News

Verite shows how Lanka can achieve sustainable debt dynamics

Verité Research, a private think tank that provides strategic analysis for Asia, hosted the online discussion Steering out of the Debt Crisis: Recipe for Budget 2022 on Oct 14. The event was anchored around addressing Sri Lanka’s debt and USD liquidity crisis, and featured presentations by Executive Director, Nishan de Mel, Research Director, Deshal de Mel, and Analyst Anushan Kapilan. An expert panel included Dr. Shantayanan Devaranjan (Georgetown University), Dr. Nandalal Weerasinghe (former Senior Deputy Governor – CBSL) and Dr. Mick Moore (Institute of Development Studies – UK).

A press release issued by the think tank said: Verité Research presented analysis pertaining to debt management and fiscal measures, including specific proposals to increase government revenue and improve the allocation of expenditure.

The Verité Research analysis showed that Sri Lanka can achieve sustainable debt dynamics by meeting two conditions with regard to its domestic debt, and two further conditions with regard to its foreign debt. The presentation explained that, despite some challenges, achieving these conditions was feasible for Sri Lanka – provided policy-makers choose to do so.

The main challenges arise from poorly formulated fiscal/budget measures, coupled with the pandemic-induced setbacks which have resulted in successive downgrades of Sri Lanka’s credit ratings. As a result, Sri Lanka has been locked out of global capital markets, and rapidly depleted its foreign reserves, as it has continued to pay back foreign bondholders, at the expense of negative feedback on the local economy.

The Verité Research analysis showed that the worst is yet to come. Sri Lanka’s foreign reserve would be completely depleted by the end of 2022 if no surprise inflows materialise, and even if they did, the crisis would simply re-emerge in 2023. This means that even if Sri Lanka can claim to be technically solvent, it does not have the liquidity to sustainably pay back its foreign debt until the country credit rating is improved by at least two notches.

The current path of repaying debt offers a high return to bondholders at the expense of huge pain to domestic businesses and consumers, and makes the credit rating outlook even more precarious. The solution is to share the pain with bondholders by pre-emptively restructuring the debt. This can improve the foreign reserve position more quickly, and thereby improve the country’s credit rating more quickly as well. This alternative path is less painful to the local economy, offers a faster recovery, with a higher probability of success. It is a better path for the Sri Lankan economy than repaying foreign bondholders in full, even if it were able to do so.

A clear distinction needs to be made between a forced restructuring which would occur if a country were to default in a disorderly way without negotiating with creditors, and an orderly pre-emptive restructuring of debt following negotiations with creditors. The sooner Sri Lanka moves to an orderly pre-emptive debt restructure, the easier it would be to do so, and the more favourable it would be for the Sri Lankan economy. Delaying the decision is damaging and can result in outcomes that are highly disruptive.

Currently the primary deficit is at 7.4% of GDP. At the current GDP growth rate of a little under 4% (predicted by Verité Research), it is necessary to reduce the primary deficit to around 2% of GDP or less to help stabilise the debt.

The Verité Research analysis showed that in the base case scenario with no policy changes, the debt to GDP Ratio would increase to 123.08% by 2025, however with prudent fiscal measures it can be kept down to 108.8% by 2025.

The fiscal measures proposed included the reduction of the personal income threshold to LKR 1 Mn per Annum; the reintroduction of PAYE with a threshold of LKR 1.5Mn; reintroduction of WHT on interest income; increasing the VAT rate to 10% in 2022 and to 12% in 2023; reducing the VAT free thresholds from LKR 300 Mn to LKR 150 Mn in 2022; simplifying the corporate tax regime to a three-tier regime; and increasing the total taxes on cigarettes and alcohol in line with increases in inflation and GDP according to a tobacco taxation formula introduced in the 2019 budget.

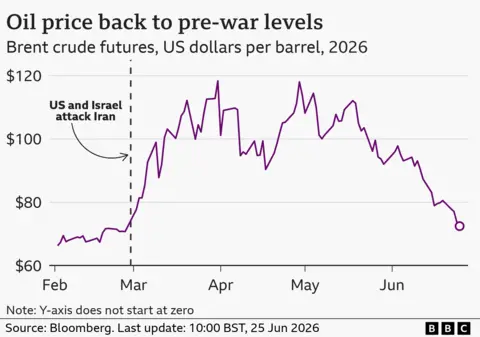

The price of oil has fallen to levels not seen since before the Iran war as traffic through the key Strait of Hormuz shipping route gradually resumes.

Global benchmark Brent crude briefly fell below $72.48 (£55) a barrel, the price it was at the day before the US and Israel launched attacks on Iran on 28 February, before edging up to $73.23.

Energy prices have been on a wild ride since Iran responded to the strikes by effectively closing the strait, a critical waterway for oil and gas shipments.

The cost of crude has been moving sharply lower since the US and Iran signed a Memorandum of Understanding (MOU) on 17 June which set out a 60-day period for negotiations on Tehran’s nuclear programme and other measures to end the war.

Representatives from the two sides met in Switzerland last weekend for talks to end the war, which resulted in the US partially lifting sanctions on Iranian oil exports.

The number of vessels crossing the Strait of Hormuz has risen significantly since the MOU was signed, according to maritime intelligence firm Kpler.

Its latest data suggests 284 vessels have made the transit from 18 June, the day after the deal was signed, although that is is still well below the pre-conflict average of some 138 crossings each day.

The ships passing through the waterway in recent days include those carrying crude oil, liquefied natural gas (LNG), fertiliser and other goods, Kpler told the BBC.

The US and Iran had also formed a “communication line” to prevent misunderstandings “with the aim of safe passage for commercial vessels through the Strait of Hormuz”, mediators Qatar and Pakistan said in a joint statement on Monday.

There has been a “tremendous shift” with far more ships using the strait in recent days, said Dimitris Maniatis, the chief executive of Marisks, a maritime risk advisory firm working with ships stuck in the region.

A limited number of ships can cross a northern passageway with the permission of Iranian authorities, he said.

The US navy has also provided guidance for vessels to travel through a southern route that is safe from mines and other obstacles that has been laid out since the war, Maniatis said.

But the number of ships crossing the strait is still below levels seen before the war, when it was used by more than 100 ships a day.

Hundreds of ships still appear to be waiting in the Gulf.

Fuel prices at the pump rose sharply when the Iran war began, and now the focus is on how quickly they will fall.

“On the back of the lowest oil price since before the Iran war started, drivers should see the average price of petrol fall below 150p [a litre] in the next week or so,” said Simon Williams, head of policy at UK motoring group the RAC. He added the price of diesel “ought to go back under 160p.

Petrol peaked at 159.53p a litre on 28 May, according to the RAC, while diesel has fallen from a high of 191.54p on 15 April.

The average price of regular gasoline in the US has dropped to around $3.93 a gallon after reaching $4 a gallon in April, its highest since 2022, but is still well above pre-war levels.

US President Donald Trump on Wednesday ordered an investigation into major energy companies, accusing Shell, ExxonMobil and other firms of “gouging” drivers by not reducing fuel prices even as oil costs fell.

“Oil prices have come down so much and we are not seeing anything at the pump by comparison the way they should be,” Trump told reporters in the Oval Office.

The American Petroleum Institute, which represents the oil and gas industry in the US, said fuel prices “don’t move in lockstep with crude oil”.

British energy firms have faced similar accusations of unfairly hiking petrol prices since the Iran war.

The UK competition watchdog said last month that there was no widespread evidence of this, adding that average profit margins were “broadly unchanged” between February and March

(BBC)

Representatives from the ’The Ceylon Chamber of Commerce’ met with Prime Minister Dr. Harini Amarasuriya on Wednesday [24th of June] at the Parliament premises.

During the meeting, discussions focused on the Sri Lanka Economic and Investment Summit 2026 (SLEIS 2026), which is scheduled to be held on 12 and 13 October 2026. Attention was also given to digitalization initiatives, the introduction of digital technologies in schools under new education reforms, and the transformative role of Artificial Intelligence (AI) in Sri Lanka’s education sector.

Representatives of the Chamber noted that the summit would serve as an important platform for encouraging both local and foreign investment, while also contributing to the shaping of the country’s future economic policies.

The meeting was attended by Krishan Balendra, Chairman of The Ceylon Chamber of Commerce; Vinod Hirdaramani, Deputy Vice Chairman; Shiran Fernando, Secretary General and Chief Executive Officer; Aliki Perera, Deputy Secretary General and Chief Operating Officer; and Anagi Rodrigo-Weerasekera, Chief Economist and Head of Economic Intelligence, along with several other representatives.

[Prime Minister’s Media Division]

A discussion to review the progress of the housing project under which 4,700 houses are being constructed for the Malayagam community with Indian assistance was held this afternoon (24) at the Presidential Secretariat under the chairmanship of the Chief of Staff to the President, Prabath Chandrakeerthi.

Under this housing programme, 2,026 houses are to be provided to families identified by the National Building Research Institute (NBRI) as being at disaster risk. The remaining houses are expected to be allocated to eligible workers residing in the plantation sector.

Accordingly, the houses will be provided to Malayagam community families living on estates belonging to 22 Regional Plantation Companies, as well as estates under the State Plantations Corporation, Janawasama and Elkaduwa Plantations.

For the construction of each house, the Government of India has allocated Rs. 2.8 million, while the Government of Sri Lanka has contributed Rs. 400,000.

During the discussion, Chandrakeerthi instructed officials to ensure that the housing project is completed before the end of this year. He further directed that land identified for the construction of houses be released without delay and that the National Building Research Institute provide the necessary reports to identify suitable land for the project.

The housing project is being implemented jointly by the Ministry of Plantation and Community Infrastructure, the National Housing Development Authority, the State Engineering Corporation and the Plantation Human Development Trust.

Among those present were Additional Secretary (Development) of the Ministry of Plantation and Community Infrastructure, K. S. Wijayakeerthi; Director General (Engineering), N. D. N. Pushpakumara; Director General (Planning), W. A. K. S. Damayanthi; the Secretary General of the Planters’ Association; and officials from the National Housing Development Authority, the State Engineering Corporation, relevant institutions and plantation companies.

(PMD)

Sri Lanka seek big win against Scotland to keep semi-final hopes alive

Oil price falls back to pre-Iran war levels

Venezuela earthquakes: At least 164 dead, 971 injured as toll rises

Representatives from the Ceylon Chamber of Commerce meet PM

Progress of Housing Project for Malayagam Community families funded by India reviewed

South Africa stun South Korea to reach World Cup knockouts for the first time

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News7 days ago

News7 days agoCreditor receives USD 2.5 mn as Lankan public bears loss from theft of Treasury funds

-

News6 days ago

News6 days agoCreditor not yet paid

-

News6 days ago

News6 days agoConsumers bearing 22% tax burden despite 18% VAT claim: Dr. Harsha de Silva

-

Features5 days ago

Features5 days agoNanda Pethiyagoda Wanasundara as three generations of family saw her

-

Features4 days ago

Features4 days agoSri Lanka developing independent hydrographic capabilities

-

Opinion7 days ago

Opinion7 days agoSriLankan Airbus struck by lightning

-

Editorial5 days ago

Editorial5 days agoFuel crisis: Beyond price debate

-

Latest News4 days ago

Latest News4 days agoSooryavanshi thumps fastest List A fifty as India A win tri-series