Business

Breaking free from conventional investment paths; How to make your money work harder – Part II

Contineud from Yesterday

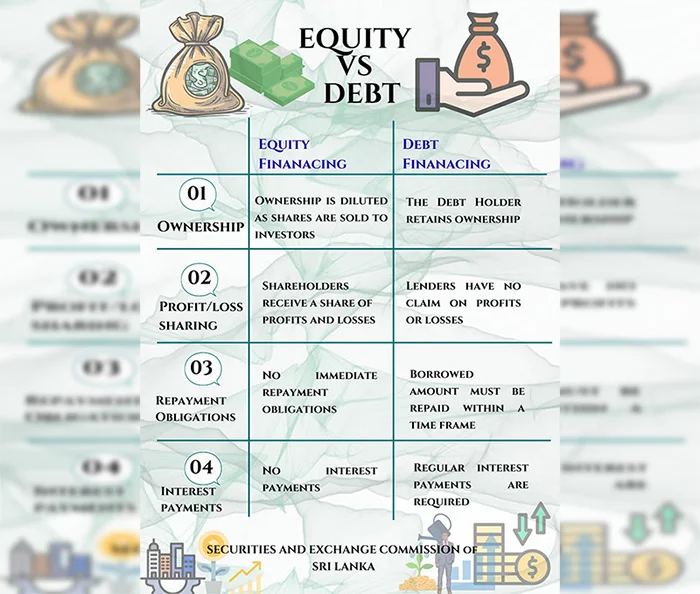

Repayment obligations – No immediate repayment obligations in equity financing. In debt financing however, the borrowed amount must be repaid within a time frame.

Interest payments – In terms of equity financing, there are no interest payments but in debt financing regular interest payments are required.

Debentures Decoded: The Company IOU System

Debentures are essentially formal IOUs that companies give you when you lend them money. What makes them particularly attractive to investors is their predictable nature and security features. They offer fixed returns, meaning you know exactly how much you’ll earn or can predict your return with certainty. Most debentures provide regular income through interest payments made every six months, creating a steady cash flow for investors. Each debenture comes with a specific maturity date when the company must repay the full principal amount you originally lent them. Perhaps most importantly, debenture holders enjoy priority treatment in the company’s capital structure, which means if the company faces financial difficulties, debenture holders get paid before shareholders, providing an additional layer of security for your investment.

The Flip Side: What Could Go Wrong?

Like any investment, debentures come with risks:

Interest Rate Risk – When interest rates rise, existing bond prices fall since newer bonds offer higher yields. Long-term bonds are more sensitive to rate changes than short-term ones. This creates potential capital losses if you need to sell before maturity.

Credit Risk – The borrower may default on interest payments or fail to repay the principal. This is particularly relevant to corporate bonds, high-yield bonds, and emerging market debt. Even government bonds aren’t immune, as sovereign defaults can occur.

Inflation Risk – Fixed-rate debt investments lose purchasing power when inflation exceeds the bond’s yield. Your real return (after inflation) may be negative even if you receive all promised payments.

Liquidity Risk – Potential difficulty in buying or selling a bond at a fair price, especially during periods of market stress. This risk arises because some corporate bonds may have fewer buyers and sellers compared to government bonds, making it harder to execute trades quickly without impacting the price significantly.

Event Risk Corporate restructuring, mergers, natural disasters, or regulatory changes can suddenly impact a borrower’s ability to service debt, even for previously stable issuers.

Prepayment Risk Borrowers may pay off debt early when interest rates fall, forcing you to reinvest at lower rates. This is common with mortgage-backed securities and callable bonds.

Tips on How To Balance The Devil On Your Shoulder; Guide to Risk Management

Build bond ladders with staggered maturities to reduce timing risk and provide regular reinvestment opportunities. Shorter-duration bonds (under 5 years) are less sensitive to rate changes. Consider floating-rate bonds that adjust with interest rate movements.

Diversify across multiple issuers, sectors, and credit ratings rather than concentrating in single borrowers. Research credit fundamentals and consider professional credit analysis for corporate bonds.

The Array of Debt Securities Facilitated; Invest In What You Believe In

The Securities and Exchange Commission of Sri Lanka serves as both the gatekeeper and facilitator of bond investments. Acting like a financial referee, the SEC creates rules and approval processes that allow companies to borrow money from the public through bonds while protecting investors from fraud and misinformation. Their dual role as regulator and facilitator has enabled the development of innovative bond markets, ensuring that when companies want to issue bonds, they must provide complete and honest information about their finances and intentions. Through this careful oversight and facilitation, the SEC has made possible the following bond categories that serve both investor returns and broader societal goals:

Corporate Promises of Economic Affluence: Corporate Bonds

The corporate bond market presents a fascinating risk-reward spectrum. At one end, bonds offered from established corporations with good credit ratings offer reliable returns slightly higher than government securities. At the other end, high-yield or “junk” bonds from less financially stable companies entice investors with premium interest rates to compensate for elevated risk.

The corporate bond market offers remarkable diversity, allowing investors to precisely calibrate their desired balance between safety and yield.

Save the Planet and Make Profit: Unlocking Value Through GSS+ Bonds

GSS+ refers to a category of financial products designed to fund projects with positive environmental and social impacts. The Regulatory Framework for listing and trading the following Bond categories have been enabled at the CSE:

Green Bonds – Green Bonds debt securities specifically designed to fund projects with positive environmental or climate benefits.

Blue Bonds – Blue Bonds are debt securities designed specifically to finance projects related to ocean conservation and sustainable marine activities.

Social Bonds – Social Bonds are debt securities that raise funds specifically for projects delivering positive social outcomes and addressing social challenges. They offer investors a way to generate financial returns while supporting social welfare initiatives.

Sustainability Linked Bonds – Sustainability Linked Bonds differ from the other types of GSS+ Bonds in that their proceeds are not used to finance specific projects but are instead made available for general corporate purposes, with the issuer contractually undertaking to achieve predefined, measurable sustainability targets or Key Performance Indicators (KPIs).

“Faith-Based Finance Finds Home”: Shariah-Compliant Debt Securities

Shariah compliant Debt Securities, commonly known as Sukuk, represent Shariah-compliant financial certificates that embody partial ownership in an underlying asset, usufruct, service, project, business, or investment. Unlike conventional bonds that create debt obligations with interest payments, sukuk are structured as investment certificates that provide returns derived from asset performance rather than interest.

Enabling this product at the CSE is expected to attract previously untapped capital by opening doors to foreign portfolio investments from Shariah seeking investors.

Sri Lanka’s Blooming GSS+ and Faith-Based Bond Market

DFCC Bank Pioneers Green Bond

Sri Lanka’s first Green Bond was issued by the DFCC Bank in September 2024 for a total value of LKR 2.5 billion at a coupon of 12%.

This issue was oversubscribed. In December 2024, the DFCC went on to obtain a dual listing for its Green Bond at the Luxembourg Stock Exchange (LuxSE).

Alliance Finance Issues LKR One Billion Worth of Green Bonds

Alliance Finance Company PLC, a Non-Banking Financial Institution (NBFI) issued LKR 1 billion of Green Bonds in February 2025 at a coupon of 10.75%, which was also oversubscribed.

Sri Lanka’s First Ever Faith Based Bond

Vidullanka, a renewable energy company pioneering Rs. 500 m Sukuk issue (Compliant with Shariah Law) was oversubscribed on the opening day itself.

More GSS+ investment opportunities on the horizon

Several other corporate entities such as Resus Energy PLC and Sarvodhaya Development Finance are in the pipeline for issuing GSS+ Bonds.

“Building Tomorrow Today”: Infrastructure Bonds

The introduction of Infrastructure Bonds marks a significant step toward addressing the nation’s infrastructure financing gap. These specialized debt instruments will channel private capital into critical projects spanning transportation, energy, water, and digital infrastructure.

With extended maturities designed to match the long-term nature of infrastructure assets, these bonds offer investors stable, predictable returns while contributing to national development priorities.

Infrastructure Bonds will create a win-win scenario where investors gain exposure to essential assets with inflation-protected returns, while the country benefits from accelerated infrastructure development.

Capital Fortified: Unlocking value through Basel III Tier 2 Instruments

Basel III-compliant debentures represent a specialized category of debt instruments that adhere to the regulatory standards established by the Basel Committee on Banking Supervision in response to the 2007-2008 global financial crisis. These debentures are designed to strengthen bank capital requirements, stress testing, and market liquidity risk management.

“Endless Opportunities”: Perpetual Bonds

True to its name, Perpetual Bonds are debt securities with no maturity date and pays interest indefinitely. These instruments offer unique advantages for both issuers seeking stable long-term funding and investors looking for consistent income streams.

Unlike conventional bonds, perpetuals remain outstanding until the issuer chooses to redeem them, typically after a specified initial period.

Perpetual Bonds represent financial innovation at its finest. They provide corporates with quasi-equity financing without diluting ownership, while investors benefit from higher yields compared to traditional fixed-income products.

“Higher Risk, Higher Reward”: High-Yield Bonds

Rounding out the new offerings are High-Yield Bonds, sometimes known as “junk bonds,” which carry higher interest rates to compensate for their greater risk profile. These instruments typically come from issuers with lower credit ratings or newer enterprises without established credit histories.

Market participants have welcomed the addition, noting it completes the CSE’s fixed-income ecosystem by catering to investors with more aggressive risk appetites.

High-yield bonds fill a crucial gap in our market. They offer potentially attractive returns in a low-interest environment and provide companies that might not qualify for investment-grade ratings with vital access to capital. Currently this is facilitated for entities regulated by the CBSL or the Insurance Regulatory Commission of Sri Lanka (IRCSL)

Why Capital Markets Matter: The Win-Win Story

For Companies Raising Money:

Cheaper Funding: Instead of paying high bank interest rates, companies can often raise money more cheaply through capital markets.

No Collateral Hassles: Unlike bank loans that require mortgaging property, companies can raise funds based on their business prospects.

Flexibility: They can choose between giving away ownership (equity) or borrowing (debt) based on their needs.

Growth Capital: Access to large amounts of money helps companies expand, hire more people, and in turn contribute to economic growth.

For Everyday Investors:

Better Returns: Instead of earning a lesser return from bank deposits, you might be able to earn significantly higher returns in the capital market

Choice and Control: You decide which companies to support with your money.

Wealth Building: Over time, successful investments can significantly grow your wealth.

Economic Participation: You become part of Sri Lanka’s economic growth story.

The Bigger Picture: Building Tomorrow’s Sri Lanka

Capital markets aren’t just about making money – they’re about building the future. When you invest in a renewable energy company’s debenture, you’re funding clean power for Sri Lanka. When you buy shares in a tech startup, you’re supporting innovation and job creation.

Getting Started: Your First Steps

Ready to explore capital markets? Start small:

Learn the basics through free regulatory sources like Securities and Exchange Commission of Sri Lanka

Open a trading account with a licensed stockbroker

Start with blue-chip companies – established firms with good track records

Diversify your investments – don’t put all eggs in one basket

Think long-term – capital markets reward patience

Still feeling apprehensive? Try Unit Trusts.

Unit Trust Funds are a collective investment scheme that is a pooling vehicle of your funds, offering professionally managed investment pools with various risk profiles suitable for unsophisticated investors.

Minimum investment begins from as low as LKR 1,000.00. Risk level varies based on type of the Scheme who creates a diversified portfolio based on the fund’s parameters to earn a return.

Then your money is used by professional fund managers who know what they’re doing. They take everyone’s money and buy a mix of different investments – like shares in companies, government bonds, and other financial assets.

Steps to follow;

Choose a licensed managing company and open a unit trust account

Open your account with as little as Rs.1000

Choose the Scheme – Once your account is open, you need to choose a fund to invest in. You can choose from a range of funds such as Growth funds, Income funds, Balanced funds, Money Market funds, Sector Funds and Index Funds. Each fund has different risks and returns, so you need to decide which is the best fit for your goals and risk appetite.

Monitor your investment

The beauty of unit trusts is their simplicity – investors receive the benefit of professional management without needing to be a financial expert.

Finally, it’s important to remember, all investments carry risks. Never invest money you can’t afford to lose and always do your homework before making investment decisions.

Capital markets have democratized finance in Sri Lanka, giving everyone a chance to participate in the country’s economic growth, offering opportunities to grow your wealth while supporting businesses that create jobs and drive progress.

To be Continued

by Securities and Exchange Commission

of Sri Lanka

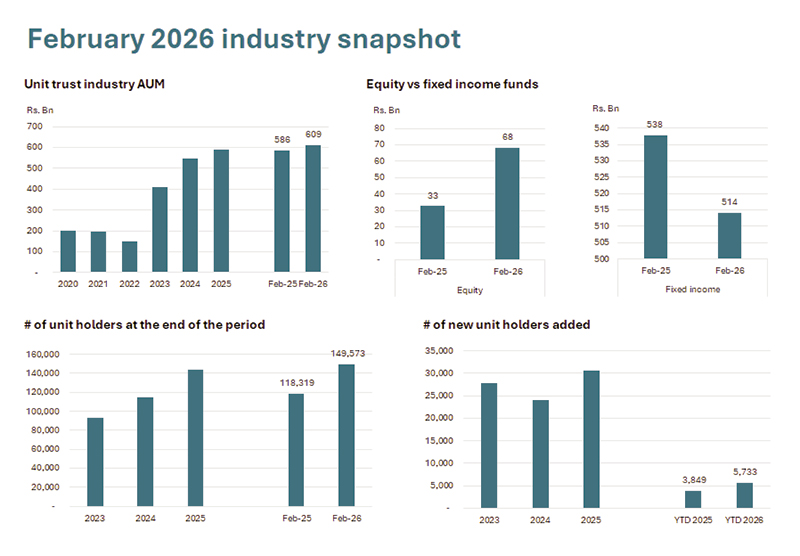

The unit trust industry of Sri Lanka reported assets under management (AUM) of Rs. 609 Bn, up 4.0% year-over-year and largely unchanged compared to the previous month. These assets are currently managed across 85 funds by 16 management companies.

AUM was supported by flows to equity-related funds, which doubled year-over-year to Rs. 68 Bn. Fixed income funds, on the other hand, declined by 4.4% year-over-year. In addition, since 2025, there has been a gradual shift from shorter-term instruments towards more medium to longer-term investment options, with inflows into open-ended income funds, open-ended equity index/sector funds, and open-ended growth funds (equity), alongside a decline in flows to money market funds.

During the month, the industry added 2,623 new unit holders, up 69.8% year-over-year, bringing the total number of unit trust investors to 149,573, which represents a 26.4% increase year-over-year.

Commenting on the February industry results, newly elected President of the Unit Trust Association of Sri Lanka (UTASL) and Director/CEO of Senfin Asset Management, Jeevan Sukumaran, stated: “The industry’s performance as at end-February 2026 reflects a degree of consistency, with continued activity in equity-related funds. We are also observing a gradual shift towards more balanced investment allocations across fund categories.”

He further noted: “As we move forward, our priority will be to build on this momentum by enhancing investor awareness, broadening access to unit trust products, and working closely with regulators and market participants to strengthen further the industry’s depth, resilience and long-term relevance within Sri Lanka’s financial landscape. In a dynamic market environment, maintaining a disciplined, long-term approach whilst reinforcing the resilience of the unit trust structure, with its focus on diversification and professional fund management, will remain key priorities for the industry.”

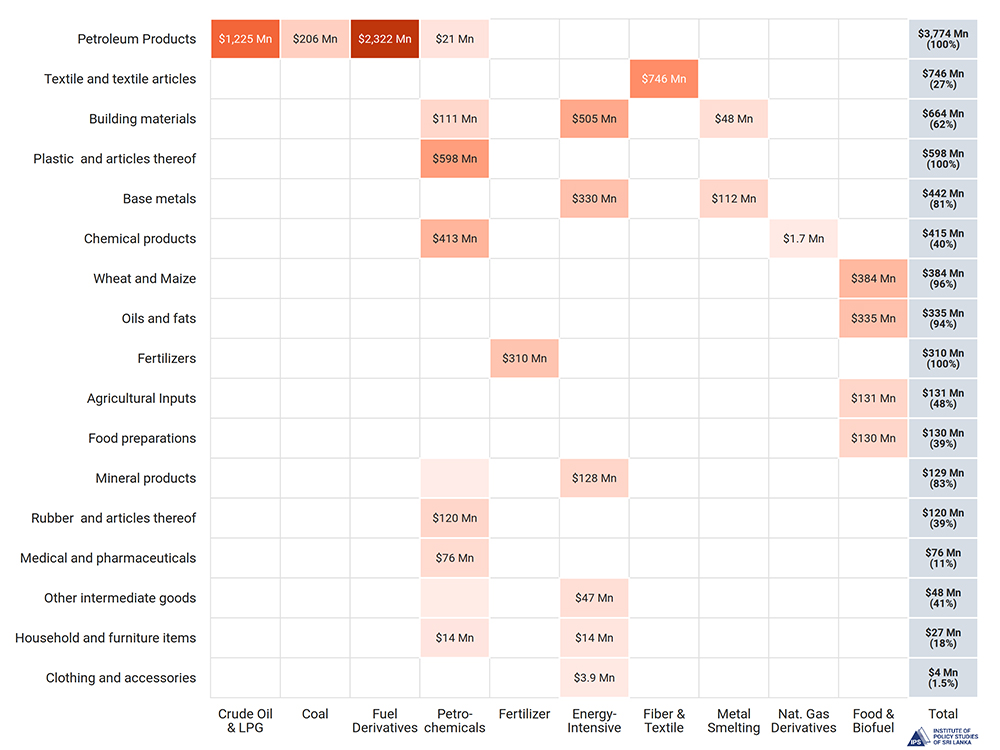

The supply shock in the commodity market directly affects 39.3% of imports of Sri Lanka, or USD 8.3 Bn, across 951 products.

The price shock extends beyond petroleum and petrochemicals to nitrogenous fertiliser, biodiesel alternatives like palm oil, and food, exerting pressure on food prices.

Currently, price pass-through and demand management are the best options, while easing regulatory barriers, such as licensing schemes, are necessary to ensure food security.

The closure of the Strait of Hormuz has unsettled global energy markets. According to the International Energy Agency (IEA), 20 Mn barrels of crude oil products were transported through the Strait in 2025, which accounted for a quarter of the world’s daily energy needs. The closure has driven fuel futures higher, with the Brent futures reaching USD 112 per barrel on 19 March 2026 . A phenomenon called “backwardation” is clearly visible in the fuel market, implying that spot market prices for “physical” fuel are significantly higher than futures prices for “paper” fuel.

The economic impact of the energy price shock can impact Sri Lanka through various channels, and if hostilities in oil-producing regions continue, the effects will intensify over time. The immediate impact stems from rising commodity markets, including not only fuel but also biodiesel feedstocks such as soybean, canola, and palm oil; petrochemicals; fertilisers that use liquefied natural gas (LNG) as a feedstock; and aluminium and base metals, which demand significant energy for smelting.

Against this background, this article examines the future prevalence of high fuel prices, Sri Lanka’s vulnerability, the impacts on foreign exchange outflows, and the necessary policy measures to mitigate the adverse effects.

High Fuel Prices and the Effects on Sri Lanka’s Import Basket

Given that a quarter of the global energy supply is disrupted, the current energy shock is unprecedented. After the Russian invasion of Ukraine, fuel prices rose above USD 100 per barrel in 2022, and they remained there for roughly 90 days. The high energy cost resulted in a high inflation episode in 2022-2023. As shown in Figure 2, by the end of 2023, energy prices had returned to and stabilised around the pre-invasion level. Notably, Russia’s share of the global energy market was about 11%, while the Hormuz crisis accounts directly for around a quarter of the global energy supply. The energy infrastructure damage so far has also been significant. Thus, high fuel prices may prevail if there is no swift resolution to the crisis. Sri Lanka should consider such a possibility.

Based on 2025 import data, 39.3% of Sri Lanka’s imports, or USD 8.3 Bn, are directly exposed to rising commodity prices. Of this, USD 3.7 Bn are petroleum products, including crude oil, liquid petroleum gas (LPG) and refined fuel. Currently, the fuel price shock is 38.9% when forward-curve movements in Brent futures are factored in. Additionally, energy-intensive base metals and crude oil-based products like plastics and synthetic fibres will be expensive in the world market. These are important intermediate imports for Sri Lanka’s manufacturing sector.

Since natural gas is a key raw material for urea, increasing urea prices, in turn, raises the costs of related agricultural commodities like wheat. As shown in Figure 3, Sri Lanka spent USD 310.1 Mn on fertiliser in 2025, while the import bill for wheat and maize was USD 384.1 Mn. The global increase in fuel prices has boosted demand for biodiesel feedstocks, putting pressure on oil and fat prices, including palm oil used for cooking. Soybean meal and maize are used in poultry feed, so price hikes will have direct nutritional effects on households, mainly through reduced protein intake.

If high prices persist, Sri Lanka’s import bill is likely to increase, as the price response can be inelastic in the short run, which is common for essential commodities with few substitutes. Using 2025 monthly import values and assuming a future fuel price shock equal to the futures market-reflected percentage increase, it is estimated that Sri Lanka’s import bill could rise by USD 1.9 Bn. This means Sri Lanka will incur a 23% increase in imports over the baseline of USD 8.3 Bn. However, the estimated value is at the upper-bound as it is assumed that Sri Lanka would consume the same quantity as in 2025. If high prices persist, adjustments across the entire economy will inevitably necessitate changes in quantity. Demand will contract when a high import price is passed on to consumers. Such a response can be quantified using product-level import demand elasticities. If higher prices lead to reduced demand, Sri Lanka’s import bill could fall by about USD 608 Mn relative to the baseline. However, such a reduction would mainly occur if energy use adjusts in line with longterm demand patterns. This estimate also does not account for wider, economywide adjustments to higher import prices. Under a full demandadjustment scenario, the overall effect would therefore be a net reduction of USD 608 Mn.

Policy Options for Sri Lanka

Although inflationary pressures remain a serious concern for Sri Lanka in the post-Hormuz crisis period, a transparent pass-through of the supply shock to price levels is a suitable policy. While memories of recent high-inflation episodes are still vivid, the Hormuz crisis and the 2022-2024 sovereign debt crises are fundamentally different events. The elevated inflation during 2022-2024 was driven by structural changes in fiscal and monetary policy. Policy implementations such as cost-reflective utility pricing, energy price pass-through, and a floating exchange rate were introduced sequentially, leading to higher inflation. The economy was moving toward reforms to address multiple distortions introduced by a low interest rate and a controlled exchange rate regime.

In the current crisis, significant price shocks from corrective policies are not anticipated. Instead, inflationary pressure resulting from the Hormuz disruption is an external, supply-side shock primarily transmitted through the prices of imported fuel, rather than via domestic policy reversals. Since high airfares and rising shipping fuel costs may impact foreign exchange inflows, managing the reserve position becomes crucial. In this context, restricting fuel consumption is essential while ensuring available fuel is allocated primarily for industrial use.

A fiscal response that suppresses the price signal, such as reducing taxes on certain imported goods, might not be suitable at the moment, as it could boost demand for very costly imported products like fuel. The analysis shows that the import bill can rise substantially if a high price prevails without a quantity adjustment. Notably, under the current framework, such import demands are transmitted to the exchange rate, which can further increase inflationary pressures. However, Sri Lanka should consider easing import licensing schemes for animal and poultry raw materials as global market prices rise, to facilitate imports and secure food supply. Temporarily removing the existing Special Commodity Levy (SCL) on corn imports should also be considered. These products incur small reserve outflows but play a larger role in the country’s protein nutrition.

By Dr Asanka Wijesinghe, Research

Fellow, Institute of Policy Studies of Sri Lanka

The Australian High Commissioner, Matthew Duckworth, hosted a pivotal ‘Thought Leadership’ educational session titled ‘ConnectEd” at his residence in Colombo recently, focusing on disaster recovery efforts following Cyclone Ditwah. This event was part of a series organized by the Australian Trade, Investment & Education division, aimed at fostering discussion on pressing issues in Sri Lanka.

The discussion aimed to reflect this ambition, inviting participants to share their insights and engage with expert speakers. Attendees were encouraged to voice their questions and contribute their perspectives, fostering a collaborative environment for learning and growth.

“As we approach 80 years of bilateral relations between Australia and Sri Lanka, this exchange highlights the enduring value of our partnership built on dialogue and trust. Today, we focus on recovery and rebuilding in the aftermath of Cyclone Ditwah. Effective recovery requires collaboration across various sectors to ensure that we not only address immediate needs but also build resilience over time. I encourage everyone here to actively engage in our discussions, as your expertise is invaluable to shaping a stronger future together, the Australian High Commissioner said in his opening remarks at the event.

He further noted that “this session is being held under Chatham House Rules, which I hope fosters a frank, open, and constructive exchange. A vital aspect here is uniting Australian and Sri Lankan thought leaders, reflecting our longstanding partnership and aligning discussions with Sri Lanka’s broader priorities and ambitions”.

‘ConnectEd’ event was coordinated by Ms. Sandy Seneviratne, Director of Education for the Australian Government based in Colombo. The session brought together key stakeholders to address the challenges and strategies involved in recovering from natural disasters. The dialogue was enriched by insights from notable panelists, Prof. (Ms.) Udayangani Kulatunga, Department of Building Economics at the University of Moratuwa, Sri Lanka, specializing in disaster risk reduction, construction management, and performance measurement and Professor Pat Rajeev, Chair, Department of Civil and Construction Engineering from Swinburne University of Technology in Australia. Lauren Nicholson, Second Secretary for Development at the Australian High Commission moderated the session.

By Claude Gunasekera

Courtesy call by the Heads of Mission- Designate on Prime Minister

Three dead after helicopter crash in Hawaii

Woods charged with driving under influence after crash

Showers may occur at a few places in the Rathnapura, Kaluthara, Galle, and Matara districts during the evening or night

SC finds Keheliya, others, guilty of violating FRs of public through corrupt drug procurement deal

Sajith nudges govt. to follow India’s example in giving relief to consumers by slashing taxes on fuel

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News4 days ago

News4 days agoSenior citizens above 70 years to receive March allowances on Thursday (26)

-

Features21 hours ago

Features21 hours agoA World Order in Crisis: War, Power, and Resistance

-

Features6 days ago

Features6 days agoTrincomalee oil tank farm: An engineering marvel

-

News2 days ago

News2 days agoEnergy Minister indicted on corruption charges ahead of no-faith motion against him

-

News3 days ago

News3 days agoUS dodges question on AKD’s claim SL denied permission for military aircraft to land

-

Features6 days ago

Features6 days agoThe scientist who was finally heard

-

Business3 days ago

Business3 days agoDialog Unveils Dialog Play Mini with Netflix and Apple TV

-

Sports2 days ago

Sports2 days agoSLC to hold EGM in April