Business

Supporting the Increase in Withholding Tax: A Step Toward Strengthening Sri Lanka’s Tax System

By Sanjeewa Jayaweera

The government’s decision to increase the withholding tax (WHT) rate to 10%, effective 1 April 2025, deserves commendation. Too often, political leaders have avoided necessary but unpopular decisions, opting to appease the electorate. This has led to various issues, from economic stagnation to the erosion of minority and religious rights. The proposed tax increase, however, marks a significant step in addressing a pressing concern: Sri Lanka’s persistent tax evasion problem.

Tax evasion in Sri Lanka is alarmingly high. While some degree of evasion is common in many countries, effective tax compliance is largely achieved through a comprehensive tax policy and an efficient tax administration. Unfortunately, Sri Lanka has fallen short in both these areas. Since the early 1990s, successive governments have either reduced or eliminated key taxes, granted widespread exemptions, and failed to adequately develop the Inland Revenue Department (IRD) in terms of manpower and technology.

Rather than addressing these systemic issues, governments have relied on increasing indirect taxes. The contribution of direct taxes to overall revenue has fallen to a mere 20%. Indirect taxes, such as Value Added Tax (VAT), are largely hidden from the consumer, as the IRD has mandated that supplier invoices do not show VAT charged. This has created a society that is not accustomed to paying direct taxes. Additionally, the acceptance of corruption as a “necessary evil” has contributed to the perception that tax evasion is acceptable.

Consequently, the imposition of new taxes, rate increases, and threshold reductions often generates confusion and frustration among the public. Opposition parties frequently exploit these sentiments to mislead the electorate, complicating the government’s efforts. To counter this, the government must invest in educating the public about taxes, the need for tax revenue, and the civic duty of tax compliance. This is a long-term effort that, if successful, could lead to improved tax revenues and higher compliance rates.

Policymakers should consider insights from an OECD report published in 2021, which analyzed taxpayer education initiatives in 59 developed and developing countries. The report revealed that over 80% of such initiatives improved tax morale—the intrinsic motivation to pay taxes. The findings underscore the importance of tax literacy in shaping a culture where citizens understand how their tax contributions affect their daily lives.

The report suggests a step-by-step approach for designing and implementing taxpayer education initiatives customized to local contexts. Three key strategies for promoting tax compliance emerged:

· Teaching tax: Engaging all audiences, including youth, adults, and entrepreneurs, through long-term educational programs.

· Communicating tax

: Raising awareness through campaigns, tax fairs, TV shows, and behavioural economics-based messaging.

· Supporting compliance

: Providing practical assistance, particularly for vulnerable taxpayers, to navigate modern e-administration tools and fulfill reporting requirements.

Verité Research, an independent think tank, has long advocated increasing the WHT rate on interest income from 5% to 10%. Their estimate suggests that this increase could generate an additional Rs. 90 billion in revenue for the state. Despite this, the government of Ranil Wickremesinghe hesitated to act, even though it had already raised VAT to 18% and introduced progressive income tax rates as high as 36% and reduced the monthly tax-free threshold to Rs. 100,000.

Importantly, WHT on interest income is not an additional tax; it is a prepayment of taxes collected by the payer on behalf of the government, similar to the Pay As You Earn (PAYE) system used for salaried employees. The challenge, however, lies in the fact that individuals often earn interest from multiple banks, unlike salary income, which typically comes from a single employer. As a result, financial institutions cannot easily determine whether an individual’s total income surpasses the annual tax-free threshold of Rs. 1,200,000 (or Rs. 1,800,000 starting April 2025).

To address this, the IRD should implement a system allowing individuals over 18 to obtain a letter from the IRD confirming that WHT need not be deducted if their total annual income is below the threshold. While this will initially be challenging due to the lack of tax files for many individuals, it is a step that should be supported. Despite its complexities, the government’s decision to increase the WHT rate should be backed.

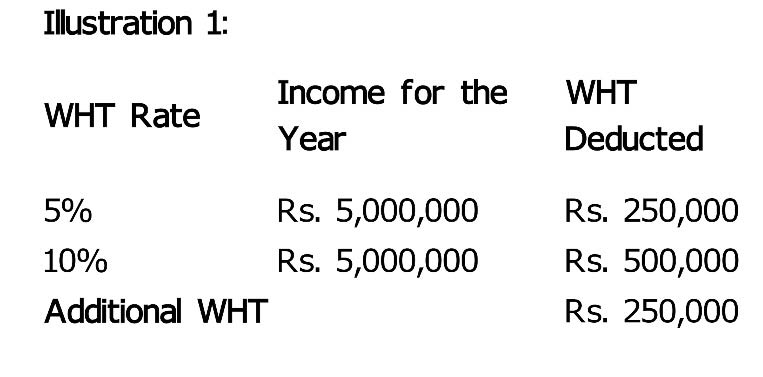

To illustrate the impact of this change, consider the following examples assuming the person’s total income is derived solely from interest:

Total Income Tax Due:

· Income: Rs. 5,000,000

· Single Person Allowance

: Rs. 1,200,000

· Taxable Income

: Rs. 3,800,000

· Income Tax at Progressive Rates

: Rs. 918,000

· Less WHT Collected at Source

: Rs. 250,000

· Tax Evaded

: Rs. 668,000

With the WHT Rate Increase:

· Income: Rs. 5,000,000

· Single Person Allowance

: Rs. 1,200,000

· Taxable Income

: Rs. 3,800,000

· Income Tax at Progressive Rates

: Rs. 918,000

· Less WHT Collected at Source

: Rs. 500,000

· Tax Evaded

: Rs. 418,000

As illustrated, raising the WHT rate to 10% would generate an additional Rs. 250,000 in tax revenue. I have assumed in my illustration that the recipient of interest income is not tax-compliant and is currently outside the tax net. This demonstrates how the rate increase could significantly reduce tax evasion. The IRD’s ultimate goal should be to recover the Rs. 418,000 currently evaded by taxpayers. By streamlining the reporting systems of financial institutions and integrating them with the RAMIS system, the IRD can take a significant step toward curbing tax evasion and boosting government revenue.

The Cabinet of Ministers has approved the appointment of a Committee, chaired by Senior Presidential Advisor on Digital Economy Dr. Hans Wijayasuriya, to conduct a strategic review and restructuring of SriLankan Airlines.

The other members of the committee are as follows:

• Senior Presidential Economic Advisor Duminda Hulangamuwa

• Financial and corporate strategy expert Deshal De Mel

• Transaction and investment banking, mergers and acquisitions expert Dumith Fernando

• The Secretary to the Ministry of Finance or his Representative

• The Secretary to the Ministry of Transport, Highways and Urban Development / a representative of the Civil Aviation Authority

• The Chairman of SriLankan Airlines

• Legal experts with specialised knowledge in corporate, aviation and public law

• Aviation industry experts to be appointed

The Government has recognised the urgent priority of undertaking a comprehensive strategic review of SriLankan Airlines, taking into account the broader macroeconomic context.

The main objective of this exercise is to establish a financially sustainable and commercially efficient national carrier, while reducing the long-term fiscal burden on the Government.

Accordingly, it has been deemed appropriate to establish a dedicated committee to carry out the strategic review and restructuring process in collaboration with the International Finance Corporation (IFC), which is serving as the Transaction Advisor.

The committee will be responsible for:

• Conducting an independent review and assessment of the airline’s strategic direction and future course of action

• Recommending restructuring requirements and possible restructuring models

• Evaluating specific strategic options and identifying the most suitable course of action aligned with the Government’s overall objectives

• Providing oversight, guidance and support for the implementation of the selected strategy and execution framework determined by the Government

The committee will function for the duration of the strategic review and restructuring process, or until it is formally dissolved by the Government of Sri Lanka.

(PMD)

Business

CMTA warns of further Rs. 40 billion revenue leakage in 2026, calls for urgent removal of 15% depreciation

The Ceylon Motor Traders’ Association (CMTA), the senior-most automotive association in Sri Lanka affiliated with the Ceylon Chamber of Commerce, has issued an urgent appeal to the government to abolish the 15% depreciation currently granted on used vehicle imports, warning that the concession is causing massive revenue leakages at a time when the country can least afford them.

The Association estimates that the existing depreciation mechanism resulted in approximately Rs. 40 billion in lost government revenue in 2025 alone. If corrective action is not taken immediately, a similar level of revenue leakage could occur in 2026, further impacting the government’s fiscal position and depriving the country of much-needed funds for national development and public services.

The Association notes that loopholes within the existing system have created opportunities for misuse, resulting not only in unfair advantages for certain importers but also in substantial losses to government revenue. Addressing these abuses, alongside the removal of the 15% depreciation concession, is essential to ensuring greater transparency, strengthening regulatory oversight, and protecting the integrity of Sri Lanka’s vehicle import sector.

While no official announcement has yet been made regarding the removal of the 15% depreciation, the CMTA has consistently highlighted the issue through multiple budget proposals submitted via the Ceylon Chamber of Commerce. The Association has repeatedly maintained that there is no viable justification for the continued application of this concession on used vehicle imports.

Currently, used vehicles receive a 15% depreciation on their Cost, Insurance and Freight (CIF) value for duty calculation purposes. However, the vast majority of vehicles entering the country through the used vehicle market are virtually zero-mileage units, with CIF values that are often comparable to those of brand-new vehicles. In such circumstances, the CMTA argues that granting a blanket 15% depreciation creates an unfair and unjustifiable tax advantage while significantly reducing government revenue collections.

The Association acknowledges that if the objective through this concession is making vehicles more affordable for consumers, then the CMTA stresses that affordability cannot be achieved through arbitrary concessions that create market distortions and substantial losses to the Treasury. If the intention is to reduce vehicle prices, similar policy considerations could be extended to brand-new vehicles rather than selectively benefiting one segment of the market.

Consumers who purchase brand-new vehicles benefit from manufacturer warranties, which help mitigate maintenance and repair costs during the warranty period. As a result, vehicle owners are less likely to incur additional expenses associated with importing replacement parts, providing greater long-term value, reliability, and peace of mind.

The CMTA further notes that as far back as 2013, a structured depreciation framework was implemented based on the age of a vehicle, rather than a flat-rate concession. Under this proposal, depreciation would be calculated according to a defined scale and capped at a maximum of 10%, ensuring greater fairness, transparency and alignment with the actual value of the vehicle.

The Association stated that the continued application of a blanket 15% depreciation is resulting in significant and unnecessary revenue leakages for the government. At a time when every rupee of revenue is critical to the country’s economic progress, this issue requires immediate attention and decisive action.

The CMTA therefore strongly urges the relevant authorities to take swift action to abolish the current 15% depreciation concession and close this avenue of revenue leakage without delay. The Association emphasises that every month of inaction increases the risk of further losses to the state and undermines efforts to strengthen public finances.

Should the government determine that some form of concession should continue to be extended to the used vehicle market, the CMTA maintains that it must be implemented through a structured and transparent framework based on vehicle age and capped at a reasonable level. Such an approach would ensure fairness while safeguarding government revenue and maintaining a level playing field across the automotive industry.

Businesses in Sri Lanka risk severe financial and operational disruption unless they urgently invest in climate adaptation and resilience measures, leading climate experts warned at a high-level dialogue on “Climate-Proofing Business Sri Lanka” held on Wednesday at Genesis – The Dilmah Centre for a Sustainable Future.

The event, jointly organized by Genesis and the Ceylon Chamber of Commerce, brought together corporate leaders, sustainability professionals, policymakers and climate specialists to discuss how climate change is rapidly emerging as one of the biggest risks facing Sri Lanka’s economy.

Climate Change and Disaster Risk Management Specialist Rohan Cooray said climate-related disasters were already exacting a heavy economic toll globally and locally.

He noted that climate-induced losses divert resources that could otherwise be invested in economic development and business growth and stressed the need for stronger adaptation measures to protect investments and livelihoods.

Delivering the keynote address, internationally renowned climate lawyer and governance specialist Dr. Lalanath de Silva said climate change was no longer a future threat but a present-day economic reality that businesses could not afford to ignore.

“The impacts are coming whether we like it or not,” he said. “The question is whether we prepare now or pay a much higher price later.”

Dr. de Silva explained that while global efforts have largely focused on mitigation—reducing greenhouse gas emissions—adaptation has become equally important, particularly for vulnerable countries such as Sri Lanka.

“Sri Lanka contributes less than one percent of global greenhouse gas emissions, yet we are among the countries most vulnerable to climate impacts,” he said.

He warned that climate change would alter rainfall patterns, intensify floods and droughts, increase the frequency of extreme weather events and place growing pressure on infrastructure, agriculture, water resources and businesses.

“We are very good at producing plans in Sri Lanka. What we have not been good at is implementing them.”

Calling for stronger institutional coordination, Dr. de Silva proposed the establishment of a high-level climate coordination mechanism operating at the highest level of government to ensure coherent action across ministries and agencies.

Providing scientific context to the discussion, Cooray presented projections based on global and regional climate models adopted by Sri Lanka’s Department of Meteorology.

According to Cooray, rainfall patterns across Sri Lanka are expected to become increasingly erratic.

The wet zone is projected to receive more intense rainfall events while many dry-zone regions could experience prolonged drought conditions interspersed with extreme rainfall episodes.

“The danger is not simply that some places become wetter and others become drier. The danger is the increasing variability and unpredictability of rainfall,” he said.

While mitigation projects often generate measurable returns, adaptation investments require innovative financing mechanisms and stronger public-private partnerships, speakers noted.

The event also featured contributions from Dilhan C. Fernando, chairman of Dilmah Ceylon Tea Company PLC; Shiran Fernando, Secretary General and CEO of the Ceylon Chamber of Commerce; and Yasangi Randeni, Chief Sustainability Officer of Aitken Spence PLC.

Speakers agreed that climate-proofing businesses is no longer simply about environmental responsibility but about safeguarding assets, maintaining competitiveness, protecting supply chains and ensuring long-term economic sustainability.

The consensus emerging from the forum was clear: while mitigation remains important, Sri Lanka’s immediate priority must be preparing businesses, communities and institutions for climate impacts that are already unavoidable.

By Ifham Nizam

USS Canberra makes port call in Colombo

Complete the Proposed Education Reform Policy Framework Within One Month – President

Committee appointed for restructuring SriLankan Airlines

Kane Williamson retires from international cricket

Jailed South Korea ex-president gets 30 more years for sending drones into North

Holder, Joseph set up victory as West Indies go 1-0 up against Sri Lanka

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoWomen’s T20 World Cup 2026 warm-up: Chamari Athapaththu’s 94 helps Sri Lanka beat Pakistan

-

News6 days ago

News6 days agoLankan-Canadian inducted to Toronto Sports Hall of Fame

-

News7 days ago

News7 days agoAsst. Manager, security officer arrested over Rs 30 mn snatch at Horana PB branch

-

Editorial5 days ago

Editorial5 days agoProbe Sallay’s complaint

-

News3 days ago

News3 days agoLocal firms move millions of dollars overseas for phantom imports: Govt.

-

Editorial6 days ago

Editorial6 days agoPrez in the dock

-

Features6 days ago

Features6 days agoEntering MIT for my Ph.D program, coping with harsh Boston winter and breasting the tape

-

News7 days ago

News7 days agoNo blanket ban on musical performances; only those promoting LTTE