Business

Trade deficit widens as worker remittances increase

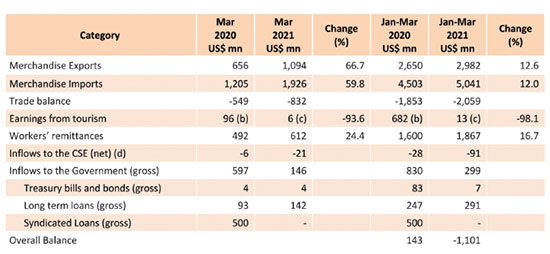

External Sector Performance – March 2021 Overview

Sri Lanka’s external sector showed a mixed performance in March 2021 with a widened trade deficit on the one hand, and a healthy growth in workers’ remittances and a slight pickup in the tourism sector on the other. The deficit in the trade account widened in March 2021, for the first time since April 2020. Both exports and imports were significantly higher in March 2021, compared to March 2020 as well as February 2021. However, workers’ remittances grew steadily, and the tourism sector continued the recovery process, albeit at a very slow pace. In the financial account, both foreign investment in the government securities market and the Colombo Stock Exchange (CSE) continued to record marginal net outflows in March 2021 as well.

The Sri Lankan rupee depreciated against the US dollar during the month, partly reflecting the seasonal demand for imports. However, mainly supported by the regulatory measures that were in place till mid-March, the Central Bank absorbed foreign exchange on a net basis during the month, to strengthen the gross official reserve position. Meanwhile, in March 2021, the Central Bank entered into a bilateral currency swap arrangement with the People’s Bank of China (PBoC) for Chinese yuan 10 billion (approximately US dollars 1.5 billion) with a view to promoting bilateral trade and direct investment for economic development of the two countries, and to be used for other purposes agreed upon by both parties.

Trade Balance: The deficit in the trade account widened on a year-on-year basis in March 2021, for the first time since April 2020, to US dollars 832 million compared to the deficit of US dollars 549 million recorded in March 2020 and US dollars 572 million in February 2021. Both exports and imports were significantly higher in March 2021, compared to March 2020 and February 2021. Meanwhile, the cumulative deficit in the trade account during January – March 2021 widened to US dollars 2,059 million from US dollars 1,853 million recorded over the same period in 2020. The major contributory factors for the increase in the trade deficit as at end March 2021 are shown in Figure 1.

Terms of Trade: Terms of trade, i.e., the ratio of the price of exports to the price of imports, deteriorated by 6.3 per cent in March 2021 as the increase in import prices were higher than the increase of export prices, compared to March 2020.

Overall exports: Earnings from merchandise exports in March 2021 increased by 66.7 per cent to US dollars 1,094 million, from low earnings from merchandise export in March 2020 (US dollars 656 million) during the first wave of the COVID-19. Earnings from exports improved considerably in March 2021 compared to February 2021 also raising export earnings towards pre-pandemic export levels.

Industrial exports: Earnings from all subsectors of industrial goods exports, excluding petroleum products and leather, travel goods and footwear, improved in March 2021, year-on-year. On a month-on-month basis, earnings from Industrial exports increased, except for the subsector of leather, travel goods, and footwear. Earnings from textiles and garments, rubber products (mainly gloves and tyres), food, beverages and tobacco (mainly value added coconut products), base metals and articles, chemical products, and machinery and mechanical appliances exports recorded considerable growth rates compared to February 2021. Meanwhile, earnings from the export of petroleum products declined on a year-on-year basis due to the significant reduction in volumes of aviation fuel and bunkering fuel supplied to aircraft and ship arrivals, despite the increase in the average prices of these export products. Earnings from leather, travel goods and footwear export declined in March 2021 both on year-on-year and month-on-month bases.

Agricultural exports: Export earnings from all subsectors related to agricultural goods increased in March 2021, compared to a year ago, as well as compared with February 2021. Export earnings from tea, seafood, coconut (both kernel and non-kernel products), spices (mainly pepper), and minor agricultural products (mainly arecanuts) recorded considerable increases over February 2021.

Mineral exports: Mineral exports in March 2021 were also higher than the exports observed in March 2020 and February 2021, due to increased earnings in subsectors of earths and stone (mainly quartz) and ores, slag and ash (mainly titanium ores).

Export indices: The export volume index and the unit value index increased by 56.5 per cent and 6.5 per cent, respectively, on a year-on-year basis, in March 2021. This indicates that the increase in export earnings were due to the combined impact of higher export volumes and prices.

(CBSL)

Dialog Axiata PLC announced its consolidated financial results for the quarter ended 31 March 2026 on Friday 15 May 2026. Financial results included those of Dialog Axiata PLC (the “Company”) and of the Dialog Axiata Group (the “Group”).

Group Performance

The Group delivered revenue growth of 9% Year on Year (“YoY”) on the back of strong performances in Mobile, Fixed and Digital Pay Television businesses as Group Revenue reached Rs 47.3Bn, despite the continued strategic scaling down of the low-margin international wholesale business. On a Quarter-on-Quarter (“QoQ”) basis, revenue increased by 2% supported by Data Revenue growth and advertising revenue generated by Television Business.

The Group Earnings Before Interest, Tax, Depreciation and Amortisation (“EBITDA”) was recorded at Rs 24.3Bn, up 23% YoY supported by Revenue performance and Cost Rescaling Initiatives. EBITDA margin expanded by 5.8pp YoY to reach 51.3%. On a QoQ basis Group EBITDA grew 5%.

Group Net Profit After Tax (“NPAT”) was recorded at Rs 9.2Bn for Q1 2026, up +>100% YoY and 56% QoQ, supported by robust EBITDA growth, lower net finance costs and lower forex losses.

Reflecting strong operational performance, the Group recorded Operating Free Cash Flow (“OFCF”) of Rs 14.6Bn for Q1 2026, up 8% YoY.

Interim Dividend to Shareholders

The Board of Directors of Dialog Axiata PLC approved an interim dividend for Q1 2026, after considering the financial performance of the Group and taking into account the forward investment requirements, at the meeting held on 14th May 2026. The approved first interim dividend for FY 2026 amounts to Rs 0.70 per share and would translate to an Annualized Dividend Yield of 9.2% based on share closing price for Q1 2026.

Company and Subsidiary Performance

At an entity level, Dialog Axiata PLC (the “Company”) continued to be the primary contributor to Group Revenue (76%) and Group EBITDA (75%). Supported by YoY growth in the Data segment and effective cost-rescaling initiatives, Company revenue for Q1 2026 increased by 12% YoY to Rs 36.0Bn, while EBITDA rose 29% YoY to Rs 18.2Bn. On a QoQ basis, Company revenue grew by 4% while EBITDA grew by 7% QoQ, primarily attributable to the flow-through impact of revenue growth and reduction in direct costs. Furthermore, NPAT for Q1 2026 was recorded at Rs 7.6Bn, up +>100% YoY. On a QoQ basis, Company NPAT grew 83% QoQ.

The balance of trade between Canada and Sri Lanka which is in Canada’s favour, could be developed more evenly by promoting to a greater extent trade, investment, tourism and business partnerships between the countries, Canadian Chamber of Commerce in Sri Lanka (CanCham SL) Secretary General Nilupul De Silva said.

‘CanCham SL was established as a dynamic platform to promote trade, investment, tourism and strategic business partnerships between Canada, Sri Lanka and the wider Indo-Pacific Region, Secretary General De Silva explained.

‘The Chamber aims to facilitate stronger commercial engagement while supporting sustainable economic growth and regional collaboration. More than 65 percent of the world’s population resides is in the region, she said at a media conference held at CanCham House, Horton Place recently.

The Secretary General added: ‘The Canadian High Commissioner to Sri Lanka serves as the Patron of CanCham SL, further reinforcing the Chamber’s commitment towards strengthening bilateral and regional economic cooperation.’

‘The Canadian Chamber of Commerce in Sri Lanka proudly participated in a historic milestone with the formal signing of a landmark MOU alongside all Canadian Chambers across the Indo-Pacific region, in the presence of the Canadian Prime Minister Hon. Mark Carney, she said.

‘The agreement signifies a new era of collaboration among the Canadian Chambers of the Indo-Pacific, with a strong focus on strengthening trade and investment ties, enabling strategic resource sharing, enhancing regional cooperation and fostering knowledge exchanges across member chambers and markets, founder and board member CanCham SL M.H.K.M Hammez said.

He said that PM Carney announced a Canadian commitment of CAD 0.5 trillion (CAD 500 billion) towards strengthening Canada’s economic relationship with the Indo-Pacific region over the next decade.

‘Subsequently Canada established a sovereign wealth fund with an allocation of Canadian dollars 25 billion to support long term strategic and international economic initiatives in the region, Hammez said.

‘The Chamber will work closely with business leaders, diplomatic missions, government institutions, investors and industry stakeholders to create meaningful opportunities for Canadian and Sri Lankan enterprises, he added.

‘Not having a permanent Sri Lankan High Commissioner for Canada is one of the biggest issues we are encountering. There is nobody to coordinate and communicate from that end, Hammez said.

‘CanCham is an independent entity trying its level best to promote certain priority development sectors in the country with Canadian support, he explained.

By Hiran H.Senewiratne.

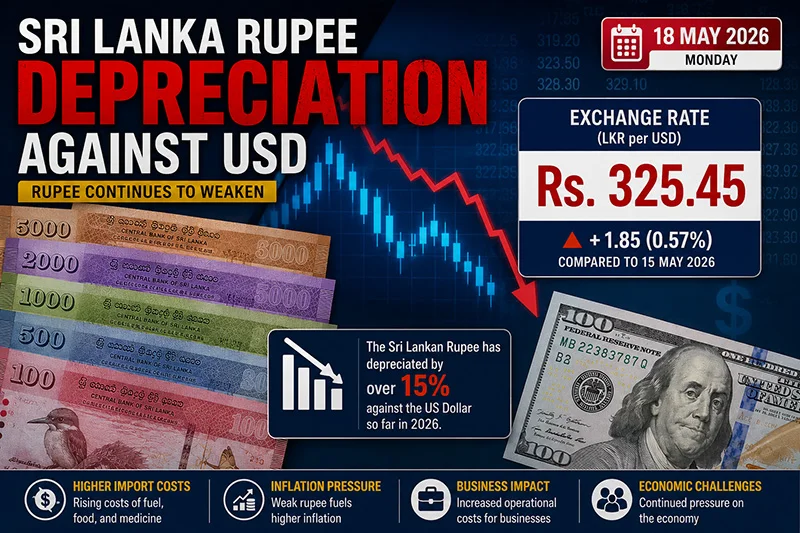

The continued depreciation pressure on the Sri Lankan rupee is exposing deep-rooted structural weaknesses within the economy, while simultaneously creating limited opportunities for export-oriented sectors, according to Rajkumar Kanagasingam.

Kanagasingam warned that while some export industries may temporarily benefit from a weaker currency, the broader economic strain caused by rising import costs, inflationary pressures, and investor uncertainty continues to weigh heavily on businesses and consumers alike.

Speaking to The Island Financial Review, he said local industries are struggling to absorb rising costs linked to imported raw materials, machinery, fuel, and intermediate goods as the rupee remains under pressure.

“Local industries are coping through cost-cutting measures, selective price increases, tighter inventory management, and delaying certain capital investments,” he said. “Many businesses are also exploring alternative suppliers and improving operational efficiency to manage rising import-related costs.”

He noted that import-dependent sectors are among the hardest hit by currency depreciation, particularly construction, transport, pharmaceuticals, manufacturing, and food imports, where businesses face mounting operational expenses and shrinking margins.

At the same time, Kanagasingam observed that export-oriented sectors such as apparel, tea, IT services, tourism, and businesses promoting local substitutes may gain some competitive advantage from the weaker rupee, as foreign exchange earnings translate into higher rupee revenues.

“A weaker rupee can improve the competitiveness of export-oriented sectors by increasing rupee earnings from foreign exchange,” he explained. “However, the benefits may be partially offset by higher imported input costs, energy expenses, and broader economic pressures.”

He stressed that small and medium-scale enterprises (SMEs) remain significantly more vulnerable than larger corporates during periods of currency instability.

“SMEs generally have limited financial buffers, less access to foreign currency, and weaker bargaining power,” he said. “Larger corporates are typically better positioned to manage exchange rate fluctuations through stronger reserves, export earnings, and diversified financing options.”

Kanagasingam added that consumers are ultimately carrying much of the burden created by rupee depreciation, with higher prices increasingly visible across food, transport, utilities, imported goods, and daily services.

“In many cases, increased business costs are gradually passed on to consumers,” he said, warning that sustained currency weakness could continue to fuel inflationary pressure across the economy.

He also pointed to a growing shift among local manufacturers toward localization and import substitution as businesses attempt to reduce reliance on imported inputs.

“There is growing interest in strengthening domestic supply chains and local production,” he noted. “However, Sri Lanka still faces challenges in terms of industrial scale, technology, and the availability of locally sourced raw materials.”

According to Kanagasingam, persistent currency volatility also undermines investor confidence and complicates long-term industrial planning.

“Currency fluctuations create uncertainty for investors, particularly in areas such as pricing, financing, debt servicing, and long-term project planning,” he said. “Greater exchange rate stability generally improves investor confidence and supports long-term industrial growth.”

He urged policymakers and the Central Bank to prioritize macroeconomic stability, foreign reserve strengthening, export expansion, energy efficiency, and targeted support for SMEs in order to cushion the impact of exchange rate volatility.

“The priority should be maintaining macroeconomic stability, strengthening foreign reserves, supporting export growth, improving energy efficiency, encouraging local production, and providing targeted support for SMEs,” he said. “Consistent and predictable policy measures are also essential to strengthen investor confidence.”

Kanagasingam further cautioned that prolonged rupee depreciation could eventually lead to job losses in sectors heavily dependent on imports.

“Prolonged depreciation could place pressure on import-dependent industries, potentially leading to reduced production, delayed expansion, and job losses, particularly among smaller businesses and vulnerable sectors,” he warned.

Describing the current exchange rate situation as more than a temporary market adjustment, Kanagasingam said Sri Lanka must address its long-standing structural vulnerabilities if it hopes to achieve lasting currency stability.

“It reflects both short-term external pressures and deeper structural challenges within the economy,” he said. “These include high import dependence, limited export diversification, debt-related pressures, and the need for stronger foreign exchange generation over the long term.”

Economic analysts note that the rupee’s trajectory in the coming months will remain closely tied to external debt management, reserve accumulation, export performance, remittance inflows, and broader investor sentiment surrounding Sri Lanka’s economic recovery efforts.

By Ifham Nizam

At least 100 dead in Ebola outbreak in DR Congo, official says

Trump says he called off new Iran attack at request of Gulf states

Lanka Premier League returns after two years, opener set for July 17

Cummins, Kishan, Klaasen power Sunrisers Hyderabad into playoffs; Chennai Super Kings not out yet

Mushfiqur ton, Litton and Joy fifties set Pakistan 437

Showers will occur at times in the Western, Sabaragamuwa, Central, North-western, Northern and Southern provinces and in Anuradhapura district

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoEx-SriLankan CEO’s death: Controversy surrounds execution of bail bond

-

Features2 days ago

Features2 days agoSri Lankan Airlines Airbus Scandal and the Death of Kapila Chandrasena and my Brother Rajeewa

-

News3 days ago

News3 days agoLanka’s eligibility to draw next IMF tranche of USD 700 mn hinges on ‘restoration of cost-recovery pricing for electricity and fuel’

-

Midweek Review6 days ago

Midweek Review6 days agoA victory that can never be forgotten

-

News2 days ago

News2 days agoKapila Chandrasena case: GN phone records under court scrutiny

-

Opinion5 days ago

Opinion5 days agoElectricity tariffs have skyrocketed: Can further increases be prevented?

-

Features4 days ago

Features4 days agoMysterious Death of United Nations Secretary General Hammarskjöld

-

News2 days ago

News2 days agoRupee slide rekindles 2022 crisis fears as inflation risks mount