Business

Learning for Sri Lanka on SOE Reforms – Malaysia’s Khazanah Nasional Berhad

Introduction

A super-holding company for managing State-Owned Enterprises (SOEs) has been identified as a globally successful model for SOE management. This model allows the government to adopt a more arms-length approach to SOEs’ operational decision-making, relieving it of the direct responsibility of overseeing all SOEs dispersed across various industries, and redirect its budget and energy elsewhere. The merits of this model have enabled countries such as Malaysia and Singapore, which employ similar holding company structures, to ensure impressive performances of their SOEs.

This article is the second of a three-part series where part one and two provide an in depth analysis of the case of Singapore’s and Malaysia’s SOE holding company models (Singapore’s Temasek Holdings and Malaysia’s Khazanah Nasional), and their role in enabling economic growth and development for the respective countries. Part three will provide learnings for Sri Lanka, which can be adopted for the country’s SOE reform process. This series of articles is a joint effort by the Ceylon Chamber of Commerce (CCC) and the Colombo Stock Exchange (CSE).

Part Two: Malaysia’s Khazanah Nasional Berhad

Overview

Khazanah is a Malay word that originated from an Arabic word, which means ‘treasure’ so, Khazanah Nasional translates to ‘national treasure’. Khazanah was incorporated under the Companies Act in Malaysia in 1993 as a public limited company, that manages state assets in selected sectors on behalf of the Malaysian government. It also takes investment decisions on behalf of the government, including listing, divestment, and acquisition of shares.To balance the dual objectives required by the Malaysian economy, two separate funds have been established, namely; Commercial Fund (CF) and the Strategic Fund (SF) with distinct objectives, policies and strategies.The SF undertakes investments to deliver impactful and measurable economic and societal returns for Malaysia and its people, while CF focuses on investing responsibly and commercially to preserve and grow the long-term value of assets.

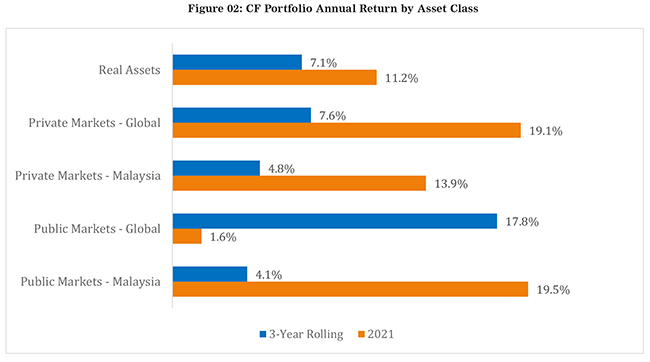

The CF generated a three-year rolling Time-Weighted Rate of Return (TWRR) of 7.0% against the targeted return of the Malaysian Consumer Price Index (CPI) at 3% on a five-year rolling basis. In 2021, the TWRR stood at a significant 19%. This was led by asset classes such as global private markets and public markets in Malaysia, which outperformed in 2021 when compared to the 3 year rolling of 7.6% and 4.1% respectively of the same asset classes (refer figure 02).

Source: Khazanah Nasional Berhad The two funds were valued RM 106 billion (around USD 25 billion) and RM 28 billion (around USD 7 billion) for CF and SF, respectively at the end of 2021. A majority of the investments (63.5%) were made within Malaysia, with the rest in China (14.8%), Asia – excluding China (12%), and around 10% in Europe, the Middle East, Africa (EMEA) and North America by the end of 2021.Consumer Goods, Energy, Financials, Healthcare, Industrials, Information Technology, Media, Real Estate, Telecommunications and Utilities are among the sectors Khazanah has invested in.

Why was Khazanah Successful?

Post the Asian Financial Crisis, most SOEs in Malaysia were not performing well. To address this Khazanah was revamped in 2004 to play an active role from the previous passive role to enable efficiency and to drive growth of the SOEs. This was coupled with major corporate restructuring and institutional reforms through the GLC Transformation Program (2005-2015) for which Khazanah functioned as the secretariat.

The revamp shifted Khazanah’s focus from a Sovereign Wealth Fund (SWF) to a Sovereign Development Fund (SDF). The salient feature of a SDF is that it not only delivers high financial performance but also fosters development. Today, Khazanah comprises two funds (CF and SF) which aim to achieve the dual objectives and its total Net Asset Value (NAV) has grown from RM79 billion to RM86 billion in 2021. The 10 key factors that were critical to its success are outlined below:

1. Clear Objectives

Khazanah focused on three clear objectives to drive its financial, economic and societal returns as given below. Performance – focusing on corporate restructuring to improve efficiency, productivity and value creation. This was achieved by issuing guidelines on KPIs and anchoring KPI’s to performance. Relevant KPIs were developed together with appropriate benchmarks and targets, and rewards were linked to performance coupled with time based contracts such as 3-year contracts. This was also enabled through reconstituting the senior management and implementing board composition reforms. National Development – focusing on national development goals such as creating jobs and economic multipliers. Supporting government policy formation and adopting a long-term view in catalysing social progress in Malaysia to deliver high social impact in communities.

Good Governance –took a holistic and multipronged approach to measure how public institutions conduct and manage public resources.

2. National Support

A degree of national consensus is vital with all relevant stakeholder groups involved and powered by political will. The reform process was carried out over 10 years from 2005 onwards where the reform of Khazanah started under the 4th Prime Minister of Malaysia, the GLC Transformation (GLCT) Programme under the 5th Prime Minister and continued under the 6th Prime Minister.

3. Communications, transparency, public accountability

Transparency and consistent periodic reporting are vital to the success of the programme. KPIs were announced publicly with regular public updates, with internal KPIs being identical to external KPIs. This was followed by consistent and relevant stakeholder engagement across multiple categories.

4. Active, competent, and empowered Holding Company

Khazanah was revamped as an active and strategic SDF (Sovereign Development Fund). Khazanah was also tasked to come up with an overarching programme for other funds from 2005 to 2015. This programme was known as the GLC Transformation Program (GLCT) with Khazanah acting as its Secretariat.

5. A robust Programme Management approach over 10 to 15 years

The GLCT Programme was carried out for 10 years with a careful designed implementation structure. It consisted of 22,981 man days of programme management and 29 meetings were chaired by the Prime Minister to review progress over the 10-year period. It is imperative to stay the course since the prize of seeing it through and the price of not doing so is large. However, it must be ensured that it’s done correctly.

6. Talent and Leadership

Right leadership is critical. Therefore, the Chief Executive Officer. the Board and the Senior Management should be selected under specified criteria to appoint individuals based on their capacity and knowledge to deliver in their role. This should also be followed by a robust selection process.

7. Transformation Acupuncture

Targeted 10 critical areas for improvement in corporate restructuring in key companies. The critical areas included Board governance, CSR, procurement, leadership development, performance based compensation, regulation, operational improvement and finance.

8. Accountability

This included headline KPIs, performance-based compensation, senior management limited to 3-year performance based contracts and a robust appointment process, emulating a carrot and stick approach.

9. Getting key sectors right in terms of the policy mix

It is important to identify the critical sectors such as electricity, telecom, banks, aviation, infrastructure, etc. that play a vital role in the economy. Planning the sector strategy, regulation, pricing, social policy, etc. for the selected sectors instead of reforming all the sectors will also divert resources to effective and efficient use.

10. Using the levers of ownership, financing and controls

Sorting between principally commercial and principally social enterprises is also pertinent. Understanding which particular category enterprises come under will provide clarity on how to run these enterprises such as whether to list or delist, to conduct partial or full asset sales and to understand the required capital structure controls, debt discipline, and external audits.

How has it contributed to Development Goals?

Khazanah’s principal funding is from shareholder equity. It utilises debt financing and proceeds from divestment activities to fund its investment activities. Khazanah’s ultimate holding body and hence the sole shareholder, is the Ministry of Finance (MoF).In terms of contribution, between 2004 and 2021, Khazanah paid RM15.6 billion in dividends to the government (or MoF) averaging RM 1.3 billion a year over the past five years. Dividends of RM2 billion each had been declared in 2020 and 2021.

Investment income contributed to 16.3% of total government revenue in 2021, of which Khazanah contributed to about 6% of investment income through its dividends. Though the contribution to government revenue through dividends remains marginal when compared to other tax revenue streams, Khazanah continued to deliver societal value and impact through various other initiatives.

During the pandemic, RM20 million was contributed by Khazanah as COVID-19 relief to the government. Therefore, Khazanah acts as a buffer against future pandemics and can assist the government in its relief measures.One of Khazanah’s foundations – Yayasan Hasanah – directly and indirectly assisted 1.5 million people through Covid-19 relief efforts and various other programmes, with an allocation of RM554 million in 2021.The Khazanah Research Institute was set up to undertake analyses and research on the pressing issues of the nation, and based on the research, provide policy recommendations to improve the well-being of Malaysians. A total of 30 publications were released in 2021.

Khazanah also works on development projects for the improvement of the Malaysian economy. This includes Dana Impak, which is a newly created project with an allocation of RM6 billion over 5 years. This is carried out to increase Malaysia’s economic competitiveness and build national resilience. This focuses on 6 areas namely; digital society and technology hub, quality health and education for all, decent work and social mobility, food and energy security, building climate resilience, and competing in global markets.The full brief can be accessed at: Holding Company for SOEs: Learnings for Sri Lanka

This article was developed as part of the Strategic Insight Series of the Economic Intelligence Unit (EIU) of the Ceylon Chamber of Commerce (CCC) in collaboration with the Colombo Stock Exchange (CSE). The Strategic Insight Series are a series of briefs that focuses on key contemporary topics that matter to the private sector.

LOLC Finance PLC, the flagship finance company of the LOLC Group and Sri Lanka’s largest non-bank financial institution, delivered a strong financial performance for the year ended 31 March 2026, supported by robust lending growth, stronger recurring income, improved asset quality and a capital position that remained comfortably above regulatory requirements.

The Company reported profit after tax of Rs. 27.4 billion for the year, compared with Rs. 25 billion in the previous year. At headline level, this represents growth of around 9%. However, the headline comparison does not fully capture the improvement in the Company’s underlying performance.

The previous year’s profit included significant non-recurring gains linked to Sri Lanka sovereign bond-related impairment reversals, partially offset by a derecognition loss. On a net basis, these one-off items added approximately Rs. 4 billion to the prior year result. Adjusting for this, the prior year’s underlying profit base was closer to Rs. 21 billion. Against that adjusted base, the current year profit of approximately Rs. 27 billion reflects underlying profitability growth of close to 30%.

This is the more important message behind the numbers. LOLC Finance did not merely preserve profitability in a recovering economic environment; it expanded its recurring earnings base materially, while simultaneously growing its balance sheet and improving key credit quality indicators.

The improvement was driven primarily by core income. Interest income increased to approximately Rs. 79 billion, supported by strong expansion in the lending portfolio. Interest expense rose at a slower pace to approximately Rs. 29 billion, allowing net interest income to grow to approximately Rs. 50 billion. This demonstrates the Company’s ability to expand its loan book while maintaining control over funding costs.

Net fee and commission income also improved, rising to approximately Rs. 3 billion, reflecting higher business volumes and broader customer activity. Total operating income increased to approximately Rs. 56 billion, despite the absence of the large sovereign bond-related gains that benefited the previous year. This shift from one-off gains to recurring operating income is a clear positive from an earnings-quality perspective.

The balance sheet story was equally significant. Total assets grew by approximately Rs. 129 billion during the year, reaching around Rs. 559 billion as at 31 March 2026. The main driver of this expansion was the lending portfolio, with gross loans and advances increasing from approximately Rs. 305 billion to approximately Rs. 423 billion, representing growth of nearly 39%.

This level of loan book expansion is notable not only because of its scale, but also because it was spread across multiple product categories. Growth was recorded across key lending lines including finance leases, gold loans, speed drafts, alternate finance, personal loans and term loans. This points to a broad-based recovery in customer demand rather than growth concentrated in a single product line.

Malaiyaha Tamil workers in Sri Lanka’s private tea estates and smallholdings are facing widespread labour abuses that amount to multiple indicators of forced labour, according to a new report released last week by Amnesty International.

‘The Sri Lankan government is urged to strengthen labour protections, improve enforcement mechanisms and remove barriers that prevent Malaiyaha Tamil workers from accessing their rights under both domestic law and international obligations, a media release on the report explained.

‘Workers are being subjected to intimidation, physical violence, harassment, debt bondage, restrictions on movements, wage withholding and severely poor living and working conditions, the release added.

Some extracts from the release:

‘The research focused on tea estates in Sri Lanka’s Southern Province, particularly in the Galle and Matara Districts. It is based on visits to 45 estates conducted between January 2024 and January 2026, alongside 159 interviews with workers, discussions with Estate Managers and Supervisors, and 15 focus group discussions involving 65 workers. Across all sites, researchers found what they describe as a consistent pattern of exploitation and discrimination affecting Malaiyaha Tamil workers.

‘Workers reported being forced to meet unrealistic daily tea-picking targets, often set at more than 25 kilograms per day. Failure to meet these targets reportedly resulted in wage deductions, delays, or reduced pay, sometimes bringing daily earnings down to as little as LKR 1,000 (around USD 3.10). Workers also described a cycle of wage advances and loans that left them increasingly indebted to estate owners, raising concerns about debt bondage in the plantation sector.

‘Several workers also told researchers they had experienced or witnessed verbal and physical abuse by estate managers, particularly when they were late for work, questioned unpaid wages, or failed to meet production targets. One worker described being beaten with hands, legs, and sticks, and said such violence was still occurring. Others reported that wages were often withheld or manipulated based on arbitrary assessments of productivity.

‘Employers frequently classify them as “casual workers,” which denies them access to maternity benefits, pensions, sickness leave, and other statutory entitlements. The report also notes that trade union representation is largely absent in the Estates surveyed, leaving workers with little collective bargaining power or protection against abuse. According to the report, workers face multiple barriers in accessing justice, including language barriers, discriminatory treatment by officials, lack of documentation, and weak labour inspection mechanisms. These factors, the report says, prevent effective enforcement of labour laws and allow abusive practices to continue largely unchecked.

‘Smriti Singh, Regional Director for South Asia at Amnesty International, said the findings reflect systematic violations of labour laws and a failure of enforcement by the state. She said, private tea estates are operating with little accountability and that the pattern of abuse raises serious concerns about forced labour.’

By Hiran H. Seneviratne

Low investor sentiment persisted in the stock market yesterday due to lingering West Asian uncertainties particularly in relation to Israel and Lebanon.

Both indices moved downwards. The All Share Price Index went down by 48.78 points, while the S and P SL20 declined by 7.46 points. Turnover stood at Rs 1.67 billion with two crossings.

Those crossings were; HNB crossed 185718 shares to the tune of Rs 73.4 million; its shares traded at Rs 395 and Dialog Axiata 1 million shares crossed for Rs 44 million; its shares traded at Rs 44.

In the retail market companies that mainly contributed to the turnover were: RIL Properties Rs 148 million (5.3 million shares traded), Dialog Rs 108 million (2.4 million shares traded), Aitken Spence Rs 74.4 million (542,100 shares traded), LB Finance Rs 72.2 million (7.3 million shares traded), Royal Ceramics Rs 67.2 million (1.4 million shares traded), Renuka Agri Foods Rs 64.8 million (5.2 million shares traded) and JKH Rs 53.7 million (2.7 million shares traded). During the day 71 million shares volumes changed hands in 23582 transactions.

It is said that banking sector counters, especially HNB, performed well while the real estate sector stocks, especially RIL Properties, performed well. An overall mixed performance was noted in most of other sectors, especially finance and agriculture.

Yesterday the rupee was quoted at Rs 330.00/332.00 to the US dollar in the spot market, from 331.00/332.00 Friday, dealers said, while bond yields were flat.

By Hiran H Senewiratne

Rainy conditions are expected to increase in the southwestern parts of the island from this evening (02 June)

IMF turning a blind eye to NPP corruption: Opp.

Shavendra tells Beijing meet Sri Lanka should not become an arena for geopolitical rivalry among major powers

Govt. leaders speak to Basil more than I do – Namal

Sri Lankan teen killed in Chennai clash; three arrested

Sri Lanka’s vanishing wetlands put elusive otter under growing threat

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News3 days ago

News3 days agoIMF urges Lanka not to meddle with exchange rate

-

Business4 days ago

Business4 days agoSri Lanka’s construction industry losing ground while no one watches

-

News3 days ago

News3 days agoState of emergency extended

-

Midweek Review6 days ago

Midweek Review6 days agoIsraeli-US aggression won’t go unanswered -Iranian Ambassador

-

Features4 days ago

Features4 days agoThe Division Bell Mystery

-

News1 day ago

News1 day agoUNP challenges NPP move to amend Vihara – Devalagam Act

-

News3 days ago

News3 days agoFort Magistrate to announce whether to summon Arsecularatne PC to testify at Kapila’s inquest

-

News5 days ago

News5 days agoRTI query of Ditwah funds: Presidential Secretariat mum on key questions