Business

Is wealth tax the solution to Sri Lanka’s low tax revenue collection?

By Sathya Karunarathne

Successive governments have run fiscal deficits. Inadequate revenue collection and unrestrained government expenditure have worsened the country’s fiscal position.

Tax revenue which averaged over 20% of GDP in 1990 has declined to under 10% of GDP in 2020. Ad hoc tax policy changes have significantly eroded the tax base. Weak tax administration has also contributed to the sharp decline in tax collection.

While tax revenue has contracted, government expenditure has ballooned over time. Today, government revenue is not sufficient even to meet its expenditure on salaries and wages and transfers and subsidies to households which include pension payments and social welfare payments such as Samurdhi.

In this context, there are various proposals put forward to raise government revenue. One proposal is the reintroduction of the wealth tax.

A wealth tax is expected to bridge the gap between the rich and the poor, achieving equality. This tax shifts the tax burden to affluent households, taxing an individual’s net wealth, which is the market value of total owned assets. Proponents of wealth taxation argue that this is a progressive system of taxation and is a more powerful tool in comparison to income, estate or corporate taxes as it addresses the issue of wealth concentration.

Moreover, a tax should ideally satisfy basic characteristics of taxation: it should not be distortionary; it should be fair, and it should not be difficult to collect.

The rationale for a wealth tax

One of the earliest proponents of the wealth tax for developing countries was Nicholas Kaldor. Based on his recommendation, a wealth tax together with an income tax, expenditure tax and a gift tax were introduced in Sri Lanka in 1958.1 However, these new taxes yielded little revenue due to difficulties in determining the tax base and problems in administration. Following the recommendation of the Tax Commission in 1990,2 the government abolished the wealth tax from the year of assessment 1992/1993.3

Wealth taxes have mainly been implemented in European countries. In 1990, twelve countries in Europe had a wealth tax. Today, there are only three: Norway, Spain, and Switzerland. Several non-European countries have also imposed wealth taxes from time to time including such as Argentina, Bangladesh, Colombia, India, Indonesia, Pakistan

In recent times there has been renewed interest in wealth taxes. Presidential candidates in the US proposed various forms of a wealth tax. In the UK and France, there were proposals to impose “super taxes” on the rich. The primary justification was to address the increasing inequality in society.

Issues with a wealth tax

Despite renewed interest in the wealth tax as a progressive tax based on equity, it scores poorly on the criteria of efficiency, and administrative feasibility.4

Many factors have justified the repeal of wealth taxes in OECD countries. The reasons cited are related to efficiency costs, risk of capital flight particularly in light of increased capital mobility and wealthy taxpayers’ access to tax havens, failure to meet redistributive goals as a result of narrow tax bases, tax avoidance and evasion, high administrative and compliance costs compared to limited revenues (high cost yield ratio).5

To understand the efficiency costs of wealth taxes one can look at taxing a person’s wealth accumulated through savings. Despite the common consensus that taxing savings is an effective way to redistribute, a person’s saving decisions reveal little about their underlying lifetime resources and wellbeing. It only reveals their preference to consume tomorrow rather than today. Thereby a wealth tax imposes a tax on those who prefer to spend their money later as opposed to taxing the wealthy.6 Efficiency costs refer to the reduction of the welfare of the taxed individuals by more than $1 to generate $1 of revenue.7 Therefore, the efficiency cost of a wealth tax in terms of taxing savings is a reduction of future consumption that can be bought with earnings, reducing incentive to work for those who prefer to consume the proceeds later and reducing incentive for young people to save for their retirement.8

Capital flight is the possibility of holding assets outside of one’s resident country without declaring them.As wealth taxes are imposed on residents it increases the risk of the wealthy reallocating their assets to avoid taxation. Therefore a high tax burden encourages taxpayers to change their tax residence to a lower tax jurisdiction or tax havens.9

Both income-generating and non-income generating assets are taxed under wealth taxation. They can include land, real estate, bank accounts, investment funds, intellectual or industrial property rights, bonds, shares, and even jewellery, vehicles, art and antiques.10 However, this tax base for wealth taxes has often been narrowed through exemptions. These exemptions have been justified most commonly on the grounds of social concerns such as the negative social implications of taxing pension assets. Further liquidity issues (eg – farm assets), supporting entrepreneurship and investment (eg- business assets), avoiding valuation difficulties ( eg- artwork and jewellery) and preserving countries cultural heritage (eg – artwork and antiques) have also been cited as reasons for wealth tax reliefs. While some of these exemptions can be justified, they have led to the reduction of revenue raised from wealth taxes. They have also contributed to wealth taxes being less equitable as the wealthiest such as businesses benefit from these exemptions defeating the very purpose of imposing a wealth tax which is to meet its redistributive goals.11

Narrow tax bases in wealth taxation often leads to tax avoidance and evasion opportunities. For example, Spain’s 1994 wealth tax exemption for the shares of owner managers resulted in wealthy businesses reorganizing their activities to reap benefits of the exemption resulting in a significant erosion of the wealth tax base.12

Further, several other factors have also discouraged countries to sustain a wealth tax. They are namely, the difficulty in determining the tax base or what assets to be taxed, underreporting and undervaluation of assets, difficulty in measuring wealth taxes13, distinguishing between individuals who are asset rich but cash poor, the constant need to value assets and audit returns increasing administrative and enforcement costs .

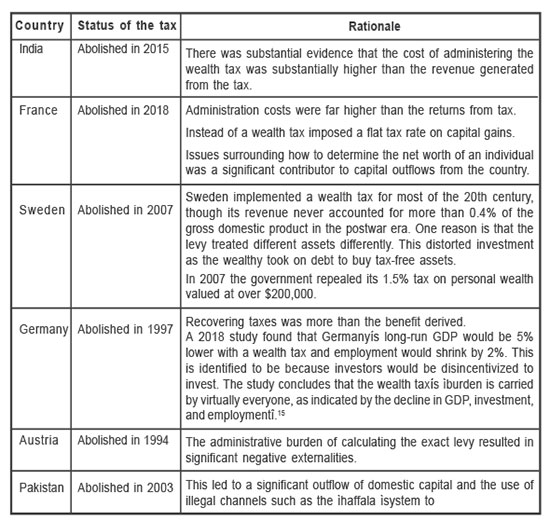

Low revenue collection as well as the other reasons discussed have led to the abolishing of wealth taxes in most countries (See Table 1 for details) . Tax revenue from individual net wealth taxes in 2016 ranged from only 0.2% of GDP in Spain to 1.0% of GDP in Switzerland. Sri Lanka’s experience with wealth taxation was no different with the tax yielding low revenue as reported by the 1990 Tax Commission.14

Conclusion

Taxing the wealth of the rich to generate income and to eliminate economic inequality sounds promising in terms of political debate. However, wealth taxes have failed to generate adequate revenue, failed to meet redistributive goals as a result of narrow tax bases, proven to have high administrative and enforcement costs, resulted in tax evasion and avoidance due to underreporting and undervaluation of assets, increased the risk of capital flight and access to tax havens and may have contributed to the reduction of investment and employment.

Therefore, imposing a wealth tax may not be the ideal policy response to Sri Lanka’s low tax revenue, especially given the country’s previous experience with the tax yielding low revenue.

Sathya Karunarathne is the Research Analyst at the Advocata Institute and can be contacted at sathya@advocata.org. Learn more about Advocata’s work at www.advocata.org. The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

09 March 2026; Colombo – SriLankan Airlines would like to inform passengers that it is resuming daily services to Riyadh tonight and Dubai tomorrow, while continuing to closely monitor the situation in the Middle East and prioritising the safety and wellbeing of its passengers and crew.

The following flights are scheduled to operate:

For more information please contact: 1979 (within Sri Lanka); +94 11 777 1979 (international); WhatsApp +94 74 444 1979 (chat only); your travel agent; visit www.srilankan.com; or follow us on social media.

Global oil prices have jumped above $100 (£75.11) a barrel for the first time since 2022 as the escalating US-Israeli war with Iran has fuelled fears of prolonged disruption to shipments through the Strait of Hormuz.

Iran on Sunday named Mojtaba Khamenei to succeed his father Ali Khamenei as Supreme Leader, signalling that a week into the conflict hardliners remain in charge of the country.

The US and Israel launched fresh waves of airstrikes across Iran over the weekend, hitting multiple targets including oil depots.

Major disruption to energy supplies from the region threatens to push up prices for consumers and businesses around the world.

Early on Monday in Asia, Brent crude was around 15.5% higher at $107.16, while Nymex light sweet was up by more than 17% at $106.77.

Stock markets in the Asia-Pacific region fell sharply in early trading on Monday, with Japan’s Nikkei 225 index down by more than 5% and the ASX 200 in Australia more than 3.5% lower.

Many in the markets predicted that oil would hit the $100 a barrel mark this week.

In the event it took about a minute to jump 10%, and then another 15 minutes to rise a further 10% in early Asian trading.

Last week the markets had been relatively relaxed about the seeming nightmare scenario for millions of barrels of crude and liquefied natural gas trapped in the Gulf, unable or unwilling to transit the Strait of Hormuz.

But the escalations over the weekend, alongside scenes of destruction of energy infrastructure both in Iran and across the Gulf, saw the markets take rapid fright.

The question now is where does this go? Some analysts argue that if the shutdown in the strait lasts until the end of March, we could see record oil prices above $150 a barrel.

The existing rise is likely to further increase petrol prices, and those of important derivative products such as jet fuel and vital precursors for fertilisers.

The physical supplies from the Gulf are mainly consumed in Asia.

Already however there are signs that Asian consumers are bidding up prices for US gas, with some tankers originally heading for Europe turning around in the mid-Atlantic.

US President Donald Trump responded to the jump in prices by saying that short term rises were a “small price to pay” for removing Iran’s nuclear threat.

His energy secretary told US broadcasters on Sunday that Israel, not the US, was targeting Iran’s energy infrastructure, amid some concern about rising domestic pump prices caused by the war.

(BBC)

The Ceylon Motor Traders’ Association (CMTA) has issued a stark cautionary note to prospective vehicle buyers, warning that the initial price advantage of reconditioned imports often masks significant long-term financial risks.

By highlighting a “structural imbalance” in the current duty valuation system – which allows near-identical vehicles to be imported under a 15% automatic depreciation bracket – the CMTA argues that the lack of manufacturer-backed warranties and tropicalised specifications in the grey market could lead to a “reconditioned trap” for unsuspecting consumers. For the savvy buyer, the association suggests that the true cost of ownership is increasingly tilting the scales in favour of brand-new vehicles from authorised agents.

If two identical 2026 models are sitting on different lots, and one is significantly cheaper because it was technically “registered and de-registered” abroad, the frugal buyer’s instinct is to take the discount. But the CMTA argues that this 15% depreciation benefit – intended for genuine used cars – is being leveraged as a loophole for zero-mileage vehicles.

For the savvy buyer, this raises a fundamental question of transparency. If the entry price of a vehicle is built on a “procedural” technicality rather than actual wear and tear, where else is the transparency lacking? Does the lower price reflect a genuine saving passed to the consumer, or does it mask a lack of manufacturer-backed after-sales support?

When a buyer chooses an authorised agent, they are essentially purchasing an insurance policy against the unknown. With a five-year manufacturer warranty, the financial burden of a faulty transmission or a software glitch stays with the global giant that built the car, not the local owner. In an era where vehicles are increasingly “computers on wheels,” the technical specialised tools and genuine parts held by authorised agents are no longer a luxury – they are a necessity for longevity.

The CMTA’s perspective also invites the buyer to look at the “Big Picture.” Every time a vehicle is imported under an under-declared value or an artificial depreciation bracket, it isn’t just a loss for the Treasury; it is a blow to the country’s foreign exchange discipline.

“A savvy buyer today is more informed than ever. They realize that a “cheap” import with no service history and no tropicalised specifications may eventually become a “minus” on the balance sheet. Frequent repairs and lower resale value can quickly evaporate the initial few lakhs saved at the point of purchase. Ultimately, the choice between brand new and used is a choice between certainty and speculation,” the Association says.

The CMTA is advocating for a level playing field where duty is based on true transaction value. Until that day comes, the burden of due diligence rests on the consumer. To be a “savvy buyer” in 2026 means looking past the showroom shine and asking: Who stands behind this car if something goes wrong tomorrow?

In conclusion, CMTA says,” For those seeking long-term peace of mind, the “brand new” path – supported by a transparent duty structure and a solid warranty – remains the gold standard for steering Sri Lanka’s complex automotive landscape.”

Before signing the papers on a reconditioned vehicle, the CMTA suggests buyers evaluate the four “minus” factors against a “brand new” purchase:

By Sanath Nanayakkare

Prime Minister on official visit to Manila, Philippines

It is the government’s responsibility to ensure women’s rights are realized in everyday Life, and are not confined merely to Laws – PM

North Korea cancels Pyongyang Marathon for ‘some reasons’

Canadian officials rescue 23 people who floated away on ice sheet

India offered sanctuary to Iranian ship three days before US sank it

Afghanistan-Sri Lanka white-ball series set to be postponed due to West Asia conflict

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News4 days ago

News4 days agoUniversity of Wolverhampton confirms Ranil was officially invited

-

News5 days ago

News5 days agoLegal experts decry move to demolish STC dining hall

-

News4 days ago

News4 days agoFemale lawyer given 12 years RI for preparing forged deeds for Borella land

-

News3 days ago

News3 days agoPeradeniya Uni issues alert over leopards in its premises

-

Business5 days ago

Business5 days agoCabinet nod for the removal of Cess tax imposed on imported good

-

News4 days ago

News4 days agoLibrary crisis hits Pera university

-

News3 days ago

News3 days agoWife raises alarm over Sallay’s detention under PTA

-

Business6 days ago

Business6 days agoWar in Middle East sends shockwaves through Sri Lanka’s export sector