’s comm

itment to achieving 70 percent renewable energy generation by 2030 and carbon neutrality by 2050, while highlighting significant opportunities in wind energy development, including an estimated 56 gigawatts of offshore wind potential.

Vimlendra Sharan, FAO Representative for Sri Lanka and the Maldives, described Sri Lanka as a country that is simultaneously “climate vulnerable and climate ambitious.”

“The real question is whether Sri Lanka is climate investment ready. That journey has only just begun, Sharan observed.

He argued that climate readiness required transforming vulnerabilities and ambitions into structured, financeable and scalable investments.

One of the country’s biggest challenges, according to Sharan, is the limited pipeline of bankable climate projects.

“The major gap is the lack of investment-ready projects. We also need stronger project preparation capacity, more data and better evidence to unlock larger volumes of climate finance, he said.

Speakers agreed that climate resilience is no longer merely an environmental issue but an economic imperative affecting trade, investment flows, supply chain access and long-term growth prospects.

By Ifham Nizam

A leading Australia-based sustainable energy solutions company, ‘365 Future Energy’, is now exploring possibilities to enter Sri Lanka to provide sustainable energy solutions to Sri Lanka at affordable prices.

‘365 Future Energy’ CEO, Isuru Yapa, together with internationally recognized energy technology entrepreneur Ludovico Finotto,visited Sri Lanka this week.

” If we could set up this plant here it would benefit Sri Lanka because it could store sustainable energy to stabilise the national grid, supply energy at an affordable operational cost and manage the energy supply system in a more stable manner, Ludovico Finotto, founder and CEO of ‘QiOn Technologies’ a globally recognized innovator in the energy, automotive and high-performance electronics sectors, said.

With over 18 years of international experience, Finotto has played a leading role in advanced developments related to electric mobility, energy storage, charging infrastructure, hydrogen technologies, marine electrification and smart energy systems in more than 24 countries.

Speaking to the Island Financial Review he said that the purpose of this strategic visit is to explore sustainable energy solutions, evaluate emerging opportunities within Sri Lanka’s energy sector and identify potential investment and technology partnerships that can contribute to the country’s future energy transformation.

‘365 Future Energy’ is focused on delivering innovative and environmentally responsible energy solutions, supporting the global transition toward renewable and sustainable power infrastructure. Through this visit, the company aims to better understand Sri Lanka’s growing energy demands and assess opportunities for collaboration in renewable energy technologies, energy storage systems, EV charging infrastructure and next-generation sustainable energy developments.

‘365 Future Energy’ believes Sri Lanka holds strong potential for future-focused sustainable infrastructure projects and clean energy investments. The company’s leadership team will engage with local stakeholders, businesses, and industry representatives during the visit to discuss opportunities for innovation, energy efficiency, and long-term sustainable growth, company sources said.

By Hiran H Senewiratne

Celebrating the spirit of Vesak, Serendib Flour Mills served the community through a Tea Bun Dansala and Plain Tea Dansala held near the Orugodawatta Bridge on 29 May 2026, distributing 12,500 buns and 12,500 cups of tea to devotees and members of the public.

The Dansala commenced with the blessings and presence of a venerable monk, reflecting the values of compassion, generosity and service that define Vesak. The initiative was carried out through the collective commitment of the Serendib Flour Mills team, who came together to serve the community and support those observing the sacred occasion.

Through this initiative, Serendib Flour Mills reinforced its belief that nourishment extends beyond food, living in the kindness shared, the relationships built and the communities uplifted. Guided by its purpose of “Nourishing the Nation,” the company remains committed to creating nourished futures through meaningful acts of service and care.

Rana and Mosaddek star as Bangladesh end 21-year wait with crushing win

Formulation of a Draft Economic Development Bill to expedite the process of Digital Transformation and Digital Economic Development

Cabinet approval for Sri Lanka Community and Health Survey – 2026/2027

A National Water Tariff Policy for all Water Supply and Sanitation Services

National Policy on Green Hydrogen in Sri Lanka

Cabinet nod to amend the Customs Ordinance

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Latest News6 days ago

Latest News6 days agoKusal Mendis, Pathum Nissanka, bowlers put Sri Lanka 1-0 up

-

News6 days ago

News6 days agoNew US tariffs proposed on 60 countries, including Sri Lanka

-

Features5 days ago

Features5 days agoPower crept into the Sangha and is now tearing it apart

-

Features5 days ago

Features5 days agoKondachchi wind farm and battery storage project to boost energy security, says Power Ministry Secretary

-

News3 days ago

News3 days agoWomen’s T20 World Cup 2026 warm-up: Chamari Athapaththu’s 94 helps Sri Lanka beat Pakistan

-

Features5 days ago

Features5 days agoSaudi Arabia sets new benchmark in Hajj management as 1.7 million pilgrims complete sacred journey

-

News4 days ago

News4 days agoAsst. Manager, security officer arrested over Rs 30 mn snatch at Horana PB branch

-

Editorial2 days ago

Editorial2 days agoProbe Sallay’s complaint