Business

Central Bank reserves poised to top USD 5 billion: State Minister

‘Commencement of loan repayments won’t make a dent in reserves’

By Sanath Nanayakkare

The amount of foreign reserves possessed by the Central Bank of Sri Lanka is now poised to exceed U5D 5 billion, and the commencement of foreign loan repayments in the coming months won’t make a dent in current reserves, State Minister of Finance Ranjith Siyambalapitiya told the media yesterday.

Responding to a query from the media whether the commencement of foreign debt repayments could see an immediate dip in the reserve levels, the state minister said that the whole objective of debt restructuring is to avert a significant depletion of foreign reserves.

“The debt restructuring process agreed with bilateral creditors and commercial creditors is being designed to ensure effective management of our foreign reserves. It is all about adjusting our loan repayments in line with the Central Bank’s foreign reserves. The Balance of Payment (BOP) transactions which consist of imports and exports of goods, services, remittances as well as transfer payments will be executed in a way that won’t put pressure on foreign reserves,” he said.

However, he mentioned that the government would not completely remove its ban on importing vehicles any time soon as it is a key measure of keeping tabs on foreign exchange outflows.

“The Central Bank acquired this desired level of foreign reserves by purchasing US dollars from the market. This is a favourable development. All import bans and restrictions have now been lifted except for vehicle imports. That too, we are opening according to emerging requirements. For example, we have allowed the importation of 750 vans and 250 buses to be deployed for tourist transportation as the requirement for it was justified. In a similar manner, vehicle imports will be allowed in accordance with the requirements. So, in future, vehicle imports will be allowed only if the government sees the genuine need for that,” he said.

When the Island Financial Review contacted Ranjith Sudasinghe, vice president of Sri Lanka Chauffeur Tourist Guide Lecturers Association, he said that members of their Association would be at risk when they don’t get new vehicles for tourist transportation while only select big companies in the industry would get them.

“We have made repeated appeals to Sri Lanka Tourism authorities pointing out that our vehicles are old and tourists won’t find them appropriate for a round-tour of Sri Lanka. Even Destination Management Companies (DMCs) would reject our vehicles when they get new vehicles. So, the authorities should create a level playing field for all tourist transportation stakeholders. The government should consider allowing us to import vehicles at a concessional duty rate after an assessment of the conditions of our vehicles. Farmers get fertilize subsidies, fisher folks get facilities from the government. But the chauffeur guides are receiving a step-motherly treatment from the authorities which is not fair. We are only asking to replace our old tourist vehicles with news ones at a concessional duty rate. At present we are charging less than what a three-wheeler charges per kilometer because we are told to be competitive with fares in the regional countries. Now with the new tourist vehicles coming in and we have been left out of the process, we are going to be squeezed out of our livelihoods,” he said.

The government has initiated what could become one of the most significant reforms of Sri Lanka’s social security system in decades by appointing a Senior Officials’ Committee to examine the feasibility of bringing the Employees’ Provident Fund (EPF) and the Employees’ Trust Fund (ETF) under a unified tripartite governance framework representing the government, employers and employees.

Cabinet approval was granted following a proposal submitted by the Minister of Labour. According to Cabinet Spokesman and Minister Dr. Nalinda Jayatissa, the committee has been mandated to study whether the two institutions could operate under a common governance structure based on internationally recognised principles promoted by the International Labour Organization (ILO).

He stressed that the committee has been appointed only to examine the feasibility of the proposal, and no final decision has been taken to merge the two funds.

The official Cabinet statement notes that the EPF, established under the Employees’ Provident Fund Act No. 15 of 1958, has more than 2.5 million members and assets exceeding Rs. 4.9 trillion, making it Sri Lanka’s largest social security fund.

Custody of the fund, investment management, financial administration and payment of benefits are currently handled by the Central Bank of Sri Lanka, while the Department of Labour is responsible for member registration, employer compliance, recovery of arrears and safeguarding employee rights.

The ETF, created under Act No. 46 of 1980, is administered by a tripartite board comprising representatives of the government, employers and employees. It manages assets of approximately Rs. 637 billion and provides coverage to more than 2.5 million active members.

The Cabinet paper highlights that tripartite governance of social security institutions is an internationally recognised best practice and a fundamental principle promoted by the ILO, which forms the basis for examining a common governance model for both funds.

The proposal is expected to attract close scrutiny from the business community, trade unions and financial market participants, given that the combined assets of the EPF and ETF exceed Rs. 5.5 trillion, making them among the country’s largest institutional investors.

Economists note that any governance reforms should strengthen transparency, accountability, professional investment management and public confidence while safeguarding workers’ retirement savings.

By Ifham Nizam

LOLC Microfinance Bank Pakistan, a fully owned subsidiary of the LOLC Group, has strategically relocated its Head Office to Gulberg Greens, Islamabad, marking a significant milestone in its growth journey. As one of the LOLC Group’s largest overseas operations in Asia, the Bank continues to advance financial inclusion and sustainable economic development across Pakistan.

The new Head Office was formally inaugurated in the presence of Chief Guests H.E. Admiral Fred Seneviratne (Retd.), High Commissioner of Sri Lanka to Pakistan, and Mr. Krishan Thilakaratne, Chairman of LOLC Microfinance Bank Pakistan. The ceremony was attended by the Bank’s Board of Directors, senior management and employees, commemorating another important chapter in the Bank’s continued expansion.

LOLC Microfinance Bank Pakistan is a fully-fledged Microfinance Bank regulated by the State Bank of Pakistan, operating through a network of 88 branches and employing over 1,200 staff members across the key cities of Karachi, Lahore, Hyderabad, Faisalabad, Sialkot, Islamabad, Peshawar and Gilgit. The Bank offers a comprehensive range of financial solutions, including business loans, microfinance, vehicle financing, gold loans and other financial products. It currently manages a loan portfolio exceeding USD 70 million and a deposit portfolio exceeding USD 90 million, comprising savings deposits, term deposits and current accounts.

The relocation to the new Head Office reflects the Bank’s expanding operations and its commitment to widening access to responsible financial services for individuals, micro-entrepreneurs and small businesses across Pakistan. In 2026, LOLC Microfinance Bank Pakistan was recognised as Pakistan’s fastest growing Microfinance Bank, highlighting its strong business momentum and growing market presence.

Addressing the gathering, H.E. Admiral Fred Seneviratne (Retd.), High Commissioner of Sri Lanka to Pakistan, stated, “The relationship between Sri Lanka and Pakistan continues to grow through meaningful partnerships such as this. LOLC Microfinance Bank Pakistan is making an important contribution by supporting entrepreneurs, strengthening the SME sector, and expanding financial access where it is needed the most. Institutions like these play a vital role in empowering communities and supporting sustainable economic growth.”(LOLC)

Citizens Development Business Finance PLC (CDB) lit up the CCC Grounds on June 28th, retaining the championship of the MCA T10 Cricket Tournament, further etching its record of being unbeaten and showcasing its signature persona of being determined and unstoppable.

Sealing the title without a single loss in the tournament from the first ball to the final cheer, Team CDB skippered by Tharindu Rathnayaka with Vice Captain Dunith Wellalage, both national players, showcased the calibre of a champion side.

Coached by national player Oshadha Fernando, CDB combined star power with relentless team spirit – the perfect combination of experience and youthful energy. CDB’s performance was not just about individual brilliance but about a collective drive that mirrors CDB’s corporate ethos of perseverance, leadership, and excellence.

The final match against the Abans Group was a fitting climax. Chasing 116, CDB powered to 120/4 in just 8.4 overs, sealing victory by six wickets. Vishad Randika rose to the occasion as Player of the Final. Nuwan Thushara’s consistent bowling prowess, including a hat trick — 2 overs, 11 runs, 4 wickets during the semi-finals — earned him the Best Bowler accolade.

This unbeaten run was more than a cricketing triumph. It was a statement by CDB of its dedication to excellence, which extends beyond financial services into fostering a high-performance culture through sports. The championship reinforced the company’s reputation as a leader in the financial sector while celebrating employee engagement, wellness, and community spirit.

President chairs discussion on 2027 Budget Proposals for the Ministry of Industry and Entrepreneurship Development

Prime Minister meets the Amir of the State of Qatar and conveys condolences on the passing of the Father Emir

Current El Niño Status in Sri Lanka

A few showers may occur in the Western, Sabaragamuwa and North-western provinces and in Kandy, Nuwara-Eliya, Galle and Matara districts.

Argentina face fine for Falklands banner in semi-final win

US launches fresh strikes on Iran as Trump warns Tehran it ‘better behave’

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News7 days ago

News7 days agoHerath warns prospective migrant workers not to get fleeced by racketeers

-

Features5 days ago

Features5 days agoPrison riots and politics: NPP’s biggest challenge and Sri Lanka’s biggest opportunity

-

Editorial6 days ago

Editorial6 days agoWhat’s the world coming to?

-

Foreign News7 days ago

Foreign News7 days agoTensions erupt in Indian state after 11-year-old raped and murdered

-

Features7 days ago

Features7 days agoDevanesan Annan – in Memoriam

-

Editorial7 days ago

Punishment in hellholes

-

Features2 days ago

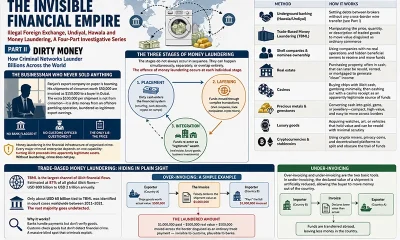

Features2 days agoDirty Money

-

Editorial5 days ago

Editorial5 days agoMuch ado about crime: Fish or cut bait