Business

Local entrepreneurs propose high-quality saree manufacturing in Sri Lanka to curb forex outflow

A group of local entrepreneurs is urging the government to overhaul the nation’s textile import policy, proposing a bold shift toward domestic saree manufacturing to stem the critical outflow of foreign exchange.

Sidambaram Karunanithi, a Pettah-based entrepreneur with deep roots in India and the textile trade, told The Island Financial Review that approximately 100,000 sarees are sold daily across Sri Lanka. He argued that the total reliance on Indian imports for this high-volume commodity represents an “unnecessary drain” on the country’s precarious dollar reserves.

The consortium, led by Karunanithi, has drafted a comprehensive roadmap to achieve self-sufficiency in the sector. The plan envisions the establishment of nine specialised factories – one in each province – to decentralize the industry.

“Our strategy is to import raw materials, specifically high-quality yarn, from India and conduct the entire manufacturing process locally,” Karunanithi explained. “By producing within the provinces, we eliminate significant freight costs as well as the need for regional dealers to travel to Pettah. These logistical savings will be passed directly to the end-consumer.”

The entrepreneurs intend to utilize advanced industrial multi-head systems sourced from leading Chinese manufacturers, capable of producing high-speed air-jet and jacquard weaves. Karunanithi emphasised that this technology would allow the local industry to reach a 50% value-addition threshold – more than the 35% standard often requested by the government for other sectors.

“India achieved global manufacturing status through partnerships like Hero Honda and Maruti Suzuki. There is no reason we cannot do the same with sarees. If there is a will, there is a way,” he noted.

Addressing the technical gap, the group plans to initially import skilled labor from India to facilitate a year-long technology and skills transfer. “Within 12 to 18 months, these foreign workers will be entirely replaced by a trained Sri Lankan workforce,” he said.

The proposal includes a request for the government to restrict Indian saree imports over one year to provide the necessary market protection for local startups. Karunanithi stressed that the group is not seeking concessional bank facilities, stating they are prepared to invest in private lands if state land is unavailable.

The entrepreneurs are calling for a meeting with President Anura Kumara Dissanayake and the Ministry of Industries to present their financial profiles and technical capacity.

“We urge the authorities not to make half-hearted or inconsistent policy decisions. If the country allows the manufacture of alcohol, why not sarees?” Karunanithi asked, adding that the foreign currency saved could be vital for the health and education sectors.

By Sanath Nanayakkare ✍️

The government has initiated what could become one of the most significant reforms of Sri Lanka’s social security system in decades by appointing a Senior Officials’ Committee to examine the feasibility of bringing the Employees’ Provident Fund (EPF) and the Employees’ Trust Fund (ETF) under a unified tripartite governance framework representing the government, employers and employees.

Cabinet approval was granted following a proposal submitted by the Minister of Labour. According to Cabinet Spokesman and Minister Dr. Nalinda Jayatissa, the committee has been mandated to study whether the two institutions could operate under a common governance structure based on internationally recognised principles promoted by the International Labour Organization (ILO).

He stressed that the committee has been appointed only to examine the feasibility of the proposal, and no final decision has been taken to merge the two funds.

The official Cabinet statement notes that the EPF, established under the Employees’ Provident Fund Act No. 15 of 1958, has more than 2.5 million members and assets exceeding Rs. 4.9 trillion, making it Sri Lanka’s largest social security fund.

Custody of the fund, investment management, financial administration and payment of benefits are currently handled by the Central Bank of Sri Lanka, while the Department of Labour is responsible for member registration, employer compliance, recovery of arrears and safeguarding employee rights.

The ETF, created under Act No. 46 of 1980, is administered by a tripartite board comprising representatives of the government, employers and employees. It manages assets of approximately Rs. 637 billion and provides coverage to more than 2.5 million active members.

The Cabinet paper highlights that tripartite governance of social security institutions is an internationally recognised best practice and a fundamental principle promoted by the ILO, which forms the basis for examining a common governance model for both funds.

The proposal is expected to attract close scrutiny from the business community, trade unions and financial market participants, given that the combined assets of the EPF and ETF exceed Rs. 5.5 trillion, making them among the country’s largest institutional investors.

Economists note that any governance reforms should strengthen transparency, accountability, professional investment management and public confidence while safeguarding workers’ retirement savings.

By Ifham Nizam

LOLC Microfinance Bank Pakistan, a fully owned subsidiary of the LOLC Group, has strategically relocated its Head Office to Gulberg Greens, Islamabad, marking a significant milestone in its growth journey. As one of the LOLC Group’s largest overseas operations in Asia, the Bank continues to advance financial inclusion and sustainable economic development across Pakistan.

The new Head Office was formally inaugurated in the presence of Chief Guests H.E. Admiral Fred Seneviratne (Retd.), High Commissioner of Sri Lanka to Pakistan, and Mr. Krishan Thilakaratne, Chairman of LOLC Microfinance Bank Pakistan. The ceremony was attended by the Bank’s Board of Directors, senior management and employees, commemorating another important chapter in the Bank’s continued expansion.

LOLC Microfinance Bank Pakistan is a fully-fledged Microfinance Bank regulated by the State Bank of Pakistan, operating through a network of 88 branches and employing over 1,200 staff members across the key cities of Karachi, Lahore, Hyderabad, Faisalabad, Sialkot, Islamabad, Peshawar and Gilgit. The Bank offers a comprehensive range of financial solutions, including business loans, microfinance, vehicle financing, gold loans and other financial products. It currently manages a loan portfolio exceeding USD 70 million and a deposit portfolio exceeding USD 90 million, comprising savings deposits, term deposits and current accounts.

The relocation to the new Head Office reflects the Bank’s expanding operations and its commitment to widening access to responsible financial services for individuals, micro-entrepreneurs and small businesses across Pakistan. In 2026, LOLC Microfinance Bank Pakistan was recognised as Pakistan’s fastest growing Microfinance Bank, highlighting its strong business momentum and growing market presence.

Addressing the gathering, H.E. Admiral Fred Seneviratne (Retd.), High Commissioner of Sri Lanka to Pakistan, stated, “The relationship between Sri Lanka and Pakistan continues to grow through meaningful partnerships such as this. LOLC Microfinance Bank Pakistan is making an important contribution by supporting entrepreneurs, strengthening the SME sector, and expanding financial access where it is needed the most. Institutions like these play a vital role in empowering communities and supporting sustainable economic growth.”(LOLC)

Citizens Development Business Finance PLC (CDB) lit up the CCC Grounds on June 28th, retaining the championship of the MCA T10 Cricket Tournament, further etching its record of being unbeaten and showcasing its signature persona of being determined and unstoppable.

Sealing the title without a single loss in the tournament from the first ball to the final cheer, Team CDB skippered by Tharindu Rathnayaka with Vice Captain Dunith Wellalage, both national players, showcased the calibre of a champion side.

Coached by national player Oshadha Fernando, CDB combined star power with relentless team spirit – the perfect combination of experience and youthful energy. CDB’s performance was not just about individual brilliance but about a collective drive that mirrors CDB’s corporate ethos of perseverance, leadership, and excellence.

The final match against the Abans Group was a fitting climax. Chasing 116, CDB powered to 120/4 in just 8.4 overs, sealing victory by six wickets. Vishad Randika rose to the occasion as Player of the Final. Nuwan Thushara’s consistent bowling prowess, including a hat trick — 2 overs, 11 runs, 4 wickets during the semi-finals — earned him the Best Bowler accolade.

This unbeaten run was more than a cricketing triumph. It was a statement by CDB of its dedication to excellence, which extends beyond financial services into fostering a high-performance culture through sports. The championship reinforced the company’s reputation as a leader in the financial sector while celebrating employee engagement, wellness, and community spirit.

Current El Niño Status in Sri Lanka

A few showers may occur in the Western, Sabaragamuwa and North-western provinces and in Kandy, Nuwara-Eliya, Galle and Matara districts.

Argentina face fine for Falklands banner in semi-final win

US launches fresh strikes on Iran as Trump warns Tehran it ‘better behave’

Govt. move to extend retirement ages of top judges: Opp. complains to UN

Dengue surge pushes hospitals to the brink as cases near 70,000

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoHerath warns prospective migrant workers not to get fleeced by racketeers

-

Features4 days ago

Features4 days agoPrison riots and politics: NPP’s biggest challenge and Sri Lanka’s biggest opportunity

-

Editorial5 days ago

Editorial5 days agoWhat’s the world coming to?

-

Foreign News6 days ago

Foreign News6 days agoTensions erupt in Indian state after 11-year-old raped and murdered

-

Features6 days ago

Features6 days agoDevanesan Annan – in Memoriam

-

Editorial6 days ago

Punishment in hellholes

-

News7 days ago

News7 days agoRepresentatives of the Organization of Professional Associations (OPA) of Sri Lanka meet the Prime Minister

-

Features1 day ago

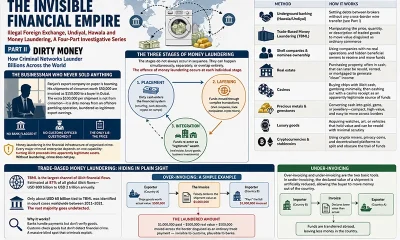

Features1 day agoDirty Money