Business

Is wealth tax the solution to Sri Lanka’s low tax revenue collection?

By Sathya Karunarathne

Successive governments have run fiscal deficits. Inadequate revenue collection and unrestrained government expenditure have worsened the country’s fiscal position.

Tax revenue which averaged over 20% of GDP in 1990 has declined to under 10% of GDP in 2020. Ad hoc tax policy changes have significantly eroded the tax base. Weak tax administration has also contributed to the sharp decline in tax collection.

While tax revenue has contracted, government expenditure has ballooned over time. Today, government revenue is not sufficient even to meet its expenditure on salaries and wages and transfers and subsidies to households which include pension payments and social welfare payments such as Samurdhi.

In this context, there are various proposals put forward to raise government revenue. One proposal is the reintroduction of the wealth tax.

A wealth tax is expected to bridge the gap between the rich and the poor, achieving equality. This tax shifts the tax burden to affluent households, taxing an individual’s net wealth, which is the market value of total owned assets. Proponents of wealth taxation argue that this is a progressive system of taxation and is a more powerful tool in comparison to income, estate or corporate taxes as it addresses the issue of wealth concentration.

Moreover, a tax should ideally satisfy basic characteristics of taxation: it should not be distortionary; it should be fair, and it should not be difficult to collect.

The rationale for a wealth tax

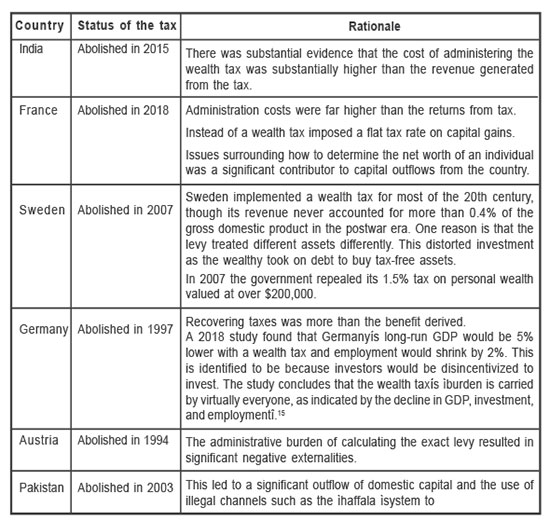

One of the earliest proponents of the wealth tax for developing countries was Nicholas Kaldor. Based on his recommendation, a wealth tax together with an income tax, expenditure tax and a gift tax were introduced in Sri Lanka in 1958.1 However, these new taxes yielded little revenue due to difficulties in determining the tax base and problems in administration. Following the recommendation of the Tax Commission in 1990,2 the government abolished the wealth tax from the year of assessment 1992/1993.3

Wealth taxes have mainly been implemented in European countries. In 1990, twelve countries in Europe had a wealth tax. Today, there are only three: Norway, Spain, and Switzerland. Several non-European countries have also imposed wealth taxes from time to time including such as Argentina, Bangladesh, Colombia, India, Indonesia, Pakistan

In recent times there has been renewed interest in wealth taxes. Presidential candidates in the US proposed various forms of a wealth tax. In the UK and France, there were proposals to impose “super taxes” on the rich. The primary justification was to address the increasing inequality in society.

Issues with a wealth tax

Despite renewed interest in the wealth tax as a progressive tax based on equity, it scores poorly on the criteria of efficiency, and administrative feasibility.4

Many factors have justified the repeal of wealth taxes in OECD countries. The reasons cited are related to efficiency costs, risk of capital flight particularly in light of increased capital mobility and wealthy taxpayers’ access to tax havens, failure to meet redistributive goals as a result of narrow tax bases, tax avoidance and evasion, high administrative and compliance costs compared to limited revenues (high cost yield ratio).5

To understand the efficiency costs of wealth taxes one can look at taxing a person’s wealth accumulated through savings. Despite the common consensus that taxing savings is an effective way to redistribute, a person’s saving decisions reveal little about their underlying lifetime resources and wellbeing. It only reveals their preference to consume tomorrow rather than today. Thereby a wealth tax imposes a tax on those who prefer to spend their money later as opposed to taxing the wealthy.6 Efficiency costs refer to the reduction of the welfare of the taxed individuals by more than $1 to generate $1 of revenue.7 Therefore, the efficiency cost of a wealth tax in terms of taxing savings is a reduction of future consumption that can be bought with earnings, reducing incentive to work for those who prefer to consume the proceeds later and reducing incentive for young people to save for their retirement.8

Capital flight is the possibility of holding assets outside of one’s resident country without declaring them.As wealth taxes are imposed on residents it increases the risk of the wealthy reallocating their assets to avoid taxation. Therefore a high tax burden encourages taxpayers to change their tax residence to a lower tax jurisdiction or tax havens.9

Both income-generating and non-income generating assets are taxed under wealth taxation. They can include land, real estate, bank accounts, investment funds, intellectual or industrial property rights, bonds, shares, and even jewellery, vehicles, art and antiques.10 However, this tax base for wealth taxes has often been narrowed through exemptions. These exemptions have been justified most commonly on the grounds of social concerns such as the negative social implications of taxing pension assets. Further liquidity issues (eg – farm assets), supporting entrepreneurship and investment (eg- business assets), avoiding valuation difficulties ( eg- artwork and jewellery) and preserving countries cultural heritage (eg – artwork and antiques) have also been cited as reasons for wealth tax reliefs. While some of these exemptions can be justified, they have led to the reduction of revenue raised from wealth taxes. They have also contributed to wealth taxes being less equitable as the wealthiest such as businesses benefit from these exemptions defeating the very purpose of imposing a wealth tax which is to meet its redistributive goals.11

Narrow tax bases in wealth taxation often leads to tax avoidance and evasion opportunities. For example, Spain’s 1994 wealth tax exemption for the shares of owner managers resulted in wealthy businesses reorganizing their activities to reap benefits of the exemption resulting in a significant erosion of the wealth tax base.12

Further, several other factors have also discouraged countries to sustain a wealth tax. They are namely, the difficulty in determining the tax base or what assets to be taxed, underreporting and undervaluation of assets, difficulty in measuring wealth taxes13, distinguishing between individuals who are asset rich but cash poor, the constant need to value assets and audit returns increasing administrative and enforcement costs .

Low revenue collection as well as the other reasons discussed have led to the abolishing of wealth taxes in most countries (See Table 1 for details) . Tax revenue from individual net wealth taxes in 2016 ranged from only 0.2% of GDP in Spain to 1.0% of GDP in Switzerland. Sri Lanka’s experience with wealth taxation was no different with the tax yielding low revenue as reported by the 1990 Tax Commission.14

Conclusion

Taxing the wealth of the rich to generate income and to eliminate economic inequality sounds promising in terms of political debate. However, wealth taxes have failed to generate adequate revenue, failed to meet redistributive goals as a result of narrow tax bases, proven to have high administrative and enforcement costs, resulted in tax evasion and avoidance due to underreporting and undervaluation of assets, increased the risk of capital flight and access to tax havens and may have contributed to the reduction of investment and employment.

Therefore, imposing a wealth tax may not be the ideal policy response to Sri Lanka’s low tax revenue, especially given the country’s previous experience with the tax yielding low revenue.

Sathya Karunarathne is the Research Analyst at the Advocata Institute and can be contacted at sathya@advocata.org. Learn more about Advocata’s work at www.advocata.org. The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

Business

Cabinet nod to accept increased Loan Grant provided by the Asian Development Bank under Policy Based Loan Facilities – 2026

Approval of the Cabinet of Ministers was granted at their meeting held on 16.03.2026 to obtain United States Dollars 380 million from the policy – based loan facilities of the Asian Development Bank in the year 2026.

United States Dollars 100 million out of it is allocated for Trade, Investment and Industries Development Programme – Sub Programme 1. However, amidst the economic uncertainty resulting from the current Middle East crisis and the climatic tragedies, the Asian Development Bank has agreed to assist

by increasing a supplementary financing package of United States Dollars 100 million so that it will beMincreased up to United States Dollars 200 million.

Accordingly, the Cabinet of Ministers approved the resolution furnished by the President in his capacity as the Minister of Finance, Planning and Economic Development to take further measures to obtain the said loan grant.

Sri Lanka is not quite ready to join the Regional Comprehensive Economic Partnership (RCEP), since it is lacking sufficient development, Trade Ministry Secretary K.A. Vimalenthirarajah said.

‘At present the Trade Ministry is establishing Sri Lanka’s readiness to join RCEP, which consists of 15 countries, through several channels, Vimalenthirarajah said at a recent round table discussion titled, ‘Sri Lanka’s Pathway to RCEP and the Emerging Global Trading Order’, organized by the Pathfinder Foundation and held at the Colombo Club, Taj Samudra.

‘Sri Lanka is actively accelerating its compliance efforts to join the 15-nation RCEP having submitted its required accession questionnaire in early 2026, he explained.

Vimalenthirarajah added: ‘The Cabinet has established a high-level policy and working committee and also obtained some technical assistance from multilateral partners because complying with RCEP requirements is challenging. Subsequently, this body responded to the follow-up questions that came up and had discussions with RCEP representatives and it expects more follow-up questions with regard to Sri Lanka’s readiness to join RCEP.

‘Sri Lanka has also secured political and diplomatic support from current RCEP members, including Australia, New Zealand, and Indonesia, to facilitate its entry process.’

Meanwhile, state officials, including Industries and Entrepreneurship Development Deputy Minister Chathuranga Abeysinghe, are implementing key economic structural reforms, a new tariff policy, and transparent investment criteria required by the bloc. Because formal accession protocols for RCEP are still being finalized, Sri Lanka is also simultaneously negotiating bilateral trade and investment agreements with regional members to accelerate integration.

Abeysinghe, participating virtually in the event said that Sri Lanka cannot achieve sustained export growth and attract large-scale investment by relying solely on its domestic market. ‘As a small economy, the country’s future lies in deeper integration with regional and global value chains. RCEP connects 15 economies, including Japan, South Korea, Australia, New Zealand, China and ASEAN member states, collectively accounting for nearly 30% of global trade, he explained.

Abeysinghe added: ‘Access to such a market would create new opportunities for Sri Lankan businesses, particularly the country’s Small and Medium Enterprises (SMEs), which currently contribute only around 10 percent to national exports.

‘However, Sri Lanka is at least a decade behind in implementing many of the reforms required to fully participate in modern global trade. Recognizing this challenge, the government is now moving forward with several critical reforms: A new tariff policy to improve competitiveness and eliminate barriers to trade, transparent and predictable investment criteria, investment facilitation reforms to improve the ease of doing business, new legislation including the Public-Private Partnership (PPP) Act and SOE reforms to strengthen investor confidence and measures to improve investment protection and unlock new sources of capital, including venture capital and angel investment funds.

‘Sri Lanka’s exports currently stand at approximately US$ 17 billion and have grown only gradually over the years. Expanding market access through bilateral and multilateral agreements, while continuing domestic reforms, is essential if the country is to achieve its long-term economic ambitions.’

By Hiran H Senewiratne

In a landmark development for Sri Lanka’s organic spice sector, Pussalla Agri Ventures has been awarded both EU Organic and USDA Organic certifications for its premium Ceylon cinnamon products. The certifications were officially conferred at Control Union Sri Lanka, signaling a major milestone in the company’s strategic transformation toward fully certified organic operations.

The recognition strengthens Pussalla Agri Ventures’ position as an emerging exporter of certified organic products, with its flagship offering, organic Ceylon cinnamon (Cinnamomum verum, also known as Cinnamomum zeylanicum), cultivated in Sri Lanka’s traditional cinnamon-growing regions.

Notably, the dual certification opens doors to some of the world’s most lucrative and compliance-driven organic markets, including the European Union and the United States.

Pussalla Agri Ventures began its structured transition into organic cinnamon cultivation several years ago, building a fully integrated system covering cultivation, processing, and value addition. The company currently manages extensive cinnamon cultivation lands and operates under strict organic agricultural principles, ensuring compliance with global certification standards.

These certifications, issued through Control Union Sri Lanka, validate that the company’s farming and processing systems meet rigorous international requirements, including restrictions on synthetic chemicals, comprehensive traceability controls, and environmental sustainability practices. These certifications add to an existing portfolio that already includes SL GAP, Food GMP, and Cosmetic GMP certifications.

Company representatives described the achievement as a “milestone” in the Pussalla organic journey, one that paves the way for expanded access to premium export markets in Europe and the United States. According to them, the certifications are expected to enhance buyer confidence, particularly among health-conscious consumers and clean-label food brands.

Pussalla Agri Ventures emphasised that its organic cinnamon is sourced entirely from its own cultivated estates.

“This estate-to-exporter integration ensures full control over quality, traceability, and processing integrity. The company’s model allows cinnamon to be harvested, processed, and packed under continuously monitored conditions, maintaining strict alignment with international organic standards,” they noted.

Speaking further they said:

“Sri Lanka supplies the majority of the world’s True Ceylon Cinnamon, a spice prized for its delicate aroma, low coumarin levels, and reputed medicinal properties. The growing global demand for certified organic spices has created new opportunities for local producers who meet international compliance standards. Pussalla Agri Ventures’ certification achievement places it among a select group of Sri Lankan exporters adopting globally recognised organic systems, thereby enhancing the country’s reputation in high-value spice markets.”

“As organic food sales continue to rise in North America and Europe, certifications such as these are becoming essential rather than optional. For Pussalla Agri Ventures, the journey from conventional to certified organic is not merely a compliance exercise but a strategic repositioning aimed at long-term sustainability and premium pricing power.”

By Sanath Nanayakkare

Report on the Final Budgetary Condition (Annual Report) – 2025 submited to parliament

Cabinet nod to accept increased Loan Grant provided by the Asian Development Bank under Policy Based Loan Facilities – 2026

Submission of Revenue Protection Order Prepared under the Provisions of the Revenue Protection Act No. 19 of 1962 to the Parliament for its approval.

Resettlement of unauthorized settlers affected by the Land Acquisition process for the implementation of Phase III of the Baseline Road Extension Project

Cabinet approves project to modernize school hostel facilities during the 2026–2028 period at an estimated cost of Rs. 1,008 million

New National Action Plan for Human-Elephant Conflict Management to be drafted

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoCIABOC summons Yoshitha over his participation in British Navy training programme

-

News7 days ago

News7 days agoLocal firms move millions of dollars overseas for phantom imports: Govt.

-

Midweek Review7 days ago

Midweek Review7 days agoJuly 09: An inexcusable overall security failure and exceptional contingency plan

-

Sports2 days ago

Sports2 days agoTharanga set for high-profile javelin clash in Ostrava

-

News4 days ago

News4 days agoCommonwealth lawyers urge Lanka to uphold rule of law

-

News5 days ago

News5 days agoJustice Minister responds to social media claims he represented Easter Sunday ringleader

-

Features3 days ago

Features3 days agoPolitics of protected species

-

News7 days ago

News7 days agoAI raises concerns over arrest of Sallay and rapper under PTA