Business

Special goods and services tax: Issues and concerns

By Dr Roshan Perera & Naqiya Shiraz

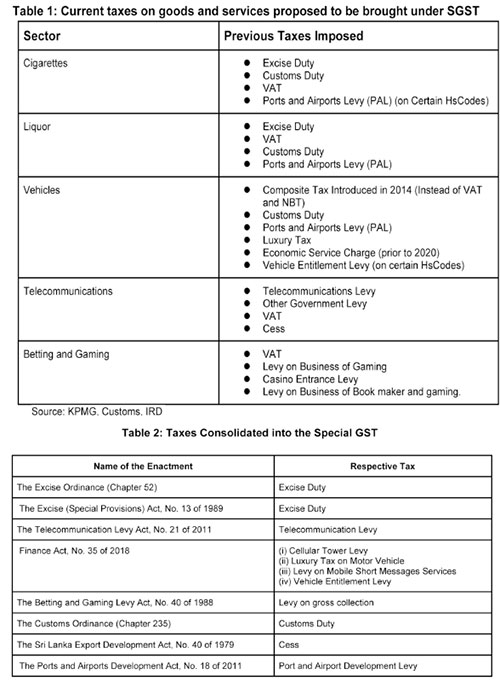

The new bill titled ‘Special Goods and Services Tax’ was published by gazette dated 07 January 2022.1 The Special Goods and Services Tax (SGST) was originally proposed in Budget speech 2021 but was not implemented. It has once again been presented in Budget 2022. The SGST aims to consolidate taxes on manufacturing and importing cigarettes, liquor, vehicles and assembly parts, while also consolidating taxes on telecommunication and betting and gaming (see table 1 for existing taxes on these products and table 2 for taxes consolidated into the SGST as per the schedule in the gazette). The rationale for this new tax as per the bill is “…to promote self-compliance in the payment of taxes in order to ensure greater efficiency in relation to the collection and administration on such taxes by avoiding the complexities associated with the application and administration of a multiple tax regime on specified goods and services.”

Given the multiplicity of taxes and the complexity of the current tax system as a whole, rationalising taxes is necessary to improve collection. However, whether the proposed SGST simplifies the tax system, while ensuring revenue neutrality or even improving revenue collection, needs to be carefully examined.

The SGST Bill is silent on the treatment of the existing VAT on these goods and services. However, according to the Value Added Tax (Amendment) Bill also gazetted on 07 January 2022,1 liquor, cigarettes and motor vehicles will be exempted from VAT while telecommunications and betting and gaming services will still be subject to VAT.

While the gazetted Bill sets out some of the features of the proposed SGST there are many important areas not covered in the Bill. These are expected to be gazetted as and when required by the Minister in charge.

Issues & Concerns

The motivation behind SGST is the simplification of the tax system. Although the objective of introducing the SGST is to improve efficiency by reducing the complexity of the tax system there are many issues and concerns with this proposed tax.

Revenue

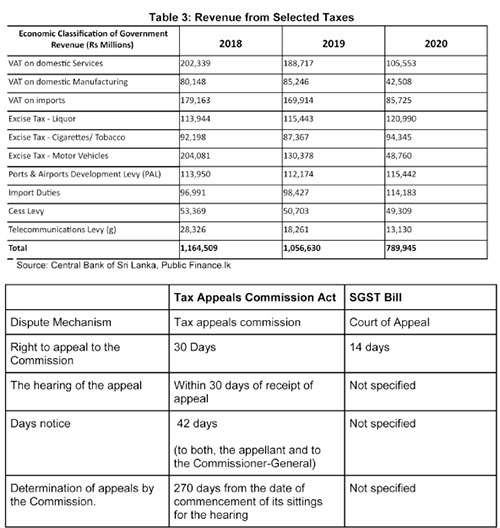

Tax revenue which was 13% of GDP in 2010, declined to 8% in 2020. Ad hoc policy changes and weak administration contributed to the decline in tax revenue collection. This continuous decline in tax revenue has led to widening fiscal deficits and increasing debt. One of the main reasons for the current macroeconomic crisis is low tax revenue collection. Hence, any change to the existing tax system should be with the primary objective of raising more revenue.

According to the budget speech the SGST is estimated to bring in an additional Rs. 50 billion in revenue in 2022.1 Revenue from taxes proposed to be consolidated under the SGST has significantly declined over the past 3 years. Given the already difficult macroeconomic environment, along with ad hoc tax policy changes raising the additional revenue estimated at Rs. 50 billion seems a difficult task.

Tax Base and Rate

For the SGST to raise taxes in excess of what is already being collected through the existing taxes, the rate and the base for the SGST needs to be carefully and methodically calculated. Further, the existing taxes have different bases of taxation. For instance the basis of taxation of motor vehicles is both on an ad valorem1 basis and a quantity basis while the basis of taxation of cigarettes and liquor is quantity.2 In light of this, the basis of taxation on which SGST isapplied becomes an issue. Having different bases and different rates for various goods and services would complicate the implementation of the tax These issues need to be carefully considered to ensure the new tax is revenue neutral or be able to enhance revenue collection.

Efficiency

One possible revenue benefit of this proposal is the inability to claim input tax credits on the sectors exempted from VAT. However, the issue is the cascading effect that would result where there would be a tax on tax with the end consumer paying taxes on already paid taxes. If the idea was to raise additional revenue by limiting tax credits, it would have been simpler to raise the tax rates on the existing taxes rather than introduce a new tax.

4. Administration

According to the bill, SGST will now be collected through a new unit set up under the General Treasury where a Designated Officer (DO) will be in charge of the administration, collection and accountability of the tax. The existing revenue collection agencies, such as the Inland Revenue Department (IRD) or the Excise Department will not be primarily responsible for the collection of this tax. By removing the IRD and Excise Department, a parallel bureaucracy will be created, at a time when public spending needs to be carefully managed. The General Treasury also has no previous experience and expertise in direct revenue collection. Weak administration is one of the key reasons for the low tax collection and success of this tax would depend on the strength of its administration.

In addition to the above mentioned concerns, as per the Bill the minister in charge of the SGST has been vested with the power to set the rates, the base and grant exemptions. Accordingly, Parliamentary oversight over fiscal matters is weakened under this proposed Bill.

It could also lead to a time lag between the gazetting and implementing of changes to the SGST (such as the rate, base etc) and obtaining Parliamentary approval for those changes.

Dispute resolution

The SGST Bill also focuses on the dispute resolution mechanism. Under the present tax system, with the enactment of the Tax Appeals Commission Act, No. 23 in 2011 the Tax Appeals Commission has the “responsibility of hearing all appeals in respect of matters relating to imposition of any tax, levy or duty”.1 The most recent amendment to the Tax Appeal

Commissions act (2013)1 seeks to address the large number (495) of cases pending before the Tax Appeals Commision2 by increasing the number of panels to hear the appeals.

Under the proposed SGST disputes will be handled through the court of appeal. However, the time period by which specific actions need to be taken is not provided in the bill. In addition, disputes have to be taken to the court of appeal. Hence, the entire process will be more time consuming. This could result in revenue lags and difficulties in revenue estimation until disputes are resolved.

Additionally, in the case that no valid appeal has been lodged within 14 days, any remaining payments would be considered to be in default. Thereafter, the responsibility is shifted to the Commissioner General of the IRD to recover the dues. Given the IRD is completely removed from the normal collection process, the rationale for bringing defaults under the IRD is not clear.

III. Policy Recommendations

As discussed, the SGST Bill has several limitations and much of this is due to the ambiguities in the Bill.

If the tax is implemented, the rate and basis of taxation needs to be revenue neutral to ensure tax collection is maximised and administrative costs minimised.

The rates, basis of taxation, exemptions etc should be specified in the Bill, as done in most other Acts. This would avoid the power for discretionary changes to the tax being placed in the hands of the minister in charge.

Given the already weak tax administration, it would be more sensible to strengthen the existing revenue collecting agencies and address the weaknesses in the existing system without creating a parallel bureaucracy.

In the case where VAT is consolidated into the proposed GST, the issue of cascading effect of input tax credits needs to be addressed. This is relevant particularly in the case of capital expenditure.

Given the critical state of revenue collection in the country the question to ask is whether this is the best time to introduce a new tax. Focus should be on fixing issues in the existing tax system to ensure revenue is maximised. The VAT is the least distortionary tax and it is the easiest to administer. Given these features it can be a very efficient revenue generator for a country. Therefore instead of introducing a new tax, capitalising on systems that are already in place and amending the VAT rate, threshold and exemptions may be a more practical solution to the revenue problem that the country is currently facing.

Dr. Roshan Perera is a Senior Research Fellow at the Advocata Institute and the former Director of the Central Bank of Sri Lanka.

Naqiya Shiraz is a Research Analyst at the Advocata Institute.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

The weekly Colombo Tea Auction concluded with offerings increasing to 6.5 million kilogrammes, a marginal rise from the previous week’s 6.4 million kilogrammes. However, the market witnessed a significant pullback from key international buyers, leading to a subdued trading atmosphere and declining prices across several categories.

Industry sources reported a noticeable lack of interest from shippers to the traditional markets of the United Kingdom and the European continent. While shippers to the Commonwealth of Independent States (CIS) and the Middle East maintained a presence, their participation was described as selective and at lower price levels. Buyers from Japan and China also operated at reduced levels, with South African shippers showing minimal engagement.

This cautious stance from the shipping community cast a shadow over the Ex-Estate sector, which offered 1.0 million kilogrammes. The overall quality of teas in this category was described as relatively uninteresting, leading to a weakening of prices. In the Western High Grown category, prices for the best available BOP/BOPF grades declined by Rs. 20 to 40 per kilogramme, while the plainer varieties saw a drop of about Rs. 20 per kilogramme. A fair quantity of these teas remained unsold due to a lack of suitable bids.

Nuwara Eliya teas attracted little to no interest, with the majority of offerings remaining unsold. Uda Pussellawa BOPs weakened further by up to Rs. 50 per kilogramme, while the corresponding BOPFs struggled to maintain their previous price levels. In the Uva region, BOPs saw prices fall by Rs. 50 per kilogramme, though the BOPF varieties were relatively more stable. The High and Medium Grown CTC teas continued to be a weak feature, with many lots unsold and those that were sold recording a price drop of Rs. 20 to 40 per kilogramme. Off-grades and dust grades also experienced a sluggish market, with fair volumes remaining unsold.

In contrast to the gloom in the High Growns, the Low Grown sector, which totalled approximately 2.7 million kilogrammes, met with more encouraging demand. The Leafy and Semi-Leafy categories saw fair demand, while the Tippy and Premium categories were met with good interest. While some well-made varieties in the Leafy catalogues remained firm, many other grades experienced easier prices. However, the Tippy catalogue saw high-priced FBOPs holding firm and the FF1s generally becoming dearer. The Premium catalogue, featuring tippy teas, also met with good demand and saw prices appreciate overall.

Based on Forbes & Walker Tea Brokers comments

By Sanath Nanayakkare

The Asian Development Bank (ADB) has formally entered into its first partnership with the International Committee of the Red Cross (ICRC), marking a significant step towards integrating humanitarian action with long-term development efforts in fragile and conflict-affected regions across Asia and the Pacific.

A Letter of Intent establishing the collaboration was signed on June 10 by ADB Vice-President for Sectors and Themes Fatima Yasmin and ICRC Director-General Pierre Krähenbühl. The agreement provides a framework for coordinating programmes, exchanging knowledge on emerging humanitarian challenges, promoting innovation and sharing best practices through joint events and publications.

The partnership brings together ADB’s development expertise and financing capabilities with the ICRC’s operational experience and access to communities affected by conflict and violence.

Highlighting the significance of the initiative, ADB President Masato Kanda wrote on X on June 17 that the partnership would help strengthen resilience in fragile and conflict-affected areas.

“By bringing together ADB’s longer-term development perspective with ICRC’s humanitarian field presence and operational experience, we can better support people affected by conflict and violence,” Kanda said.

Speaking at the signing ceremony, Yasmin said today’s interconnected challenges require development institutions to move beyond traditional approaches.

“The ICRC brings trusted access to affected communities and credibility in environments that ADB alone cannot easily reach,” she said.

Krähenbühl described the agreement as an important step towards bridging humanitarian assistance and long-term development, adding that it could create opportunities for joint responses in fragile settings across the region.

A Sri Lankan socio-economist told The Island Financial Review that the partnership reflects a growing recognition among development institutions that conflict, fragility and climate-related shocks are becoming major constraints on economic progress.

“Traditionally, development banks focused on long-term infrastructure and economic projects while humanitarian agencies addressed immediate crises. This partnership seeks to connect those two worlds by reducing vulnerability before crises deepen,” he said.

Prime Residencies, the real leader in the modern real estate, and a subsidiary of Prime Group, officially marked the commencement of construction on its latest ultra-luxury residential development, THE GOLF, with its groundbreaking ceremony held at the project site on Lake Drive, Colombo 8. The event brought together key stakeholders and project partners to mark the ceremonial breaking of the ground, signalling that a vision long in the making is currently under construction.

Cricket journalist and broadcast legend Qamar Ahmed dies aged 88

Stafanie Taylor, spinners help West Indies overcome Scotland threat

Showers will occur at times in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Thirty-five killed as gunmen attack Niger’s biggest airport

Creditor receives USD 2.5 mn as Lankan public bears loss from theft of Treasury funds

Former Minister Nalin raises defence of double jeopardy

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News4 days ago

News4 days agoRelease of 2025 O/L results likely to be delayed

-

Sports4 days ago

Sports4 days agoTharanga set for high-profile javelin clash in Ostrava

-

Features5 days ago

Features5 days agoPolitics of protected species

-

News3 days ago

News3 days agoBeijing Capital Airlines to resume flights to Colombo signalling boost to tourism

-

News4 days ago

News4 days agoTheft of USD 2.5 mn from Treasury: CoPF accused of complicity in NPP cover-up

-

News6 days ago

News6 days agoCommonwealth lawyers urge Lanka to uphold rule of law

-

Opinion4 days ago

Opinion4 days agoDecoding Trump’s 12.5% “Forced Labor Tariff” on Sri Lanka

-

Opinion4 days ago

Opinion4 days agoPalm leaf manuscripts of Sri Lanka – Part V