Business

Union Assurance study reveals low saving patterns among Sri Lankans

Leading Life Insurer, Union Assurance commissioned a research study with the expertise from pioneer in the market and social research, Survey Research Lanka, with the objective of better understanding the savings and retirement habits of Sri Lankans in order to encourage healthy savings for a financially secure future. The research was further validated by Prof. K.A.P. Siddhisena, Emeritus Professor of the Faculty of Arts, University of Colombo.Union Assurance takes pride in launching this study to uncover valuable insights and information.

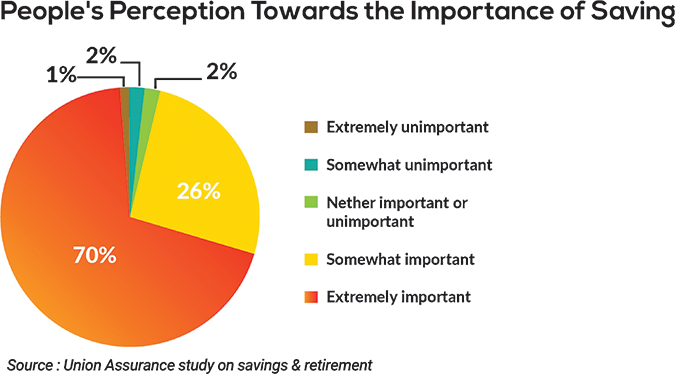

The data collection period for the study was post-covid and pre-crisis, and the sample size was 1,004 people from 9 provinces in Sri Lanka.According to the study findings, people have a positive attitude towards saving for the future. An overwhelming 70% of respondents believe that retirement savings are extremely important. However, only 27% of them save an adequate amount, while 21% have no savings yet.Current Saving % from Gross Salary for the Future

The amount saved by Sri Lankans generally falls well below 10-15% of one’s gross salary recommended by financial planners (CNBC, 2019). According to the study, nearly one-quarter of the population has no future savings, while 37% save only between 1% and 5% of their income (which is insufficient). As shown, only 20% of the population has a healthy saving pattern as it is in line with expert opinions on saving above 10%.It is indeed regrettable that only 48% of respondents said they have a plan to save for the future.

Pandemic Impact on Saving

A significant impact was evident between income earned and saving patterns. As many as 40% of respondents stated that their income decreased to a greater extent, while 49% stated the same about their savings. Only 20% experienced no change in income or savings.

Trust in Life Insurance Companies More interesting insights gained on trust levels in Life insurance companies as a source of future savings. While 13% said their trust level is extremely high, 41% said their trust level is somewhat high. Therefore, over 50% of the population has high levels of trust in Life insurance.

Financial Safety Net

Life Insurance offers a financial safety net for citizens, particularly during tough times. The stability of your future is largely dependent on your savings. Life Insurance ensures that policyholders and their families are continuously protected.

It is unfortunate that Sri Lanka’s household savings rate has steadily declined over the last decade (World Bank, 2021). This is particularly worrying since 12.3% of the population is aged 60 or older, making it the country with the fastest ageing populations in South Asia (World Bank, 2021). Therefore, income insecurity in old age is going to be a serious issue in the future. Hence, there is a need to encourage people to invest in insurance plans offered by Life insurance companies.

In conclusion,

Saving money is important to ensure a secure financial future. Setting a saving target helps indicate how much one should save over time for their future. The sooner one starts saving and investing, the greater the long-term benefit.

Visit www.unionassurance.com for the full report.

Business

Sri Lanka Climate Summit flags need to ‘mainstream climate action into country’s growth story’

Sri Lanka has reached a critical juncture where climate action must evolve from policy discussions into tangible investments capable of driving economic growth, strengthening competitiveness and attracting international capital, speakers at the second Sri Lanka Climate Summit 2026 organised by the Ceylon Chamber of Commerce said.

Held under the theme “From Risk to Opportunity: Mainstreaming Climate Action into Sri Lanka’s Growth Story,” the summit at Taj Samudra yesterday brought together policymakers, multilateral agencies, financiers and private sector leaders to assess whether Sri Lanka is climate-ready for investment and how climate resilience can be transformed into an economic advantage.

Delivering the welcome address, Chairman of the Ceylon Chamber of Commerce, Krishan Balendra, said climate action could no longer be treated as a separate sustainability agenda.

“As Sri Lanka enters its next phase of economic growth and recovery, climate action must become part of our competitiveness agenda, our investment agenda and ultimately our national growth story, Balendra said.

He noted that since the inaugural Climate Summit in 2024, the Chamber had moved beyond advocacy to practical implementation through initiatives promoting Environmental, Social and Governance (ESG) practices, climate disclosures, green innovation and public-private collaboration.

The Chamber has also established a public-private working group jointly led by the Ministry of Environment and the Chamber to support implementation of Sri Lanka’s Nationally Determined Contributions (NDCs) and emerging carbon market frameworks.

Environment Minister Dr. Dhammika Patabendi, delivering the keynote address titled “Sri Lanka’s Climate State of the Nation 2026, said the government was positioning climate resilience as a cornerstone of economic transformation.

“We are working directly with the Chamber to transform global climate risks into Sri Lanka’s greatest competitive advantages, the minister said.

He highlighted landmark amendments to the National Environment Act aimed at modernising environmental governance while providing greater certainty to investors.

According to Patabendi, the reforms would shift environmental compliance from a reactive and punitive model to a proactive framework that provides businesses with greater operational clarity before projects commence.

The minister also stressed that environmental compliance is increasingly becoming a prerequisite for access to premium export markets.

“Enhanced environmental standards act as an economic shield for our exporters, validating the ‘Made in Sri Lanka’ brand as an ethically secure, low-carbon choice, he said.

Patabendi reaffirmed Sri Lanka’s comm

itment to achieving 70 percent renewable energy generation by 2030 and carbon neutrality by 2050, while highlighting significant opportunities in wind energy development, including an estimated 56 gigawatts of offshore wind potential.

Vimlendra Sharan, FAO Representative for Sri Lanka and the Maldives, described Sri Lanka as a country that is simultaneously “climate vulnerable and climate ambitious.”

“The real question is whether Sri Lanka is climate investment ready. That journey has only just begun, Sharan observed.

He argued that climate readiness required transforming vulnerabilities and ambitions into structured, financeable and scalable investments.

One of the country’s biggest challenges, according to Sharan, is the limited pipeline of bankable climate projects.

“The major gap is the lack of investment-ready projects. We also need stronger project preparation capacity, more data and better evidence to unlock larger volumes of climate finance, he said.

Speakers agreed that climate resilience is no longer merely an environmental issue but an economic imperative affecting trade, investment flows, supply chain access and long-term growth prospects.

By Ifham Nizam

A leading Australia-based sustainable energy solutions company, ‘365 Future Energy’, is now exploring possibilities to enter Sri Lanka to provide sustainable energy solutions to Sri Lanka at affordable prices.

‘365 Future Energy’ CEO, Isuru Yapa, together with internationally recognized energy technology entrepreneur Ludovico Finotto,visited Sri Lanka this week.

” If we could set up this plant here it would benefit Sri Lanka because it could store sustainable energy to stabilise the national grid, supply energy at an affordable operational cost and manage the energy supply system in a more stable manner, Ludovico Finotto, founder and CEO of ‘QiOn Technologies’ a globally recognized innovator in the energy, automotive and high-performance electronics sectors, said.

With over 18 years of international experience, Finotto has played a leading role in advanced developments related to electric mobility, energy storage, charging infrastructure, hydrogen technologies, marine electrification and smart energy systems in more than 24 countries.

Speaking to the Island Financial Review he said that the purpose of this strategic visit is to explore sustainable energy solutions, evaluate emerging opportunities within Sri Lanka’s energy sector and identify potential investment and technology partnerships that can contribute to the country’s future energy transformation.

‘365 Future Energy’ is focused on delivering innovative and environmentally responsible energy solutions, supporting the global transition toward renewable and sustainable power infrastructure. Through this visit, the company aims to better understand Sri Lanka’s growing energy demands and assess opportunities for collaboration in renewable energy technologies, energy storage systems, EV charging infrastructure and next-generation sustainable energy developments.

‘365 Future Energy’ believes Sri Lanka holds strong potential for future-focused sustainable infrastructure projects and clean energy investments. The company’s leadership team will engage with local stakeholders, businesses, and industry representatives during the visit to discuss opportunities for innovation, energy efficiency, and long-term sustainable growth, company sources said.

By Hiran H Senewiratne

Celebrating the spirit of Vesak, Serendib Flour Mills served the community through a Tea Bun Dansala and Plain Tea Dansala held near the Orugodawatta Bridge on 29 May 2026, distributing 12,500 buns and 12,500 cups of tea to devotees and members of the public.

The Dansala commenced with the blessings and presence of a venerable monk, reflecting the values of compassion, generosity and service that define Vesak. The initiative was carried out through the collective commitment of the Serendib Flour Mills team, who came together to serve the community and support those observing the sacred occasion.

Through this initiative, Serendib Flour Mills reinforced its belief that nourishment extends beyond food, living in the kindness shared, the relationships built and the communities uplifted. Guided by its purpose of “Nourishing the Nation,” the company remains committed to creating nourished futures through meaningful acts of service and care.

Formulation of a Draft Economic Development Bill to expedite the process of Digital Transformation and Digital Economic Development

Cabinet approval for Sri Lanka Community and Health Survey – 2026/2027

A National Water Tariff Policy for all Water Supply and Sanitation Services

National Policy on Green Hydrogen in Sri Lanka

Cabinet nod to amend the Customs Ordinance

Cabinet nod to submit the Anti-Corruption (Declaration of Assets and Liabilities through Centralized Electronic System) Regulations 2026, made under Section 156 of the Anti-Corruption Act, No.9 of 2023, for approval by Parliament

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Latest News6 days ago

Latest News6 days agoKusal Mendis, Pathum Nissanka, bowlers put Sri Lanka 1-0 up

-

News6 days ago

News6 days agoNew US tariffs proposed on 60 countries, including Sri Lanka

-

Features5 days ago

Features5 days agoPower crept into the Sangha and is now tearing it apart

-

Features5 days ago

Features5 days agoKondachchi wind farm and battery storage project to boost energy security, says Power Ministry Secretary

-

Features5 days ago

Features5 days agoSaudi Arabia sets new benchmark in Hajj management as 1.7 million pilgrims complete sacred journey

-

News3 days ago

News3 days agoWomen’s T20 World Cup 2026 warm-up: Chamari Athapaththu’s 94 helps Sri Lanka beat Pakistan

-

News4 days ago

News4 days agoAsst. Manager, security officer arrested over Rs 30 mn snatch at Horana PB branch

-

Editorial2 days ago

Editorial2 days agoProbe Sallay’s complaint