Business

Reform or perish, it’s not too late

Sri Lankan economy in historic crisis

By K.D.D.B Vimanga and Naqiya Shiraz

The Sri Lankan economy faces a historical crisis. The root causes are the twin deficits. First, the persistent fiscal deficit – the gap between government expenditure and income. Second, the external current account deficit – the gap between total exports and imports. The problems have been festering for too long. Without urgent reforms, the crisis could easily morph into a full-blown debt crisis.

Sovereign debt workouts are extremely painful for citizens. A mangled debt restructuring can perpetuate the sense of crisis for years or even decades. A return to normal economic activity may be delayed, credit market access frozen, trade finance unavailable.

With the global pandemic, these are unusual and difficult times. The next five years are going to be crucial for the country. The problems can no longer be avoided and should be faced squarely. The journey ahead is going to be painful but the longer these are delayed the worse the problem becomes and the magnitude of the damage compounds.

With the global pandemic, these are unusual and difficult times. The next five years are going to be crucial for the country. The problems can no longer be avoided and should be faced squarely. The journey ahead is going to be painful but the longer these are delayed the worse the problem becomes and the magnitude of the damage compounds.

State of the Economy

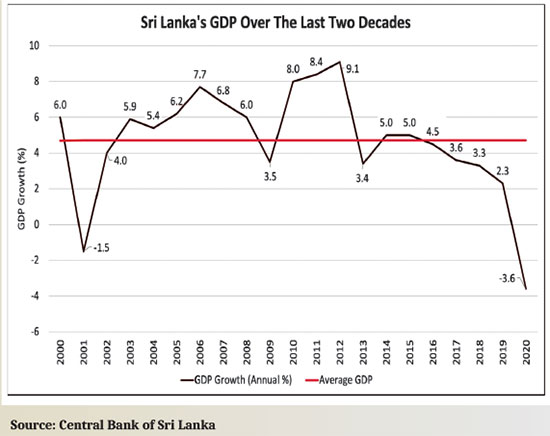

The new government inherited a fragile economy, battered by the Easter attacks of 2019, the constitutional crisis of October 2018 and the worst drought in 40 years in 2017. With the pandemic in 2020 Sri Lanka’s economy shrank by 3.6% with all sectors of the economy contracting.

Yet, the pandemic is not the sole cause – it only accelerated the decline of Sri Lanka’s economy that was weak to begin with. The country has long been plagued by structural weaknesses, with growth rates in the last few years even below the average growth rate during the war. Mismanaged government expenditure coupled with a long term decline in revenue have characterised Sri Lanka’s fiscal policy. As of 2020 total tax as a percentage of GDP fell to just 8%, while recurrent expenditure increased.

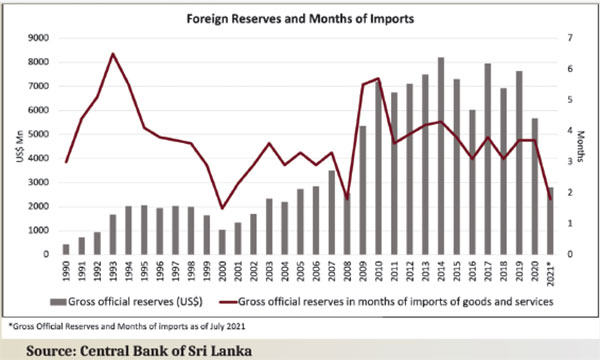

Borrowing to finance the persistent budget deficits is proving to be unsustainable. Total government debt rose to 101% of GDP in 2020 and has grown since. Sovereign downgrades have shut the country from international debt markets. The foreign reserves declined from US$ 7.6 bn in 2019 to US$ 5.7bn at the end of 2020 and to US$ 2.8 bn by July 2021. This level of reserves is equivalent to less than two months of imports. With future debt obligations also in need of financing, the situation is dire.

The import restrictions placed to combat this foreign exchange crisis have failed to achieve their purpose and are doing more harm than good. imports rose 30% in the first half of 2021 compared to 2020 despite stringent restrictions.

The problem lies not in the trade policy but in loose fiscal and monetary policy that has increased demand pressures within the economy, drawing in imports and leading to the balance of payments crisis and consequently the depreciation of the currency.

Measures by the Central Bank to address this by exchange rate controls and moral suasion have caused a shortage of foreign currency leading to a logjam in imports.

Fundamental and long-running macroeconomic problems were intensified by the pandemic.Import restrictions, price and exchange controls do not address the real causes.

Treating symptoms instead of the underlying causes is a recipe for disaster.

The continuation of such policies will lead to the deterioration of the economy, elevate scarcities, disadvantage the poor who are more vulnerable and in the long run lead to even higher prices and lower output due to lack of investment.

Sri Lanka’s GDP growth over the last decade has been alternating between short periods of high growth and prolonged periods of low growth. This is a result of the state-led, inward looking policies of the last decade.

A comprehensive reform agenda must be built around five fundamental pillars:

i) fiscal consolidation – The need to manage government spending within available resources and to reduce debt are paramount. Revenue mobilization must improve but the control of expenditure cannot be ignored. Budgetary institutions must be strengthened and there must be reviews not only of the scale of spending but also the scope of Government.

ii) Much of government expenditure is rigid – the bulk comprises salaries, pensions and interest so reducing these is a long term process. Reforming State Enterprises, especially in the energy sector and Sri Lankan Airlines is less difficult and could yield substantial savings. Continued operation of inefficient and loss-making SOE’s is untenable under such tight fiscal conditions. Financing SOE’s from state bank borrowings and transfers from government reduces the funds available for vital and underfunded sectors such as healthcare and education. Excessive SOE debt also weakens the financial sector and increases the contingent liabilities of the state. Therefore SOE reforms commencing with improving governance, transparency, establishing cost reflective pricing and privatisation are necessary. This can take a significant weight off the public finances and by fostering competition contribute to improvements in overall economic productivity.

iii) Tighten monetary policy and maintain exchange rate flexibility. Immediate structural reforms include, Inflation targeting, ensuring the independence of the central bank by way of legislation and enabling the functioning of a flexible exchange rate regime. Further significant attention has to be placed on the financial sector stability with a cohesive financial sector consolidation plan, with special emphasis on restructuring of SOE debt.

iv) Supporting trade and investment. Sri Lanka cannot achieve economic growth without international trade which means linking to global production sharing networks. Special focus has to be given to reducing Sri Lanka’s high rates of protection which creates a domestic market bias in the economy along with measures to improve trade facilitation and attract new export oriented FDI.

Attempts to build local champions supported by high levels of protection have

(a) diverted resources away from competitive businesses,

(b) created a hostile environment for foreign investment,

(c) been detrimental to consumer welfare,

(d) dragged down growth

v) Structural reforms to increase productivity and attract FDI – Productivity levels in Sri Lanka have not matched pace with the rest of the growing economies. The reforms mentioned above are extensively discussed in Advocata’s latest publication “Framework for Economic Recovery”.

Sri Lanka stumbled into the coronavirus crisis in bad shape,with weak finances; high debt and widening fiscal deficits. It no longer has the luxury to delay painful reforms. Failure to do so will not only jeopardize the economy; it could even spawn social and humanitarian crises.

Naqiya Shiraz is the Research Analyst at the Advocata Institute and can be contacted at naqiya@advocata.org.K.D.D.B. Vimanga is a Policy Analyst at the Advocata Institute. He can be contacted at kdvimanga@advocata.org.

Sri Lanka Insurance Corporation General Limited (SLICGL) unveiled Beechat, the country’s first generative AI‑powered insurance assistant, heralding a milestone for Sri Lanka’s insurance industry and move towards digital services.

Beechat is designed to transform the customer experience. Available through the SLICGL website (https://www.slicgeneral.com/) and customer portal, the Assistant offers customers instant access to policy information, real-time claim status updates, and insurance-related help 24 hours a day, seven days a week.

For customers, Beechat makes insurance simpler and always available. Instead of waiting in queues, calling hotlines, or being limited to business hours, customers can check policies, track claims, and receive instant answers in Sinhala, Tamil, or English, empowering every customer, whatever their language, to manage their insurance with ease.

The inclusivity ensures every customer, regardless of language preference, can engage with insurance services seamlessly. The AI‑driven platform reduces complexity, eliminates delays, and builds trust. Ultimately, Beechat transforms insurance from a process often seen as slow and complicated into a smooth digital journey that fits modern lifestyles.

The launch of SLICGL Beechat is strategically important for the organization because it strengthens its position as a leader in innovation within Sri Lanka’s insurance industry. Introducing the country’s first generative AI‑powered, trilingual insurance assistant, SLICGL demonstrates a commitment to digital transformation and technology‑driven service excellence.

The initiative reaffirms the company as forward‑thinking and customer‑centric and differentiating from competitors who still rely on traditional service models. It signals to industry stakeholders that SLICGL is setting new standards for accessibility, efficiency, and convenience in insurance.

Pioneering AI‑driven customer engagement, the company sets a new benchmark. Beechat demonstrates how technology can elevate insurance from a traditional service into a dynamic, futuristic experience, strengthening SLICGL’s relationship with the people it services. (SLICGL)

Lanka Tractors Limited officially reopened its original showroom in Colombo 11, marking the return of one of Sri Lanka’s most recognised agricultural machinery companies and the official launch of the ACE Tractor brand in the country.

Located at 343 Olcott Mawatha, Colombo 11, the showroom was ceremonially declared open by Chief Guest Dudley Sirisena, Chairman of the Araliya Group of Companies, in the presence of Upul Jayasuriya, Chairman of Lanka Tractors Limited, Thilina Abeysuriya, Managing Director, Nishantha Yapa, Head of Business, and Rajiv Gunawardena, CEO of Asia Asset Finance PLC.

Originally established in 1971 as the State Trading (Tractor) Corporation, Lanka Tractors was restructured in 1991 and became one of Sri Lanka’s largest importers and distributors of agricultural machinery. Over the decades, the company represented internationally renowned brands including Massey Ferguson, Kubota and TAFE, earning the trust of generations of Sri Lankan farmers through quality products, technical expertise and dependable after-sales support. The reopening of its original Colombo 11 showroom, first established in 1982, marks the revival of an institution that has played a pivotal role in the mechanisation of Sri Lankan agriculture for more than five decades.

The company’s revival commenced in late 2025 through an exclusive partnership with ACE Tractors, the agricultural division of Action Construction Equipment (ACE) Limited, one of India’s leading engineering and manufacturing companies. ACE manufactures tractors, agricultural machinery, construction equipment and industrial equipment, with annual production capacity exceeding 9,000 tractors, exports to more than 37 countries, and a dealer and service network spanning over 100 locations worldwide.

Prior to the commercial launch, Lanka Tractors adopted an extensive validation programme to ensure the products were ideally suited to Sri Lankan farming conditions. Three introductory models—the ACE VEER 3000 (26 HP 4WD), ACE DI 350 NG (40 HP 2WD) and ACE DI 450 NG (45 HP 4WD)—underwent rigorous field testing across multiple agricultural regions under the supervision of ACE technical specialists. Following several product refinements based on local operating conditions, the tractors were introduced to the market in April 2026.

The desire to communicate and be understood is at the heart of what it is to be human. In contemporary life, digital infrastructure underpins how we work, live, and share information, but the letterforms that carry our languages are rarely neutral.

Arkurugraphy, a new exhibition at the Geoffrey Bawa Space, explores the history, culture, and future of letterforms across Sri Lanka’s three official languages. Presenting the decade-long practice of Colombo-based type foundry Mooniak, it examines how decisions about the digitisation of Sinhala, Tamil, and Latin scripts impact legibility and carry deep consequences for who is seen, who is heard, and whose language endures.

Writing systems carry human thought and knowledge across time and space. Letterforms can become a form of cultural artefact, unique graphic symbols representing identity and belonging. Today, these inherited letterforms often take shape as digital fonts, their design demanding fluency across history, aesthetics, linguistics, and technical standards. Akurugraphy asks audiences to look at letterforms beyond the act of reading: to appreciate their form, trace their past, and consider the decisions that impact their future.

Akurugraphy brings together typographic specimens, archival material, and software development spanning Mooniak’s full body of practice. It is a celebration of letterforms as art and an examination of the technical and political stakes of designing scripts for the digital age. As part of the exhibition, the Geoffrey Bawa Space will host a programme of monthly talks, curatorial tours, workshops, and children’s programmes.

Akurugraphy is open Wednesday through Sunday, 10:30 a.m. – 5:30 p.m., and will be on view until 8 November 2026. The exhibition is designed to be accessible and welcoming to all visitors. The Geoffrey Bawa Space offers step-free access and wheelchair accessible facilities. Tactile elements are available throughout the exhibition. More information is available at geoffreybawa.com/akurugraphy .

Dharmaraja and Kingswood set for historic rugby clash on Saturday

Sri Lankan singer Mariazelle Goonetilleke passes away at the age of 68

Tensions erupt in Indian state after 11-year-old raped and murdered

US and Iran trade attacks as Khamenei is buried

Several spells of showers will occur in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Canadian PM visits Saudi Arabia to strengthen energy, mining partnerships

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoSingapore-based Buddhist monk marks nearly four decades of humanitarian service

-

News7 days ago

News7 days agoFreedom 250: US Embassy celebrates America’s 250th Independence Day through magic of American cinema

-

News21 hours ago

News21 hours agoHerath warns prospective migrant workers not to get fleeced by racketeers

-

News5 days ago

News5 days agoAI concerned over proposed SL military deployment in Haiti

-

Midweek Review3 days ago

Midweek Review3 days agoUnexpected focus on ‘pieces of tin’ worn by military men

-

Latest News4 days ago

Latest News4 days agoNyamhuri and Ngarava stun Bangladesh by defending 141

-

Features6 days ago

Features6 days agoThe NPP’s New Challenge: Balancing Easter Lawfare and Economic Welfare

-

News2 days ago

News2 days agoNegombo Prison riot: Ensuring protection of prisoners fundamental responsibility of the state – UN