Business

Income Tax, Professionals and Migration

by Naomal Goonewardena

I am a lawyer by profession who also happens to have an interest in the subject of tax. My tax liability and income tax payments for the year of assessment 2023/2024 would be more than 300% of that in 2021/2022. Not great by any means.

I have been watching in silence the continuous agitation by professionals in particular with regard to the Inland Revenue (Amendment) Act No.45 of 2022 (“2022 Amendment”) and the additional tax which is payable thereunder by individuals. Almost all of the arguments against the increased tax is accompanied by an implied threat that the high tax rates would accelerate the rate of migration of professionals from the country and the dire consequences which would arise therefrom.

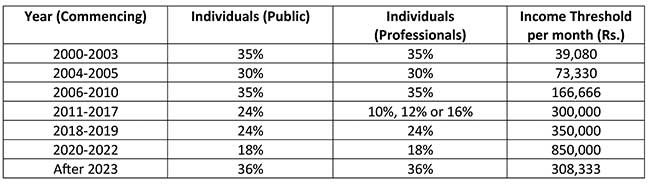

It would be pertinent to analyze the marginal tax rates which have been applicable for individuals from the year 2000 to present and the level of income at which the highest marginal rate would have become applicable. The last column set out above is indicative of the level of income which a person should have on a monthly basis after which he would be liable to pay income tax at the maximum rate specified in the table.

The aforesaid table is clearly indicative that for the period 2000 -2010 the marginal rates of tax were relatively high and therefore, largely comparable to what is going to apply from 2023 onwards. The real problem seems to be that from 2011 onwards, the rate of tax for professionals in particular has fallen down dramatically (other than for 2018/2019) with the result that professionals for all intents and purposes have “forgotten” to pay tax.

The enhanced threshold at which the maximum tax was applicable even at the lower rate increased dramatically from 2020 – 2022 and that seems to be the starting point for any entitlements which are now being spoken of. For example, during this period a person with an income of Rs. 500,000 per month would have only paid about Rs. 10,000 per month as income tax (i.e 2% of income). This is clearly unacceptable. The aforesaid table is clearly indicative that society in general has borne the brunt of this for the benefit of professionals at large very specially between 2011-2017. In my view there is absolutely no justification for professionals to be given any tax concessions which are not available to the other tax paying persons in this country.

I am well aware that in view of inflation in particular, affordability of the tax is in question. The personal reliefs and the level at which the maximum marginal tax rate would apply are also debatable. The real question is as to whether a person having an income of approximately Rs. 300,000 per month should or should not be contributing tax at the rate of 36% on his excess income in the context of large segments of our society being unable to eke out a bare existence for their very survival.

It is easy to say that a large part of government revenue is either wasted or subject to corrupt practices. However, the reality seems to be that major part of government revenue goes towards debt service (i.e interest expenses on borrowing) for which we are all responsible, government salaries and pensions. It is also ironic that persons who are the beneficiaries of these expenses or who have failed miserably in their basic obligation to ensure price stability are also among those who are agitating for a reduction in revenue by way of reduced tax.

It is a fallacy for employees who are subject to Pay-As-You-Earn (PAYE) tax to think that in view of the automatic deduction that they are subject to more tax than others or that other individuals in society who are liable to tax do not pay their tax. The latter pay their tax through the quarterly payment mechanism under the Inland Revenue Act of No.24 of 2017 (“IRA”). The often quoted reason for being reluctant to pay tax is that large parts of society are evading tax and therefore, one should not pay taxes. This in my view is too simple a presumption and it is for any person who says that there are other tax evaders to take the necessary steps to report them specifically to the authorities in a manner that they could share the tax burden of all. However, based on my professional training, pointing to other tax evaders and providing that as a justification for not paying your own taxes is an argument unworthy of a professional.

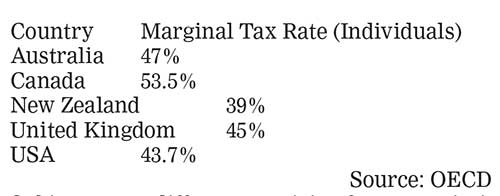

With regard to migration, the following table illustrates the marginal tax rates for individuals in the countries which are often mentioned as being attractive for migration by professionals.

Subject to any differences arising from permissibility of expenses in computing the taxable income, it is clear that any migrant would walk into higher taxes. The migrant would not dare to evade tax in those countries either since the migrant will be summarily thrown out or put behind bars. If a professional wishes to migrate, please do so but do not cite excessive tax in your home country or insufficiency of personal reliefs in computing your taxable income, since any reasonable man in those countries would think that such arguments are hollow to say the least.

We are a Highly Indebted Poor Country (HIPC) and each of us must understand the implications of this. Whichever political party is in power, the government needs revenue. We have exercised our franchise and elected idiots in the past. In 2015 we voted for public sector salary increases which were totally unrealistic which drained the public coffers. In 2019, we the professionals voted for tax cuts, pocketed the additional monies and deprived the State of its due share of revenue. It is now pay-back time for the professionals. In the short term, the increased tax rates should be bearable and in the medium and long term will become palatable.

Increased government revenue is a necessity with current VAT rate of 15% and the marginal income tax rates for individuals and corporates of 36% and 30% being reasonable in a global sense. If any politicians seek your vote or mine on the basis of reducing these tax rates in the absence of alternative concrete revenue generating proposals, let us classify them appropriately as mentioned above and treat them with the contempt which they deserve.

Business

Industry and Entrepreneurship Development Minister Handunneththi’s visit to Lumala highlights key industrial concerns

With the aim of assesing the current challenges faced by local industrialists and explore avenues for government support, Minister of Industry and Entrepreneurship Development Hon. Sunil Handunneththi visited City Cycle Industries Manufacturing (Pvt.) Ltd., widely known as Lumala, on March 24 at its factory in Panadura.

During the visit, Minister Handunneththi engaged with senior officials and employees to understand their concerns and operational difficulties. In a statement shared on social media, the Minister acknowledged the pressing challenges affecting Sri Lanka’s manufacturing sector and emphasized the government’s commitment to providing swift and effective solutions.

Minister Handunneththi further reiterated the government’s intent to position local manufacturers as key stakeholders in Sri Lanka’s economy by addressing regulatory hurdles, market imbalances, and supply chain constraints.

The visit comes amid growing concerns from Lumala employees and management regarding the state of Sri Lanka’s bicycle manufacturing industry, in the backdrop of facing significant challenges, including an influx of imported bicycles and components that circumvent regulatory checks. In addition, the high taxes on raw materials used in local manufacturing has further exacerbated production costs, making it difficult for domestic manufacturers to remain competitive.

Earlier this year, Lumala employees called for urgent government intervention to address these challenges, warning that ongoing financial strain could lead to further shutdowns of critical production units, job losses, and setbacks to the broader industrial ecosystem. With a local value addition of 50-70 percent verified by the Ministry, its workforce remains hopeful that government action will help achieve an ethical manufacturing industry.

Lumala, a household name in Sri Lanka’s bicycle industry, has been a key player in sustainable mobility solutions for over 35 years. The company was recently honored with the Best National Industry Brand award under the Large-Scale Other Industry Sector category at the National Industry Brand Excellence Awards 2024.

With a production capacity of 2,000 bicycles per day and a workforce of 200, Lumala continues to cater to both domestic and international markets, producing a diverse range of bicycles, electric bikes and light electric vehicles. In line with Sri Lanka’s goal to expand forest cover to 32 percent by 2030 and cut GHG emissions by 14.5%, Lumala is actively contributing to this mission—both as a company and through its diverse range of products.

As Sri Lanka works towards strengthening its local manufacturing sector, Minister Handunneththi’s visit signals a crucial step toward addressing industrial concerns and reinforcing government support for sustainable and competitive domestic production.

Sri Lanka’s country rating was upgraded from ‘Restricted Default’ to ‘CCC’ following the successful exchange for the new International Sovreign Bonds (SL ISBs) during December 2024. The three types (03) of exciting new sovereign bonds have restored foreign investor confidence.

The Central Bank of Sri Lanka (CBSL) has performed a remarkable role in guiding the economy out of default status and restored economic stability, and gained Sri Lanka a non-default Country Rating of ‘CCC’. Among the key achievements of CBSL, have been to reduce treasury interest rates under 9% and stabilize the currency while rebuilding foreign reserves to $ 6Bn.

SL offers four Macro Linked Bonds (MLBs) linked to GDP growth, a Governance Linked Bond (GLB) and a short term, Fixed Coupon Bond for unpaid Past Due Interest (PDI). The MLBs offer variable returns depending on SL’s GDP growth from 2024 to 2027, (e.g. haircuts can vary between 16% to 39%). The GLB interest can vary depending on meeting 15.3% and 15.4% of Total Revenue/ GDP thresholds in 2026 and 2027 respectively. The PDI bond offers a fixed coupon of 4% until 2028 and trades at around $94.

This combination of unique, variable returns offers global investors an exciting opportunity to capitalize on SL’s economic revival and US interest rate movements. Sri Lanka’s economic resurgence in 2024 was promising, with a 5% GDP growth rate. With improving investor confidence, SL ISB daily turnover now exceeds $10mn.

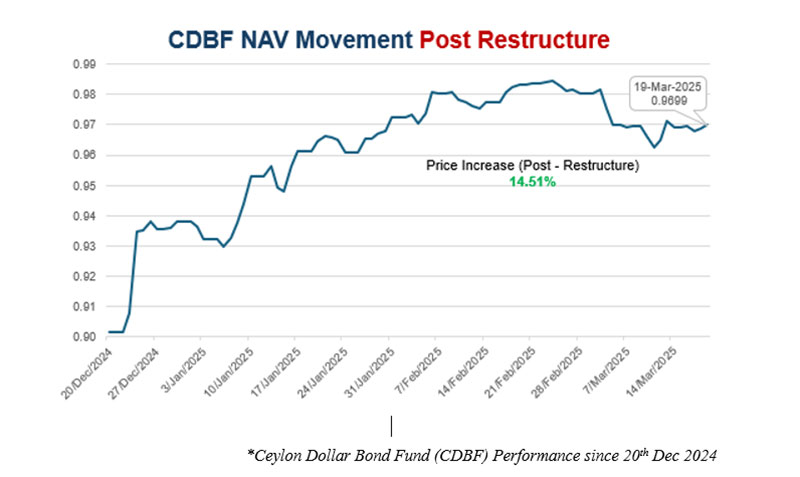

The Ceylon Dollar Bond Fund (CDBF) is the only USD Sovereign Bond Fund that is exclusively invested in SL ISBs with Deutsche Bank acting as the Trustee and Custodian Bank. The Fund reported returns of 53% in 2023 and 39% in 2024.

We invite foreign investors to enter CDBF while Sri Lanka is rated at ‘CCC’ and consider realizing their investment upon SL reaching a Country Rating of ‘B- ‘. Other advantages of CDBF are, the ability to withdraw anytime and being tax exempted.

Ceylon Asset Management (CAM), the Fund Manager, has commenced an advertising campaign to promote the CDBF to the Sri Lankan Diaspora, South Asian, Middle Eastern and Australian Investors. CAM is an Associate Company of Sri Lanka Insurance Corporation (SLIC) and licensed under the Securities and Exchange Commission of Sri Lanka Act, No. 19 of 2021.

Meanwhile, the Ceylon Financial Sector Fund managed by CAM emerged as the top performing rupee fund in Sri Lanka during 2024, with a return of 64%. Investors can find out more on www.ceylonassetmanagement.com or write to us on info@ceylonam.com.

Past performance is not an indicator of the future performance. Investors are advised to read and understand the contents of the KIID on www.ceylonam.com before investing. Among others investors shall consider the fees and charges involved.(CAM)

CSE plunged at open, falling for the second consecutive day yesterday, down over 300 points in mid- morning trade.US President Donald Trump has imposed a 44 percent tax on Sri Lanka’s exports in an executive order which he claimed, spelt out discounted reciprocal rates for about half the taxes and barriers imposed by the island on America.

As a result both indices showed a downward trend. The All Share Price Index dropped 300 points, or 2.32 percent, to 15,294.94, while the S&P SL20 dropped 101 points, or 2.71 percent, to 4,517.37.

Turnover stood at Rs 3.1 billion with six crossings. Those crossings were reported in Sampath Bank which crossed 1.6 million shares to the tune of Rs 181 million and its shares traded at 109, JKH 4.1 million shares crossed to the tune of 80.5 million and its shares sold at Rs 19.5.

Hemas Holdings 400,000 shares crossed for Rs 45.6 million; its shares traded at Rs 114, CTC 25000 shares crossed to the tune of Rs 32.2 million; its shares traded at Rs 1330, Commercial Bank 200,000 shares crossed for 27 million; its shares traded at Rs 135 and TJ Lanka 157,000 shares crossed for Rs 20 million; its shares traded at Rs 46.

In the retail market top six companies that have mainly contributed to the turnover were; Sampath Bank Rs 296 million (2.9 million shares traded), JKH Rs 220 million (11.2 million shares traded), Haylays Rs 195 million (142,000 shares traded), HNB Rs 151 million (519,000 shares traded), Commercial Bank Rs 138 million (1 million shares traded) and Central Finance Rs 129 million (735,000 shares traded). During the day 218 million shares volumes changed hands in 22000 transactions.

It is said the banking sector was the main contributor to the turnover, especially Sampath Bank, while manufacturing sector, especially JKH, was the second largest contributor.

Yesterday, the rupee opened at Rs 296.75/90 to the US dollar in the spot market, stronger from Rs 296.90/297.20 on the previous day, dealers said, while bond yields were up.

A bond maturing on 15.10.2028 was quoted at 10.35/40 percent, up from 10.25/30 percent.

A bond maturing on 15.09.2029 was quoted at 10.50/60 percent, up from 10.45/55 percent.

A bond maturing on 15.10.2030 was quoted at 10.60/70 percent, up from 10.30/65 percent.

By Hiran H Senewiratne

Dulling the pangs of hunger

Worst week for US stocks since Covid crash as China hits back on tariffs

Three-wheeler stolen from court car park run by retired cop

-

News5 days ago

News5 days agoBid to include genocide allegation against Sri Lanka in Canada’s school curriculum thwarted

-

Sports6 days ago

Sports6 days agoSri Lanka’s eternal search for the elusive all-rounder

-

News7 days ago

News7 days agoGnanasara Thera urged to reveal masterminds behind Easter Sunday terror attacks

-

Sports2 days ago

Sports2 days agoTo play or not to play is Richmond’s decision

-

News6 days ago

News6 days agoComBank crowned Global Finance Best SME Bank in Sri Lanka for 3rd successive year

-

Features6 days ago

Features6 days agoSanctions by The Unpunished

-

Features6 days ago

Features6 days agoMore parliamentary giants I was privileged to know

-

Latest News4 days ago

Latest News4 days agoIPL 2025: Rookies Ashwani and Rickelton lead Mumbai Indians to first win