Business

Income Tax, Professionals and Migration

by Naomal Goonewardena

I am a lawyer by profession who also happens to have an interest in the subject of tax. My tax liability and income tax payments for the year of assessment 2023/2024 would be more than 300% of that in 2021/2022. Not great by any means.

I have been watching in silence the continuous agitation by professionals in particular with regard to the Inland Revenue (Amendment) Act No.45 of 2022 (“2022 Amendment”) and the additional tax which is payable thereunder by individuals. Almost all of the arguments against the increased tax is accompanied by an implied threat that the high tax rates would accelerate the rate of migration of professionals from the country and the dire consequences which would arise therefrom.

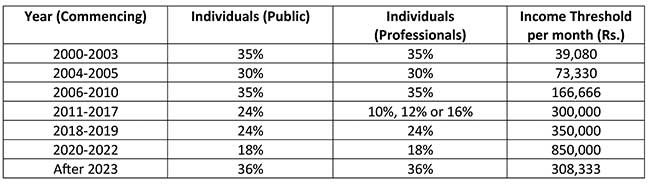

It would be pertinent to analyze the marginal tax rates which have been applicable for individuals from the year 2000 to present and the level of income at which the highest marginal rate would have become applicable. The last column set out above is indicative of the level of income which a person should have on a monthly basis after which he would be liable to pay income tax at the maximum rate specified in the table.

The aforesaid table is clearly indicative that for the period 2000 -2010 the marginal rates of tax were relatively high and therefore, largely comparable to what is going to apply from 2023 onwards. The real problem seems to be that from 2011 onwards, the rate of tax for professionals in particular has fallen down dramatically (other than for 2018/2019) with the result that professionals for all intents and purposes have “forgotten” to pay tax.

The enhanced threshold at which the maximum tax was applicable even at the lower rate increased dramatically from 2020 – 2022 and that seems to be the starting point for any entitlements which are now being spoken of. For example, during this period a person with an income of Rs. 500,000 per month would have only paid about Rs. 10,000 per month as income tax (i.e 2% of income). This is clearly unacceptable. The aforesaid table is clearly indicative that society in general has borne the brunt of this for the benefit of professionals at large very specially between 2011-2017. In my view there is absolutely no justification for professionals to be given any tax concessions which are not available to the other tax paying persons in this country.

I am well aware that in view of inflation in particular, affordability of the tax is in question. The personal reliefs and the level at which the maximum marginal tax rate would apply are also debatable. The real question is as to whether a person having an income of approximately Rs. 300,000 per month should or should not be contributing tax at the rate of 36% on his excess income in the context of large segments of our society being unable to eke out a bare existence for their very survival.

It is easy to say that a large part of government revenue is either wasted or subject to corrupt practices. However, the reality seems to be that major part of government revenue goes towards debt service (i.e interest expenses on borrowing) for which we are all responsible, government salaries and pensions. It is also ironic that persons who are the beneficiaries of these expenses or who have failed miserably in their basic obligation to ensure price stability are also among those who are agitating for a reduction in revenue by way of reduced tax.

It is a fallacy for employees who are subject to Pay-As-You-Earn (PAYE) tax to think that in view of the automatic deduction that they are subject to more tax than others or that other individuals in society who are liable to tax do not pay their tax. The latter pay their tax through the quarterly payment mechanism under the Inland Revenue Act of No.24 of 2017 (“IRA”). The often quoted reason for being reluctant to pay tax is that large parts of society are evading tax and therefore, one should not pay taxes. This in my view is too simple a presumption and it is for any person who says that there are other tax evaders to take the necessary steps to report them specifically to the authorities in a manner that they could share the tax burden of all. However, based on my professional training, pointing to other tax evaders and providing that as a justification for not paying your own taxes is an argument unworthy of a professional.

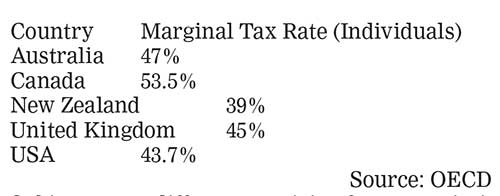

With regard to migration, the following table illustrates the marginal tax rates for individuals in the countries which are often mentioned as being attractive for migration by professionals.

Subject to any differences arising from permissibility of expenses in computing the taxable income, it is clear that any migrant would walk into higher taxes. The migrant would not dare to evade tax in those countries either since the migrant will be summarily thrown out or put behind bars. If a professional wishes to migrate, please do so but do not cite excessive tax in your home country or insufficiency of personal reliefs in computing your taxable income, since any reasonable man in those countries would think that such arguments are hollow to say the least.

We are a Highly Indebted Poor Country (HIPC) and each of us must understand the implications of this. Whichever political party is in power, the government needs revenue. We have exercised our franchise and elected idiots in the past. In 2015 we voted for public sector salary increases which were totally unrealistic which drained the public coffers. In 2019, we the professionals voted for tax cuts, pocketed the additional monies and deprived the State of its due share of revenue. It is now pay-back time for the professionals. In the short term, the increased tax rates should be bearable and in the medium and long term will become palatable.

Increased government revenue is a necessity with current VAT rate of 15% and the marginal income tax rates for individuals and corporates of 36% and 30% being reasonable in a global sense. If any politicians seek your vote or mine on the basis of reducing these tax rates in the absence of alternative concrete revenue generating proposals, let us classify them appropriately as mentioned above and treat them with the contempt which they deserve.

Sri Lanka must urgently strengthen policy consistency, accelerate investment reforms and fully leverage Colombo Port City as a global financial and services hub if it is to emerge as South Asia’s premier destination for foreign direct investment (FDI), business leaders and policymakers said at a high-level Public Relations Association of Sri Lanka (PRASL) forum on Monday.

The discussion, themed “Taking Sri Lanka to the World,” followed an address by internationally renowned scholar Prof. Patrick Mendis, who called for a foreign policy anchored in Sri Lanka’s own identity under what he termed the “Mahaweli Doctrine.”

Delivering the keynote business perspective, Colombo Port City Economic Commission chairman, President’s Counsel Harsha Amarasekara described the Port City as Sri Lanka’s largest public-private partnership and one of the country’s most significant economic transformation projects.

He stressed that unlike many large infrastructure developments, the Port City had not added a single dollar to Sri Lanka’s sovereign debt, with ownership of the reclaimed land remaining entirely with the government of Sri Lanka.

“The Port City is designed to compete globally in high-value services, finance, technology, tourism and innovation. It is not another industrial zone—it is a gateway connecting Sri Lanka to international markets, Amarasekara said.

He said that nine land parcels had already been leased, five major projects were under construction and several additional investments were expected before the end of the year.

The Port City, operating as a Special Economic Zone with transactions permitted in 14 foreign currencies, is targeting multinational corporations seeking regional headquarters, Global Capability Centres (GCCs) and innovation hubs.

Amarasekara said the project’s greatest long-term value would be knowledge transfer, international expertise and high-quality employment opportunities for Sri Lankan professionals.

Former Board of Investment chairman Arjuna Herath warned that Sri Lanka risked losing its long-standing competitive advantage unless it rapidly upgraded its logistics and investment ecosystem.

He noted that nearly 80 percent of Colombo Port’s business depended on transshipment, with India accounting for almost half that volume while aggressively expanding its own port capacity.

“If Sri Lanka fails to invest and improve efficiency, competitors will overtake us, Herath cautioned.

He argued that attracting FDI was no longer simply about offering incentives but about creating a predictable business environment built on policy consistency, regulatory certainty, efficient institutions and investor confidence.

Herath also highlighted Sri Lanka’s global strengths in apparel manufacturing, tyre exports and logistics, saying these industries demonstrated the country’s ability to compete internationally.

International investment strategist Lakshan Madurasinghe, Chief Executive Officer of SolutionsGround (Pvt.) Ltd and former president of the American Chamber of Commerce in Sri Lanka, said Sri Lanka must fundamentally rethink the way it markets itself to global investors.

While welcoming the country’s ambitious investment targets, he noted that actual inflows remained well below expectations.

“The first investment is important. The second, third and fourth investments are what truly measure investor confidence, he said.

Madurasinghe proposed a three-point framework—Positioning, Showing Up and Disruption (PSD)—to reposition Sri Lanka in the global investment marketplace.

He called for a single national investment brand backed by the President, government institutions, overseas missions, the private sector and the Sri Lankan diaspora.

“Every stakeholder must communicate one consistent message to the world. Investors must clearly understand why Sri Lanka is different and why they should choose us, he said.

He also urged authorities to improve investor facilitation, strengthen aftercare services and pursue innovative investment channels, including family offices, strategic partnerships and non-traditional FDI sources.

The forum concluded that Sri Lanka possesses significant structural advantages—including its strategic location, skilled workforce and expanding Port City—but these strengths must be supported by consistent policies, transparent governance and coordinated national promotion if the country is to achieve its ambition of becoming a leading regional investment, financial and services hub.

By Ifham Nizam

The Automobile Association of Ceylon (AAC), the oldest motoring organization established in 1904 and the Galle Services Club (GSC), which is an old sports and recreational body established in 1946, recently entered into a Reciprocal Membership Agreement for the use of facilities of the clubs reciprocally by members on days / hours when the clubs are open for business.

The rationale for the agreement is to enhance members’ benefits of both clubs and to enable them to access a broader range of services, discounts and facilities while encouraging greater participation in community engagement.

It is also intended to explore joint events, training programmes, road safety campaigns and travel related activities that leverage the strengths of each organization.

The Reciprocal Membership Agreement was duly signed and shared between Dhammika Attygalle, President – AAC; Senaka De Silva, President – GSC, at Radison Blue Hotel on July 4, during a sing along programme organized by GSC.

Reaffirming its unmatched leadership and excellence in Sri Lanka’s banking sector, the Commercial Bank of Ceylon has been named Best Bank in Sri Lanka for the 15th consecutive year at the FinanceAsia Awards 2026, while also winning six other prestigious accolades across key areas of banking, the most by Sri Lankan bank.

In addition to being named the country’s Best Bank, Commercial Bank was also honoured as Best Bank for SMEs, Best Bank for Use of Technology, Best Islamic Finance House, Best Sustainable Bank, Best Private Bank and Best Retail Bank in Sri Lanka. Collectively, these accolades underscore the Bank’s leadership across key areas of the financial services spectrum.

Widely regarded as one of the most respected benchmarks in the Asia-Pacific financial services industry, the FinanceAsia Awards recognise institutions that demonstrate excellence in performance, innovation, leadership, customer service and resilience. The 2026 edition marks the 30th edition of these flagship awards, which evaluate banks on financial strength, strategic growth, digital transformation, sustainability initiatives and overall contribution to their respective economies.

“Recognition at globally respected award programmes such as the FinanceAsia Awards further strengthens our standing among leading regional and international peers, while affirming our performance in financial strength, innovation, customer service and sustainability,” said Sanath Manatunge, Managing Director/CEO of Commercial Bank. “This success also enhances stakeholder confidence and reinforces customer trust in the Bank’s ability to deliver consistent value across multiple areas of banking.”

The awards were accepted on behalf of Commercial Bank by Chinthaka Dharmasena, Assistant General Manager – Services, and Krishan Gamage, Deputy General Manager – Information Technology (Operations), at the gala ceremony held on 24th June 2026 in Hong Kong.

Explaining the basis for its selections, FinanceAsia noted that the 2026 awards celebrate institutions that demonstrated determination to deliver desirable outcomes during 2025 through strong commercial and technical acumen, despite operating in complex and evolving market conditions.

The first Sri Lankan bank with a market capitalisation exceeding US$ 1 Bn., and the first bank in the country to be listed among the Top 1000 Banks of the World, Commercial Bank has the highest capital base among all Sri Lankan banks, is the largest private sector lender in Sri Lanka, and the largest lender to the country’s SME sector. Ranked No. 1 in the Business Today Top 40, the Bank is recognised as the most respected and most-awarded bank in Sri Lanka, is a leader in digital innovation and is the country’s first 100% carbon-neutral bank.

Commercial Bank operates more than 270 strategically-located branches and an extensive network of automated machines island-wide, and has the widest international footprint among Sri Lankan banks, with 21 branches in Bangladesh.

President chairs 2027 Pre-Budget talks on Agriculture Ministry

Committee Appointed to investigate unrest at Negombo Prison

Archer, Tongue hand India their biggest T20I defeat

“Badhu Shakthi 2026” National Tax Week begins

Renovated Narahenpita Railway Station reopens to the public under the ‘Dream Destination’ initiative

High-scoring draw gives West Indies rare series win

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News4 days ago

News4 days agoSingapore-based Buddhist monk marks nearly four decades of humanitarian service

-

News5 days ago

News5 days agoFreedom 250: US Embassy celebrates America’s 250th Independence Day through magic of American cinema

-

News5 days ago

News5 days agoCIABOC to question Harak Kata on Rs. 200 mn bribery allegation

-

News6 days ago

News6 days agoSLAF conducts successful rescue mission under UN command in Central African Republic

-

News3 days ago

News3 days agoAI concerned over proposed SL military deployment in Haiti

-

News5 days ago

News5 days agoUNEP support pledged to strengthen Sri Lanka’s Environmental Priorities

-

Business6 days ago

Business6 days ago‘Dialog Air Fibre powers a new era of Ultra Fast Home WiFi’

-

Features4 days ago

Features4 days agoThe NPP’s New Challenge: Balancing Easter Lawfare and Economic Welfare