Business

Special goods and services tax: Issues and concerns

By Dr Roshan Perera & Naqiya Shiraz

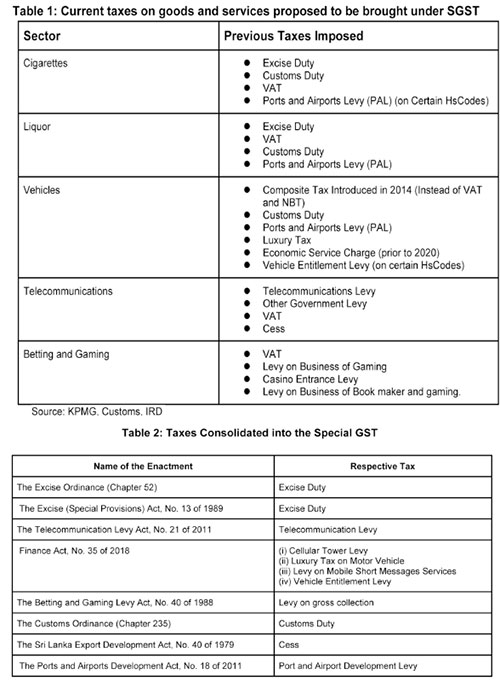

The new bill titled ‘Special Goods and Services Tax’ was published by gazette dated 07 January 2022.1 The Special Goods and Services Tax (SGST) was originally proposed in Budget speech 2021 but was not implemented. It has once again been presented in Budget 2022. The SGST aims to consolidate taxes on manufacturing and importing cigarettes, liquor, vehicles and assembly parts, while also consolidating taxes on telecommunication and betting and gaming (see table 1 for existing taxes on these products and table 2 for taxes consolidated into the SGST as per the schedule in the gazette). The rationale for this new tax as per the bill is “…to promote self-compliance in the payment of taxes in order to ensure greater efficiency in relation to the collection and administration on such taxes by avoiding the complexities associated with the application and administration of a multiple tax regime on specified goods and services.”

Given the multiplicity of taxes and the complexity of the current tax system as a whole, rationalising taxes is necessary to improve collection. However, whether the proposed SGST simplifies the tax system, while ensuring revenue neutrality or even improving revenue collection, needs to be carefully examined.

The SGST Bill is silent on the treatment of the existing VAT on these goods and services. However, according to the Value Added Tax (Amendment) Bill also gazetted on 07 January 2022,1 liquor, cigarettes and motor vehicles will be exempted from VAT while telecommunications and betting and gaming services will still be subject to VAT.

While the gazetted Bill sets out some of the features of the proposed SGST there are many important areas not covered in the Bill. These are expected to be gazetted as and when required by the Minister in charge.

Issues & Concerns

The motivation behind SGST is the simplification of the tax system. Although the objective of introducing the SGST is to improve efficiency by reducing the complexity of the tax system there are many issues and concerns with this proposed tax.

Revenue

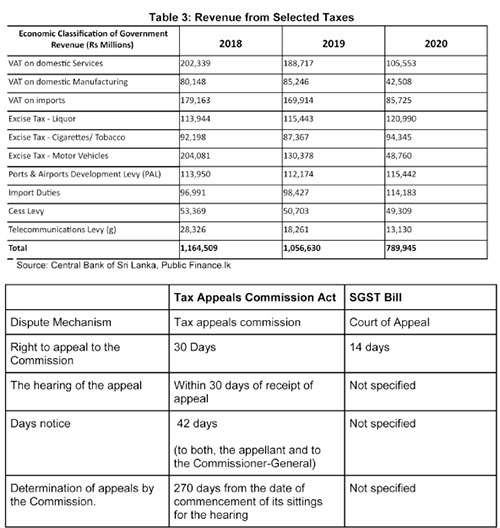

Tax revenue which was 13% of GDP in 2010, declined to 8% in 2020. Ad hoc policy changes and weak administration contributed to the decline in tax revenue collection. This continuous decline in tax revenue has led to widening fiscal deficits and increasing debt. One of the main reasons for the current macroeconomic crisis is low tax revenue collection. Hence, any change to the existing tax system should be with the primary objective of raising more revenue.

According to the budget speech the SGST is estimated to bring in an additional Rs. 50 billion in revenue in 2022.1 Revenue from taxes proposed to be consolidated under the SGST has significantly declined over the past 3 years. Given the already difficult macroeconomic environment, along with ad hoc tax policy changes raising the additional revenue estimated at Rs. 50 billion seems a difficult task.

Tax Base and Rate

For the SGST to raise taxes in excess of what is already being collected through the existing taxes, the rate and the base for the SGST needs to be carefully and methodically calculated. Further, the existing taxes have different bases of taxation. For instance the basis of taxation of motor vehicles is both on an ad valorem1 basis and a quantity basis while the basis of taxation of cigarettes and liquor is quantity.2 In light of this, the basis of taxation on which SGST isapplied becomes an issue. Having different bases and different rates for various goods and services would complicate the implementation of the tax These issues need to be carefully considered to ensure the new tax is revenue neutral or be able to enhance revenue collection.

Efficiency

One possible revenue benefit of this proposal is the inability to claim input tax credits on the sectors exempted from VAT. However, the issue is the cascading effect that would result where there would be a tax on tax with the end consumer paying taxes on already paid taxes. If the idea was to raise additional revenue by limiting tax credits, it would have been simpler to raise the tax rates on the existing taxes rather than introduce a new tax.

4. Administration

According to the bill, SGST will now be collected through a new unit set up under the General Treasury where a Designated Officer (DO) will be in charge of the administration, collection and accountability of the tax. The existing revenue collection agencies, such as the Inland Revenue Department (IRD) or the Excise Department will not be primarily responsible for the collection of this tax. By removing the IRD and Excise Department, a parallel bureaucracy will be created, at a time when public spending needs to be carefully managed. The General Treasury also has no previous experience and expertise in direct revenue collection. Weak administration is one of the key reasons for the low tax collection and success of this tax would depend on the strength of its administration.

In addition to the above mentioned concerns, as per the Bill the minister in charge of the SGST has been vested with the power to set the rates, the base and grant exemptions. Accordingly, Parliamentary oversight over fiscal matters is weakened under this proposed Bill.

It could also lead to a time lag between the gazetting and implementing of changes to the SGST (such as the rate, base etc) and obtaining Parliamentary approval for those changes.

Dispute resolution

The SGST Bill also focuses on the dispute resolution mechanism. Under the present tax system, with the enactment of the Tax Appeals Commission Act, No. 23 in 2011 the Tax Appeals Commission has the “responsibility of hearing all appeals in respect of matters relating to imposition of any tax, levy or duty”.1 The most recent amendment to the Tax Appeal

Commissions act (2013)1 seeks to address the large number (495) of cases pending before the Tax Appeals Commision2 by increasing the number of panels to hear the appeals.

Under the proposed SGST disputes will be handled through the court of appeal. However, the time period by which specific actions need to be taken is not provided in the bill. In addition, disputes have to be taken to the court of appeal. Hence, the entire process will be more time consuming. This could result in revenue lags and difficulties in revenue estimation until disputes are resolved.

Additionally, in the case that no valid appeal has been lodged within 14 days, any remaining payments would be considered to be in default. Thereafter, the responsibility is shifted to the Commissioner General of the IRD to recover the dues. Given the IRD is completely removed from the normal collection process, the rationale for bringing defaults under the IRD is not clear.

III. Policy Recommendations

As discussed, the SGST Bill has several limitations and much of this is due to the ambiguities in the Bill.

If the tax is implemented, the rate and basis of taxation needs to be revenue neutral to ensure tax collection is maximised and administrative costs minimised.

The rates, basis of taxation, exemptions etc should be specified in the Bill, as done in most other Acts. This would avoid the power for discretionary changes to the tax being placed in the hands of the minister in charge.

Given the already weak tax administration, it would be more sensible to strengthen the existing revenue collecting agencies and address the weaknesses in the existing system without creating a parallel bureaucracy.

In the case where VAT is consolidated into the proposed GST, the issue of cascading effect of input tax credits needs to be addressed. This is relevant particularly in the case of capital expenditure.

Given the critical state of revenue collection in the country the question to ask is whether this is the best time to introduce a new tax. Focus should be on fixing issues in the existing tax system to ensure revenue is maximised. The VAT is the least distortionary tax and it is the easiest to administer. Given these features it can be a very efficient revenue generator for a country. Therefore instead of introducing a new tax, capitalising on systems that are already in place and amending the VAT rate, threshold and exemptions may be a more practical solution to the revenue problem that the country is currently facing.

Dr. Roshan Perera is a Senior Research Fellow at the Advocata Institute and the former Director of the Central Bank of Sri Lanka.

Naqiya Shiraz is a Research Analyst at the Advocata Institute.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

As agreed with the Sri Lanka Banks’ Association (Guarantee) Ltd. (SLBA), to provide relief measures to affected SMEs by licensed commercial banks and licensed specialised banks, Circular No. 04 of 2024 dated 19.12.2024, and its addendum, Circular No. 01 of 2025 dated 01.01.2025 were issued by the Central Bank of Sri Lanka to ensure the effective implementation of the relief measures specified in the cited Circulars in a consistent manner across all licensed banks.

In case of any rejections or disputes, borrowers are requested to contact the respective banks and to appeal to the Director, Financial Consumer Relations Department of CBSL (FCRD), if required through the following channels:

Based on the repayment capacity and the submission of an acceptable business revival plan by the borrower, the relief measures extended to affected SMEs include rescheduling of credit facilities up to a period of 10 years, extending the time to commence repayments based on the capital outstanding, waiving off unpaid interest subject to conditions, and providing new working capital loans. Despite the availability of the above relief measures, limited number of borrowers had approached licensed banks to avail themselves of these benefits to date.

In addition to the above measures, with the gradual recovery of the economy, in order to facilitate the sustainable revival of businesses that were adversely affected during the recent past, several other measures were taken by CBSL together with the banking industry.

Accordingly, inter alia, strengthening the Post Covid 19 revival units of licensed banks, CBSL issued Circular No. 02 of 2024 dated 28.03.2024 on “Guidelines for the Establishment of Business Revival Units of Licensed Banks” mandating banks to establish Business Revival Units (BRUs) to assist viable businesses that are facing financial and operational difficulties.

Under BRUs, banks may provide support to viable businesses, such as restructuring and rescheduling of credit facilities including the adjustment of interest rates, maturity extensions, providing interim financing, advisory services etc., subject to the condition that such borrowers are required to submit acceptable business plans and feasible repayment plans. As reported by banks, by the end of 2024, around 6,000 facilities had been facilitated through these BRUs.

The above cited Circulars and Guidelines can be accessed via https://www.cbsl.gov.lk

Visa (NYSE: V), the global leader in digital payments reiterated its support to women entrepreneurs across Sri Lanka as a part of its International Women’s Month celebrations across the world, by stating a firm commitment towards financial inclusion and digitization of women-led businesses, and hosted women from different walks of life in a specially curated event at Colombo.

Avanthi Colombage, Country Manager for Visa in Sri Lanka and Maldives stated, “At Visa, we believe in being the best way to pay and be paid by uplifting everyone, everywhere. This year, we celebrated International Women’s Month to support the very capable businesswomen in our country, with an event titled ‘Overcoming Barriers to Growth’ along with Square Hub, an incubator and business accelerator.”

The event by Visa brought together 35 upcoming women entrepreneurs across various sectors, including fashion, e-commerce, fintech, technology, manufacturing, and agriculture. While prominent industry experts shared views, learnings and experiences from their own journeys, the event also facilitated open discussions and networking among entrepreneurs, on how they can build and sustain thriving businesses.

Avanthi elaborates that Visa has built a firm foundation in supporting female entrepreneurship and the empowerment of women in Sri Lanka and understands the challenges women-owned businesses face when seeking capital, access, networks and guidance and continues to actively uplift women in Sri Lanka. Globally and in Sri Lanka, Visa believes that the participation of women is key to the growth of an economy. Avanthi adds, “Two years ago, when we celebrated 35 years of Visa in Sri Lanka, we announced a grant for The Asia Foundation to assist women-led small and medium businesses (SMBs) throughout the country. This initiative offered vital seed funding, skills training, and financial inclusion opportunities for women entrepreneurs, helping remove some major barriers to their success,” she recalled.

Environmental groups, including the Wildlife and Nature Protection Society (WNPS), the Centre for Environmental Justice (CEJ) and the Environmental Foundation Ltd. (EFL), are raising renewed concerns about the potential ecological impact of large-scale wind energy development on Mannar Island. Conservationists argue that the island, home to a unique and sensitive ecosystem, faces serious risks from industrial projects that may disrupt biodiversity and endanger local wildlife.

At the heart of the controversy is whether the environmental issues raised by Adani Group’s proposed wind energy project in Mannar were being adequately considered. Critics argue that tariff negotiations and economic interests overshadowed ecological assessments, potentially leading to a project that might compromise the island’s rich natural heritage.

“Can wind energy coexist with Mannar Island’s fragile ecosystem? asked environmental scientist Hemantha Withanage of the CEJ.

He told The Island Financial Review: “We must ensure that our transition to renewable energy does not come at the cost of irreplaceable biodiversity.”

Other conservationists have pointed out that environmentalists are often misrepresented as obstructionists in debates over development. “Are we being painted as enemies of progress, or is the public being misled about the real consequences of such projects? questioned Dr. Rohan Pethiyagoda, a leading environmental advocate.

With Adani’s possible withdrawal from the project, there is now an opportunity to reevaluate Sri Lanka’s approach to sustainable energy. Experts emphasize the need for a smarter, science-driven path that prioritizes both renewable energy and environmental conservation.

A joint media conference, scheduled for today at the Dutch Burgher Union, Colombo, aims to address these concerns. Organized by WNPS, CEJ, EFL and Pethiyagoda, the event will explore questions such as whether the project might resurface under a new guise and who the true beneficiaries of such large-scale energy initiatives are.

By Ifham Nizam

Cabinet approves providing relief to the people of Myanmar

Cabinet appoints ministerial committee to submit report on sanctions imposed on 04 Sri Lankans by the United Kingdom

Revised Aswasuma Welfare Benefit Payment Scheme to be submitted for the concurrence of the Parliament.

-

Sports4 days ago

Sports4 days agoSri Lanka’s eternal search for the elusive all-rounder

-

News3 days ago

News3 days agoBid to include genocide allegation against Sri Lanka in Canada’s school curriculum thwarted

-

News5 days ago

News5 days agoGnanasara Thera urged to reveal masterminds behind Easter Sunday terror attacks

-

Business6 days ago

Business6 days agoAIA Higher Education Scholarships Programme celebrating 30-year journey

-

News4 days ago

News4 days agoComBank crowned Global Finance Best SME Bank in Sri Lanka for 3rd successive year

-

Features4 days ago

Features4 days agoSanctions by The Unpunished

-

Latest News2 days ago

Latest News2 days agoIPL 2025: Rookies Ashwani and Rickelton lead Mumbai Indians to first win

-

Features4 days ago

Features4 days agoMore parliamentary giants I was privileged to know