Features

How CSE is designed to fail retail investors

Six Charges, 700% More Expensive:

![]() Imagine walking into two shops selling the same product. In the first shop, you pay a simple 0.6% fee. In the second shop, you’re hit with a bewildering array of charges from multiple entities, and by the time you’re done, you’ve paid 2.27%. And that’s for a complete transaction: buying and selling.

Imagine walking into two shops selling the same product. In the first shop, you pay a simple 0.6% fee. In the second shop, you’re hit with a bewildering array of charges from multiple entities, and by the time you’re done, you’ve paid 2.27%. And that’s for a complete transaction: buying and selling.

The Shocking Numbers

Sri Lanka loves to say it wants to “develop the capital market.” But the way we charge investors tells the real story – a story of policy confusion, fee-layering, and a system designed to favor big players while suffocating small retail investors.

The evidence isn’t hidden. It’s printed clearly in every contract note that brokers issue.

Think about what this means in real terms. If you’re a teacher, government servant, or small business owner investing Rs. 100,000 in shares, you’ll pay approximately Rs. 2,270 just to complete a buy-sell cycle in Sri Lanka. In New Zealand, that same transaction costs just Rs. 300.

Sri Lanka is nearly four times more expensive than New Zealand – for the exact same act of investing.

Death by a Thousand Cuts

The problem isn’t just the total amount – it’s the sheer complexity. While New Zealand streamlines everything into one clean charge, Sri Lankan investors face a labyrinth:

The problem isn’t just the total amount – it’s the sheer complexity. While New Zealand streamlines everything into one clean charge, Sri Lankan investors face a labyrinth:

* Brokerage (negotiable, but only if you’re wealthy)

SEC Fee (Security Exchange Commission)

* CSE Fee (Colombo Stock Exchange)

CDS Fee (Central Depository Systems fees)

* STL (Share Transaction Levy)

Clearing Fee

* Foreign Brokerage for foreign transactions

* Various “special fees” are added periodically

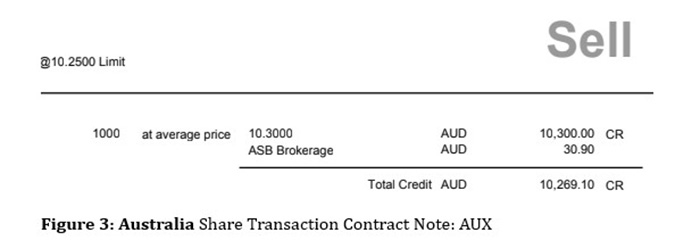

Sri Lanka’s stock trading contract note reads like a mini-budget speech (Figure 1). Meanwhile, most modern markets charge one number. For an ordinary person trying to understand their contract note, it’s nearly impossible to figure out what they’re actually paying and why. Figures 2 and 3 show the stock trading “Sell” contract notes for a New Zealand Stock Exchange transaction and an Australian Stock Exchange transaction, (“Buy” contracts are similar) respectively.

The Rich Get Richer – By Design

Here’s where it gets truly disturbing. While small investors are locked into these punishing charges, the CSE allows brokers to negotiate lower fees for large transactions – typically those exceeding Rs. 100 million.

Let that sink in: If you’re a retail investor putting in your life savings of Rs. 500,000, you pay the full 2.27%. But if you’re moving Rs. 100 million, you get a discount.

This isn’t just unfair – it’s a systematic transfer of wealth from small investors to large players. The very people who need protection are subsidising the fees for those who need it least.

In modern markets like India, New Zealand, Canada, and Japan, all investors pay the same percentage. No negotiation. No special deals behind closed doors.

The Market Manipulation Connection

This two-tier system has darker implications. Large players, already enjoying preferential fee structures, have repeatedly been caught manipulating the market. The Securities and Exchange Commission has filed numerous cases against major investors for price manipulation, insider trading, and other violations.

These large players can:

* Move in and out of stocks quickly due to lower transaction costs

* Manipulate prices knowing small investors can’t react fast enough (their costs are too high)

* Accumulate positions while retail investors are trapped by the fear of paying 2.27% round-trip costs

Sri Lanka’s fee structure encourages large speculative swings, discourages genuine retail participation, creates an uneven playing field, and opens doors for manipulation and cornering of illiquid stocks.

The Ethical Bankruptcy of Regulatory Charges

Let’s call this what it is: regulatory authorities charging fees that actively harm the market they’re supposed to develop are ethically bankrupt. In most countries, regulators protect investors. In Sri Lanka, they bill investors. Every trade finance the regulator (SEC), the exchange operator (CSE), the clearing house (CDS), the broker, and the government (through VAT).

This is ethically questionable because:

Regulators must be neutral – not profit from transactions

Charging retail investors to fund regulation creates a conflict of interest

It reduces trust, especially after repeated market manipulation cases

When regulators impose charges that make it unprofitable for ordinary people to invest, they’re not protecting investors – they’re protecting their own revenue streams at the expense of market development. When exchanges allow discriminatory fee structures, they’re not creating a level playing field – they’re creating a rigged game.

Why Sri Lanka’s Market Cannot Grow

Sri Lanka keeps asking: “Why is liquidity so low? Why don’t more people invest? Why doesn’t the stock market support economic growth?” Based on my research, using AI tools, here’s a comprehensive comparison table of stock market participation across the countries we mentioned:

Sri Lanka stands out negatively. The CSE has 284 listed companies representing 20 business sectors. Despite having a population similar to Australia (22 million vs 26 million), Sri Lanka has an estimated 50-100 times fewer stock market participants.

According to the Central Depository Systems (CDS) Annual Report 2024 for the Colombo Stock Exchange (CSE), the total number of local account holders (traders/CDS holders) was approximately 706,864 in 2024, up from 693,415 in 2023. The number of foreign account holders was 11,082 in 2024 compared to 10,937 in 2023. This places the total number of traders around 718,000+ in 2023-2024.

Critical Implications

Sri Lanka’s stock market participation rate, estimated at a low 3-4%, starkly trails regional peers such as India, where participation hits 6-8%, roughly two to three times higher. This gap highlights a critical structural problem in the Colombo Stock Exchange (CSE) ecosystem, where high fees averaging 2.27% combined with low participation create a vicious cycle that severely impedes market development. The core issues are both systemic and strategic.

The Marketing Failure: A Stock Exchange That Doesn’t Want Customers

Unlike its counterparts globally, the CSE remains more akin to an exclusive club rather than an accessible retail investment platform.

Where India’s National Stock Exchange (NSE) partnered with fintech innovators to create user-friendly investment apps while the CSE’s outreach is limited to sporadic seminars mostly attended by brokers and affluent investors. The CSE doesn’t want millions of small investors; it wants thousands of large ones who won’t complain about the fees.

There are no robust nationwide campaigns demystifying investing, no telecom partnerships to penetrate rural markets, and the mobile apps are not intuitive and fail to simplify account opening processes as expected. The CSE’s web and social media presence remain outdated, and when India onboarded over 40 million retail investors in three years via aggressive digital marketing, Sri Lanka struggled to add even 40,000 investors. This is not accidental, but symptomatic of an institution that profits more from high fees on lower volumes than from a broad base of smaller investors. The system favors wealth extraction from a few large players while discouraging retail participation.

Bureaucratic Ossification: When Vision Dies in Committee Rooms

The CSE suffers from a stifling bureaucratic culture, trapped in colonial-era mindsets with fragmented decision-making authority dispersed over multiple regulatory bodies like the SEC, Central Bank, and ministries. Sri Lanka’s capital market leadership remains focused on maintaining the status quo, prioritizing regulatory compliance over innovation. Without a strategic vision to increase retail participation, possibly aiming for even a modest 10% target, the exchange risks remain a peripheral entity rather than a genuine engine of national wealth.

The CSE suffers from a stifling bureaucratic culture, trapped in colonial-era mindsets with fragmented decision-making authority dispersed over multiple regulatory bodies like the SEC, Central Bank, and ministries. Sri Lanka’s capital market leadership remains focused on maintaining the status quo, prioritizing regulatory compliance over innovation. Without a strategic vision to increase retail participation, possibly aiming for even a modest 10% target, the exchange risks remain a peripheral entity rather than a genuine engine of national wealth.

The disconnect between high market returns (close to 50% in 2024) and low investor participation underscores the urgent need for the CSE to radically change course from a fee-heavy, opaque, bureaucratic institution to a transparent, technology-enabled, investor-friendly market. Unless Sri Lanka’s capital market astrology embraces inclusive, technology-driven, and simplified structures combined with aggressive marketing and retail investor protection, it will continue to underperform relative to regional peers, hampering broader economic growth and wealth creation.

Marketing Malaise: How the CSE Misses the Retail Wave

There are no nationwide campaigns to demystify investing. No partnerships with firms like financial institutions and tertiary education establishments, such as universities, where eligible customers are abundant and to reach rural areas. When India added over 40 million new retail investors in just three years through aggressive digital outreach, Sri Lanka couldn’t add 40,000. This isn’t accidental – it’s the natural result of an institution that makes more money from high fees on low volumes than it would from low fees on high volumes.

Bureaucratic Ossification: When Vision Dies in Committee Rooms

The CSE’s administration suffers from a fatal combination: colonial-era bureaucratic mentality married to a complete absence of strategic vision. While global exchanges have transformed into technology-driven, investor-first platforms, the CSE remains trapped in a time warp protecting its turf and revenue streams. Decision-making moves at the speed of a government file, while markets move at the speed of light.

The result is an exchange governed by administrators rather than visionaries. When Singapore launched a comprehensive digital trading ecosystem, when India implemented T+1 settlement cycles, when New Zealand simplified its entire fee structure to one transparent charge, Sri Lanka’s was busy protecting the status quo. There’s no long-term strategic plan to achieve even 10% retail participation. No vision for how Sri Lanka’s capital market fits into the economy of 2030. The CSE operates like a government department completing its KPIs rather than a dynamic institution building national wealth. The entire ecosystem – from the SEC to CDS to brokers – protects a broken system because they all profit from it.

Whenever the question of low retail participation comes up, officials trot out the same tired excuses: lack of investor awareness,’ ‘risk appetite,’ budgetary constraints for promotions.’ What they never admit is the elephant in the room, Sri Lanka’s fee structure. Charging 2.27% in a fragmented, opaque system while allowing negotiated rates for the wealthy isn’t market design, it’s a wealth extraction scheme dressed in regulatory language (Figure 3).

Add to that a lethargic marketing approach for attracting a wider population. Instead of proactive campaigns, digital engagement, and investor education, the system relies on outdated methods that fail to inspire confidence. The result? A market that moves backward while global peers surge ahead.

Our regulatory authorities have created a system that achieves the exact opposite of what a stock market should do. Instead of encouraging saving and investment, we punish it. Instead of attracting retail participation, we drive small investors away. Instead of ensuring fairness, we let the rich negotiate better terms.

The Bottom Line

The Colombo Stock Exchange and its regulatory framework aren’t just failing small investors – they’re actively working against them. No stock market can flourish when fees punish participation and policy rewards big players while suffocating small ones.

If Sri Lanka wants a real capital market – not just a slogan – it must not only stop taxing retail investors to fund inefficiencies and start building a market that ordinary citizens can finally trust, but also, they should actively promote the retail participation with more promotional activities to reach them by making collaborations with relevant firms such as financial institutions and tertiary educational establishments, especially universities.

Until someone in authority has the courage to blow up this exploitative system and start fresh, ordinary Sri Lankans will continue to be better off keeping their money under the mattress.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT, Malabe. The views and opinions expressed in this article are personal.)

Sri Lanka is witnessing the dismantling of the culture of impunity that dominated public life for decades. This is happening through the courts, police investigations and legal process. It is not an easy task and requires strong leadership as it is generating strong resistance. The ongoing revelations about the nexus between politicians, including those at the highest levels, and criminal networks show that the government’s electoral mandate with regard to corruption and crime is now being translated into action through the legal system. The vote of the people at the last national elections was for a corruption free country and an end to the climate of impunity that had prevailed for decades. They voted for a system change that would replace impunity with accountability under the rule of law. They expected those who had looted the country and brought it to the point of bankruptcy to be held accountable through the due process of law.

The cases that are being investigated by the police, in tandem with the Attorney General’s Department, and adjudicated by the judiciary are based on hard evidence. Much of the evidence that is now receiving publicity had been available several years ago and had even entered the legal process. In the past those cases failed to reach fruition. Investigations lost momentum, prosecutions failed to marshal the available evidence and many cases were dismissed, some on technical grounds. Between 2019 and 2024, a total of 102 cases were withdrawn from the courts by the government authorities. The public knew, or strongly believed, that corruption and serious crimes had taken place. The inability to establish wrongdoing before a court of law and hold those responsible accountable created a climate in which political power appeared to provide protection from legal accountability.

A countrywide study titled Factors Guiding Voter Preference in Elections in Sri Lanka was commissioned by the National Peace Council prior to the 2024 elections under the European Union funded project Active Citizens for Elections and Democracy and conducted by researchers Dr Mahesh Senanayake and Ms Crishni Silva of the University of Colombo. It found overwhelming public support for accountability and good governance. While 93 percent of respondents identified resolving the economic crisis as their foremost electoral concern, an equally striking 83 percent said they prioritised candidates committed to fighting corruption. The mandate given to the government can, therefore, be interpreted to mean to restore integrity to public life and end the long standing culture of impunity.

Different Approach

Today, it can be seen that the police, the Commission to Investigate Allegations of Bribery or Corruption, the Attorney General’s Department and the judiciary are approaching matters of impunity in respect of corruption and crime in a manner that is markedly different from the past. Several persons who formerly occupied high office have now been subjected to due legal process and, in a number of cases, convicted after judicial scrutiny at different levels of the court system. This is an important difference from earlier years when cases involving politically prominent persons frequently failed to proceed or collapsed before reaching their conclusion. The strength of the present accountability process lies not only in the convictions that have been secured but also in the growing public confidence that no one is above the law. It is in this context that reports of a government proposal to extend by two years the retirement age of judges of the Supreme Court and the Court of Appeal have generated support from those who wish to see the present accountability process continue and opposition from those who see it as an attempt to influence the judiciary.

Many countries have increased judicial retirement ages in recognition of longer life expectancy and the value of retaining experienced judges. This has not only been limited to the judiciary but also the academia and the public service. However, the controversy in Sri Lanka is due to the context and as the proposal for an extension of the period of service of judges of the superior courts comes at a time when the courts are hearing politically significant corruption and criminal cases. The Bar Association of Sri Lanka has taken the lead in questioning the proposed constitutional amendment. The BASL has stated that it “notes with grave concern” reports that the government is considering increasing the retirement age of judges of the Supreme Court and the Court of Appeal. It has warned that extending the tenure of sitting judges at this point of time is likely to be viewed by the public as an attempt to interfere with the independence of the judiciary.

The main issue raised by the BASL is therefore one of preserving public confidence in the administration of justice. A discussion organised by the BASL also highlighted that this issue has implications beyond Sri Lanka. Representatives of the Commonwealth Lawyers Association and LAWASIA acknowledged that many countries have increased the retirement age of judges in recognition of greater life expectancy and the value of retaining experienced judges. Their concern was not with increasing the retirement age itself but with changing the tenure of sitting judges while politically significant corruption cases are before the courts. In such circumstances, even well intentioned reform could create a public perception that the judiciary is being influenced to take forward the government’s mandate in a partisan manner.

Maintain Confidence

The challenge before the government is to preserve two equally important objectives. The first is to continue implementing the people’s mandate to hold the corrupt and those responsible for grave crimes accountable before the law. The second is to ensure that nothing is done which could diminish public confidence in the independence and impartiality of the judiciary that is entrusted with carrying out that responsibility. The strength of the present accountability process lies in the confidence it has generated among the public that investigations, prosecutions and judicial decisions are being made according to law as in the convictions that have been secured. Sri Lanka has come a long way from the days when politically sensitive cases rarely reached a successful conclusion. It would be unfortunate if doubts regarding the independence of the judiciary were to overshadow what has otherwise been a significant institutional achievement.

In the face of the concerns expressed by the BASL, opposition political parties and international legal organisations, it would be prudent for the government to widen the discussion on the proposed amendment. If there is a compelling case to increase the retirement age of judges of the superior courts, that case should be placed before the public and parliament and debated openly. Such a constitutional amendment should not rest solely on the government’s parliamentary majority, even if it has the numbers to secure its passage. Simply utilising the numbers that the government on its own to make changes to the constitution will not increase its legitimacy or credibility. Those values will be strengthened if they were preceded by public consultation and supported across party lines in Parliament. Bipartisan political support can be expected from those in the opposition, of whom there are many, who have shown an inclination to practice responsible politics in the national interest.

The people voted not only to change a government but to change a system. They expected those who abused public trust to be held accountable through institutions that commanded public confidence. That expectation is beginning to be fulfilled. It should not be placed at risk by constitutional change that lacks broad public acceptance. If the government believes there is a compelling case to extend the retirement age of the judges of the superior courts, it should first make that case to the people and seek bipartisan support in Parliament with those in the opposition who are also sincere about anti-corruption and good governance. The challenge is to protect the independence of the judiciary while ensuring that no one is above the law. Overcoming this challenge is the surest way to make Sri Lanka’s transition from a culture of impunity to one of accountability a lasting one.

by Jehan Perera

In an increasingly volatile and interconnected world, the strength of a nation is no longer determined solely by the size of its military, the abundance of its natural resources, or the growth of its economy. The true measure of national strength lies in the resilience of its institutions, the confidence of its people, the effectiveness of its governance, and its ability to anticipate and respond to emerging challenges before they become national crises.

The twenty-first century has introduced a security landscape that is far more complex than ever before. Nations today confront not only conventional military threats but also terrorism, organised crime, cyber-attacks, economic instability, disinformation, climate change, pandemics, energy insecurity, irregular migration, financial crimes, and geopolitical competition. These challenges are interconnected and demand integrated responses rather than isolated solutions.

To navigate this evolving environment successfully, every nation requires a shared strategic vision supported by strong institutions working in harmony. At the centre of this vision should be a modern, professional, and intelligence-led system of governance that enables informed decision-making, protects democratic values, and promotes sustainable national development.

A Shared Strategic Vision

Every successful nation should aspire towards a common national vision:

A Sovereign Nation Happy People Peaceful Society Prosperous Economy A Respected Global Partner

These are not independent aspirations but interconnected national outcomes. Achieving them requires every State institution to work collectively under a common strategic framework rather than as isolated entities pursuing individual objectives.

A sovereign nation is one that possesses not only secure borders but also strong institutions, economic resilience, social cohesion, and the confidence to make independent national decisions. Sovereignty today extends beyond territorial integrity to include economic security, cyber resilience, energy security, food security, environmental sustainability, and protection against external influence.

Good Governance: The Cornerstone

The foundation of every successful nation is good governance.

Transparency, accountability, integrity, professionalism, and efficient public administration create an environment where citizens trust their institutions and investors have confidence in the country’s future. Corruption, political interference, inefficiency, and weak institutions undermine national resilience and weaken sovereignty from within.

Good governance is not merely an administrative principle; it is a national security imperative.

When public institutions function efficiently, public services improve, economic opportunities expand, and social grievances diminish. This reduces vulnerabilities that extremist groups, organised criminals, and foreign actors often exploit.

The Rule of Law and Judicial Independence

An independent judiciary is one of the strongest pillars of democracy.

Justice must be administered impartially and without fear or favour. Citizens must have confidence that the law applies equally to everyone, regardless of social status or political influence.

Judicial independence strengthens public confidence, attracts foreign investment, and reinforces national stability. Investors are more likely to invest in countries where contracts are enforceable, disputes are resolved fairly, and property rights are protected.

Likewise, professional law enforcement agencies play a vital role in safeguarding public order. Intelligence-led policing, supported by modern investigative techniques, community engagement, and technological innovation, enables law enforcement to prevent crime rather than merely react to it.

Human Rights: A Strategic Asset

There is often a misconception that national security and human rights exist in opposition. In reality, they reinforce one another.

Respect for human dignity, equality before the law, freedom of expression, religious freedom, and constitutional rights strengthens national unity and social cohesion. Citizens who trust their institutions are more willing to cooperate with authorities, report suspicious activities, and participate in community safety initiatives.

Communities become the first line of defence against extremism, organised crime, and social unrest when mutual trust exists between citizens and the State.

Human rights should therefore be viewed not as obstacles to security but as essential components of sustainable national security.

Intelligence: The Strategic Nerve Centre

At the heart of modern governance lies an effective national intelligence network.

Traditionally, intelligence was associated primarily with military operations and counter-terrorism. Today, its responsibilities extend much further.

Modern intelligence supports political leadership by providing timely, accurate, objective, and actionable information that enables informed decision-making. It anticipates threats, identifies opportunities, and supports strategic planning across all sectors of government.

An effective intelligence system should be:

* Predictive rather than reactive.

* Preventive rather than investigative alone.

* Integrated rather than fragmented.

* Technology-driven rather than paper-based.

* People-centred rather than institution-centred.

Artificial intelligence, big data analytics, cyber intelligence, financial intelligence, geospatial intelligence, satellite imagery, behavioural analysis, digital forensics, and open-source intelligence are transforming the intelligence profession worldwide.

Countries that fail to modernise their intelligence capabilities risk strategic surprise and reduced competitiveness in an increasingly data-driven world.

Intelligence Beyond National Security

Modern intelligence should no longer be confined to counter-terrorism or espionage.

Its role should extend to supporting national development through the protection of critical infrastructure, monitoring economic trends, securing supply chains, safeguarding maritime interests, protecting natural resources, and assessing climate-related risks.

Intelligence should assist policymakers in areas such as:

* Economic planning

* Public health preparedness

* Disaster risk reduction

* Cybersecurity

* Energy security

* Food security

* Environmental protection

* Artificial intelligence governance

* Foreign policy

* Investment protection

An intelligence-led government anticipates future challenges instead of merely responding after crises emerge.

Whole-of-Government Cooperation

One of the greatest weaknesses in many developing nations is institutional fragmentation.

Government agencies often collect valuable information independently but fail to share it effectively. This creates duplication, delays, and missed opportunities.

A National Intelligence Fusion Centre should integrate information from intelligence services, police, armed forces, immigration, customs, financial intelligence units, cyber security agencies, disaster management authorities, health services, and environmental agencies.

Such integration provides decision-makers with a comprehensive national picture and significantly improves crisis management and strategic planning.

Economic Prosperity Through Security

Economic development depends fundamentally upon stability.

Foreign investors seek countries where governance is predictable, corruption is controlled, contracts are enforceable, infrastructure is secure, and political stability is maintained.

An effective intelligence system quietly protects these conditions by identifying threats to investment, monitoring organised crime, preventing financial fraud, protecting critical infrastructure, and safeguarding strategic industries.

Security and economic development are therefore mutually reinforcing.

Investment creates employment.

Employment reduces poverty.

Reduced poverty strengthens social stability.

Social stability reinforces national security.

International Partnerships

No nation can successfully confront modern threats alone.

Transnational organised crime, cybercrime, narcotics trafficking, terrorism, money laundering, illegal migration, and environmental crimes operate across borders.

Regional and global intelligence cooperation has therefore become indispensable.

Information sharing, joint investigations, coordinated maritime surveillance, and collaborative cyber defence significantly enhance national capabilities while strengthening diplomatic relationships.

Strong intelligence supports effective diplomacy.

Effective diplomacy enhances trade, investment, tourism, education, and technological cooperation.

Ultimately, international confidence contributes directly to national prosperity.

The Relationship Between National Stakeholders

National success depends upon collaboration among all stakeholders.

Government provides leadership and policy direction.

The judiciary safeguards justice.

Law enforcement protects public safety.

The intelligence community provides foresight and early warning.

Civil society strengthens social cohesion.

Educational institutions develop future leaders.

The private sector generates investment and innovation.

International partners facilitate trade, cooperation, and knowledge sharing.

Citizens themselves remain the most important stakeholders.

When these institutions operate with mutual trust, shared objectives, and effective coordination, they create a resilient State capable of responding confidently to both domestic and international challenges.

The Strategic Path Forward

Every nation requires a long-term vision rather than short-term political agendas.

That vision should place national interest above partisan interests and institutional collaboration above bureaucratic competition.

The pathway is straightforward:

Good Governance Independent Judiciary Professional Law Enforcement Protection of Human Rights Effective National Intelligence Network Political Stability Investor Confidence Economic Growth Foreign Direct Investment Peaceful Society Happy People A Sovereign Nation

This strategic chain demonstrates that sovereignty is not achieved through military strength alone. It is the cumulative outcome of good governance, justice, intelligence, economic resilience, and public confidence.

The future belongs to nations that can anticipate change, adapt rapidly, and make informed strategic decisions. Intelligence must therefore evolve from being viewed solely as a security function to becoming a central pillar of national governance and development.

A modern intelligence network should serve as the strategic nervous system of the State—connecting governance with justice, justice with security, security with economic prosperity, and prosperity with international respect.

A sovereign nation is ultimately one where institutions are trusted, citizens are protected, rights are respected, opportunities are created, and decisions are guided by knowledge rather than assumption. When all stakeholders work in harmony under a shared strategic vision, the result is a nation that is secure, prosperous, peaceful, and respected on the global stage.

The challenge before every developing nation is therefore not simply to strengthen its security apparatus but to embrace Intelligence-Led Governance as a national philosophy—one that integrates good governance, rule of law, human rights, innovation, and strategic foresight into a unified framework for sustainable national development. Such a vision will not only safeguard sovereignty but also ensure that future generations inherit a nation defined by stability, prosperity, and enduring peace

By Mahil Dole, SSP (Rtd.)

It has been almost two months since the judgement of Abeyasinghe v Tilakaratne and others by the Supreme Court. Since then, I have often been asked a simple question, which I, too, have asked myself. “Has anything actually changed?” My answer is both yes and no. Judgements can uphold the law, direct institutions and clarify principles. But they cannot, by themselves, change cultures.

It has been almost two months since the judgement of Abeyasinghe v Tilakaratne and others by the Supreme Court. Since then, I have often been asked a simple question, which I, too, have asked myself. “Has anything actually changed?” My answer is both yes and no. Judgements can uphold the law, direct institutions and clarify principles. But they cannot, by themselves, change cultures.

I shall take the liberty of writing this piece because, in the weeks following the judgment, I have found myself reflecting less on the outcome of the case and more on what it reveals about our institutions. Yet institutions do not change simply because a court has spoken. They change only when they are willing to question long-held assumptions, reflect honestly on their procedures and practices, learn from their shortcomings and act decisively to foster a culture that places accountability at its centre.

The myth of the perfect victim

One such assumption is about the conduct of the Ideal or Perfect victim. The concept of the “ideal victim” was first articulated by the Norwegian criminologist Nils Christie in 1986. Interestingly, Christie was not concerned with identifying those most likely to become victims of crime. Instead, his question was who is most readily recognised and accepted by society as a “real” victim? Society is often more willing to extend sympathy and credibility to victims who fit a particular stereotype. According to Christie, the “ideal victim” is someone perceived to be weak and vulnerable, engaged in a respectable activity, in a place where they have every right to be, harmed by someone clearly viewed as “big” or “bad,” and, importantly, a stranger rather than someone they know. These characteristics continue to influence how victims are perceived today. Although we may not consciously apply such criteria, they often shape our instinctive judgments about who deserves to be believed.

In the context of sexual violence within universities, the assumptions surrounding the ideal victim quickly begin to unravel. Power relationships within universities are often complex, and professional relationships may have existed before the misconduct. The alleged perpetrator may not be a stranger but a lecturer, supervisor, colleague, or fellow student. The complainant may continue interacting with the alleged perpetrator because academic progression or employment leaves little choice. When a victim does not fit the mould of the “perfect victim,” attention shifts away from the conduct of the alleged perpetrator and towards the conduct of the complainant.

What should be kept in mind is that victims respond to trauma differently. Some report immediately; many do not. Some become emotional; others appear composed. Some resign from their workplace, while others continue to work because they have no realistic alternative or because they wish to confront the violence head on. Some preserve every piece of evidence; others delete messages simply because they cannot bear to see them again. Yet these perfectly human responses are often interpreted as reasons to doubt credibility.

Universities provide a particularly complex setting for this phenomenon. Most complainants do not initially seek justice. More often, they simply want the harassment to stop so that they can continue their education or employment in an environment where they feel safe. Sometimes victims make anonymous complaints, not because they wish to avoid accountability, but because anonymity provides the only sense of security they have. During preliminary inquiries/ fact finding processes, confidentiality can often be maintained. However, if the matter proceeds to a formal disciplinary process, complainants are usually required to reveal their identities. It is at this point that many decide not to proceed further, not because the harassment did not occur, but because the personal cost of pursuing justice becomes overwhelming.

Perhaps this should prompt us to ask a different question. Instead of asking why anonymous complaints exist or why complainants don’t come forward (sooner), should we not ask why so many complainants feel unsafe engaging with the institutional process?

The subject of scrutiny

When survivors do come forward, they frequently encounter another familiar phenomenon, victim blaming.

“Why didn’t you complain earlier?”

“Why didn’t you go to the police?”

“If you were sexually harassed, why are you still working there?”

“Why did you continue interacting with him?”

“The reason this happened is because you showed positivity towards him.”

“There is no smoke without fire.”

Although these questions appear different, they have something in common. They all examine the behaviour of the complainant. Very few begin by asking why the alleged perpetrator behaved in the way described. The familiar proverb, “There is no smoke without fire,” is often used to suggest that the complainant must have done something to invite the misconduct. Yet perhaps we have misunderstood where the fire lies. The fire is not the complainant’s behaviour. The fire is the conduct of the alleged perpetrator. The complaint is the smoke that finally becomes visible.

These responses also reveal another contradiction. If a victim complains immediately, some might question their motives. If they delay, the delay becomes the issue. If they resign, they may be described as unstable or unable to cope. If they remain in employment, their continued presence is taken as evidence that the misconduct could not have been serious or that it never had happened. If they show emotion, they risk being dismissed as irrational. If they remain composed, they may be accused of exaggerating. In truth, there is often no version of events in which a complainant can satisfy every expectation placed upon them. If our systems only work for the “perfect victim,” then they were never truly designed for victims at all.

The silence that speaks

The recent judgment also prompted me to reflect on another aspect of institutional culture, silence. Within academia, even discussing judgments concerning one’s own institution may be framed as bringing the institution into disrepute. Such framing places academics in an impossible position. Those who speak are sometimes portrayed as being disloyal or as failing to respect the institution they serve. Yet genuine respect for an institution should not require silence in the face of injustice. Universities are places that encourage academic freedom, critical inquiry, evidence-based reasoning, and intellectual debate. They should, therefore, be places where uncomfortable conversations are not avoided but embraced.

The relative silence surrounding the judgment in academia raises important questions. Does silence reflect satisfaction that justice has been served? Does it reflect concern about damaging the reputation of one’s university? Does it reflect uncertainty about whether difficult institutional conversations are welcome? Or does it reflect a real or perceived fear of professional consequences for speaking openly? These are questions that deserve thoughtful reflection.

Post judgement reflections

At the same time, my experience in the weeks following the judgment has also been one of hope. Individuals who have experienced different forms of abuse have quietly come forward to share their own stories with me. Some have sought legal advice. Others have simply wanted someone to listen. Their experiences remind me that judgments do more than resolve disputes between parties. They send messages to those who have remained silent, that seeking justice remains possible. Perhaps that is one answer to the question I posed at the beginning of this article. Has anything actually changed? For some victims, I believe the answer is yes. A judgement can restore hope and encourage those who had previously felt that their voices would never be heard.

Yet judgments alone cannot erase trauma, restore lost years, or undo the personal and professional consequences that many victims endure. Courts can interpret the law, but they cannot, by themselves, transform institutional culture. Culture changes only when institutions and university communities are willing to learn from judgments rather than merely comply with them. It changes when realities of power imbalances are recognised, when credibility is assessed through evidence rather than stereotypes, and when the question “Why did the victim not come forward sooner?” is replaced with “What conditions made it so difficult for the victim to come forward?” Ultimately, the true value of a judgement lies not only in the orders it makes, but also in the conversations it inspires and the institutional self-reflection it demands. Whether anything truly changes will not depend on the judgement itself, but on whether institutions have the courage to learn from them.

(Udari Abeyasinghe is attached to the Faculty of Dental Sciences at the University of Peradeniya)

Kuppi is a politics and pedagogy happening on the margins of the lecture hall that parodies, subverts, and simultaneously reaffirms social hierarchies.

by Udari Abeyasinghe

Commander of the Navy pays courtesy call on Speaker of the Parliament

Woman suspected of Monaco bomb attack found dead in Ukraine

Balogun reprieve in vain as Belgium beat USA to set up Spain quarterfinal

Trump confirms he asked Fifa to review Balogun ban

Late Spain goal eliminates Portugal, ends Ronaldo’s international career?

Nyamhuri and Ngarava stun Bangladesh by defending 141

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News3 days ago

News3 days agoSingapore-based Buddhist monk marks nearly four decades of humanitarian service

-

News4 days ago

News4 days agoFreedom 250: US Embassy celebrates America’s 250th Independence Day through magic of American cinema

-

News5 days ago

News5 days agoCIABOC to question Harak Kata on Rs. 200 mn bribery allegation

-

News5 days ago

News5 days agoSLAF conducts successful rescue mission under UN command in Central African Republic

-

Midweek Review7 days ago

Midweek Review7 days agoH’tota port’s strategic status remains focal point of geopolitical scrutiny

-

News2 days ago

News2 days agoAI concerned over proposed SL military deployment in Haiti

-

News5 days ago

News5 days agoUNEP support pledged to strengthen Sri Lanka’s Environmental Priorities

-

Features3 days ago

Features3 days agoThe NPP’s New Challenge: Balancing Easter Lawfare and Economic Welfare