Features

Sri Lanka’s Debt Restructuring Roadmap: Following the Evidence

By Dr Dushni Weerakoon

Debt restructuring is fundamentally about allocating the associated economic costs to someone. The onus is typically on the debtor country to secure participation from its creditors, applying comparable treatment to all. As with all negotiations, the level and modalities of relief will always be subject to some degree of controversy. Sri Lanka’s recently gazetted domestic debt restructuring (DDR) exercise too has drawn expressions of both support and criticism. Overall though, negotiations have to be framed within certain desired outcomes to minimize costs to the economy. To this end, Sri Lanka’s negotiating stance dovetails neatly with crucial research evidence.

A restructuring process, whether pre-emptive or post-default, imposes significant output costs. For a debtor country to minimize these, some notable findings are:

Output losses are higher in post-default restructuring.When defaults are accompanied by a banking crisis, the fall in output is particularly large.

Even in a post-default setting, output costs can be reduced the quicker the debtor country is able to reach an agreement with its creditors.The size of creditor losses (haircuts) is among the best predictors of participation rates on bond restructuring.

To begin with, there was no real appetite to include a DDR in Sri Lanka’s case, especially in view of the substantial real erosion in value to debt holders as inflation spiraled. But, as opening gambits commenced with external creditors, the bondholder group’s request that ‘domestic debt is reorganized in a manner that both ensures debt sustainability and safeguards financial stability’ could not be ignored if only to avoid an impasse. Sri Lanka has limited room to circumvent a DDR altogether. As a middle-income country, the inclusion of domestic debt optimization is implicitly encouraged in the IMF’s debt sustainability framework (DSF) for market-access countries. It focuses on the total stock of public debt but is avoided by low-income countries where the applicable DSF focuses only on external public debt.

Having opened the door to a DDR, there would have been very real concerns that the combination of skyrocketing inflation and financial fragility would test the banking sector’s resilience to deal with a DDR. Figures on capital adequacy and asset quality (with the non-performing loan ratio on stage three loans rising from 5.2% in 2020 to 11.3% in 2022) and exposure to restructuring the country’s international sovereign bonds (ISBs) meant the stakes were high. When times are uncertain, a herd mentality will rule, and this is to be avoided at all costs.

Another element in a DDR is that there are negative externalities that need to be internalised – i.e. there may be direct costs to a country’s financial sector from a DDR, such as recapitalization and these have to be taken on board. This is particularly so where there is a strong link between the sovereign and its financial system. In setting aside resources to ensure financial system stability, the anticipated fiscal benefits of a DDR can potentially reduce. Thus, on both counts, ring-fencing the banking sector to avert a far more damaging economic crisis and deeper output losses has been the first step in Sri Lanka’s approach.

Having left out the banking sector, the economic cost appears to have been disproportionately directed at the savings of workers contributing to pension funds. Private bondholders have been exempted denying ‘comparable treatment’ while the captive nature of the Employees Provident Fund (EPF), managed by the Central Bank of Sri Lanka (CBSL), means there has been no attempt to ‘secure participation’.

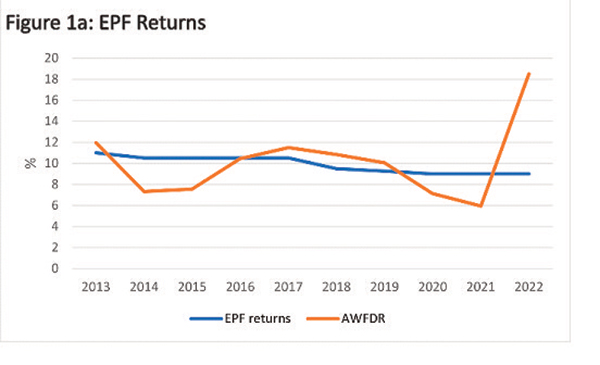

Sri Lanka’s DDR treatment in effect is an example of the considerable degree of influence that a sovereign can exert over domestic legal and regulatory frameworks, unlike that of an external debt restructuring (EDR). Under the terms, pension funds are required to opt for a 30% haircut or be liable for higher taxation at 30% instead of the prevailing 14%. For EPF savers, there is the only assurance of receiving a 9% return in the long-term for a fund that has often performed below par even against the simplest alternative instrument that an average saver may look at, such as one-year fixed deposits (Figure 1a). Where there has been a substantial erosion of real savings from a crisis-induced economic environment, this is scant consolation for workers. The premise of a return to single-digit inflation merely means that price increases have slowed from the previous exorbitant high levels, but the erosion of the value of savings remains very real.

The second step of the negotiating process is to bring as many of Sri Lanka’s external creditors on board as quickly as possible. Having complied with the bondholder group’s request on including a DDR, comparable treatment is being offered by way of a 30% haircut on EDR too. As a bilateral creditor, China’s preference globally is for deferral rather than reduction. But merely pushing repayments down the line with maturity extensions (and some coupon adjustments) still leaves Sri Lanka at the risk of being permanently illiquid and, therefore, vulnerable to repeat short-term crises. Clearly, the deeper the haircut, the more sustainable the debt becomes, but negotiations will likely drag on. A complex creditor group and geo-political wrangling add to these risks. Ecuador, a middle-income country, came to an agreement with its bondholders to a haircut of 9% on USD 17.4 billion in 2020, with a high 98% of bondholders agreeing to the deal. China persisted with maturity extensions and coupon adjustments.

Corralling in the bilateral creditors will require more diplomatic persuasion than economic analysis. China’s recently concluded deal with Zambia to restructure USD 4.2 billion of loans under an initiative driven by the G20 Framework for low-income countries pushed back repayments and accommodated interest rate cuts. This follows on from its deal with Ecuador a year earlier that included maturity extensions and interest rate adjustments on debts worth USD 4.4 billion. There are two key arguments put forward by China for not taking losses in debt restructurings: first, that its loans are development-oriented, tied to projects that generate revenues for the recipients, and second, that multilateral banks should also participate, instead of the current preferred status of having their loans repaid in full. In many ways, Sri Lanka will be a test case on these issues.

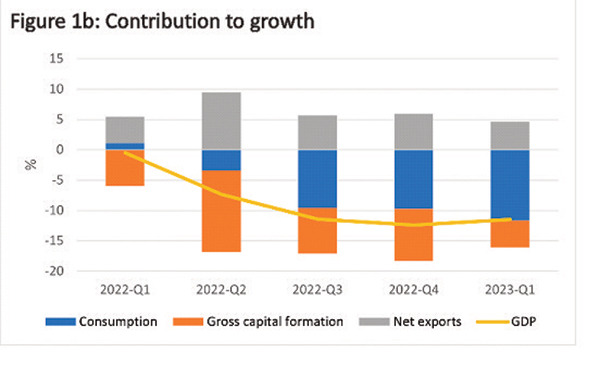

The expected deceleration in the contraction of Sri Lanka’s economic output in the coming months is only the start to claw back lost output. This too is under threat. As domestic consumption faltered, net exports were the only positive driver of growth in recent quarters, but there are concerning signs of a slowdown (Figure 1b). In the event, it is even more probable that the allocation of costs associated with debt negotiations will be weighed and measured against the need to get an overall deal done as quickly as possible to support Sri Lanka’s slow-burn economic recovery.

Link to blog: https://www.ips.lk/talkingeconomics/2023/07/18/sri-lankas-debt-restructuring-roadmap-following-the-evidence/

About the Author:

Dushni Weerakoon is IPS’ Executive Director and Head of its Macroeconomic Policy research. She has nearly three decades of experience at IPS and functioned as its Deputy Director from 2005 to 2017. Since joining IPS in 1994, her research and publications have covered areas related to regional trade integration, macroeconomic policy and international economics. She has extensive experience working in policy development committees and official delegations of the Government of Sri Lanka. She holds a PhD in Economics from the University of Manchester.

The West Asian peace effort continues waveringly amid uncertainties. The world could be considered as having ‘some breathing space’ currently in this tangled situation on account of a dip in oil prices but whether such relief would be of a long term nature is left to be seen.

The West Asian peace effort continues waveringly amid uncertainties. The world could be considered as having ‘some breathing space’ currently in this tangled situation on account of a dip in oil prices but whether such relief would be of a long term nature is left to be seen.

Meanwhile, some vital ‘details’ in the peace process are continuing to hobble it. One such factor is the nuclear issue. While US President Donald Trump is on record that Iran’s purported nuclear programme from now on will be monitored by the International Atomic Energy Agency (IAEA), this assertion is being denied by the Iranian authorities who indicate that Iran will be coming under no such regime. That is, Iran will be answerable to no one with regard to its legitimate right to defend itself.

Accordingly, an early closure to the nuclear question could not be expected and the furthering of peace in the region hinges on the principal sides being of one mind on the issue. Moreover, toll-free shipping through the Strait of Hormuz is proving to be a bone of contention between the warring sides.

However, perhaps going largely unnoticed in the Middle East region are identity questions of considerable magnitude that have stood in the way of the region making some headway towards a peace settlement and which would continue to undermine such a process going forward. Identity, or a group’s self conception, is by far the most intractable of the factors in the conflict and the main sides would do well to manage it effectively before long.

US Vice President J.D. Vance, as pointed out in this column last week, fired one of the first salvos in this regard in the current peace effort. He reportedly said: ‘Regional peace and stability includes stopping the funding of “terrorist organizations” .’ He probably had in mind the Hezbollah organization which is funded and armed by Iran but, needless to say, the latter would reject this statement out of hand because it does not see the Hezbollah as terroristic in orientation.

Accordingly, the tangled issue of ‘who is a terrorist?’ would recur to hamper the West Asian peace bid. An important corollary to this matter is that Middle Eastern militants would be branding US administrations as terroristic considering the humanly costly military interventions undertaken by the latter over the decades in the world’s war zones.

It is difficult to see the main sides taking up the issue of terror and arriving at a common understanding on the problem over the next couple of months in their peace deliberations but the unresolved question could be expected to be the proverbial ‘elephant in the room’ that could even wear the sides down. Accordingly, ‘quick fixes’ to the Middle East imbroglio would need to be ruled out.

However, paring down terror to its essentials, it needs to be found that in contemporary times it is identity and issues growing out of it that keep the question alive and render it intractable. In fact the problem should be seen as igniting and sustaining a multiplicity of conflicts world wide.

So pervasive are identity questions that they are seen by some as having played a role in leading to the recent resignation of Keir Starmer as UK Prime Minister. Among other things, the latter is seen as having been incapable of managing migration related issues besides falling short in strengthening domestic social cohesion.

Identity issues came to a head in the UK in the form of the recent anti-immigrant riots in Northern Ireland. Clearly, some immigrants continue to be seen as aliens and parasitic in nature in some parts of the UK by jingoistic elements. Thus is ignited anti-foreigner violence.

That said, some of the most laudable measures for the promotion of peaceful race relations are found in the UK today. The latter’s race relations legislation could be seen as constituting a model for the rest of the world and needs to be studied and adopted by particularly the global South where identity conflicts are rampant.

Unfortunately, racial amity is not being considered a priority by the Trump administration. Under the latter immigrants are being seen by supremacist whites as the archetypal ‘Other’ who should be violently shunned. Accordingly, social cohesion in the US too is being steadily undermined and stepped-up race hate in the country shouldn’t come as a surprise.

In the West Asian region, archetypal ‘Othering’ could prove particularly pernicious and destructive. It could lead to the unraveling of the current peace talks between the adversaries and needs to be addressed by them if the negotiations are to prove productive.

For far too long the West and Israel have been viewed as archetypal enemies by Iran and its supporters. On the other hand, Palestinian militants have been habitually seen by the Far Right in the US and by hard line Israelis as sworn enemies who are best eliminated. These seemingly unresolvable divides in the Middle East could bring down the present negotiatory process.

Even if the present round of mediated negotiations between the US and Iran lead to a substantive cessation of hostilities in West Asia, the divisive mindsets of the prime antagonists, that is, the US and its ally Israel on the one side and Iran and its supportive militant groups on the other, would need to be changed for the better if enduring peace is to be given a chance. That is, mindsets would need to be transformed on both sides of the divide from mutual hostility to mutual amicability. No doubt, a long-gestation process.

It cannot be stressed enough that those mediating in this long-running conflict, themselves need to approach peace-making with unbiased minds. It needs to be realized, for example, that Israel too has been ‘hurting’ badly in this conflict over the decades to the degree to which the Palestinian side has been victimized cruelly, dispossessed and divested of dignity.

Any negotiated peaceful settlement should seek to address this persistent mindset malaise as well and turn enmity into amicability. An equitable solution that addresses the lingering grievances of both sides could lay the basis for this process of ‘Turning Spears into Ploughshares.’

‘Land and Bread’ have been at the heart of the Middle East conflict over the decades or even centuries. An equitable solution should provide these assets in equal measure for both sides. There is no getting away from the ‘Two State Solution’.

Long End Street is not a summation of Short End Streets. Eighteen short-term crises and no long-term growth in sight!

For quite some time, there has been no agency of government dealing with long-term economic and social policy questions. Nor have universities been of any help. There has been a National Planning Department in the Ministry of Finance but we have not seen any worthwhile reports from them. M. D. H. Jayawardena, in 1956, presented in Parliament the Six-Year Programme of Investment. Soloman Bandaranaike established a National Planning Council and a Planning Department, with Princy Siriwardena as its Director. They wrote the Ten-Year Plan, better known for its readability than its depth of analysis or policy content. Ten years or so later Dudley Senanayake established a Ministry of Planning and Employment with Gamani Corea (later of high international repute) as its Permanent Secretary. The Ministry was responsible for some useful analytical work and the development of a bureaucracy responsible for plan implementation. The latter was the work of a brilliant member of the Ceylon Civil Service, Godfrey Gunatilleke, who also worked in the Ministry. The major pre-occupation of the Ministry turned out to be the annual government budget and the management of direly scarce foreign exchange, all short term considerations. They set up a bureaucratic mechanism to evaluate capital expenditure in the government budget. The Ministry won plaudits for its Foreign Exchange Budget, some analytical wok on the economy, including population projections as well as education, in both schools and universities. As the 1970s wore on, planning earned a bad press and the new government of 1971 disbanded most of that and created a Department of National Planning in the Ministry of Finance, which survives to date.

A part of the purpose of this narrative has been to bring out that, all along, government has had no outfit of economists and sociologists whose job was to study long term changes in our society and the economy and in the rest of the world and propose solutions for consideration by governments. (A brilliant exception was the work on education, that was directed by Jinapala Alles, who had graduated in chemistry and was a fast learner and was at great ease with numbers. He was also an effortless leader of a small team of self-selected competent and enthusiastic public servants.) The government depended on the Central Bank for advice on long term development of the economy. Princy Siriwardena was seconded for service in the Planning Secretariat; similarly, Gamani Corea was from the Bank. Later, he was replaced with H.A.de S. Gunasekera, likely the most brilliant economics teacher in the University of Ceylon. He taught monetary economics, essentially short term. (His favourite economist Keynes famously wrote, “In the long run we are all dead”.)

When the Ministry of Planning and Employment was established in 1965, government plundered the Central Bank to staff it: Gamani Corea, R. M. Seneviratne, N. Ramachandran, Nihal Kappagoda and G. Usvatte-aratchi. Later, W. M. Tillekeratne and A. S. Jayawardena both long term employees of the Central Bank, were appointed as the chief economist of government. Jayawardena still later became the Governor of the Bank. Several other employees of the Bank, including J. B. Kelegama, P. B. Karandawela, P. B. Jayasundera worked at high levels in successive governments and that practice continued when Mahinda Siriwardena became the Secretary to the Ministry of Finance when Anura Dissanayake became the Minister of Finance. It is mysterious that the government saw no need for specialist advisers who would identify long term economic and social problems and solutions therefor, look out for markets and technology and warn of impending pitfalls, in contrast to our mighty neighbour which had a Planning Commission that handled long term problems and a Central Bank which had learnt to handle masterly, monetary problems.

Pitambar Pant, Montek Singh Ahluwalia, Manmohan Singh, I. G. Patel and Raghu Ram Rajan were most distinguished economics policymakers and central bankers. Japan benefited greatly from the work of MITI. So did Korea from its counterpart. This is not to argue that had there been an outfit of that sort, Sri Lanka would now be rich but to warn that the Central Bank is neither equipped nor fit to fight those battles. If you scan the Central Bank Act of 2023, you will find stabilisation the most frequently recurring theme. Clause 6 reads ‘The primary object (objective?) of the Central Bank shall be to achieve and maintain domestic price stability.’ The most generous reading that the Bank may have anything to do with economic development is in Clause 6 (4) ‘In pursuing the primary object (objective?), the Central Bank shall take into account, inter alia, the stabilisation of output towards its potential level.’ Lawyers may have a field day with that and economists may beg for its meaning.

Amarananda Jayawardena was the last Governor of the Central Bank who had understood that the central bank was equipped to handle short term problems and that not always valiantly, and that it had neither the tools nor the resources to plan and engineer long term development. As Governor, he did not speak for the government on long term economic and social problems, although prior to assuming duties as Governor of the Bank, he had been the chief economist of the government. Jayawardena knew all too well the nature of the tools and the resources he had and how far he could confidently aim and shoot. It was simply silly to produce a Five-year Road Map (no matter how colourful the accompanying graphics), when a central bank mainly used transactions in the short-term financial assets market to move interest rates and the demand for money. The Bank of England, for most of the 20th century, used Commercial Paper with two ‘good names’ at its Discount Window. Short-term and long-term rates of interest, normally, behave in a predictable relationship, although occasionally, and in volatile times, that relationship may become inverted. (I am not well read on recent Fed and the Riks Bank market operations.)

The economists at the Central Bank are experts in monetary policy and are rarely knowledgeable about economic growth. An exception was S. B. D. de Silva and he found writing a half page note to the Centra Bank Bulletin (monthly) stultifying. He left the Bank quite young and continued studying economics until the very end of his life. As undergraduates they may have read on economic growth and development but as professionals in the central bank, it is unlikely that they kept working on problems in that area. They may also have learned, some time, that there has been no central bank credited with spearheading economic development in any country. Therefore, to pretend that they can advise the government on economic planning, is a hobby which they would be wise to desist from.

We did a splendid job of saving our new born children and their mothers as indicated in low infant mortality and maternal mortality rates. We scored an even more resounding victory in educating all our children. If we have any claim to any civilizing missions in the 20th century, these two stand out. Beside them, we have been mostly failures. The economy has advanced only laggardly. It has miserably failed to exploit excellent opportunities to sell in burgeoning markets, output employing a healthy and educated labour force. Japan, South Korea, China, Vietnam, south India, Ethiopia, Rwanda and several other countries, all (except Japan) late comers to the game compared to Sri Lanka, succeeded in doing just that. It is wrong to blame governments alone for poor economic growth, as many do. Most economic activity in this country is run by the private sector and leaders there have made poor use of opportunities.

When ministers of government and its employers collect bribes, private sector persons pay bribes. The markedly rapid economic growth in Andhra Pradesh, Telangana, Karnataka, Tamil Nadu and Keralam and poor growth in Madhya Pradesh, Uttar Pradesh, Bihar and many others in the north east are under the same central government dispensation, sharply pointing to differences in the quality of business leadership in the two groups. ‘Big business’ here run betting shops, supermarkets, hospitals, import and market household equipment, banks and insurance companies and, most ambitiously maintain construction companies. (In the widely watched IPL cricket matches 2026, Sri Lanka advertised regularly a Betting Centre!) Tourism in this country is the business of small-scale enterprises with low productivity. The ubiquitous kade with a stock-in-trade of less than one hundred thousand rupees, borrowed from a relative or a friend, is a sign of rampant unemployment and not of budding entrepreneurship. When you go to consult a doctor in a private hospital in Colombo and wait endless hours, count the number of men and women employees idling, supervised by a proportionately large number of idling supervisors. Where are the large-scale manufacturing and service companies, selling the world over, where economies of scale abound in the 21st century? So far as I recall, there has been no Initial Public Offering (IPO) of shares in the Colombo Stock Market during the last 7 years. Nor have multinational companies established here any large factories or offices.

Is the air we breathe deathly to enterprise?

by Usvatte-aratchi

By the time Sir Keir Rodney Starmer resigned, polls showed that he had become the least popular Labour Prime Minister in living memory. His fall was all the more striking because his political beginnings had once suggested a very different trajectory. As a teenager in the Labour Party Young Socialists, and later as editor of the Marxist journal Socialist Alternatives, he had stood firmly on the radical left. As a human rights lawyer he opposed the illegal invasion of Iraq, earning a reputation for principle and moral clarity.

It was this early radicalism that his supporters later weaponised, presenting him as a unifying leftwing figure in the aftermath of the coup against the Labour Party leader Jeremy Corbyn. The right-wing of Labour, having spent years undermining Corbyn (including through a coordinated campaign that framed him, falsely, as anti-Semitic) found in Starmer a vessel through which they could reclaim the party while reassuring the membership that continuity with the Corbyn surge remained intact.

In his resignation speech, Starmer claimed to have inherited a politically, morally and financially bankrupt Labour Party. Yet the record shows that Corbyn had revived the party’s grassroots, drawing tens of thousands of new members back to a party embodying the tradition of Keir Hardie. The oligarchy closed ranks against this leftist heavyweight, using Starmer and the Labour right wing as their weapon. Starmer’s “Changed Labour” was not a renewal but a repudiation, embracing the very Thatcherite revisionism that had hollowed Labour out in the first place.

A Britain battered by decades of neoliberal restructuring formed the backdrop to Starmer’s rise. The cumulative effects of Maggie “milk-snatcher” Thatcher’s programme, deepened by Blair, Cameron, May, and Johnson, combined with the convulsions of Brexit to produce a profound economic, social, and political crisis. The Conservative Party imploded under the weight of its own contradictions. Starmer, offering managerial calm, an a Corbyn-lite manifesto, rode the wave of Tory collapse to a landslide victory.

But once in office, he revealed himself as a Blairite in sombre tones: a Thatcherite in Labour clothing. Within weeks he slashed winter fuel payments for pensioners, inaugurating a harsh antiworkingclass agenda. He embraced the Israeli government even as it carried out genocide in Gaza. The former human rights lawyer now used antiterror legislation to suppress dissent, particularly protests against the genocide. His immigration rhetoric, invoking an “island of strangers,” echoed the poisonous cadences of Enoch Powell.

Throughout his premiership he remained pofaced, showing little emotion even when forced into humiliating Uturns by public outrage. He displayed no visible sorrow at the mass killing of children in Gaza. Only at the prospect of losing office did he appear moved. He was, in the words of Saki, a man with “the soul of a meringue,” a mediocrity whose obedience to the oligarchic class and to Zionist backers embodied what Hannah Arendt called the banality of evil. His legacy – and that of the Tories who preceded him – is a nation distrustful of politicians of whatever hue, open to the pseudo-anti-elite, deception of the billionaire-backed racist far-right

His resignation leaves Britain at a crossroads – will it follow the fascistic path of Nigel Farage’s Reform Party, or will it go down the green-red road of Zach Polanski and Corbyn? Even replacing Starmer with the newly-elected Andy Burnham will only provide more-of-the-same Tory policies – Burnham went on record saying his first foreign visit as Prime Minister would be to Israel. These are the same policies that created a visceral hatred of Starmer and opened the gates for Reform’s surge.

When news of his resignation broke, a friend told this writer that the one who had engineered the exit of Jeremy Corbyn had been unable to complete two years in office. He added, ‘Rajakam kalath kalakam palade”-– even if you reign, your deeds will bear consequences.

And, so ends the Starmer era, not with the dignity of a statesman, but with the hollow thud of a project built on betrayal, opportunism, and the abandonment of the very principles he once claimed to uphold.

by Vinod Moonesinghe

Sri Lanka seek big win against Scotland to keep semi-final hopes alive

Oil price falls back to pre-Iran war levels

Venezuela earthquakes: At least 164 dead, 971 injured as toll rises

Representatives from the Ceylon Chamber of Commerce meet PM

Progress of Housing Project for Malayagam Community families funded by India reviewed

South Africa stun South Korea to reach World Cup knockouts for the first time

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News7 days ago

News7 days agoCreditor receives USD 2.5 mn as Lankan public bears loss from theft of Treasury funds

-

News6 days ago

News6 days agoCreditor not yet paid

-

News6 days ago

News6 days agoConsumers bearing 22% tax burden despite 18% VAT claim: Dr. Harsha de Silva

-

Features5 days ago

Features5 days agoNanda Pethiyagoda Wanasundara as three generations of family saw her

-

Features4 days ago

Features4 days agoSri Lanka developing independent hydrographic capabilities

-

Opinion7 days ago

Opinion7 days agoSriLankan Airbus struck by lightning

-

Editorial5 days ago

Editorial5 days agoFuel crisis: Beyond price debate

-

Latest News4 days ago

Latest News4 days agoSooryavanshi thumps fastest List A fifty as India A win tri-series