Business

‘PUCSL electricity tariff revision is discriminatory’

Electricity tariff design must meet two main objectives: firstly, raising the money needed to pay for the costs of provision, and secondly, sending the right economic signals to each customer to favour the optimal socio-economic use of electricity.

To achieve the above objectives the principles that must be followed when designing tariffs are;

Economic sustainability or revenue sufficiency,

Equity or non-discrimination among users,

Economic efficiency in resource allocation, and

Transparency, simplicity, and stability of the methodology.

A well-defined and appropriate tariff structure must balance the financial sustainability of the sector on the one hand and the well-being of various segments of society on the other. The CEB’s tariff revisions seem to be mainly focused on the aspect of revenue sufficiency, ignoring the other aspects. As electricity is a commodity, there should be no difference in the prices charged to different users, except when reflecting any differences in the cost of providing services to different classes of users.

A differential tariff implies that some categories are subsidised leading to the question of who pays these subsidies. The current structure is such that households consuming an excess of 60 Kwh, and general purpose bulk supply users subsidise the industrial, hotel and charitable sectors.

Households that consume over 90 Kwh and general purpose bulk customers are charged a tariff that is double that of industries and hotels. With regards to hotels, in effect, domestic consumers subsidise foreign tourists. However, the differential tariff between general bulk supply and industrial/hotel users is meaningless. For example, a hall that hosts weddings and celebrations would be treated as a general bulk customer and be charged double the tariff that a hotel would be charged, even though both host similar events. A restaurant in a shopping mall would be charged as a general customer, but the same restaurant located within a hotel would enjoy a tariff half of that which a hotel incurs. While this differential existed under the previous tariff, it is made worse under the new structure; hotels faced a 10% increase in tariff while general users faced a 20% increase.

If the idea behind a lower tariff for hotels is to make the sector more competitive, then the solution is to address the causes of uncompetitiveness directly. One area is construction costs which raises the level of investment and the cost of maintenance. Protectionism for the domestic construction materials industry raises the costs of steel bars and rods, sanitary ware, aluminium extrusions, granite, electrical fittings, and carpets resulting in high overall construction cost. The effective protection granted on these items can exceed 200%; the savings in finance cost from a lower capital outlay would probably exceed the savings from a lower electricity tariff.

Economic value creation can take place in many different ways in an economy and the service sector is no less important than other sectors. The cross subsidisation between customers violates the equity or non-discrimination principle of a good tariff and discourages use by the overcharged and promotes overconsumption by the subsidised.

For example, the higher domestic tariff may serve as a disincentive for remote work. Remote or flexible work arrangements can reduce transport costs, congestion, energy use and for some, enable a better work/life balance. The government should be facilitating flexible work but the higher rates applicable to some domestic consumers may be a disincentive.

Economic activity is increasingly complex and a value chain can involve many different sectors. For example, the tea industry involves agriculture, processing in factories, transport, warehousing, blending, financing, marketing and exports. Moreover, products are now more knowledge intensive, so a greater part of the value addition arises in non-production-oriented components of the value chain. With differential tariffs, parts of the same value chain may pay different prices for use of the same commodity.

Further, a lower tariff to “industry” penalises new economy enterprises while promoting highly energy intensive users. This distorts resource allocation by encouraging excessive energy consumption, artificially promoting capital-intensive industries where the country may not have a clear comparative advantage. A subsidised tariff also blunts the incentive to economise.

The cost of supplying electricity fluctuates throughout the day, depending on the power generation mix, cost of fuels used, transmission costs and energy losses but as electricity storage is not economically viable, it has to be consumed whenever it is produced. Households with rooftop solar thus enjoy a subsidy. Domestic solar generation takes place in day time where the cost of generation is low but the import of electricity to the house takes place at night when the cost of generation is high. Offsetting units generated against units imported results in a subsidy because of the difference in costs between the two. Time of use metres should be mandated for all domestic users on net metering with the import/export being accounted for on the respective time of use tariff. Indeed all users who consume above 60 Kwh should move to the time of use tariff.

Should the government decide to subsidise the capital or operating costs to serve certain customer classes, it should do so directly from the budget and while a lifeline tariff for the poor is justified the high domestic users pay a tariff 7.4x that of the lowest. Not all households are the same size and an extended family living in a single house may face a much higher tariff although their income level may not differ greatly from the average.

The PUCSL should review tariffs to prevent the distortions highlighted above. Instead of cross-subsidies, the regulator should be working to reduce overall cost of the provision of electricity through better procurement and greater efficiency.

Treating all costs as a pass-through in computing the tariff is a mistake. The PUCSL needs to set efficiency targets in order to set fair and reasonable tariffs. The CEB should be incentivised to control its costs by specifying and enforcing performance requirements. Benchmarking CEB performance against regional and international peers to assess relative efficiency is necessary, as is consulting stakeholders on achievable efficiency targets.

Advocata is an independent policy think tank based in Colombo, Sri Lanka. We conduct research, provide commentary and hold events to promote sound policy ideas compatible with a free society in Sri Lanka. Visit advocata.org for more information.

Advocata spokespersons are available for live and pre-recorded broadcast interviews via 0774858401

CONTACT:

Subashini Kaneshwaren,

Senior Communications Executive, Advocata Institute

Email: subashini@advocata.org

The Asian Development Bank is no longer treating digitalisation as a secondary development theme. Increasingly, the bank views digital infrastructure as the economic nervous system of Asia’s future growth model – a strategic national asset now considered as critical to economic competitiveness as highways, ports, and power grids.

That shift carries an important message for countries like Sri Lanka: modernise digital systems rapidly or risk falling behind regional competitors.

This was among the clearest signals emerging from the 59th Annual Meeting of the ADB held in Samarkand from May 3 to 6, where digital connectivity and technology-driven growth dominated many of the bank’s strategic discussions.

The ADB is steadily repositioning itself from being primarily a traditional infrastructure lender into a major catalyst for digital transformation across Asia and the Pacific. At multiple forums in Samarkand, bank officials and sector experts repeatedly stressed that digital connectivity is no longer simply a technology issue. It is now deeply tied to productivity, governance, financial inclusion, education, healthcare, climate resilience, and regional economic integration.

A key figure driving this agenda is Antonio García Zaballos, Director of the Digital Sector Office at the ADB. Widely recognised for his expertise in telecommunications regulation and broadband policy, Zaballos emphasised that digital infrastructure should be treated as essential national infrastructure rather than a luxury service.

Under the ADB’s Strategy 2030 framework and subsequent policy reviews, digital transformation has emerged as one of Asia’s defining development priorities. The bank’s digital agenda now broadly focuses on expanding broadband access, building digital public infrastructure, supporting e-governance, promoting fintech and digital payments, strengthening cybersecurity, developing AI-ready economies, and advancing regional digital integration.

Discussions in Samarkand also highlighted a persistent reality: despite rapid mobile and internet growth across Asia, the region’s digital divide remains severe. Millions in rural communities, small businesses, and low-income populations still lack affordable and reliable digital access. For the ADB, digitalisation is therefore not merely an innovation agenda, but also an inclusion challenge.

One of the strongest indications of the bank’s ambitions came with the announcement of a regional connectivity initiative involving energy and digital infrastructure investments worth up to US$70 billion by 2035. A central component is the proposed “Asia-Pacific Digital Highway” – a major initiative aimed at expanding fibre-optic networks, satellite systems, and regional data centres.

ADB President Masato Kanda observed that energy and digital access would ‘define the region’s future,’ while emphasising that cross-border digital networks could reduce costs and widen economic opportunity across Asia and the Pacific.

Zaballos and other ADB officials also stressed the importance of regulatory modernisation, public-private partnerships, and regional coordination to build stronger broadband ecosystems. Their policy focus increasingly includes affordable internet access, cybersecurity frameworks, digital public infrastructure, cross-border data governance, and digital inclusion for underserved populations.

Another major pillar of the ADB’s strategy involves digital economy agreements and harmonised regional regulations. According to ADB research released in 2025, digital trade, AI governance, cross-border payments, and cybersecurity standards are rapidly becoming central to regional economic integration.

The bank increasingly sees fragmented digital regulations as a growing obstacle to regional commerce. As a result, it is promoting interoperable payment systems, common digital standards, regional cybersecurity cooperation, and coordinated cross-border data governance frameworks.

This has particular relevance for South Asia, where digital fragmentation still limits deeper regional trade integration.

For Sri Lanka, the implications are significant. Although the country enjoys relatively high mobile penetration and comparatively strong digital literacy, major gaps remain in rural broadband access, government digital integration, SME digitalisation, cybersecurity preparedness, and digital export competitiveness.

ADB’s growing emphasis on digital public infrastructure and regional connectivity could align closely with Sri Lanka’s ambitions to expand fintech services, IT exports, e-governance systems, and digital entrepreneurship.

The larger question now is whether policymakers – particularly the Ministry of Digital Economy – can move quickly enough to position Sri Lanka within this rapidly evolving regional digital architecture. In Asia’s next development cycle, digital readiness may well determine which economies move ahead – and which are left struggling to catch up.

By Sanath Nanayakkare

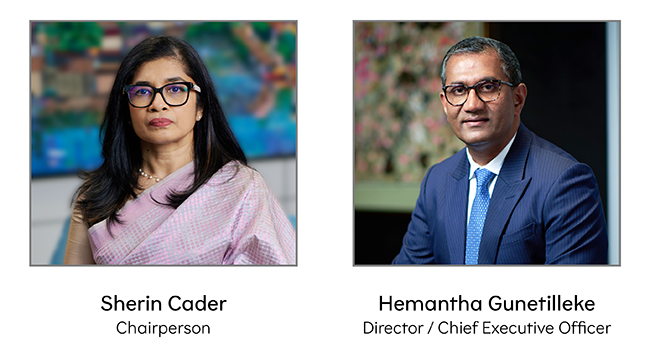

Nations Trust Bank PLC (NTB) commenced the financial year on a positive note, delivering a strong performance for the three months ended 31st March 2026, with a Profit After Tax (PAT) of LKR 4.6Bn, marking a 12% yearonyear increase. The results were supported by steady asset growth, stable Net Interest Margins (NIMs), and prudent risk management, reflected in a low Net Stage 3 Ratio of 1.10%. A robust capital position further supported the Bank’s performance, with Return on Equity (ROE) reaching 18.98%, indicating the Bank’s continued momentum and a positive outlook for growth in the year ahead.

Nations Trust Bank, Director and Chief Executive Officer, Hemantha Gunetilleke, stated,

“The Bank’s performance in 1Q 2026 highlights its strength and the progress of its strategy as we move into the next phase of growth. This is reflected in the expansion of our loan book and our continued focus on supporting customers across consumer, commercial and corporate segments. In doing so, the Bank has contributed to broader economic growth in Sri Lanka, supporting investment and expansion across key sectors. As we further strengthen our capital and liquidity positions, we remain focused on delivering value through high service standards, improved digital capabilities, and a strong customer focus.”

Business

LOLC Life Assurance expands branch network to strengthen customer accessibility and service excellence

LOLC Life Assurance continues to reinforce its commitment to delivering accessible, customer-centric life insurance solutions through the strategic expansion of its branch network across key locations in Sri Lanka. The recent opening of new branches in Mathugama and Beruwala marks a significant milestone in enhancing customer accessibility, improving service convenience, and delivering inclusive insurance protection across these strategically important key regional markets.

This expansion reflects the company’s continued focus on bringing life insurance services closer to customers, ensuring greater convenience, improved responsiveness, and stronger community-level engagement. By strengthening its physical presence, LOLC Life Assurance aims to provide personalised support and seamless access to its comprehensive range of life protection and investment solutions.

The new Beruwala branch, located at No. 207, Galle Road, Beruwala, and the Mathugama branch, located at No. 110/1, Aluthgama Rd, Mathugama were officially opened by Mr. Jayantha Kalinga, Chief Operating Officer of LOLC Life Assurance together with the company’s senior management team. As a trusted life insurer in Sri Lanka, LOLC Life Assurance remains committed to innovation, superior customer experience, and inclusive financial protection, further strengthening its vision of becoming a lifelong partner that offers security, care, and confidence at every stage of life.

The relocation of the Jaffna branch to No 62/3, Stanley Road, Jaffna reflects the company’s ongoing efforts to optimise its branch network through improved infrastructure and enhanced accessibility. The branch was officially reopened in the presence of Mr. Chandana L. Aluthgama, Executive Director and Mr. Jayantha Kalinga, Chief Operating Officer of LOLC Life Assurance, providing a more modern and customer-friendly environment aligned with the region’s growing economic activity. The upgraded facility is expected to further enhance customer experience by ensuring efficient access to the company’s full suite of life insurance solutions.

Sri Lanka’s World Cup winning team conduct coaching session in KL

Fatima Sana smashes fastest fifty in women’s T20Is

On the hunt for China’s most famous green tea

Marsh onslaught, Akash three-for dent Chennai Super King’s playoffs chances

ICC suspends funding to Cricket Canada over governance-related issues

Showers will occur at times in the Western, Sabaragamuwa, Central, North-western and Northern provinces and in Anuradhapura, Galle and Matara districts

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News7 days ago

News7 days agoLanka Port City officials to meet investors in Dubai

-

News4 days ago

News4 days agoEx-SriLankan CEO’s death: Controversy surrounds execution of bail bond

-

Features5 days ago

Features5 days agoWhen University systems fail:Supreme Court’s landmark intervention in sexual harassment case

-

Features5 days ago

High Stakes in Pursuing corruption cases

-

Midweek Review4 days ago

Midweek Review4 days agoA victory that can never be forgotten

-

Features7 days ago

Features7 days agoServing as MR’s Deputy Finance Minister and the travel the job entailed

-

Features7 days ago

Features7 days agoBengal Turns BJP, Didi Falls

-

News6 days ago

News6 days ago150th anniversary celebrations of Ave Maria Convent, Negombo