Features

Is the Auditor General the panacea for all our ills?

by Avantha Munasinghe

One of the contentious issues surrounding the 20th Amendment seems to be the issue of the removal of Auditor General’s capacity to audit companies where the Government, Public Corporation or a Local Authority has a majority shareholding. Many critics seem to have picked on this issue, and most of them are resisting the proposed change. Their fear seems to be that if the Auditor General is not permitted to audit a certain government company, it is prone to be riddled with corruption and malpractices.

The audit by definition is a systematic and an independent review and investigation on certain subject matter, which in this case is the financial statements, management accounts, management reports, accounting records etc. of a company. In the case of a company, there is a statutory requirement for such review and investigation to be reported to shareholders annually. The review, is produced as an “opinion” of the “Auditor”.

Other than the shareholders, it is also customarily used by the tax authorities, banks, creditors, analysts or public for their respective decision-making and also to form their own opinion about the status of the company and its future. In all the government companies, the law required them to be audited by independent auditors, qualified to do so as specified by the Companies Act, until 2015. The 19th Amendment changed their auditor to be the Auditor General.

Auditing, just like Accounting, depends on certain commonly adopted set of principles. The audit of financial statements is normally done in accordance with International Standards on Auditing sometimes modified by local auditing standards. In Sri Lanka’s case, the Sri Lanka Auditing Standards are based on the International Standards on Auditing (ISAs) published by the International Auditing and Assurance Standards Board (IAASB) of the International Federation of Accountants (IFAC), with slight modifications to meet local conditions and needs. Thus, to begin with, whether it is the Auditor General or a private auditor, the standards applicable to the task are the same. It is the approach that is different.

There are a large number of companies in Sri Lanka whose shareholding in some way is linked to Government or quasi government entities for whom Auditor General has now become the Statutory Auditor. Some of these companies are merely an extension of government entities serving a function of the government. For example, Rakna Arakshaka Lanka Limited is a government-owned company, providing security services to government installations. Another is Ceylon Petroleum Storage Terminal Ltd., whose only customers are its parent entities i.e. Ceylon Petroleum Corporation and Lanka IOC PLC, only to whom it provides services. Such entities do not have to face competition to secure business.

However, there are also a large number of government-owned companies which do business in the marketplace competing with other local and international companies, which are publicly and privately owned. Lanka General Trading Company Ltd., Lanka Hospitals Ltd., Sri Lanka Insurance Corporation Limited and Milco (Pvt.) Ltd., are a few examples. Each of them has to compete for business with large segment of local and foreign companies which are purely driven by profit motive and enhancement of shareholders’ value.

These companies have very flexible systems and procedures. Their boards of directors can take appropriate decisions in a timely manner to make an urgent procurement or select suppliers to be more competitive and manage all their affairs just in time. They can buy their raw materials without calling for quotations if they think it is a profitable opportunity. Even a junior level executive of such a company may be able to decide a price discount to secure a sale.

The situation of a state-owned company in the marketplace in such scenarios is quite the opposite. They cannot do procurement as the situation demands. They have to dutifully follow the procurement rules, which even the board of directors cannot overrule. The officials have very little flexibility to seize a business opportunity. It is so easy for a private company to grab business from state-owned enterprises as the latter cannot be proactive. There is little surprise most such companies are loss-making and is a burden to the government and taxpayers.

The government officials and Ministers however want these quasi state organizations to be profitable or run at least without being a burden to the Treasury. The basic business model of these organizations is at a severe disadvantage to begin with. What 19th Amendment brought to such companies by way of auditing by the Auditor General was to push them from pillar to post. This is quite evident by the powers granted to the Auditor General in the National Audit Act, which even a crime investigator would envy. Some of the powers are:

(1) The Auditor-General shall…

… access or call for any written or electronic records or other information relating to the activities of an auditee entity;

… call any person whom the Auditor-General has reasonable grounds to believe to be in possession of information and documents, as he may consider necessary to carry on the functions under this Act, to obtain written or oral statements and require the production of any document, from any person, who may be either in-service or otherwise;

… examine and make copies of or take extracts from any written or electronic records and search for information whether or not in the custody of the auditee entity;

… after obtaining permission from the relevant Magistrate’s Court, examine and audit any account, transaction or activity of a financial institution, of any person, where the Auditor-General has reason to believe that money belonging to an auditee entity has been fraudulently, irregularly or wrongfully paid into such person’s account;

…require any officer of financial institutions to produce any document or provide any information relating to an account, transaction, dealing or activity of person referred to in paragraph (d) and to take copies of any document so produced, if necessary… There is a fundamental difference in the audit approach of a professional auditor and a Supreme Audit Institution such the Auditor General. In a private sector audit, the primary objective is to ensure the report’s recipient gets a true and fair view of the financial status of the company. While the professional auditor is supposed to report on adequacy of the controls in place and report any lapses to shareholders, the focus is primarily on the status of the shareholder’s investment.

The approach of Auditor General is more on ensuring the Compliance to rules, regulations and procedures. This is natural since the Auditor General is supposed to audit the manner in which a government organization has handled its allocation from the consolidated fund to provide a service to the public. The approach is, therefore, not focused on whether the organization is making adequate return on the government’s funds.

What the 19th Amendment did was to replace the professional auditor, who focused on performance of government companies by the Auditor General who is focused on compliance. The officers running such government-owned companies got a signal quite contrary to what the government officials and ministers were pushing them before. Compliance became the key. There is no better way to achieve compliance than to do nothing. The truth is in the last few years; these organization put profit motive in the back burner and wanted to escape from various audit queries raised by the Auditor General. The best way to do that is not to go that extra mile their competitors would go to make the organization profitable. Doing nothing became the modus operandi.

Some of the supporters of Auditor General’s auditing argue that his mere presence stops corruption. Stamping out corruption was the all-pervasive theme of the 19th Amendment. So many new entities were instituted under it to check corruption. Where are we today? Do we see any positive results? In the Corruption Perception Index published by the Transparency International in the year 2015, when the 19th Amendment was enacted, Sri Lanka’s scored 37 out of hundred. In 2019, our score was only 38. We rank 93 out of 198 countries, four places down. It is no secret that the public perceives state sector organizations as corrupt as ever and certainly more corrupt than any private sector organization in this country. The Auditor General has been auditing these state sector organizations for more than 200 years. If the cure against corruption is audit being done by the Auditor General, why are we in this situation today?

The truth is the Auditor General’s presence is a necessary evil in any government ministry or department, which does not have a commercial objective. His presence does ensure at least some level of corruption is made more difficult to accomplish. However, we must not come into the false conclusion that the presence of the Auditor General is the way to root out corruption. In a State-Owned Enterprise (SoE) with commercial objectives, his presence certainly does more harm than benefit.

There is a wrong perception that most public companies are loss making and, therefore, they should be subjected to an Audit by the Auditor General so that the “control” of public funds will put things right. As explained above, it is the business model and restrictions placed that is the very cause for loss-making SoEs to proliferate. If this argument is correct, we should see, out of more than 120 or so government companies, at last one which became profitable due to the Auditor General’s presence during last five years. There is none to show. In fact, this remedy will only make the patient even more sick.

Another untruth floated on the matter is that the financial statements of the government companies are not required to be submitted to Parliament unless they are audited by the Auditor General and that would undermine parliamentary financial oversight. The truth is that the entity, which is the shareholder in these companies, have to consolidate the company’s financial statements with that of the parent entity and the latter is certainly subjected to parliamentary oversight with financial statements of the company audited by a private auditor.

Another misconception is that supervision by COPE will put everything right in the public institutions. COPE’s examination carried out by set of parliamentarians, who on most occasions have no knowledge of the particular business, is not what is required to put these organizations right. In most cases it is the bad business model rather than lack of COPE’s oversight that fail these businesses.

SriLankan Airlines is a case of point. Many people say the bad procurement deals, continued losses and increased dependence on the Treasury by the airline would continue to happen if the Auditor General is not auditing the airline. It was making losses ever since it was set up with or without Auditor General as the auditor. The Airline business is one of the most competitive businesses globally. Even the largest airlines sometimes find it difficult to be in the black. The industry needs split second decisions to be made by professional management. As said before, this is not possible at SriLankan Airlines. We have seen Chairmen and Directors coming and going with every change of the subject minister. Nobody is having a long-term commitment to make it a success. Its competitors have boards, which are removed only if the airline makes losses, not if their political masters change. Without changing the business model, even if we have hundred auditors to audit SriLankan Airlines, nothing will change.

We all know that our country is suffering from a severe debt crisis. We invested on massive infrastructure projects, which were all debt financed. To balance that off, we desperately need to bring foreign equity into our economy. Further debt, while giving us temporary solace, will only aggravate the problem. The government is devising Public Private Partnership (PPP) programs to bring Foreign Investment from large global corporations. The government also needs to be in control of them. The 19th Amendment requires such PPP companies to have the Auditor General as its Auditor. Which global business entity would drop their global audit arrangements by the likes of KPMG, Ernst & Young or PwC and accept this arrangement? We can talk till the cows come home on how professional our Auditor General is and how independent he is, but the reality is that we live in a dream if we seriously want to promote PPP structures with this kind of legislation on.

The effective functioning of Superior Audit Institutions such as the Auditor General is definitely an essential requirement of a functioning democracy. However, let’s not fool ourselves – it is not a panacea for all ills.

Even in India where the previous Companies Act required the appointment of Auditors to Government Companies by the Controller and Auditor General of India, the arrangement has been questioned in the Report of the Expert Committee On Company Law, which said “The Committee discussed the application of the corporate law framework to Government companies on many occasions and took the view that in general, there should not be any special dispensation for such companies. …Therefore, the extension of special exemptions and protections to various commercial ventures taken up by Government companies in the course of their commercial operations along with strategic partners or general public should be done away with so that such entities can operate in the market place on the same terms and conditions as other entities. In particular, reflection of financial information of such ventures by Government companies and their audit should be subject to the common legal regime applicable. The existing delays are enabling a large number of corporate entities to evade their responsibilities and liability for correct disclosure of true and fair financial information in a timely manner. In this context, the relevance of the present section 619B of the Act was considered appropriate for a review.”

If the government needs its companies to compete with private sector, the way forward is to make their management more flexible. Throwing those decision-makers to the Auditor General is the last thing required to be done if we want them to compete effectively with the private sector. While the world is moving to embrace the scarce private capital by making things easier for such investors, some of our so-called professionals seem to be, while paying lip service for bringing more and more FDI, doing exactly the opposite by criticizing the removal of this disastrous piece of legislature brought in by the 19th Amendment.

(The writer is an Accountant based in New South Wales, Australia)

AUSTRALIA

For the first time since 2017, Australia do not have global silverware to defend, with last year’s ODI World Cup semi-final exit following the relinquishing of the T20 title in 2024 after a hat-trick of trophies. They have a new captain, too, in Sophie Molineux who has taken over from the retired Alyssa Healy butAl has had a tricky start to her job due to a back injury.

Having been beaten at home by India in February, it’s a vital few weeks for the side to reaffirm their standing at the top of the tree. However, they find themselves in the group of death with one of them, India and South Africa unable to make the semi-finals.

While Healy has retired, the core of the squad remains very familiar although the call-up of left-arm quick Lucy Hamilton hints at the new generation. There is no shortage of spin options, so much so that Alana King may struggle to find a place in the XI despite recently being the Player of the Series in West Indies.

Squad: Phoebe Litchfield, Beth Mooney, Georgia Voll, Ellyse Perry, Ashleigh Gardner, Tahlia McGrath, Annabel Sutherland, Grace Harris, Nicola Carey, Sophie Molinuex (capt), Georgia Wareham, Alana King, Kim Garth, Megan Schutt, Lucy Hamilton

Player to watch

Even before Healy’s retirement, injuries had prevented her playing T20Is since the last World Cup so Georgia Voll has had a decent run to establish herself at the top of the order. She has taken it with both hands. In 12 matches Voll is averaging 39.50 with a strike-rate of 156.43 – while the sample size remains small, that’s the highest figure of anyone with at least 400 runs in T20Is.

She made her mark against New Zealand last year, then enjoyed an impressive start to 2026 with 88 against India in Canberra before a breakout century in West Indies, her batting characterised by power down the ground. It feels as though she is already at the stage where she can star in a global event.

Predicted finish: Finalists

BANGLADESH

Player to watch

Pace bowler Marufa Akter could relish the conditions in England, particularly given her ability to swing the ball at decent speeds. An on-song Marufa is a delightful sight for those who love to see the ball seam and shape towards the batters. She has taken eleven wickets in as many matches this year, while maintaining a good economy rate.

But she has little support in terms of pace from the other end. Bangladesh have left-arm seamer Fariha Islam and Ritu Moni’s slow-medium pace. As a result, Marufa has to do most of the attacking in the powerplay, and then return to bowl pinpoint yorkers and slower balls at the death.

Predicted finish: Group stage

INDIA

India enter the T20 World Cup with the tag of ODI champions. However, their form heading into this tournament has been a little iffy. In the last six months, they won at home against Sri Lanka and away against Australia but lost both the away series against South Africa (4-1) and England (2-1).

The three match series against England showed their inclination to have the returning Yastika Bhatia batting at No. 3, which meant Jemimah Rodrigues and Harmanpreet Kaur occupied Nos. 4 and 5. Bhatia was the leading run-getter in the series with 119 runs but her strike rate (126.79) was the lowest among the top-five scorers.

Injuries to Amanjot Kaur and Kashvee Gautam mean India’s combination leans towards a five-bowler strategy with Shafali Verma’s part-time offspin as the addition. India’s familiarity with English conditions – they also toured England in 2025 with wins in each of the white-ball series – means they head into the T20 World Cup with some confidence.

Squad: Harmanpreet Kaur (capt), Smriti Mandhana (vice-capt), Shafali Verma, Jemimah Rodrigues, Deepti Sharma, Richa Ghosh (wk), Arundhati Reddy, Renuka Singh, Kranti Gaud, Shree Charani, Shreyanka Patil, Bharti Fulmali, Yastika Bhatia (wk), Nandani Sharma, Radha Yadav

Player to watch

Smriti Mandhana is the lynchpin of this India team, and their fortunes will hinge on her. This is evidenced by the fact that she was India’s leading run-getter in last year’s ODI World Cup which they won. She also led Royal Challengers Bengaluru to their second WPL title earlier in the year, while topping the batting charts.

She is not just among the most experienced players in the Indian team but has the advantage of knowing conditions in the UK, thanks to her regular presence in the Kia Super League and the Hundred.

Predicted finish: Semi-finalists

NETHERLANDS

Netherlands will be at their first-ever women’s T20 World Cup (Cricinfo)

Everybody loves a newcomer, and this edition of the T20 World Cup welcomes Netherlands. They secured their spot at the qualifying tournament, where they finished in fourth place and beat the last tournament debutants, Scotland, along the way.

Though cricket is a minority sport in the country, it continues to punch above its weight and history provides plenty of reasons to regard the Dutch as plucky. In 2009, their men’s team made their first T20 World Cup appearance and beat England at Lord’s. In 2023, they were the only Associate nation to play at the men’s ODI World Cup. The women don’t have England in their group but take on heavyweights Australia, India – both for the first time – and South Africa, along with Bangladesh and Pakistan.

In personnel terms, Netherlands have four players with more than 1,000 runs in the format – Sterre Kalis, Babette de Leede, Robine Rijke and Silver Siegers – and they’re all in this squad. Iris Zwilling, their leading seamer, is two wickets away from 100. This will also be a swansong for coach Neil MacRae, who will hand over the reins to former Leicestershire, Namibia and Titans’ women’s coach Pierre de Bruyn on August 1.

Squad: Babette de Leede (capt), Caroline de Lange, Frederique Overdijk, Hannah Landheer, Heather Siegers, Iris Zwilling, Isabel van der Woning, Lara Leemhuis, Myrthe van den Raad, Phebe Molkenboer, Robine Rijke, Rosalie Lawrence (wk), Sanya Khurana, Silver Siegers, Sterre Kalis

Player to watch

Not only is Sterre Kallis their leading run-scorer in T20Is, but she has significant experience playing in England, across the domestic system and in the Hundred. Most recently, Kalis scored three fifties in the ECB Women’s One-Day Cup where she is the sixth leading run scorer.

Kalis has also played at the WBBL and will be able to provide her team-mates with inside information into a side they have never come across before. Along with Babette de Leede, who has experience playing in South Africa, Kalis will headline the batters as the Dutch look to show what they can do against some of the world’s best bowlers.

Predicted Finish One group stage upset and that’s where it will end.

PAKISTAN

As the women’s game develops at pace in many places around the world, there’s a sense Pakistan are struggling to keep up and this tournament could be a litmus test. Not only have their own board’s plans to develop a franchise T20 tournament akin to the men’s PSL stuttered then stopped entirely but, for reasons including geopolitics, their players have almost no exposure to major leagues. The consequences speak for themselves: Pakistan have won only one T20I series in the last two-and-a-half years and that was against women’s FTP newcomers Zimbabwe in May, and won one match in each of the last four editions of the T20 World Cup.

Though they are stacked with talent and have a well-resourced support staff, consistent results and major success are lacking. At an expanded tournament, their first aim will be to show they are a cut above the qualifiers and then to see if they can take some big names along the way. They’ll be hopeful of having their premier seamer, Diana Baig, for the entire tournament after she was injured during the 2024 event and will need their big hitters: Gull Feroza, Eyman Fatima and Natalia Pervaiz to come good to have a successful event.

Squad: Fatima Sana (capt), Aliya Riaz, Ayesha Zafar, Diana Baig, Eyman Fatima, Gull Feroza, Iram Javed, Muneeba Ali (wk), Nashra Sundhu, Natalia Pervaiz, Rameen Shamim, Sadia Iqbal, Saira Jabeen, Tasmia Rubab, Tuba Hassan

Key Player

Pakistan’s dynamic captain, Fatima Sana captured hearts when she had to leave the previous T20 World Cup after the sudden death of her father but then returned to lead thesa side in their final game. Though she earned much goodwill, she was unable to take Pakistan out of the group stage and was criticised for batting too low. Sana remains at No.6 but has had a remarkable 2026 so far, which has included scoring the fastest fifty in women’s T20Is, off 15 balls, and striking at over 200. Combine that with her new-ball bowling skills and the responsibility she carries as skipper, and it’s clear she is key to their chances.

Predicted Finish: Group Stage

SOUTH AFRICA

South Africa have done everything but win a World Cup recently – they have reached the last three finals across white-ball formats – so every cricketing conversation in the country is about when they will take the next step. Pressure? What pressure?

While they may face plenty of it from a home base hungry for its first senior white-ball World Cup, South Africa routinely find themselves spoken about behind the big three. That means they may feel less of the spotlight in England, where the home nation has hearts aflutter and other eyes are directed towards the big two in their group. Six-time champions Australia and current ODI World Cup title-holders India stand in South Africa’s path to the semis and the smart money could be on that pair but… South Africa beat India 4-1 in a pre-tournament series at home and knocked Australia out of the last tournament so they’ll back themselves to rise above the reputations they face.

They selected their strongest possible squad, which includes two former captains (Dane van Niekerk and Sune Luus), six seamers, five spinners, two wicketkeepers and a well-set top seven. On paper, they have all the ingredients. In practice, they need to cook.

Squad: Laura Wolvaardt (capt), Tazmin Brits, Nadine de Klerk, Annerie Dercksen, Shabnim Ismail, Sinalo Jafta (wk), Marizanne Kapp, Ayabonga Khaka, Suné Luus, Karabo Meso (wk), Nonkululeko Mlaba, Kayla Reyneke, Tumi Sekhukhune, Chloé Tryon, Dané van Niekerk

Player to watch

It’s hard to look past Laura Wolvaardt, who was the leading run-scorer at the last three ICC events, including two T20 World Cups, as being crucial to South Africa’s chances but they’ve also put their faith in reverse-retiree Shabnim Ismail. At 37, Ismail has not been an active international for over three years but is the leading seamer in league cricket and lost none of the aggression that made her so intimidating to face.

Predicted Finish: Ch… we’d never touch the money.

(Cricinfo)

The Preamble to Sri Lanka’s Constitution states: “The PEOPLE of SRI LANKA having by their Mandate … entrusted and empowered their Representatives … to draft, adopt and operate a new Republican Constitution in order to achieve the goals of a DEMOCRATIC SOCIALIST REPUBLIC, whilst ratifying the immutable republican principles of REPRESENTATIVE DEMOCRATIC”.

The intent of this exercise is to ascertain whether the practices as adopted by successive Governments to elect the People’s representatives are in keeping with the “immutable principles of Representative Democracy”.

According to Article 3 of the Constitution: “Sovereignty includes the powers of government, fundamental rights and the franchisee”. Furthermore, Article 3 is an entrenched article – Article 83. According to Chapter XIV, titled “The Franchise And Elections”, Article 88 states: “Every person shall, unless disqualified….be qualified to be an elector at the election of the President and of the Members of Parliament or to vote at a Referendum”. Therefore, it is the electors in the Electoral Districts, as determined by the Delimitation Commission (DC), that elect the President and Members of Parliament.

EXISTING INCONSISTENCIIES

= The first relates to Article 96 (1). This states: “The (DC) shall divide into not less than twenty and not more than twenty-four electoral districts…”. The reason for the upper limit for Electoral Districts is perhaps because Sri Lanka was originally divided into twenty-for Administrative Districts (now 25), and 96 (3) establishes a relationship between Electoral Districts and Administrative Districts when it states: “Where a Province is divided into a number of electoral districts the Delimitation Commission shall have regard to the existing administrative districts so as to ensure as far as practicable that each electoral district shall be an administrative district or a combination of two or more administrative districts or more electoral districts together constitute an administrative district”

Despite the fact that the Constitutional direction to the DC was that the Electoral District was to “have regard to the existing Administrative District”, the number of Electoral Districts established by the DC is twenty-two (22) while the number of Administrative Districts are now twenty-five (25). Although the provision to combine Administrative Districts into one Electoral District exists, the reason for the difference is reportedly because the DC decided to factor in issues, such as land which is extraneous to franchise thus compromising the sanctity of franchise and the sovereignty of the electors. On the other hand, if the Electoral District is coterminous with the Administrative District, not only would it protect the elector’s Franchise but also enable the elected members to address the administrative interests of the electors. Would such an opportunity not give substance to the “immutable republican principle of Representative Democracy”?

= The second inconsistency relates to Article 96 (4). This states: “The electoral districts of each Province shall together be entitled to return four members, (independently of the numbers which they are entitled to return by reference to the number of electors whose names appear in the registers of electors of such electoral districts), and the Delimitation Commission shall apportion such entitlement equitably among such electoral districts”.

Consequently, the four members to be returned from each of the nine Provinces amounts to thirty-six additional members, shall be apportioned equitably by the DC among the twenty-two (22) Electoral Districts together with the one hundred and sixty members from the electoral registers, thus making a total of one hundred and ninety-six members being elected through the franchise of the electors. The balance twenty-nine through the National List nominated by Political Parties is also elected by the electors, thus making a total of two hundred and twenty-five (225) Members of Parliament elected through Electoral Districts.

The irony however, is that although Members of Parliament are elected through Electoral Districts, all Executive Powers of the Line Ministries of the Central Government are implemented by the District Secretaries in the twenty-five Administrative Districts. The present convoluted process of appointing a Parliament through Electoral Districts and administering its functions through Administrative Districts cannot be justified. What would be more meaningful is to make Administrative Districts also perform Electoral functions such as appointing the Members of Parliament.

= The third inconsistency relates to the election of Members for Provincial Councils. According to the Provincials Councils Act: “Every administrative district in a Province shall for the purposes of elections to the Provincial Council established for that province, constitute an electoral area”

This is a departure from the practice adopted to elect Members to Parliament since they are based on outcomes from twenty-two (22) Electoral Districts. Therefore, it is worth exploring why Members to Parliament and Provincial Councils cannot be elected using the existing 25 Administrative Districts.

RECOMMENDATIONS

The intention is for an arrangement where Administrative Districts are also assigned electoral functions, so that both Members to Parliament and Provincial Councils could be elected by a single unit. The advantage would be that Administrative Districts could carry out Central Government functions under a District Secretary as at present, a parallel unit within the Administrative District could be set up to implement devolved powers in each of the Administrative Districts, while retaining the existing structural arrangements of Provincial Councils. This would facilitate the coordination of devolved powers with Central Government activities, thus improving productivity of each.

CONCLUSION

The current practice is that while representative of the Government of Sri Lanka is elected by Electoral Districts as stated above, Provincial Councils in the periphery with less powers than the Government are elected by electors in Administrative Districts of each Province. If elections to Parliament and to Provincial Councils are elected by electors in each of the twenty-five Administrative Districts, perhaps one election could elect Members to both bodies.

In view of the significant cost savings involved, it is imperative that serious consideration is given to equip Administrative Districts to serve as Electoral Districts for Parliamentary Elections as well as for Provincial Council Elections, since such an arrangement would further fortify the “immutable republican principle of Representative Democracy”. Furthermore, since such an arrangement would be closer to the People, services to them would be better served.

By Neville Ladduwahetty

The much-dreaded power cuts are already here though not declared as such. The tragedy is that the power cuts are not due to inadequate electricity supply, but the inability of the power and energy authorities to use the abundant solar and wind power installed without any financial or economic burden on the state. They ought to admit their lack of wisdom to be mindful of the rapid changes in the sector and the need to be equipped.

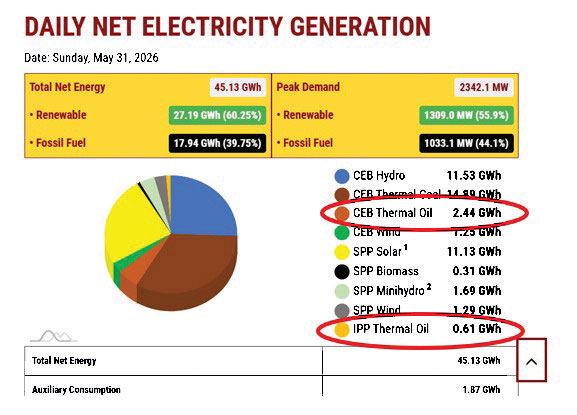

Fuel Prices have been increased again up to the 2022 levels. Therefore another Electricity tariff hike is inevitable. Perhaps, the government may hold it back until September, when the next tariff revision is due. An appeal has been made to “prosumers” to switch off their solar PV system in the fear of grid stability being affected. While there is excess solar power, which they are unable to manage, even when the demand is below the installed capacity and high contribution of hydro, solar and wind. May 31 (Sunday) energy mix indicated substantial use of oil in CEB-owned power plants and those belonging to the Independent Power Producers (IPPs) . What is the rationale? One would believe that even the hydro reservoir water can be saved for use during the night, without curtailing solar and wind power. It will be said that the system is very complex and beyond the understanding of mere mortals like ordinary “prosumers”, who have added over 2300 MW to the grid, entirely at their expense and at rates well below the average cost of generation. (See Image 1)

Storage Batteries and Renewable Transition

The fact that the growing need for storage batteries to optimise the utilisation of variable renewable energy (VRE) has been felt for the last decade or more, and nothing was done about it, is never mentioned in their laments.

However, there is a glimmer of hope due to the initiatives taken by the Public Utilities Commission of Sri Lanka (PUCSL). An increase in the demand due to a general GDP growth will have to be met using renewable resources. It has been clearly noted that such alternatives must be developed while curtailing the use of oil and ensuring the uninterrupted power to the consumers.

Recognising this need and the fact that fastest intervention is possible by promoting BESS (Battery Energy Storage Systems) to be added to all existing renewable energy sources, the PUCSL has initiated stakeholder consultation to determine the feed-in tariff payable for each type of BESS. A detailed methodology for determining the FIT has been circulated. The identified types of BESS discussed were as follows”

1. Power Plants

a. Mini -Hydro

b. Mini – Hydro-Local: mini hydro plants that at least use locally manufactured turbines

c. Wind

d. Wind – Local: Wind plants that at least use locally manufactured turbine blades

e. Biomass – Dendro – Biomass plants that use sustainably grown fuel wood

f. Biomass – Agricultural/Industrial Waste; Biomass fired plants use byproducts, like paddy husk, sawdust, sugar cane bagasse, etc.

g. Municipal Solid Waste

h. Waste Heat Recovery

i. Ground Mounted Solar PV

j. Floating Solar PV

2. Prosumers

a. Roof Top Solar PV

b. Rooftop Solar PV with Battery Energy Storage System (BESS)

c. Prosumers with behind the meter Battery Energy Storage System (BESS)

3. Power Plants with BESS

We mentioned in an earlier article that the PUCSL proposed a scheme whereby we can get rid of use of oil for power generation in stages, commencing with elimination of the diesel use by 2027 and all imported oils by 2030.

Stakeholder Meeting & Feed In Tariff( FIT)

The PUCSL has been empowered by the new Electricity Act No 36 (as amended), which came into full force on 09 March, 2026, with responsibility for calculating and announcing all FIT schemes, both for purchase and sale of electricity to consumers.

A well-represented stakeholder meeting was held recently, when the proposed methodology for determining the FIT of each type of BESS was given to them to provide further specific inputs. It is, therefore, realistic to expect such a FIT to be declared by the end of June, 2026.

While this is a welcome and progressive step unlike the ad hoc process adopted hitherto. But the fact remains that the responsibility for the effective use of FIT to attract investors to add the BESS at different scales, lies with the one or more of the newly appointed companies to take over the functions of the former Ceylon Electricity Board (CEB).

Government Recognition of Fossil Fuel Risks

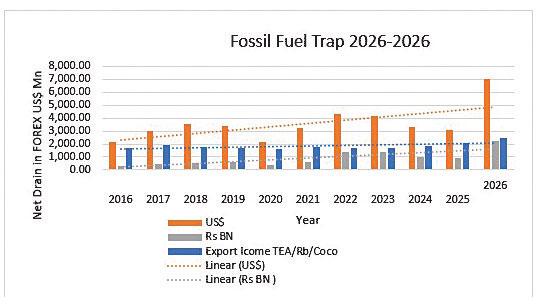

The current government has reportedly recognised the danger of overdependence on imported fossil fuels, which we have absolutely no control over. This is something we have been stressing for a long time. However, better late than never. As a matter of interest, we show the degree of fossil fuel dependence and its adverse impact on the economy. (See Graph 1)

It is to be noted that earnings from our traditional exports of tea, rubber and coconuts fail to meet the ever-increasing cost of importing fossil fuels. Time was when earnings from these exports barely helped meet the cost of import of fuels which was back in 2010. The rupee cost of imports is shown in Billions to keep the data columns within the bounds of the chart. This is the factor which affects you and me directly.

However, we earnestly urge the government to direct the electricity companies to take immediate action to prepare the grid which costs only a fraction of the values predicted by the CEB to institute their schemes which are not in line with the ground reality to accept the BESS system once the FIT is announced. Reasonable BESS and FIT will help attract investors with the assurance of short-term and long-term improvement, at no cost to the state.

Solar PV & BESS Proposal

We proposed some time back of the opportunity for those “prosumers” using 300 units per month, for installing solar PV with adequately sized batteries, which is more economical than drawing power from the grid, and to gain the happy situation, to be insulated from the danger of power cuts and further increases in consumer tariff.

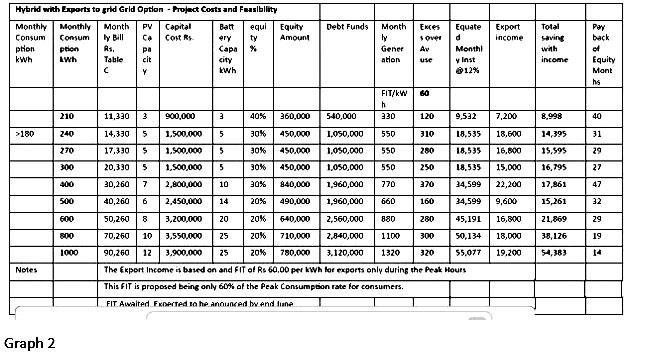

The PUCSL intervention to declare a BESS tariff will add a great impetus to those who are willing to adopt the above proposal. They will be encouraged to increase the capacity of their installations as well as the battery capacity so that the excess can be exported to the grid during peak hours, when firm economic power is most needed. Such additional features would enhance their financial returns and would enable rapid elimination of the use of diesel during peak hours. In recent months with the depreciation of the rupee, coupled with the increase of costs of solar panels, inverters and batteries, our original analysis of financial viability of this interevention was facing some uncertainties. As such, we welcome this move by the PUCSL, whereby the consumers would have a steady revenue in addition to the savings on their monthly electricity bills. It is likely that the level of FIT and the permitted number of exports will be adequate to work with the increased costs, as shown. (See Table 1)

It must be noted that the cost values are highly volatile ,and some variations are to be expected. FIT for export on energy is stated as 60% of the current peak time energy charge of Rs 106/kWh.

This revolution is well within the means of the over 200,000 potential “Prosumers” who consume over 250 units per month. While they would fulfil their own goal of being immune to any power cuts as well as being insulated from future tariff increases, they would be serving the country by progressively eliminating the need for any fossil fuels for power generation. For example, if 50,000 of them add 10 kWh of battery capacity, the peak power demand can be reduced by 500 MW, thereby obviating the need for using the most expensive diesel during the peak period. Very special advantages can be derived by those also purchasing EVs instead of petrol and diesel vehicles. It will be possible to save on LPG, which costs Rs 4,700.00 per cylinder at present. Thus, the excuse for demanding ever increasing consumer tariff in the future will not be available. As such this move would help all consumers down to the lowest level of consumers.

It is hoped that the energy authorities recognise this reality and support the PUCSL proposals by approving the BESS FIT system and directing all Utility companies to adopt the same and urgently initiate action to install the simple infrastructure additions to accept the BESS energy, as proposed. If they care to review this proposal having discarded biases and any other agendas, they, too, will benefit.

Conclusion

The inescapable conclusion one can derive from the above is that the solution to the crisis is available from the consumers themselves in a manner that is attractive and profitabe to them. It would also be of major assistance for the Utility to manage the sector effectively and efficiently. In addition, all consumers will benefit by gradually weaning themselves away from the grid an use of oil for power generation. This would obviate any more demands for consumer tariff increases by the National System Operator. The PUCSL has taken an essential first step with its intention to declare a BESS FIT. It is up to the government to ensure that the Ministry and the Utility companies adopt the correct stance and make a commitment to ensure the success of this scheme as soon as possible.

by Eng Parakrama Jayasinghe

Past President and Council Member

Bio Energy Association of Sri Lanka

T20 World Cup: Heavyweights, hopefuls and a debutant headline Group 1

Showers in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Diesel replacement costs up to Rs. 4.5 bn in April

Sallay on hunger strike: Counsel warns CID

Opp. questions why Rs 10 bn meant for Ditwah victims held in Treasury account

‘Samurdhi Bank operates without dedicated audit framework’

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoLankan duo emerge winners in Latin dance championship held in Blackpool, UK

-

Latest News4 days ago

Latest News4 days agoKusal Mendis, Pathum Nissanka, bowlers put Sri Lanka 1-0 up

-

News4 days ago

News4 days agoNew US tariffs proposed on 60 countries, including Sri Lanka

-

Features3 days ago

Features3 days agoPower crept into the Sangha and is now tearing it apart

-

News6 days ago

News6 days agoSri Lankan teen killed in Chennai clash; three arrested

-

Features3 days ago

Features3 days agoKondachchi wind farm and battery storage project to boost energy security, says Power Ministry Secretary

-

News2 days ago

News2 days agoAsst. Manager, security officer arrested over Rs 30 mn snatch at Horana PB branch

-

Features3 days ago

Features3 days agoSaudi Arabia sets new benchmark in Hajj management as 1.7 million pilgrims complete sacred journey