Business

Union Assurance study reveals low saving patterns among Sri Lankans

Leading Life Insurer, Union Assurance commissioned a research study with the expertise from pioneer in the market and social research, Survey Research Lanka, with the objective of better understanding the savings and retirement habits of Sri Lankans in order to encourage healthy savings for a financially secure future. The research was further validated by Prof. K.A.P. Siddhisena, Emeritus Professor of the Faculty of Arts, University of Colombo.Union Assurance takes pride in launching this study to uncover valuable insights and information.

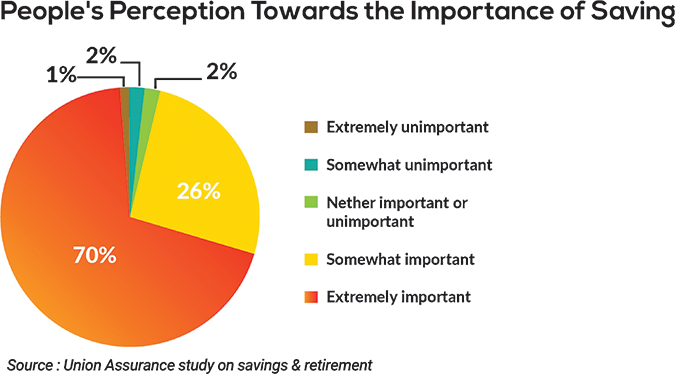

The data collection period for the study was post-covid and pre-crisis, and the sample size was 1,004 people from 9 provinces in Sri Lanka.According to the study findings, people have a positive attitude towards saving for the future. An overwhelming 70% of respondents believe that retirement savings are extremely important. However, only 27% of them save an adequate amount, while 21% have no savings yet.Current Saving % from Gross Salary for the Future

The amount saved by Sri Lankans generally falls well below 10-15% of one’s gross salary recommended by financial planners (CNBC, 2019). According to the study, nearly one-quarter of the population has no future savings, while 37% save only between 1% and 5% of their income (which is insufficient). As shown, only 20% of the population has a healthy saving pattern as it is in line with expert opinions on saving above 10%.It is indeed regrettable that only 48% of respondents said they have a plan to save for the future.

Pandemic Impact on Saving

A significant impact was evident between income earned and saving patterns. As many as 40% of respondents stated that their income decreased to a greater extent, while 49% stated the same about their savings. Only 20% experienced no change in income or savings.

Trust in Life Insurance Companies More interesting insights gained on trust levels in Life insurance companies as a source of future savings. While 13% said their trust level is extremely high, 41% said their trust level is somewhat high. Therefore, over 50% of the population has high levels of trust in Life insurance.

Financial Safety Net

Life Insurance offers a financial safety net for citizens, particularly during tough times. The stability of your future is largely dependent on your savings. Life Insurance ensures that policyholders and their families are continuously protected.

It is unfortunate that Sri Lanka’s household savings rate has steadily declined over the last decade (World Bank, 2021). This is particularly worrying since 12.3% of the population is aged 60 or older, making it the country with the fastest ageing populations in South Asia (World Bank, 2021). Therefore, income insecurity in old age is going to be a serious issue in the future. Hence, there is a need to encourage people to invest in insurance plans offered by Life insurance companies.

In conclusion,

Saving money is important to ensure a secure financial future. Setting a saving target helps indicate how much one should save over time for their future. The sooner one starts saving and investing, the greater the long-term benefit.

Visit www.unionassurance.com for the full report.

If the price of oil hits $150 a barrel it will trigger a global recession, the boss of US financial giant BlackRock has told the BBC.

Larry Fink, who leads the world’s largest asset manager, said if Iran “remains a threat” and oil prices stay high it will have “profound implications” for the world economy.

In a wide-ranging exclusive interview, he also denied there was an AI bubble, although he said the new technology meant too many people were pursuing university degrees and not enough doing technical training.

BlackRock is a financial colossus, controlling assets worth $14 trillion (£10.5tn), and is one of the biggest investors in many of the world’s largest companies.

Its size and spread gives Fink – who is one of the eight co-founders of the business, which started in 1988 – a unique insight into the health of the global economy.

The conflict in the Middle East has triggered wild moves on financial markets as people try to assess what will happen to energy costs.

For Fink, it is too early to determine the ultimate scale and outcome of the conflict, but he believes it will be one of two extreme scenarios.

In one, if the conflict is settled and Iran becomes a country that can be accepted again by the international community then the price of oil could fall back to below where it stood before the war.

But if not, he says, then there could be “years of above $100, closer to $150 oil, which has profound implications in the economy” and an outcome of “a probably stark and steep recession”.

The surge in energy costs has led to some in the UK to argue that it should be focusing more on producing its own oil and gas.

On Tuesday, industry body Offshore Energies UK said that without more domestic production, the country risks becoming reliant on imports “at a time of rising global instability”.

Fink says countries need to be pragmatic about their energy mix by using all sources available to them, but providing cheap energy is key to driving growth and raising living standards.

“Rising energy prices is a very regressive tax. It affects the poor more than the wealthy.”

While the UK already has some solar and wind power and hydrocarbons, if oil prices were to rise to $150 for three or four years, “you would have so many countries moving so rapidly towards solar and maybe even wind”.

Countries should not depend on just one source, he says.

“Use what you have unquestionably, but also aggressively move towards alternative sources too.”

Some analysts have suggested that there are some echoes of the run-up to the 2007-08 financial crisis in the markets at the moment.

Energy prices are surging and some have flagged signs of cracks in the financial system. BlackRock itself is one of several firms to have limited withdrawals by nervous investors from private credit funds.

But Fink is adamant there is no chance of a repeat of the financial trauma seen in 2007-08, when several banks around the world collapsed or had to be rescued, as he believes financial institutions today are more secure.

“I don’t see any similarities at all,” he says. “Zero.”

The issues affecting some funds account for a small fraction of the overall market and investment from institutions remains strong, he says.

Fink also rejects suggestions that the surge in investment in AI, which has seen billions of dollars invested in the new technology, has been overblown.

“I do not believe we have a bubble at all,” he says.

“Could we have one or two failures in AI? Sure, that I’m fine with.”

Last year, BlackRock was part of a consortium that bought one of the world’s largest data centre providers, Aligned Data Centres, in a $40bn deal.

“I believe there’s a race for technology dominance. I believe that if we do not invest more, China wins. I believe it’s mandatory that we are aggressively building out our AI capabilities.”

The biggest issue he feels that is hindering the expansion of AI in the US and Europe is the cost of energy.

While China is investing hugely in solar and nuclear power, in Europe “I just see a lot of talk and no action”, he says, while in the US “as much as we are energy independent, we better start focusing on solar… because we need to have cheap, inexpensive power to move into AI”.

Earlier this week, in his annual letter to shareholders, Fink said the boom in artificial intelligence risked widening inequality, with only a small number of firms and investors seeing the benefits.

However, speaking to the BBC, he emphasised AI was going to create an “enormous amount of jobs”.

He said that in his letter he had written about how many jobs would be created “related to electricians and welders and plumbers”.

In contrast, there might not be as much demand for some office jobs as AI evolves and this could lead to a rethink about what roles are needed as “society is changing and evolving”.

“We really put judgement on so many jobs and so many people who probably should not have gone into banking or media or law, [who] probably should have been a great worker with their hands, and we need to now rebalance that approach,” he says.

In the US, he says, after World War Two “we built the foundation of education, and we said to all the young people, go to college, go to college, go to college. And we probably overdid it”.

“We need to balance that out, and we need to be proud that… a career can be just as strong in these fields of plumbing and electricians.”

(BBC)

Mahindra Ideal Finance Limited (MIFL) has announced the successful conclusion of its debut Rs 1 Billion debenture issue, which was oversubscribed on the first day of opening, marking a significant capital market milestone for one of Sri Lanka’s fastest-growing licensed Non-Banking Financial Institutions.

The Issue comprised up to Ten Million (10,000,000) Tier 2, Listed, Rated, Unsecured, Subordinated, Redeemable Debentures at a par value of LKR 100 per Debenture, raising up to Sri Lanka Rupees One Thousand Million (LKR 1,000,000,000), with a five-year tenure maturing in 2031.

Commenting on the outcome, MIFL Managing Director/CEO, Mufaddal Choonia said the proceeds of the Company’s inaugural debenture issue will be deployed to strengthen lending capacity across its core business segments, including vehicle leasing, gold loans, SME loans, and business loans.

“The success of our first debenture issue is testament of our performance so far and speaks of the confidence that investors have placed in our future growth story. The strong market response is also the best validation we can secure from the investor community on the strong fundamentals that underpin our business. We will honor that trust by deploying these funds to further provide accessible credit to enrich the lives of our customers and for the communities we serve.”

The capital raise also strengthens the Company’s Tier 2 capital base in compliance with the Central Bank of Sri Lanka’s Capital Adequacy Requirements.

The Debentures were offered in two structures — Type A, at a fixed rate of 12.00% per annum payable annually, and Type B, at a floating rate of the 364-Day Treasury Bill rate plus 3.50% per annum payable semi-annually.

The Issue carried a credit rating of A (lka) from Fitch Ratings Lanka Limited, with MIFL holding an entity rating of AA-(lka) with a Stable Outlook. The Issue was managed by NDB Investment Bank Limited, with Bank of Ceylon serving as Joint Placement Agent. (MIFL)

The Securities and Exchange Commission of Sri Lanka (SEC) and the Colombo Stock Exchange (CSE) jointly organized an awareness session recently, for auditors of companies which are currently on the CSE Watchlist. The session focused on enhancing awareness of enforcement actions and timelines, reducing prolonged Watchlist durations, and fostering a more coordinated regulatory approach among regulators, auditors, and listed companies.

Addressing the session, the Chairman of the SEC, Senior Prof. D.B.P.H. Dissabandara highlighted the core professional virtues of an auditor drawing from his own career beginnings, “At the heart of every auditor’s role lies three virtues: integrity, objectivity and confidentiality.” He reminded the gathering, that while an auditor may formally be recognized as a supplementary service provider under the SEC Act, their true value runs far deeper. Every time a listed company submits its financial statements, it is the auditor’s opinion that gives investors the confidence to trust those numbers. In that sense, auditors are not just ticking a regulatory box, they are the ones holding the line on transparency.

Senior Prof. D.B.P.H.

Dissabandara

Further, Professor Dissabandara drew attention to the current Watchlist situation, noting that while the inclusion of certain companies on the Watchlist is an appropriate regulatory measure, their prolonged presence on the Watchlist may send adverse signals to investors. He called for a structured connected approach involving auditors and listed company management to ensure incremental progress towards resolving Watchlist triggers, particularly those arising from going concern issues and the non-submission of financial statements.

The Head of Listed Entity Compliance at the CSE, Kassapa Weerasekara delivered a presentation focused on enforcement actions that can lead to securities being transferred to the watchlist. Weerasekara reminded the gathering “If companies take the right steps and obtain independent verification on the resolution of all matters giving rise to Modified Opinion and Emphasis of Matter on Going Concern, their securities can be fully reinstated.” He closed by emphasizing that the process is designed to give companies a fair and structured opportunity to correct course.

Russia launches 948 drones at Ukraine in largest attack over 24-hour period

Oil at $150 will trigger global recession, says boss of financial giant BlackRock

Showers will occur at several places in the Western and Sabaragamuwa provinces and in Galle and Matara districts after 2.00 pm

Senior citizens above 70 years to receive March allowances on Thursday (26)

CEB Engineers warn public to be prepared for power cuts after New Year

Japanese boost to Sri J’pura Hospital, an outright gift from Tokyo during JRJ rule

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features2 days ago

Features2 days agoTrincomalee oil tank farm: An engineering marvel

-

News6 days ago

News6 days agoBailey Bridge inaugurated at Chilaw

-

News5 days ago

News5 days agoCIABOC tells court Kapila gave Rs 60 mn to MR and Rs. 20 mn to Priyankara

-

News6 days ago

News6 days agoPay hike demand: CEB workers climb down from 40 % to 15–20%

-

Features5 days ago

Features5 days agoScience and diplomacy in a changing world

-

News4 days ago

News4 days agoColombo, Oslo steps up efforts to strengthen bilateral cooperation in key environmental priority areas

-

News2 days ago

News2 days agoSubstandard coal deepens energy crisis, warns former CEB Chief

-

Features6 days ago

Features6 days agoIllegal solar push ravages Hambantota elephant habitat: Environmentalist warns of deepening crisis