Business

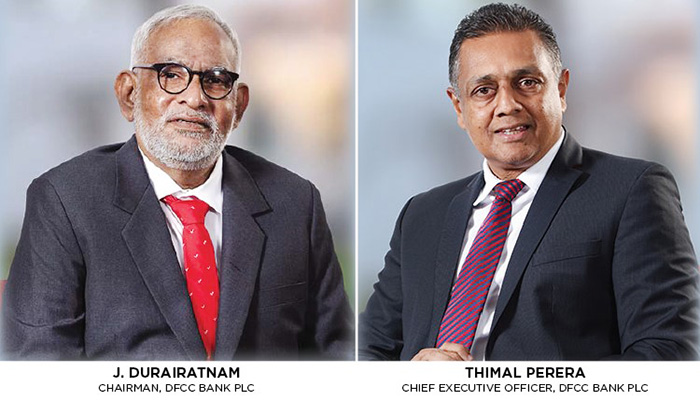

DFCC Bank delivers strong financial performance despite adverse market conditions

The following commentary relates to the unaudited Financial Statements for the period ended 31 March 2023, presented in accordance with Sri Lanka Accounting Standard 34 (LKAS 34) on “Interim Financial Statements”.

Financial Performance

Profitability

DFCC Bank PLC, the largest entity within the Group, reported a Profit Before Tax (PBT) of LKR 2,684 Mn and a Profit After Tax (PAT) of LKR 1,749 Mn for the quarter ended 31 March 2023. This compares with a PBT of LKR 143 Mn and a PAT of LKR 366 Mn in the previous period.

The Group recorded a PBT of LKR 3,001 Mn and PAT of LKR 2,062 Mn for the quarter ended 31 March 2023 as compared to LKR 326 Mn and LKR 527 Mn respectively in 2022. All the member entities of the Group made positive contributions to this performance.

The Bank’s Return on Equity (ROE) increased to 10.88% during the quarter ended 31 March 2023 from 5.04% recorded for the year ended 31 December 2022. The Bank’s Return on Assets (ROA) before tax for the quarter ended 31 March 2023 is 1.63% compared to 0.46% for the year ended 31 December 2022.

Net Interest Income

The Bank’s Net Interest Income (NII), increased by 75% over Q1 of 2022 to reach LKR 8.34 Bn by the quarter end of March 2023. The tight liquidity conditions in the domestic money market have resulted in rising market interest rates. As a result, the Bank’s deposit and lending products experienced a significant increase in interest rates during the period under review. While the higher interest rates may have continued to depress the lending portfolio, it led to an overall improvement in Net Interest income (NII). Strategically, the Bank increased the fixed income investment portfolio, which contributed significantly to an increase in investment interest income. In line with the increase in the AWPLR over the past 12 months, the interest margin increased from 3.80% in March 2022 to 5.93% by March 2023.

Fee and Commission Income

The untiring efforts of the Bank’s staff led to increased remittances, trade-related commissions and other fee income lines which contributed to the increase of non-funded business during the period. Fee income generated by credit cards also increased significantly in line with the volume of the transactions. Accordingly, net fee and commission income have increased to LKR 1,064 Mn for the quarter ended 31 March 2023, compared to LKR 639 Mn in the comparative period in the year 2022.

Impairment Charge on Loans and Other Losses

The impaired loan (stage 3) ratio has increased from 4.36% in December 2022 to 4.80% as of 31 March 2023, a continuation of the trend in the prevailing economic condition. To address the current and potential future impacts of the current economic conditions on the lending portfolio, the Bank made adequate impairment provisions during the period by introducing changes to internal models to account for unseen risk factors in the current highly uncertain and volatile environment. With these provisions made to cover the additional risks in the economic environment, the impairment charge recorded an increase of 67% against the comparative period and stood at LKR 4.69 Bn for the quarter ended 31 March 2023 compared to LKR 2.81 Bn in the comparable period.

Operating Expenses

The operating expenses for the quarter ended on 31 March 2023 increased due to an increase in IT-related expenses as a result of infrastructure upgrades, as well as cost increases due to inflation and the Sri Lanka Rupee devaluation. However, the numerous process automation and workflow management systems introduced over the period helped curtail and manage operating expenses at reduced levels.

Other Comprehensive Income

Changes in the fair value of investments in equity securities and fixed income securities (treasury bills and bonds) and movement in hedging reserves are recorded through other comprehensive income.

Due to the application of hedge accounting, the impact on the bank equity due to the exchange fluctuation was minimized. A fair value gain of LKR 2,034 Mn was recorded on account of equity securities outstanding as at 31 March 2023. The increase in the share price of Commercial Bank of Ceylon PLC during the period was the main contributor to the reported fair value gain in equity securities. The favourable movement in the treasury bills and bonds yields resulted in a fair value gain of LKR 908 Mn during the period.

Business Growth

Assets

Despite the challenges faced by the economy and the banking sector, DFCC Bank’s total assets increased by LKR 9.8 Bn, recording a growth of 1.75% from December 2022. In line with the bank’s growth strategy and the current economic situation, an increase in investment in fixed income securities, combined with positive fair value movement in both fixed income securities and equity securities, has contributed to a 49% increase in investment in financial assets at fair value through other comprehensive income as of 31 March 2023 compared to the balance as of 31 December 2022. With increased provision for expected credit losses and appreciation of the Sri Lanka Rupee, the net loan portfolio has recorded LKR 357 Bn as at 31 March 2023.

Liabilities

The Bank’s deposit base experienced a growth of 2.29%, recording an increase of LKR 8,490 Mn to LKR 378,805 Mn from LKR 370,314 Mn as at 31 December 2022. This resulted in recording a loan to deposit ratio of 104.33%. Further the CASA ratio is 18.05% as at 31 March 2023. The Bank’s funding costs were also contained by using medium to long-term concessionary credit lines. When these concessionary term borrowings are considered, the CASA ratio further improved to 29.86% and the loans to deposit ratio improved to 89.02% as at 31 March 2023.

Equity and Compliance with Capital Requirements

DFCC Bank’s total equity increased to LKR 57 Bn as at 31 March 2023 with the recorded profit after tax of LKR 1.75 Bn. The favourable movements in the equity portfolio and fixed income security portfolio classified as fair value through other comprehensive income and positive movement in hedging reserve also resulted in an increase of the Bank’s total equity.

As at 31 March 2023, the Bank Recorded Tier 1 and Total Capital ratios of 10.171% and 12.848%, respectively. The Bank’s Net Stable Funding Ratio (NSFR) was 128.24%, and Liquidity Coverage Ratio (LCR) – all currency was 226.43% as at 31 March 2023. All these ratios were maintained above the minimum regulatory requirement.

CEO’s Statement

“As we reflect on the last quarter’s performance, we are pleased to report strong financials across all business areas. Sri Lanka’s resilient and adaptable economy and our commitment to innovation, operational excellence, and customer-centricity continue to pay off, as evidenced by our steady revenue growth and increased profitability. We are confident that our robust growth strategy and prudent risk management practices will enable us to continue delivering sustainable value to our stakeholders in the long term, which bodes well for the overall economic situation of Sri Lanka.”

Construction giant Sanken Lanka behind the move

When Bathiya & Santhush took their seats alongside Rohit Sachdev, CEO and Founder of Soho Hospitality, at a recent press briefing in Colombo, it seemed at first like a courtesy appearance. Moments later, it became the headline: the duo were introduced as co-investors in Charcoal Tandoor Fire Grill’s Colombo debut.

That revelation that Bathiya and Santhush are not merely endorsing but co-owning the restaurant venture alongside Sanken Lanka, the company behind the Capitol TwinPeaks skyscraper is likely to resonate strongly with Sri Lankan audiences.

Charcoal Tandoor Fire Grill will open on the 50th floor of Capitol TwinPeaks at Union Place – home to Colombo’s tallest sky bridge, rising nearly 600 feet above the city. The Bangkok-born brand marks the first South Asian expansion of Soho Hospitality’s flagship Indian dining concept.

Founded in 2014 in Bangkok, Charcoal built its reputation by reinterpreting North Indian tandoor traditions and Mughlai richness through a contemporary, design-led lens. Live fire cooking, layered spice profiles and slow techniques define its culinary identity – dramatic yet calibrated.

For Bathiya, the investment is rooted in artistic kinship.

“Rohit is passionate about what he is doing,” he said. “His culinary art goes parallel to our showbiz in its finer details. We wanted Sri Lankans to devour that delicacy. We wanted to bring that brand excellence to our shores.”

Santhush drew an even broader connection between gastronomy and performance.

“For three decades we’ve worked to make Sri Lankan music a global product – to create that Sri Lankan musical vibe felt across the world,” he said. “Hospitality is part of the entertainment landscape. We take music and events to the outside world. Now we wanted to bring a global product and experience home.”

He likened Sachdev’s precision in the kitchen to orchestral mastery. “He works like a master of an orchestra – going into intricate details in his culinary art as we sift through every frequency of sound.”

Sachdev described Sri Lanka as a deliberate, data-driven choice for Charcoal’s first step beyond Thailand.

“Charcoal has always been built on heritage, movement and exchange – of flavours, ideas and experiences,” he said. “Sri Lanka felt like a natural step beyond Thailand. We see strong long-term fundamentals in Colombo, from tourism growth to an increasingly discerning dining audience.”

Colombo’s positioning at the crossroads of South Asia, the Middle East and Southeast Asia aligns neatly with Charcoal’s “Spice Route” narrative — a concept inspired by historic trade routes that blended flavours and commerce across regions.

Bathiya and Santhush built their careers by exporting Sri Lankan creativity to the world stage. Now, in a reversal of that flow, they are importing a globally recognised hospitality brand — embedding it within Colombo’s evolving skyline, backed by Sanken Lanka.

By Sanath Nanayakkare

The strongest financial performance in its history

Sampath Group has delivered the strongest financial performance in its history for the year ended December 31, 2025, recording a Profit Before Tax (PBT) of Rs 53.0 billion and a Profit After Tax (PAT) of Rs 32.6 billion. This marks year-on-year growth of 8% and 13% respectively, solidifying the Group’s position as one of Sri Lanka’s most resilient and forward-thinking financial institutions.

The Group also surpassed a significant milestone with its total asset base crossing the Rs 2 trillion mark—up 12% from 2024—reflecting strong credit expansion and prudent portfolio management.

The Sampath Bank, the Group’s flagship entity, continued to be the main engine of growth, posting its highest-ever profitability with a PBT of Rs 49.3 billion and PAT of Rs 30.2 billion—up 5% and 11% respectively. Adjusted for the one-off gains from the 2024 restructuring of Sri Lanka’s international sovereign bonds, both PBT and PAT grew an impressive 22%.

Driven by strong credit momentum, the Bank’s gross loan book expanded by Rs 259 billion (27%), reaching Rs 1.2 trillion by end-2025. Deposits rose 12% to Rs 1.65 trillion, underscoring the Bank’s trusted franchise and continued market confidence.

Shareholders benefited from a higher final dividend of Rs 10.30 per share, up Rs 0.95 from last year, with a payout ratio of 39.98%. The Bank’s Return on Equity (ROE) edged up to 17.93% (2024: 17.74%), while Return on Assets (ROA, before tax) stood at 2.60%.

Sampath Bank also reinforced its robust balance sheet, ending the year with Tier 1 and Total Capital Adequacy Ratios of 14.75% and 17.65% respectively—well above regulatory requirements. Liquidity remained strong with a Liquidity Coverage Ratio of 239.79% and Net Stable Funding Ratio of 173%.

Gross income grew 12% to Rs 218.8 billion, supported by the Bank’s diversified earnings base. Interest income dipped marginally by 1% to Rs 181.1 billion, reflecting lower market rates, but was offset by significant growth in non-fund-based income streams.

Net fee and commission income rose 21% to Rs 21.2 billion, buoyed by increased economic activity, higher card usage, and process efficiencies. Notably, the Bank recorded a Rs 6.5 billion trading gain, reversing a Rs 2.8 billion loss in 2024—largely due to exchange gains following a Rs 16.63 depreciation of the rupee against the dollar.

In a major turnaround, Sampath reported an impairment reversal of Rs 0.6 billion, supported by recovery efforts, lower Stage 2 and Stage 3 loan exposure, and improved customer repayment capacity. Stage 3 loans dropped to 9.6% from 13.7% in 2024, while Stage 2 fell to 7.6% from 15.7%.

Operating expenses increased 19% as the Bank accelerated investments in technology, staff expansion, and strategic initiatives aimed at long-term growth. Consequently, the cost-to-income ratio rose slightly to 42.7%.

Sampath Bank remained one of the largest contributors to government revenue, paying over Rs 39 billion in total taxes during 2025, compared with Rs 33.8 billion the previous year. Its effective tax rate was 52.3%.

The Sampath Group continues to broaden its financial presence, operating four subsidiaries—Siyapatha Finance PLC, Sampath Securities (Pvt) Ltd, Sampath Information Technology Solutions Ltd, and Sampath Centre Ltd. In January 2026, it established a new wealth management arm to meet emerging customer needs, pending regulatory approval.

Reaffirming its leadership in sustainability, Sampath Bank expanded its ESG-driven initiatives under its “Wewata Jeewayak” program, restoring its 28th village tank to support rural agriculture. The Bank also continued its coral and mangrove restoration, forest replantation, and turtle conservation projects.

In a pioneering move, the Bank implemented Sri Lanka’s SLFRS S1 and S2 standards under its Climate First Action Plan and introduced a Green Fixed Deposit framework with independent assurance for credibility and transparency.

Responding to the devastation of Cyclone Ditwah, Sampath Bank donated Rs 100 million to the “Rebuilding Sri Lanka” fund, alongside humanitarian aid to the Sri Lanka Red Cross and Air Force.

“Our record-breaking performance in 2025 reflects not just financial resilience, but a steadfast commitment to national progress and sustainable growth,” said Sanjaya Gunawardana, Managing Director and CEO of Sampath Bank PLC.

National Savings Bank (NSB) has been awarded the Gold Award in the State Bank Category at the TAGS Awards 2025, organized by the Institute of Chartered Accountants of Sri Lanka (CA Sri Lanka). Celebrated under the theme “Diamond Chapter – The Grand Honour of Excellence,” the awards recognize organizations that demonstrate exceptional commitment to transparency and governance through their annual reports.

The Gold Award, bagged by NSB, highlights the Bank’s continued dedication to maintaining high standards of disclosure and stakeholder engagement while strengthening governance and accountability across all operations. The rigorous evaluation process assesses not just financial performance, but also how effectively organizations communicate strategy, sustainability initiatives, and long-term value creation.

Chairman Dr. Harsha Cabral PC, accepting the award alongside the NSB team, stated that the recognition is a testament to the collective efforts of the Board, Management, and staff in upholding the highest standards of corporate governance and responsible banking. He noted that maintaining transparency remains fundamental to sustaining public trust, particularly as NSB advances its digital transformation journey while supporting national economic development.

The achievement reflects the Bank’s disciplined financial stewardship and its commitment to presenting a forward-looking account of its performance.

Dottin out obstructing the field as Sri Lanka clinch series

Prime Minister Attends the 40th Anniversary of the Sri Lanka Nippon Educational and Cultural Centre

Navy’s latest addition P 628 sails for Colombo from Baltimore

Commander of the Navy attends International Fleet Review

Prime Minister attends 169th birth anniversary celebration of Lord Robert Baden-Powell

Coal ash surge at N’cholai power plant raises fresh environmental concerns

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features2 days ago

Features2 days agoWhy does the state threaten Its people with yet another anti-terror law?

-

Features2 days ago

Features2 days agoVictor Melder turns 90: Railwayman and bibliophile extraordinary

-

Features2 days ago

Features2 days agoReconciliation, Mood of the Nation and the NPP Government

-

Features2 days ago

Features2 days agoVictor, the Friend of the Foreign Press

-

Latest News3 days ago

Latest News3 days agoNew Zealand meet familiar opponents Pakistan at spin-friendly Premadasa

-

Latest News3 days ago

Latest News3 days agoTariffs ruling is major blow to Trump’s second-term agenda

-

Latest News3 days ago

Latest News3 days agoECB push back at Pakistan ‘shadow-ban’ reports ahead of Hundred auction

-

Features13 hours ago

Features13 hours agoLOVEABLE BUT LETHAL: When four-legged stars remind us of a silent killer