Business

First multi-stakeholder initiative on Child Rights in Tourism launched in Sri Lanka

On World Tourism Day, representatives from leading hotel businesses, tourism associations, NGOs, and government departments convened in Colombo to officially launch the Mother and Child-Friendly Seal for Responsible Business in Tourism. This pioneering initiative, the first of its kind in Sri Lanka, brings together key actors from the tourism supply chain to enhance the well-being of children and families connected to the sector through long-term, continuous actions.

The launch comes on the heels of a new study by The Centre for Child Rights and Business in partnership with Save the Children, highlighting serious child rights risks in Sri Lanka’s tourism industry. The study identifies key challenges such as sexual exploitation, child labour, and educational disruptions, driven by factors like inadequate regulation of guesthouses and homestays, the absence of child safeguarding measures among tourism providers, and a lack of formalised pathways to decent work for youth.

This event marks a significant milestone in the expansion of the Mother and Child-Friendly Seal, which has already seen success in Sri Lanka’s tea sector, with seven major plantation companies and exporters committing to initiatives that improve the welfare of tea communities. The extension of this Seal to the tourism sector is timely, as Sri Lanka prepares to welcome over 3 million tourists by 2025, positioning the industry to align with global human rights due diligence regulations and the growing demand for ethical tourism.

This event marks a significant milestone in the expansion of the Mother and Child-Friendly Seal, which has already seen success in Sri Lanka’s tea sector, with seven major plantation companies and exporters committing to initiatives that improve the welfare of tea communities. The extension of this Seal to the tourism sector is timely, as Sri Lanka prepares to welcome over 3 million tourists by 2025, positioning the industry to align with global human rights due diligence regulations and the growing demand for ethical tourism.

At the launch, stakeholders engaged in practical discussions about the child rights risks facing the tourism sector and explored collective solutions. Issues such as the outmigration of mothers and its impact on children were brought up, with participants offering valuable insights into areas for Seal members to address.

The panel discussed the critical issues that women and children face in the travel and tourism industries and some of the priorities and opportunities that the industry could address.

“Young children often do not realise they are being exploited. Providing a safe and respectful environment for them should be our primary goal. We must consider the risk factors in these scenarios, as there is currently no data to support issues in tourism, such as trafficking and exploitation. While problems like festival tourism have existed, they have increased since COVID-19 and have been exacerbated by the economic crisis,” said Buddhini Withana, Senior Technical Advisor Child Protection and Child Rights in Business, Save the Children.

Irstel Janssen, Director, Sustainable Sri Lanka added: “10% of women are working in this sector due to social stigma, safety concerns, and harassment. The economic crisis has forced women to step into this industry, but they are not employed in roles that match the nature of the work. The Seal initiative is an important step to address these issues and encourage more women’s participation.”

One of the highlights of the event was a keynote speech delivered by Cinnamon Hotels, where they underscored their commitment to protecting women and children. The company outlined key initiatives, including robust policies to support the female workforce, a zero-tolerance stance on misconduct, and a comprehensive sexual harassment policy. Cinnamon Hotels also conducts awareness sessions to educate staff about these policies, provides parental leave, and offers 100 days of paternity leave. Additionally, the company places a strong emphasis on mental health benefits for all employees. Their efforts served as an inspiration for other accommodation providers, offering practical steps to strengthen child safeguarding and empower women in the tourism sector.

For more information about the Mother and Child-Friendly Seal for Responsible Business, visit srilanka-motherandchildseal.org or contact info.SL@childrights-business.org.

Saudi Arabia has reaffirmed its long-term commitment to Sri Lanka’s economic and social development with the inauguration of the USD 50 million Faculty of Medicine at Sabaragamuwa University, a flagship investment expected to strengthen higher education, healthcare capacity and human capital while reinforcing the growing bilateral partnership between the two countries.

The project, financed by the Saudi Fund for Development (SFD), was inaugurated on Saturday in the presence of Prime Minister and Minister of Higher Education Harini Amarasuriya, Saudi Ambassador to Sri Lanka Khalid Hamoud Al Kahtani, SFD Deputy Chief Executive Officer Eng. Faisal Al-Kahtani, senior government officials and representatives of both countries.

Addressing the ceremony, Prime Minister Dr. Harini Amarasuriya described the project as another milestone in the enduring partnership between Sri Lanka and Saudi Arabia, expressing appreciation for the Saudi Fund for Development’s continued support in expanding higher education and creating opportunities for future generations of Sri Lankan students.

The premier said the new Faculty of Medicine would help address the country’s growing demand for qualified medical professionals while strengthening the national healthcare system.

Ambassador Khalid Hamoud Al Kahtani said the inauguration reflected the “strong and enduring partnership” between the Kingdom of Saudi Arabia and Sri Lanka and underscored the two nations’ shared commitment to education, healthcare and sustainable development.

The Ambassador added:”This achievement stands as a testament to our shared commitment to advancing education, healthcare and sustainable development.”

The Ambassador paid tribute to the Custodian of the Two Holy Mosques, King Salman bin Abdulaziz Al Saud, and Mohammed bin Salman for their vision and continued support for international development initiatives that foster economic cooperation and sustainable growth across partner countries.

He also commended the Saudi Fund for Development for financing and implementing the project, describing the Faculty as an investment in human capital, knowledge and Sri Lanka’s future healthcare workforce.

“We are confident that this new Faculty will play a vital role in educating future generations of medical professionals, serving the people of Sri Lanka and further strengthening the close friendship and cooperation between our two countries,” the Ambassador said.

SFD Deputy CEO Eng. Faisal Al-Kahtani said the project represented far more than a new academic institution.

“It is an investment in people, knowledge and opportunity. For more than four decades, the Saudi Fund for Development has partnered Sri Lanka in projects that improve lives and support sustainable economic and social development,” he said.

The state-of-the-art Faculty of Medicine features modern laboratories, para-clinical teaching facilities and a comprehensive library, significantly expanding Sri Lanka’s medical education infrastructure.

Since 1981, the Saudi Fund for Development has provided approximately USD 422.7 million through 15 development loans supporting 12 major projects in education, healthcare, water supply, transport and energy, making Saudi Arabia one of Sri Lanka’s key development partners in long-term infrastructure and human resource development.

By Ifham Nizam

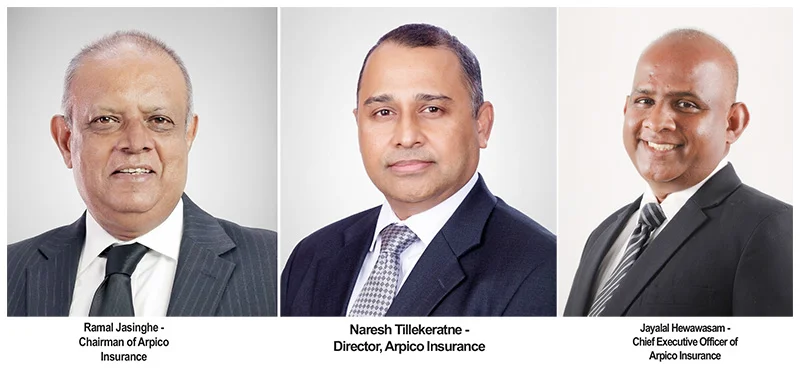

Arpico Insurance PLC, a renowned life insurance provider and a subsidiary of the blue-chip conglomerate Richard Pieris & Company PLC, has announced the appointment of Naresh Tillekeratne to its Board of Directors. This move further reinforces the Company’s commitment to operational excellence and stakeholder value as it embarks on its next phase of growth.

With a career spanning over 35 years in International Banking and Non-Bank Financial Institutions (NBFIs), Tillekeratne brings deep expertise in enterprise risk management, compliance, and corporate structuring. With over 15 years in C-level and senior management roles across Sri Lanka and the Middle East, he has forged a reputation for driving bottom-line efficiency and structural transformation.

Commenting on the appointment, Ramal Jasinghe, Chairman of Arpico Insurance PLC, stated “We are pleased to welcome Naresh Tillekeratne to our Board. He is a respected figure in the financial services landscape, recognised for his risk-management acumen and strategic foresight. As Arpico Insurance continues to scale and navigate complex and ever-evolving business and governance environments, his extensive cross-border experience will be invaluable in safeguarding stakeholder value and steering our sustainable growth trajectory.”

Prior to joining the board at Arpico Insurance PLC, Tillekeratne served as Chief Executive Officer of Assetline Finance PLC (previously Assetline Leasing Company Ltd), following a tenure as General Manager – Credit & Operations at AMW Capital Leasing and Finance PLC.

Jayalal Hewawasam, CEO of Arpico Insurance PLC, added “We are entering a dynamic phase of innovation and growth at Arpico Insurance, and strong corporate governance remains at the very heart of that journey. We are delighted to welcome Naresh Tillekeratne to our Board of Directors and the Company Management looks forward to working with him, and to harness his expertise in supporting our growth trajectory. We are confident that his proficiency in international banking, coupled with his acumen in enterprise risk management, will add tremendous depth to our leadership structure.”

Tillekeratne’s international exposure includes C-level responsibility at the Abu Dhabi Commercial Bank (UAE), where he engineered the restructuring of credit approval mechanisms and documentation controls to maximize portfolio returns. Prior to that, he completed a distinguished tenure spanning over two decades at Citibank NA Middle East, ascending to the level of Senior Vice President and Regional Head of Credit Risk Management for the Middle East, Egypt, and Pakistan. During his time with Citibank, he was also a key member of the specialized projects team tasked with advising and structuring financing for iconic state-backed development projects across Saudi Arabia, the UAE, Qatar, Egypt, and Bahrain.

Speaking on his new role, Tillekeratne noted “It is a privilege to join the Board of Arpico Insurance PLC, an institution anchored by the enduring 90-year legacy of the Richard Pieris Group. My primary focus will be to enhance our risk-governance architectures to ensure we meet our promises to policyholders while driving growth and innovation. I look forward to collaborating with the Board and the Senior Management to drive our strategic evolution with absolute integrity.”

Business

EFC new Chair reaffirms commitment to national employment policies and responsible business initiatives

The Employers’ Federation of Ceylon (EFC) recently concluded its 97th Annual General Meeting at the BMICH. At this general meeting, the Board of Trustees and Council Members representing different employer groups were appointed for the financial year 2026/27.

The outgoing Chairman, Dinesh Weerakkody expressed his appreciation to the Council, Members and the EFC Secretariat for the invaluable support extended to him throughout his tenure. Sanath Manatunge, Managing Director/CEO of the Commercial Bank of Ceylon PLC was appointed as the new EFC Chairman while Dinal Peiris, Chairman and Managing Director of the Lanka Aluminium Industries PLC Group was appointed as the Vice Chairman.

In his inaugural address, the new Chairman, while underlining the significance of the Federation, stated that, as the National Employers’ Organisation, the EFC will continue to contribute to labour law reforms that support future-ready businesses while driving responsible business initiatives. Manatunge who counts 36 years of experience having held very senior positions in the financial sector, presently serves on the Boards of Commercial Development Company PLC, and Commercial Bank of Maldives (Pvt) Ltd. as the Deputy Chairman. He is also the Chairman of the Sri Lanka Banks’ Association. Following his appointment as the new EFC Chair, the senior professional further emphasised the importance of engaging with the tripartite stakeholders to collaboratively advance shared objectives and strengthen Sri Lanka’s employment landscape.

Manatunge also represents key industry interests as a Member of the UNICEF Business Council, the Ceylon Chamber of Commerce, and the World Bank Group’s Private Sector Advisory Council. His regulatory and advisory contributions include serving as an Ex-Officio Member of the Stakeholder Engagement Committee of the Central Bank of Sri Lanka, as well as a Member of the Project Steering Committee (PSC) for the Central Bank’s Fraud Risk Management (FRM) System.

Balogun reprieve in vain as Belgium beat USA to set up Spain quarterfinal

Trump confirms he asked Fifa to review Balogun ban

Late Spain goal eliminates Portugal, ends Ronaldo’s international career?

Nyamhuri and Ngarava stun Bangladesh by defending 141

Sri Lanka try to make a play after Greaves 180, Hope 112

Dry weather except for a few showers in the Western and Sabaragamuwa provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News2 days ago

News2 days agoSingapore-based Buddhist monk marks nearly four decades of humanitarian service

-

News3 days ago

News3 days agoFreedom 250: US Embassy celebrates America’s 250th Independence Day through magic of American cinema

-

News4 days ago

News4 days agoCIABOC to question Harak Kata on Rs. 200 mn bribery allegation

-

News4 days ago

News4 days agoSLAF conducts successful rescue mission under UN command in Central African Republic

-

Midweek Review6 days ago

Midweek Review6 days agoH’tota port’s strategic status remains focal point of geopolitical scrutiny

-

News1 day ago

News1 day agoAI concerned over proposed SL military deployment in Haiti

-

News4 days ago

News4 days agoUNEP support pledged to strengthen Sri Lanka’s Environmental Priorities

-

Features2 days ago

Features2 days agoThe NPP’s New Challenge: Balancing Easter Lawfare and Economic Welfare