Business

Strong economies need strong banks: Building the system Sri Lanka’s next decade will need

The IMF, in its successive reviews of Sri Lanka’s recovery programme, has consistently emphasized that a sustained recovery requires a sound banking sector. This in turn means a sector capable of channeling credit into the productive economy, mobilizing savings, and facilitating investment, all of which represent the most critical needs of the nation.

That observation deserves attention, because it cuts against a public conversation now under way about whether banking profitability in Sri Lanka reflects value created or value extracted. The question is fair.

Banks intermediate the savings of citizens into the credit that builds the economy, while serving as the nexus of connectivity to global banking networks. This in turn facilitates the international trade and global payments on which Sri Lanka’s economic recovery hinges. The relationship between bank performance and national performance is direct, and should be carefully scrutinized.

The value beneath the surface

Such a surface-level reading, however, misses some key factors. First, what banking strength delivered through the crisis. When sovereign default came in 2022, no Sri Lankan depositor lost their savings. There were no withdrawal restrictions of the kind seen in Lebanon, Argentina or Cyprus.

Trade finance lines kept essential imports moving when foreign currency was scarce. While efforts were made to mitigate its total impact, Domestic Debt Optimisation (DDO) in 2023 was also absorbed by banks at material cost to their own balance sheets. This sensitive fiscal restructuring was made possible because the banking sector was strong enough to take the hit. A weakly capitalised system could not have done any of this.

Net Interest Margins (NIM) are another misunderstood factor. Where on the surface, Sri Lankan banks appear to be earning high NIM, this narrow view misses the outsized tax burden placed on the Sri Lankan banking industry, which is among the largest contributors to state revenue, paying corporate income tax, VAT on financial services, and other levies totaling in excess of 50%.

In HNB’s case, for every rupee retained as profit after all taxes in FY2025, approximately a rupee was paid to the state. That contribution is appropriate for the current moment. But it means the margin which appears wide in headline terms is substantially narrower once the state’s share is accounted for. In such an environment, a high NIM is necessary to continue operating while maintaining the strength and stability needed to face future headwinds.

Most importantly, the banking sector materially expanded private sector credit through 2025. Against the Government’s Rs. 95 billion MSME financing programme, several private banks including HNB deployed at or above their full allocations within the window.

At HNB, the loan book grew by approximately 30% over the financial year, with non-performing loan ratios improving over the same period. Far from retreating from the real economy, this represents capital being actively deployed into productive sectors at scale. This in turn helped to cushion the worst impacts of the successive crises that hit the Sri Lankan economy 2019 onwards.

Why a strong banking system matters now more than ever

Damith Pallewatta

Strong economies require strong banks. The question Sri Lanka now faces is how to channel the strength of its banking sector to accelerate the next phase of recovery. As an industry our first priority is to rebuild access to development funding.

Twenty-five to thirty years ago, Sri Lankan banks had access to long-tenor concessional funding through development institutions, which allowed on-lending to priority sectors at lower rates. Those channels need to be reactivated.

The most direct route to cheaper SME credit is not a regulatory cap on lending rates, which would compress credit supply. Instead, we must seek to engage further with long-tenor concessional funding lines through partners such as the ADB, the IFC, the World Bank, the EU, KfW, and JICA.

Banks lend at rates that reflect their cost of funding. With funding cost reduce, the lending rate follows, and that is ultimately what will provide the grassroots of the Sri Lankan economy with the affordable capital they require to shift from recovery to revitalisation.

Our second priority is digital infrastructure and inclusion. Sri Lanka’s digital payments ecosystem is still scaling, well short of advanced economies and regional peers. That matters for the public conversation about fees. Even India’s UPI, often cited as a zero-cost model, processed 228 billion transactions in 2025 against an operating shortfall of around USD 1 billion in FY24, and Indian regulators are now actively debating tiered fees to keep the platform viable.

The reality is that zero-cost digital payments have not proven sustainable anywhere at scale across time. Because even though digital payments offer banks a much lower operating cost than a physical banking model, they do come with a substantial cost to establish, scale up, secure, maintain, and improve.

While digital banking delivers efficiency gains over time, the assumption that each additional transaction costs progressively less overlooks the realities of regulated financial infrastructure. Processing capacity, cybersecurity, compliance certification, and software licensing all carry costs that grow with transaction volume. Annual maintenance contracts escalate at 10-15% every year, and exchange rate depreciation raises the cost of imported technology. The path to lower per-transaction costs is real, but it requires sustained investment, and that investment must be funded.

Much of what appears as a bank fee also includes pass-through cost from international card networks and domestic payment infrastructure, with the bank’s own margin a small share. The path to lower fees runs through scale, and that scale requires sustained investment from all stakeholders.

Regulatory evolution is another key priority. Sri Lanka built a regulatory framework appropriate to crisis containment. The next phase needs frameworks calibrated for sustainable credit expansion: priority sector guidance, risk-weighted incentives for productive lending, and supervisory engagement that treats credit growth as part of the public good rather than only as a source of risk. Other emerging-market central banks have shown how this can be done without compromising stability.

At the same time, the trust customers place in their banks is earned daily, and as an industry, we should hold ourselves to the highest standards. Fee disclosure, grievance mechanisms, and the quality of service to retail and small business customers are areas where the sector can and should do more, and where my own institution is committed to continuous improvement.

A multi-pronged approach to progress

These focus areas must form a core part of our industry’s transformation agenda over the next decade, and each of them requires a banking sector that is well-capitalised and operationally strong. A weakly capitalised sector could not absorb concessional development funding at scale. It could not invest in inclusive digital infrastructure. It could not extend the kind of patient credit a recovery requires.

The country that emerged from sovereign default in 2023 is not the country Sri Lanka is meant to be. In the early 2000s, this was one of South Asia’s most promising emerging economies, with the human capital, geographic position, and institutional foundations to compete with any peer in the region.

The crisis may have interrupted that trajectory, but it did not erase it. How our industry moves forward will play a pivotal role in how rapidly we are able to recover, and build resilience in a new and extremely volatile moment in the global economic landscape.

The institutions that will carry that ambition forward have to be strong enough to bear the weight of it. Banks are among them. The question is not whether Sri Lanka can afford a strong banking sector. It is whether Sri Lanka can build the renewed economy it deserves without one.

By HNB MD/CEO, Damith Pallewatte

Dialog Axiata PLC announced its consolidated financial results for the quarter ended 31 March 2026 on Friday 15 May 2026. Financial results included those of Dialog Axiata PLC (the “Company”) and of the Dialog Axiata Group (the “Group”).

Group Performance

The Group delivered revenue growth of 9% Year on Year (“YoY”) on the back of strong performances in Mobile, Fixed and Digital Pay Television businesses as Group Revenue reached Rs 47.3Bn, despite the continued strategic scaling down of the low-margin international wholesale business. On a Quarter-on-Quarter (“QoQ”) basis, revenue increased by 2% supported by Data Revenue growth and advertising revenue generated by Television Business.

The Group Earnings Before Interest, Tax, Depreciation and Amortisation (“EBITDA”) was recorded at Rs 24.3Bn, up 23% YoY supported by Revenue performance and Cost Rescaling Initiatives. EBITDA margin expanded by 5.8pp YoY to reach 51.3%. On a QoQ basis Group EBITDA grew 5%.

Group Net Profit After Tax (“NPAT”) was recorded at Rs 9.2Bn for Q1 2026, up +>100% YoY and 56% QoQ, supported by robust EBITDA growth, lower net finance costs and lower forex losses.

Reflecting strong operational performance, the Group recorded Operating Free Cash Flow (“OFCF”) of Rs 14.6Bn for Q1 2026, up 8% YoY.

Interim Dividend to Shareholders

The Board of Directors of Dialog Axiata PLC approved an interim dividend for Q1 2026, after considering the financial performance of the Group and taking into account the forward investment requirements, at the meeting held on 14th May 2026. The approved first interim dividend for FY 2026 amounts to Rs 0.70 per share and would translate to an Annualized Dividend Yield of 9.2% based on share closing price for Q1 2026.

Company and Subsidiary Performance

At an entity level, Dialog Axiata PLC (the “Company”) continued to be the primary contributor to Group Revenue (76%) and Group EBITDA (75%). Supported by YoY growth in the Data segment and effective cost-rescaling initiatives, Company revenue for Q1 2026 increased by 12% YoY to Rs 36.0Bn, while EBITDA rose 29% YoY to Rs 18.2Bn. On a QoQ basis, Company revenue grew by 4% while EBITDA grew by 7% QoQ, primarily attributable to the flow-through impact of revenue growth and reduction in direct costs. Furthermore, NPAT for Q1 2026 was recorded at Rs 7.6Bn, up +>100% YoY. On a QoQ basis, Company NPAT grew 83% QoQ.

The balance of trade between Canada and Sri Lanka which is in Canada’s favour, could be developed more evenly by promoting to a greater extent trade, investment, tourism and business partnerships between the countries, Canadian Chamber of Commerce in Sri Lanka (CanCham SL) Secretary General Nilupul De Silva said.

‘CanCham SL was established as a dynamic platform to promote trade, investment, tourism and strategic business partnerships between Canada, Sri Lanka and the wider Indo-Pacific Region, Secretary General De Silva explained.

‘The Chamber aims to facilitate stronger commercial engagement while supporting sustainable economic growth and regional collaboration. More than 65 percent of the world’s population resides is in the region, she said at a media conference held at CanCham House, Horton Place recently.

The Secretary General added: ‘The Canadian High Commissioner to Sri Lanka serves as the Patron of CanCham SL, further reinforcing the Chamber’s commitment towards strengthening bilateral and regional economic cooperation.’

‘The Canadian Chamber of Commerce in Sri Lanka proudly participated in a historic milestone with the formal signing of a landmark MOU alongside all Canadian Chambers across the Indo-Pacific region, in the presence of the Canadian Prime Minister Hon. Mark Carney, she said.

‘The agreement signifies a new era of collaboration among the Canadian Chambers of the Indo-Pacific, with a strong focus on strengthening trade and investment ties, enabling strategic resource sharing, enhancing regional cooperation and fostering knowledge exchanges across member chambers and markets, founder and board member CanCham SL M.H.K.M Hammez said.

He said that PM Carney announced a Canadian commitment of CAD 0.5 trillion (CAD 500 billion) towards strengthening Canada’s economic relationship with the Indo-Pacific region over the next decade.

‘Subsequently Canada established a sovereign wealth fund with an allocation of Canadian dollars 25 billion to support long term strategic and international economic initiatives in the region, Hammez said.

‘The Chamber will work closely with business leaders, diplomatic missions, government institutions, investors and industry stakeholders to create meaningful opportunities for Canadian and Sri Lankan enterprises, he added.

‘Not having a permanent Sri Lankan High Commissioner for Canada is one of the biggest issues we are encountering. There is nobody to coordinate and communicate from that end, Hammez said.

‘CanCham is an independent entity trying its level best to promote certain priority development sectors in the country with Canadian support, he explained.

By Hiran H.Senewiratne.

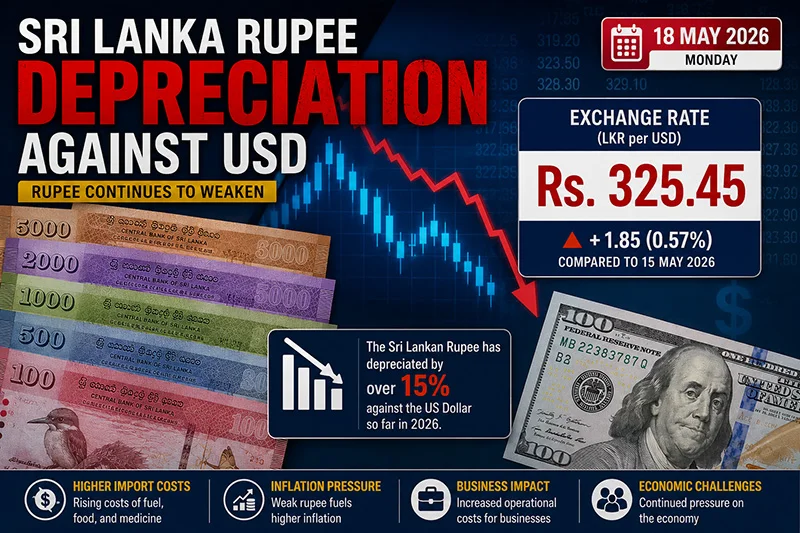

The continued depreciation pressure on the Sri Lankan rupee is exposing deep-rooted structural weaknesses within the economy, while simultaneously creating limited opportunities for export-oriented sectors, according to Rajkumar Kanagasingam.

Kanagasingam warned that while some export industries may temporarily benefit from a weaker currency, the broader economic strain caused by rising import costs, inflationary pressures, and investor uncertainty continues to weigh heavily on businesses and consumers alike.

Speaking to The Island Financial Review, he said local industries are struggling to absorb rising costs linked to imported raw materials, machinery, fuel, and intermediate goods as the rupee remains under pressure.

“Local industries are coping through cost-cutting measures, selective price increases, tighter inventory management, and delaying certain capital investments,” he said. “Many businesses are also exploring alternative suppliers and improving operational efficiency to manage rising import-related costs.”

He noted that import-dependent sectors are among the hardest hit by currency depreciation, particularly construction, transport, pharmaceuticals, manufacturing, and food imports, where businesses face mounting operational expenses and shrinking margins.

At the same time, Kanagasingam observed that export-oriented sectors such as apparel, tea, IT services, tourism, and businesses promoting local substitutes may gain some competitive advantage from the weaker rupee, as foreign exchange earnings translate into higher rupee revenues.

“A weaker rupee can improve the competitiveness of export-oriented sectors by increasing rupee earnings from foreign exchange,” he explained. “However, the benefits may be partially offset by higher imported input costs, energy expenses, and broader economic pressures.”

He stressed that small and medium-scale enterprises (SMEs) remain significantly more vulnerable than larger corporates during periods of currency instability.

“SMEs generally have limited financial buffers, less access to foreign currency, and weaker bargaining power,” he said. “Larger corporates are typically better positioned to manage exchange rate fluctuations through stronger reserves, export earnings, and diversified financing options.”

Kanagasingam added that consumers are ultimately carrying much of the burden created by rupee depreciation, with higher prices increasingly visible across food, transport, utilities, imported goods, and daily services.

“In many cases, increased business costs are gradually passed on to consumers,” he said, warning that sustained currency weakness could continue to fuel inflationary pressure across the economy.

He also pointed to a growing shift among local manufacturers toward localization and import substitution as businesses attempt to reduce reliance on imported inputs.

“There is growing interest in strengthening domestic supply chains and local production,” he noted. “However, Sri Lanka still faces challenges in terms of industrial scale, technology, and the availability of locally sourced raw materials.”

According to Kanagasingam, persistent currency volatility also undermines investor confidence and complicates long-term industrial planning.

“Currency fluctuations create uncertainty for investors, particularly in areas such as pricing, financing, debt servicing, and long-term project planning,” he said. “Greater exchange rate stability generally improves investor confidence and supports long-term industrial growth.”

He urged policymakers and the Central Bank to prioritize macroeconomic stability, foreign reserve strengthening, export expansion, energy efficiency, and targeted support for SMEs in order to cushion the impact of exchange rate volatility.

“The priority should be maintaining macroeconomic stability, strengthening foreign reserves, supporting export growth, improving energy efficiency, encouraging local production, and providing targeted support for SMEs,” he said. “Consistent and predictable policy measures are also essential to strengthen investor confidence.”

Kanagasingam further cautioned that prolonged rupee depreciation could eventually lead to job losses in sectors heavily dependent on imports.

“Prolonged depreciation could place pressure on import-dependent industries, potentially leading to reduced production, delayed expansion, and job losses, particularly among smaller businesses and vulnerable sectors,” he warned.

Describing the current exchange rate situation as more than a temporary market adjustment, Kanagasingam said Sri Lanka must address its long-standing structural vulnerabilities if it hopes to achieve lasting currency stability.

“It reflects both short-term external pressures and deeper structural challenges within the economy,” he said. “These include high import dependence, limited export diversification, debt-related pressures, and the need for stronger foreign exchange generation over the long term.”

Economic analysts note that the rupee’s trajectory in the coming months will remain closely tied to external debt management, reserve accumulation, export performance, remittance inflows, and broader investor sentiment surrounding Sri Lanka’s economic recovery efforts.

By Ifham Nizam

At least 100 dead in Ebola outbreak in DR Congo, official says

Trump says he called off new Iran attack at request of Gulf states

Lanka Premier League returns after two years, opener set for July 17

Cummins, Kishan, Klaasen power Sunrisers Hyderabad into playoffs; Chennai Super Kings not out yet

Mushfiqur ton, Litton and Joy fifties set Pakistan 437

Showers will occur at times in the Western, Sabaragamuwa, Central, North-western, Northern and Southern provinces and in Anuradhapura district

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoEx-SriLankan CEO’s death: Controversy surrounds execution of bail bond

-

Features2 days ago

Features2 days agoSri Lankan Airlines Airbus Scandal and the Death of Kapila Chandrasena and my Brother Rajeewa

-

News3 days ago

News3 days agoLanka’s eligibility to draw next IMF tranche of USD 700 mn hinges on ‘restoration of cost-recovery pricing for electricity and fuel’

-

Midweek Review6 days ago

Midweek Review6 days agoA victory that can never be forgotten

-

News2 days ago

News2 days agoKapila Chandrasena case: GN phone records under court scrutiny

-

Opinion5 days ago

Opinion5 days agoElectricity tariffs have skyrocketed: Can further increases be prevented?

-

Features4 days ago

Features4 days agoMysterious Death of United Nations Secretary General Hammarskjöld

-

News2 days ago

News2 days agoRupee slide rekindles 2022 crisis fears as inflation risks mount