Latest News

IMF Executive Board Concludes 2024 Article IV Consultation with Sri Lanka and Completes the Second Review Under the Extended Fund Facility

The Executive Board of the International Monetary Fund (IMF) completed the second review under the 48-month Extended Fund Facility (EFF) Arrangement, allowing the authorities to draw SDR 254 million (about US$336 million). This brings the total IMF financial support disbursed so far to SDR 762 million (about US$1 billion). The Executive Board also concluded the 2024 Article IV Consultation with Sri Lanka.

The EFF arrangement for Sri Lanka was approved by the Executive Board on March 20, 2023 (see Press Release No. 23/79) in an amount of SDR 2.286 billion (395 percent of quota or about US$3 billion. The first review of the EFF was completed by the Executive Board on December 12, 2023 with disbursements of SDR 254 million (about US$337 million; see Press Release No. 23/439).

The EFF-supported program aims to restore Sri Lanka’s macroeconomic stability and debt sustainability, mitigate the economic impact on the poor and vulnerable, rebuild external buffers, safeguard financial sector stability, and strengthen governance and growth potential.

Signs of economic recovery are emerging. Real GDP expanded by 3 percent (y-o-y) in the second half of 2023. May 2024 inflation was 0.9 percent and gross international reserves increased to US$5.5 billion by end-April 2024. The primary balance improved to a surplus with tax revenue increasing to 9.8 percent of GDP in 2023. Despite improvements in non‑performing loans, pockets of vulnerabilities remain in the banking sector.

The recovery remains gradual, and the medium-term growth potential hinges on appropriate policy settings. Growth is projected to recover moderately in 2024-25 given constrained bank credit and fiscal consolidation, while facing uncertainties around the debt restructuring and policy direction following the elections. Inflation is expected to temporarily increase due to one-off factors. The current account is expected to remain positive in 2024, driven by improved tourist arrivals and remittances. Domestic risks could arise from waning reform momentum, especially on revenue mobilization. External risks are associated with intensified regional conflicts, commodity price volatility, and a global slowdown. Slow progress in debt restructuring could widen financing gaps.

Following the Executive Board’s discussion, Kenji Okamura, Deputy Managing Director and Acting Chair, issued the following statement:

“Sri Lanka’s performance under its Fund-supported program remains strong. All quantitative targets were met, except for the marginal shortfall of indicative target on social spending. Most structural benchmarks were either met or implemented with delay. Reforms and policy adjustment are bearing fruit. The economy is starting to recover, inflation remains low, revenue collection is improving, and reserves continue to accumulate. Despite these positive developments, the economy is still vulnerable and the path to debt sustainability remains knife-edged. Important vulnerabilities associated with the ongoing debt restructuring, revenue mobilization, reserve accumulation, and banks’ ability to support the recovery continue to cloud the outlook. Strong reform efforts, adequate safeguards, and contingency planning help mitigate these risks.

“To restore fiscal sustainability, sustained revenue mobilization efforts, promptly finalizing the debt restructuring in line with program targets, and protecting social and capital spending remain critical. Advancing public financial management will help enhance fiscal discipline, and strengthening the debt management framework is also needed.

“Monetary policy should continue prioritizing price stability, supported by a sustained commitment to refrain from monetary financing and safeguard central bank independence. Continued exchange rate flexibility and gradually phasing out the balance of payments measures remain critical to rebuild external buffers and facilitate external rebalancing.

“Restoring bank capital adequacy and strengthening governance and oversight of state-owned banks are top priorities to revive credit growth and support economic recovery.

“The authorities need to press ahead with their efforts to address structural challenges to unlock long-term potential. Key priorities include steadfast implementation of the governance reforms; further trade liberalization to promote exports and foreign direct investment; labor reforms to upgrade skills and increase female labor force participation; and state-owned enterprise reforms to improve efficiency and fiscal transparency, contain fiscal risks, and promote a level playing field for the private sector.

Executive Board Assessment

Executive Directors commended the authorities’ strong performance under the Fund‑supported program, noting that reforms are bearing fruit. The economy has started to recover, inflation remains low, revenue collection is improving, and reserves continue to accumulate. Directors underscored, however, that important vulnerabilities and uncertainties remain, including with respect to the ongoing debt restructuring and the upcoming elections. Against this backdrop, they called on the authorities to continue strengthening macroeconomic policies to restore economic stability and debt sustainability and to sustain the reform momentum to promote long‑term inclusive growth.

Directors underscored that restoring fiscal sustainability requires additional revenue measures underpinning the 2025 Budget, further tax administration reforms, as well as limiting tax exemptions and making them more transparent. They called for protecting growth‑enhancing and social spending, and for improving the social safety net. Directors welcomed the submission of the new Public Financial Management bill to Parliament, which would strengthen fiscal discipline and establish a solid fiscal framework. They noted that further efforts to strengthen the debt management framework are also needed. Directors welcomed the progress on achieving cost‑recovery in energy pricing, noting its criticality for containing risks from state‑owned enterprises (SOEs).

Directors welcomed the progress made to advance debt restructuring to restore Sri Lanka’s debt sustainability. They called for a swift finalization of the Memorandum of Understanding with the Official Creditor Committee and final agreements with the Export‑Import Bank of China. Directors stressed the importance of seeking comparable, transparent, and timely completion of restructurings with external private creditors consistent with program targets.

Directors emphasized that maintaining price stability remains the top priority for monetary policy, which requires anchoring inflation expectations, continuing to refrain from monetary financing, and the gradual unwinding of government security holdings as markets allow. They also stressed the importance of strengthening central bank independence. Directors underscored the need to continue building external buffers, while maintaining exchange rate flexibility to facilitate external rebalancing and preserve the credibility of the inflation targeting regime. They called for gradually phasing out the balance of payments measures.

Directors underscored the need to strengthen financial sector resilience to support the recovery. They called for swift completion of the restructuring of remaining domestic law, foreign currency loans and for adequate recapitalization of commercial and state‑owned banks. Directors welcomed the enactment of the Banking Act amendments and emphasized the importance of their effective implementation to enhance supervision and the governance of state‑owned banks. They also called for further efforts to strengthen the anti‑money laundering and counter‑terrorism financing framework.

Directors stressed that pressing ahead with governance and structural reforms, supported by development partners and IMF capacity development, is crucial to unlock growth potential. They welcomed the publication of the authorities’ action plan on the key governance reforms recommended in the Governance Diagnostic Report and called for its steadfast implementation. Directors also recommended prioritizing reforms to further liberalize trade, improve the investment climate and SOE efficiency, reduce gender gaps in the labor market, and mitigate climate vulnerabilities.

| Sri Lanka: Selected Economic Indicators 2021–2029

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Rescuers are rushing to locate dozens of people missing in the southwestern Chinese city of Chongqing, after a deadly landslide buried homes in the area, according to Chinese authorities.

The landslide took place around 9:10am (01:10 GMT) on Friday in Chongqing’s Pengshui county, killing eight people, leaving 34 unaccounted for and displacing more than 1,100, reported state media.

Footage shared by China’s CCTV broadcaster showed a huge buildup of rocks and dirt covering part of a residential and commercial street at the bottom of a mountain in the region.

Ten people have been rescued from the debris, including two who are seriously injured, reported China’s state-run Xinhua news agency.

Water, electricity and gas supplies were cut off within a one-kilometre (0.6-mile) radius of the landslide to prevent further disruptions. More than 800 rescuers have gone to the site, reported CCTV.

Authorities said they sent more than 8,000 disaster relief items to Chongqing, including tents, folding beds and family emergency kits.

Pengshui county is located in the southeast part of Chongqing, bordering the provinces of Hubei and Guizhou.

The area where the landslide happened is known for “unpredictable” steep terrain, a local official told a news conference, adding that dangerous rocks remain along the sides of the cliff.

The government has allocated 50 million yuan ($7.36m) in natural disaster relief funds to support the rescue and relief operations and to provide assistance to affected residents, the Ministry of Finance and the Ministry of Emergency Management said.

[Aljazeera]

Sir Garry Sobers the legendary West Indies allrounder and one of the sport’s most towering icons, has died at his home in Barbados. He was 89 years old.

Widely regarded by many as the greatest allrounder and most gifted cricketer to have played the game, Sobers excelled as Test batter, could bowl left-arm pace as well as orthodox and wrist-spin, and he was an exceptional fielder and close-in catcher – attributes that once led his fellow all-timer, Sir Donald Bradman, to describe him as a “five-in-one cricketer”.

Sobers played 93 Test matches for West Indies between 1954 and 1974, scoring 8032 runs at an average of 57.78 and took 235 wickets at an average of 34.03. He also captained West Indies in 39 Tests between 1965 and 1972, winning nine and losing 10. The ICC’s premier annual award in men’s cricket – the Sir Garfield Sobers Award – is named in his honour and recognises the most outstanding overall performer in men’s international cricket across all formats.

Sobers made his first-class cricket debut at the age of 16, against the touring India team in January 1953, and excelled with four first-innings wickets to help his side enforce the follow-on. His Test debut followed a year later, against England in Jamaica, where he scored 14 and 26 from No.9 and took 4 for 75 in England’s first innings.

He played his initial Tests as a bowler, but at the age of 23 he scored his maiden Test hundred and also broke Len Hutton’s world record for the highest individual Test score by making 365 against Pakistan at Sabina Park in 1958. It was a record that stood until 1994, when it was broken by Brian Lara, an achievement Sobers was on hand to witness and celebrate.

A decade after that record-breaking innings, Sobers became the first cricketer to hit six sixes in an over in first-class cricket – off Glamorgan’s Malcolm Nash – while playing for Nottinghamshire in Swansea. His first-class career comprised 383 matches for West Indies, Barbados, Nottinghamshire and South Australia and he amassed 28,314 runs at an average of 54.87 and took 1043 wickets at an average of 27.74.

While Sobers played 95 List A games, his international career had wound down by the advent of ODIs and he played only one international in that format – against England at Headingley in 1973. He was knighted for his services to cricket in 1975, and in 2000, he was named as one of Five Cricketers of the Century by Wisden Cricketers’ Almanack, alongside Bradman, Sir Jack Hobbs, Sir Viv Richards and Shane Warne.

Born in Barbados in 1936, Sobers was the fifth of six children, and was raised primarily by his mother after his merchant-seaman father died during the Second World War in 1942. He was born with six fingers on each hand – the extra digits were removed in his childhood – and he excelled in all sports, including basketball, football and golf.

In a statement on behalf of Cricket West Indies, the board president, Dr. The Hon. Kishore Shallow, described Sobers as the “greatest cricketer the world has ever seen”, and offered his “heartfelt condolences to his family, the Government and people of Barbados and all those across the world who mourn his passing.

“There are moments in the story of a people when the life of one individual becomes woven into the hopes, dreams, and identity of generations,” Swallow added. “Today, the Caribbean mourns the passing of such an individual … His mastery of batting, bowling and fielding was unparalleled, but his true significance reached far beyond the boundary ropes.

“He emerged from the Caribbean at a time when our region was finding its voice and asserting its place on the world stage. Through his excellence, he gave millions across our islands and in the diaspora, a renewed belief in what was possible. He showed that greatness was not confined by the size of our nations, the geography of our islands or the circumstances of our beginnings.

“Sir Garfield Sobers became more than a sporting icon. He became a symbol of Caribbean excellence, resilience, and possibility. His achievements brought pride to Barbados, inspiration to the West Indies and admiration from every corner of the cricketing world.”

(Cricinfo)

A tsunami warning has been issued for parts of the Pacific after a powerful magnitude 7.3 earthquake struck off the coast of southern Mexico on Friday.

Showers may occur in the Western, Sabaragamuwa and North-western provinces and in Kandy, Nuwara-Eliya, Galle and Matara districts

Dengue outbreak gallops ahead: Infections surpasses 73,455, leaving 50 dead

Evidence recorded in money laundering case against Yoshitha Rajapaksa

Former IGP C.D. Wickramaratne dies in suspected suicide

CAA sets aflatoxin limit for processed liquid milk from January 2027

Son of ex-Justice Minister further remanded till July 28

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features6 days ago

Features6 days agoPrison riots and politics: NPP’s biggest challenge and Sri Lanka’s biggest opportunity

-

Features3 days ago

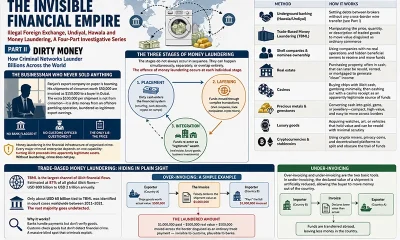

Features3 days agoDirty Money

-

Editorial6 days ago

Editorial6 days agoMuch ado about crime: Fish or cut bait

-

Features6 days ago

Features6 days agoMore on Saudi Arabia: ARAMCO and beyond

-

News1 day ago

News1 day agoMoney laundering case against Yoshitha, fixed for pre-trial conference

-

Sports6 days ago

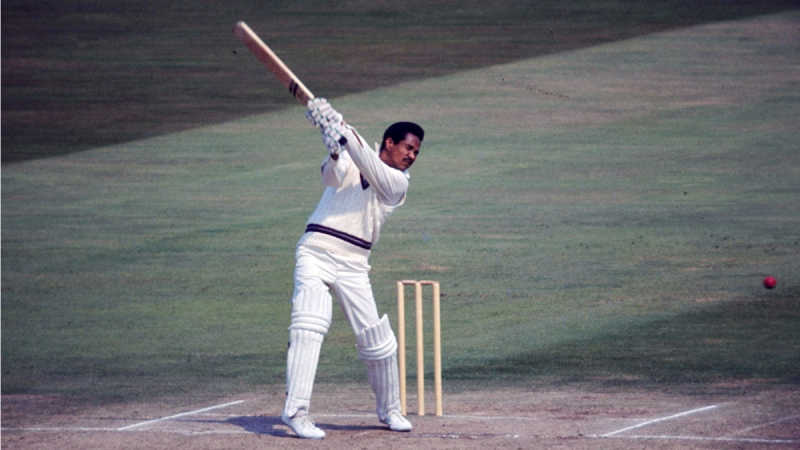

Sports6 days agoThe banker who rescued Sri Lankan cricket

-

Midweek Review3 days ago

Midweek Review3 days agoThe sordid tale of theft and tragedy at Finance Ministry

-

Latest News4 days ago

Latest News4 days agoOil prices hit 1-month high as US-Iran attacks dim Strait of Hormuz outlook