Features

Public enemy number one: Inflation? Accumulation of public debt?

Convict a man for his convictions?

by Usvatte-aratchi

The prosecution of Charles, King of England (and …) on the 20th of January 1649, was led by John Cooke, for whom the trial was ‘not only against one tyrant but against tyranny itself’. “The charge stated that, having been ‘trusted with a limited power to govern by, and according to the laws of the land, and not otherwise’, Charles had engaged in ‘a wicked design to erect and uphold in himself an unlimited and tyrannical power to rule according to his Will, and to overthrow the Rights and Liberties of the People. He had levied war against Parliament and the people it represented, had solicited foreign invasions and renewed the war, all to uphold his own interests and those of his family, against the ‘public interests, common right, liberty, justice and peace of the people of this nation. Thus, Charles was a ‘Tyrant, Traitor and Murderer, and a public and implacable Enemy to the Commonwealth of England.”

‘Then the clerk rose and read out the sentence ….’that the said Charles Stuart, as a Tyrant, Traitor, Murderer and a public enemy, shall be put to death ….’

‘… this was a court that swept away the ‘distinction of quality’, making ‘the greatest lord and the meanest peasant undergo the same judicatory and form of trial’ as each other.’

(p. 253, The Blazing World…’, Jonathan Healey, 2023.)

During the last two months or so, three statements deeply affecting economic policy have come out from the highest authorities in the land: the Supreme Court heard a petition from several citizens regarding the infringement of their fundamental rights by actions or lack thereof on the part of some of the of highest public officers of state and convicted all of them of the alleged infringements; a former president of the republic who also held the portfolio of finance in his governments declared triumphantly that he had reduced taxes year after year from 2010; the Governor of the Central Bank delivered a lecture in the University of Colombo on ‘Inflation- public enemy number one’. All three statements contain elements central to economic policy and more immediately to the present economic crises. Unfortunately, there has been no public discussion of these statements, except on television. In general, the anchors of these programmes on television have not been persons with learning and professional experience in economic policymaking. Nor did they give evidence of being familiar with current writings on economics or economic policy. These observations are truer of the daily newspapers (Sinhala and English) that I read. I lack the energy to discuss these questions adequately. I invite those better equipped to take them up in earnest.

Inflation/stagnating economy

The Governor of the Central Bank, speaking from his high chair, may see inflation as public enemy number one. The Central Bank operates at the short end of the capital market (money market) to keep prices, including the price of other currencies, reasonably stable and the banking system functioning well. In this small economy, keeping the banking system stable has turned out to be unusually difficult. Enterprises have no way of raising long-term capital in the absence of a functioning share market, long-term lending institutions or personal funds pooled together for the purpose. Prior to the introduction of the principle of limited liability (Laws were enacted in Britain in 1844), wealthy persons pooled their resources and ran large-scale operations (East India Company). But railways, telephone systems, later shipping companies and oil companies, became far too large to be financed and managed in that manner. Last century, as individual inventors came out with innovations that would become the foundation of large enterprises bringing in huge revenues in a short while but were highly risky, a new source of capital emerged: venture capital. In our economy, some of the richest people cannot openly invest their funds because their wealth has been accumulated in breach of the law. Even before black money came to darken the prospects for the development of a capital market, the skies were gloomy.

The rollover of short-term loans and advances from commercial banks has been a long-term feature of the way firms (except plantation companies which sold their shares in the London Stock Exchange) satisfied their long-term capital needs. (I vaguely recollect that N Ramachandran of the Central Bank wrote a paper on this in the 1960s.) When the market for their output collapses, borrowers cannot service their short-term loans and seek another roll over, the banking system becomes unstable. When banks quite properly prosecute errant borrowers in court, the owners go on television to blame the banks and the government. Relatively large companies finance their activities by withholding taxes payable to the government. The unpaid taxes, running into several hundred million rupees, become interest-free long-term loans from the government (taxpayers) to those enterprises. Recourse to law is an essential part of how economies function. The Central Bank cannot lend to banks to extend credit to enterprises. Solutions must be sought elsewhere.

It is difficult enough to project prices for 12 months and central bankers who predict prices for five years (Recall the 2007-2008 market crash.) must be bonkers. Central banks have instruments to intervene in the short-term market to stabilize the economy. Managing the public debt and the employees’ provident funds is none of its legitimate business, though acts of Parliament may make it legal. The Central Bank has no instruments to promote economic growth and development. But it can ruin the march to economic progress by messing up the short-term functioning of markets. Yet, the long run in which economic growth takes place is not a succession of short runs for the policymaker. The Central Bank had better dwell on the short end.

My understanding is that the public enemy number one in this economy is its stagnation. Look at the results of government policies and the behaviour of ‘absent entrepreneurs. After all, in this country, the government sector has rarely exceeded 30 percent of the total economy. If the economy has not grown, the heavier responsibility lies with private sector entrepreneurs. A newspaper publisher, owners of a few passenger transport companies, branches of a few multinational companies and a few retailers did not make an indigenous capitalist class.

In elementary terms, economies function with labour and capital. Economies grow when the employment of labour and capital increases. [(Those familiar with the economic history of England may recall trends after the Black Death (latter half of the 14th century) there.)] Labour is a complex input as capital is. A taxi driver is not the same input as a designer of a motor vehicle; a data entry clerk is not the same provider of labour as a designer of a robot. A spade, a capital good, is very different from a fast computer, another capital good. A combined harvester is very different from a woman with a scythe in Minneriya, though both may engage in agricultural operations. Economic growth takes place when labour and capital grow and when workers become highly productive with the use of advanced capital. Look at what has happened in Sri Lanka. From about 1960 to 2000, Sri Lanka has had a gift of a youthful population as China has had from somewhat later and as India and most of Africa still have. They have used that ‘population dividend’ to grow rapidly. In addition, Sri Lanka has had a healthy, literate young population. About a quarter of that potential work force has emigrated. Highly skilled workers among them flew away periodically, as they do now. The consequence has been that a healthy, literate and skilled labour force has been gifted to the workforce of other countries. The gross domestic output of the UAE, Greece, South Korea and the United Kingdom have grown faster and that of Sri Lanka has stagnated.

If your concern were with the gross domestic output of the world that is fine but if your concern were with the GDP of Sri Lanka, these movements of population created problems. With gross mismanagement of the economy, they sum to crises. The estimate of the Statistics Department that the unemployment rate in Sri Lanka is 4%, (giving statistics a bad name) hides the reality that 20% of the labour force (labour force comes from demography and work force from economics.) left the country to join the workforce of other countries. A more realistic number would be that 25% of the labour force was unemployed and that 20% of the labour force emigrated, leaving 4% of the work force unemployed in this country. By the middle of the 1960s, South Korea was as poor as we were and its rising labour force faced unemployment. (Recall the ‘Saemaul Undong’ movement). Now, it is a regular importer of unemployed educated young labour from this country. Two factors were responsible for this divergence. There was no class of entrepreneurs who sought new technology and large and expanding markets overseas. And we were governed by a class of people who excelled in plundering the public wealth rather than promoting economic growth. Individuals and families that rose from rags to riches in one generation were those who plundered the public purse, in diverse ways, rather than innovating entrepreneurs. These are public enemies number one in this society. (Thomas Stockton was not; Peter Stockman was an enemy of society. [Henrik Ibsen].)

Government expenditure without taxation

It was shocking that a former President and Finance Minister, in a press statement a few days back, triumphantly declared that he had reduced taxation from 2010 to 2014. Indeed, he was not the only Finance Minister in the country who betrayed its interests by failing to raise tax revenue to pay for rising government expenditure. Anyone interested in the figures can easily access them in the Annual Reports of the Central Bank. If you raise government expenditure and reduce government revenue, you drive your society to a crisis. When that economy is one highly dependent on imports, even for its mere survival, and a government fails to implement policies that promote exports and there are no enterprises that earn foreign exchange, there is a balance of payments crisis. Hence the economic crises that we suffer from. The choke points were designed by government policymakers and ‘absent entrepreneurs. They are public enemies of this society.

Convict convictions

In November, the Supreme Court distinguished itself by convicting seven people, who, several citizens had petitioned the court, had violated their fundamental rights. (It is useful to remember that the court comprised not merely the judges but also counsel who were officers of the court.) Many had come to believe that several of the respondents in that case were above the law. The Supreme Court, to our delight, gave life to Dr. Thomas Fuller’s 1753 dictum that ‘Be ye never so high, the Law is above you’.

However, that ennobling decision gave rise to a conundrum, entirely outside the court and solely in my mind. Economics is not physics; economists’ attitudes to policy vary with the culture in which they grew up, where they were schooled (‘freshwater schools’ or ‘saltwater’ schools in the US) and what history they had read. An Englishman who had read about Hitler’s atrocities in Germany may have a predilection to dislike ‘etatism’. An economist who grew up in Peradeniya from about 1957 to about 1970, had a good chance of disapproving neo-liberalist economic policies. IMF policies from about 1990 were associated with neo-liberal economics, the Washington Consensus. To construct a hypothetical case: if an economist who disapproves of IMF policies happens to be in a place of high responsibility for economic policymaking, he/she faces a dilemma. A wise choice is to refuse to seek appointment to such a position. But men/women are ambitious. There is a responsibility falling on those who appoint him/her to make sure that the prospective appointee is vetted for his/her attitudes to pending centrally important questions so as to avoid creating a dilemma for the appointed person and an embarrassment for the government. The appointee has a second choice: resign from his /her position when he /she learns of the imminent dilemma. If, however, a person continues to remain in that high position, and those with the authority fail to remove him from office, it is fair to assume that those who appointed him concurred with the appointee’s approach to policies. And, indeed, it may be that such confluence of attitudes, determined that that particular person was appointed. Does his conduct amount to behaviour that denies fundamental rights of other citizens? If it does, what happens to his fundamental right to live by his convictions? He is not crying ‘fire’ in a crowded theatre. God exists; God exists not. Is such a citizen an enemy of the people? Cannot a citizen live by his convictions but be convicted?

Crude oil is the lifeblood of the global industrial economy, yet the journey from a subterranean reservoir to a litre of petrol at the forecourt involves a cascade of physical transformations, commercial transactions, and fiscal interventions that profoundly shape who bears the cost, and how much. A sudden shift in the world market price of crude, whether triggered by OPEC+ supply discipline, geopolitical disruption, or a demand shock, does not translate uniformly into consumer prices across the globe. The consequences are systematically different, depending on a country’s tax policy, exchange rate, efficiencies in refining processes, distribution processes and dependence on energy imports.

Crude oil is the lifeblood of the global industrial economy, yet the journey from a subterranean reservoir to a litre of petrol at the forecourt involves a cascade of physical transformations, commercial transactions, and fiscal interventions that profoundly shape who bears the cost, and how much. A sudden shift in the world market price of crude, whether triggered by OPEC+ supply discipline, geopolitical disruption, or a demand shock, does not translate uniformly into consumer prices across the globe. The consequences are systematically different, depending on a country’s tax policy, exchange rate, efficiencies in refining processes, distribution processes and dependence on energy imports.

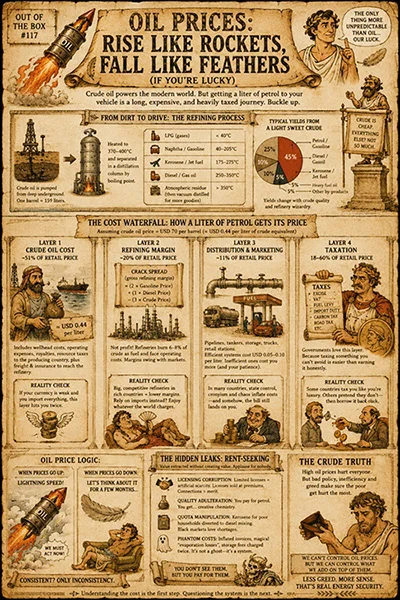

The Refining Process: From Crude to Finished Products

Crude oil is a naturally occurring mixture of hydrocarbons and its chemical composition varies by field: Heavy sour crudes from Venezuela, or Saudi Arabia, require additional processing, raising refining costs by USD 2–5 per barrel. One standard barrel contains approximately 159 litres.

Crude oil is preheated to approximately 370–400°C and the operating principle exploits differences in boiling points. The resulting fractions, collected from top to bottom, include: light petroleum gases (LPG) boiling below 40°C; naphtha and gasoline fractions in the 40–205°C range; kerosene and jet fuel between 175°C and 275°C; diesel and gas oil from 250°C to 350°C; and atmospheric residue above 350°C which is then processed in a vacuum distillation unit to recover further distillates, including lubricating oil base stocks.

Primary distillation alone is insufficient to meet market demand. Gasoline demand far exceeds the natural yield of the distillation cut. A modern complex refinery achieves the following approximate product yields from a light sweet crude: petrol/gasoline ~45%; diesel/gasoil ~25%; kerosene/jet fuel ~10%; LPG ~5%; heavy fuel oil ~10%; and other by-products ~5%. These ratios shift with crude quality and refinery configuration, and response differently to crude price changes.

The Crude Truth: How Oil Prices Punish the Poor Twice

An accounting perspective reveals a waterfall of costs, each layer added by a distinct economic actor and subject to a distinct set of market forces and regulatory interventions. A companion of the approximate cost structure for a litre of petrol at the retail level, assuming a crude oil price of USD 70 per barrel (approximately USD 0.44 per litre of crude equivalent), between advanced and emerging economies, can be explained in four layers:

Layer 1 — Crude Oil Cost (~51% of Retail Price)

The foundation of every fuel product is the crude oil acquisition cost. At USD 70/barrel, the raw material cost embedded in one litre of refined petrol is approximately USD 0.44. This figure includes wellhead lifting costs, field operating expenses, royalties, and sovereign resource taxes paid to the producing country, as well as freight and insurance for ocean tanker shipment.

For emerging economies, without domestic refining capacity, or with currencies that are not freely convertible, this layer is doubly exposed: a crude price increase is compounded by any simultaneous depreciation of the local currency.

Layer 2 — Refining Margin (~20% of Retail Price)

The gross refining margin, measured by the industry’s standard 3-2-1 crack spread;

The gross refining margin, measured by the industry’s standard 3-2-1 crack spread;

Crack Spread (gross refining margin) = (2×Gasoline Price) + (1×Diesel Price) − (3×Crude Price)

Critically, this gross figure must not be confused with profit. A refinery typically uses 6–8% of its own crude input as process fuel, and significant variable operating costs. This gross refining margin, the difference between the value of products produced and the cost of crude, varies considerably with market conditions.

In advanced economies with large, integrated refinery systems, these margins are moderated by competition and long-term supply contracts. In emerging economies, dependent on a single import refinery or on product imports rather than crude, refining costs are effectively set by the international product market, leaving little domestic control over this cost layer.

Layer 3 — Distribution and Marketing (~11% of Retail Price)

Refined products must travel from the refinery gate to the consumer through a distribution network involving primary pipelines or product tankers, regional storage terminals, secondary truck distribution, and retail fuel stations. In advanced economies, this infrastructure is mature, privately operated, and highly efficient, contributing a relatively stable USD 0.05–0.10 per litre to the retail price. In many emerging economies, the distribution infrastructure is fragmented, underdeveloped, or state-controlled, introducing additional costs, quality inconsistencies, and opportunities for rent-seeking. In Sri Lanka, for instance, the state-owned Ceylon Petroleum Corporation has historically cross-subsidised distribution costs, masking the true economic cost until subsidy withdrawal forced rapid price adjustments in 2022.

Rent-Seeking is extracting value without creating value; essentially corruption and inefficiency

Licensing corruption:Limited fuel station licenses create artificial scarcity; Licenses sold/traded at premiums; Political connections needed to obtain licenses

Quality adulteration: Consumers pay for “petrol” but get lower-quality mix

Quota manipulation:Subsidised kerosene (meant for poor households) diverted to diesel mixing; Creates black markets during shortages

Phantom costs:

Layer 4 — Taxation (18–60% of Retail Price)

Taxation is the most variable, politically sensitive, and analytically important layer in the cost structure. In advanced economies a high tax bases serve a dual purpose: generating substantial fiscal revenue and acting as an automatic price stabiliser. When crude rises, the absolute tax component remains constant, so the percentage of the price attributable to crude increases less than proportionately at the retail level.

In contrast, emerging economies historically imposed low fuel taxes or active subsidies, particularly for diesel, LPG, and kerosene used by low-income households. Sri Lanka’s fuel tax component, prior to the 2022 crisis, was, they claim, effectively negative in real terms due to administered pricing below cost.

The Impact of a Crude Price Increase: Advanced vs. Emerging Economies

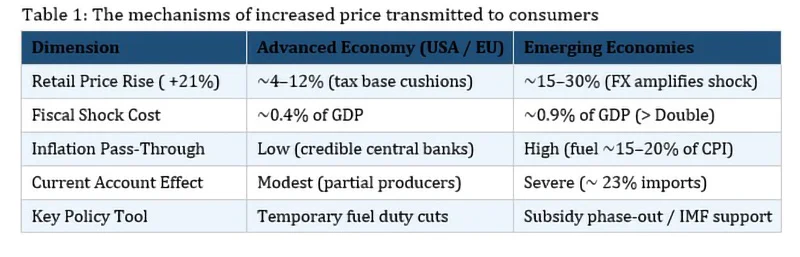

For example, if crude oil rises from USD 70 to USD 85 per barrel, an increase of approximately 21.4%. The mechanisms by which this shock is transmitted to consumers, and the capacity of economies to absorb or redistribute it, diverge dramatically along the advanced/emerging economy divide (Table 1).

Absorb shocks through tax relief

Advanced economies possess well-established fiscal frameworks that enable them to absorb temporary commodity shocks through tax relief, targeted transfers, or direct subsidies without compromising fiscal sustainability. Research by the Center for Global Development (2026) estimates the median fiscal cost of shielding consumers from the crude price increase of USD 15 scenario at approximately manageable cost of 0.4% of GDP for advanced economies.

Emerging economies face median fiscal costs of approximately 0.9% of GDP — effectively double. For Sri Lanka, entering the 2022 energy crisis with near-zero foreign reserves, even a temporary subsidy was fiscally impossible, forcing an immediate and politically destabilising pass-through of the full price increase to consumers. The lesson is stark: the ability to smooth out a commodity price shock across time is itself a function of prior fiscal strength, making the poor more vulnerable precisely because their governments are already under strain.

Inflation Pass-Through and Monetary Policy Credibility

The second transmission mechanism operates through the consumer price index and central bank behaviour. In advanced economies, fuel typically represents 3–5% of the CPI basket, and central banks enjoy high credibility in anchoring inflation expectations.

In emerging economies, fuel and food together often constitute 40–60% of CPI baskets, and central banks have historically struggled to maintain credible inflation targets. A 21% crude price increase translates into a far larger initial CPI shock. Worse, the loss of inflation credibility means that workers and businesses adjust wages and prices preemptively, generating persistent second-round inflation (> Double). To defend its inflation target, the emerging economy central bank must raise interest rates aggressively, simultaneously raising the cost of borrowing for businesses and governments, a painful policy dilemma in an economy already under stress.

Structural Current Account Vulnerability

The third and perhaps most structurally significant difference lies in the current account and foreign exchange dynamics. The advanced economies hold large reserve currencies and deep financial markets that allow them to finance import cost increases without immediate exchange rate pressure.

Sri Lanka, by contrast, allocated approximately 23% of its total import bill to petroleum products. A USD 15/barrel price increase instantly widens the current account deficit of these economies, depleting foreign exchange reserves. As reserves fall, currency markets anticipate further depreciation, precipitating speculative selling of the domestic currency. The resulting exchange rate depreciation, potentially 5–15% in a shock scenario, multiplies the cost of crude imports in local currency terms. A 21% USD price increase thus becomes a 28–39% local currency price increase at the refinery gate, before any refining, distribution, or tax component is added. This vicious cycle; crude price rise → reserve depletion → currency depreciation → amplified import cost → further reserve depletion, is a hallmark of emerging economy energy crises, and Sri Lanka’s 2022 experience illustrated it in extreme form.

Double bind when crude rises and subsidised

Countries that have historically subsidised fuel face a double bind when crude rises: the subsidy bill expands sharply (as the gap between subsidised price and market cost widens), while fiscal space contracts. The International Monetary Fund has consistently recommended subsidy reform, allowing fuel prices to reflect market cost while protecting the poor through direct cash transfers, as the fiscally sustainable path. Sri Lanka’s forced price liberalisation in 2022 (under IMF programme conditions) illustrate both the political difficulty and the macroeconomic necessity of this adjustment.

The Asymmetry of Oil Price Responses: Advanced vs. Emerging Economies

Advanced economies enjoy bidirectional flexibility in responding to oil price volatility; prices rise and fall with crude markets, leaving fiscal positions largely neutral. Emerging economies, by contrast, face a structural trap: when crude rises, subsidy bills explode, draining public finances; when crude falls, governments retain windfall savings to offset accumulated deficits rather than passing relief to consumers. Sri Lanka’s cycle from collapse to liberalisation to renewed subsidies illustrates this vividly. Underlying this is a political economy ratchet, price hikes are unavoidable, but reductions are politically captured, making permanent reform structurally elusive.

(The writer, a senior Chartered

Accountant and professional banker,

is a professor at SLIIT, Malabe. Views expressed in this article are personal.)

Life keeps throwing hurdles in his way, but Eshan Malinga keeps vaulting over them. Take his February from hell. For several months, Malinga had been building up to his first ever World Cup, a dream for pretty much anyone who ever picks up a cricket ball. But a week before that World Cup, Malinga dislocated his non bowling shoulder while bowling, which the team’s medical staff have since described as a freak injury they had never seen before.

“I was devastated,” Malinga says. “On top of it being my first World Cup, it was also at home and I didn’t know when I would get that chance again. There were a few days there where I did absolutely nothing.”

And yet in mid-May, here he is grinning from atop a pile of 16 IPL wickets, having developed a serious reputation as a reverse-swing operator. Sunrisers Hyderabad’s explosive batters may have seized the spotlight in this frenetic IPL, but on the bowling front, no SRH bowler has neared Malinga’s wicket haul, which is fifth best in the season overall. In a year in which they have not had Pat Cummins for seven of their 11 matches, it is Malinga who has held down the fort, particularly in the second half of the innings.

But trading difficulty for success is just what Malinga does. What he has long been doing. Go back eight years and Malinga had never played a hard-ball cricket match. On top of which his home district of Ratnapura – at the base of Sri Lanka’s central hills – was better known for its gems and waterfalls than cricket, never having produced a men’s international. Malinga, additionally, was not even actively trying to be a cricketer. He had moved from his first school in a village called Opanayake to Ratnapura’s Sivali Central College due to strong academic results, and found, almost by accident, that his new school had a hard-ball cricket team.

But what Malinga knew at that point was that he could bowl fast. That much had been obvious growing up in Opanayaka, where despite his mother’s occasional misgivings, Malinga was highly sought after by the organisers of the village softball team (Sri Lanka has a thriving village-level softball cricket ecosystem). And as had been the case with the better-known Malinga, this one was also aware he possessed a killer yorker – a prized asset in every form of cricket, with any kind of ball.

If he’d been on track to be a softball legend, Malinga found his horizons began to expand at a spectacular rate the moment he got a hard ball in his hands. First, his yorker and his pace began to reap big wickets in the Division Three schools competition for Sivali Central, whose coach had immediately hoisted him into the team upon seeing Malinga bowl at practice one day. Then in mid-2019, about a year into playing hard-ball cricket, came the day he still reflects on as the one that changed his cricketing life. Having missed a fast-bowling competition in Ratnapura because he had been playing for his school that day, Malinga travelled to the hill town of Badulla to bowl in the competition there, and clocked 127kph on the gun, which was enough to win him first place.

This was when he first became a blip, however faint and distant, on Sri Lanka Cricket’s radar. Visions of a cricketing life began to appear as wisps of opportunity began to materialise. The next few years, Covid-riddled though they were, became a crash course into the sport for Malinga. There were coaching camps in Colombo in which the best of the rural talent was trained up and funnelled into a programme at the next level up. There were trials for first-class teams, and eventually a fledgling domestic career.

“I don’t know how many times I came to Colombo from Ratnapura during those times,” he laughs now. “It was a lot! I would leave home at about 3am, and the bus journey to Colombo took about three-and-a-half hours. Then I’d train or play the match, and the bus back home always took longer because of traffic. So every day, I was on the road for more than seven hours.”

The Malinga who made these exhausting daily commutes was, as far as the Sri Lankan cricket system was concerned, a bowler of decent rather than blinding promise. His pace had propelled him to the top of the regional pool, but at the first-class level he was still adapting his yorker and slower ball (another weapon he had developed in his softball days). If he needed another gear, Malinga found it – again almost by accident – sometime in 2022.

“I was playing an Under-23 three-day tournament, and I remember that being the first time I really started reverse-swinging the ball,” he says. “Coaches had anyway told me that with my action and my pace, it should be possible. But it started almost automatically. It’s not something I had to learn.

“But it wasn’t that easy, because it was a long process to learn how to control it. To get reverse swing, you have to release the ball at a different point than a straight ball, because you want it to still hit the stumps when it is swinging. So I scuffed up a lot of balls and trained hard to get that line right.”

And so, the Malinga that emerged at the end of 2022 had sharp enough pace, an excellent yorker, a developing slower ball, mountains of homespun tenacity, and had also discovered that he can naturally reverse-swing the ball earlier in an innings than most. You could have seen where this is going, right? All the ingredients of an ace white-ball bowler were there. And Malinga was already a master of turning wisps of opportunities into tangible advances. Over the next three years, he’d land a spot in the national fast-bowling academy, use that as a trampoline to impress in an Emerging Teams three-dayer against Bangladesh, and from there bounce into a stint at the MRF Pace Academy in 2024, before on the franchise side of things parlaying a trial at Rajasthan Royals at Kumar Sangakkara’s invitation into a decent run at the SA20 for Paarl Royals.

Having leapt up to the fringes of the Sri Lanka team over the past 18 months, Malinga has at this IPL now seized another unusual chance. The square at SRH’s home stadium is among the barest and most abrasive in the league, and Malinga’s reverse swing has prospered upon it. Of his 16 wickets this season, 11 have come at home. In the second half of the innings, when the ball is most likely to reverse, Malinga’s economy rate is 8.37 at a venue where runs have been scored at 9.38 in that period this season.

Malinga had put in a robust 2025 season for SRH as well, so there is a body of work emerging there. Perhaps this is why this year, SRH’s bowling plans have tended to follow the contours of Malinga’s own game.

“After six overs the ball gets damaged here, so we needed to make use of that. When I bowled at practice, the ball reversed, so I think a plan emerged where we were going to use the scuffed up ball and take advantage of that.

“In the first powerplay the ball comes on to the bat nicely here. After that we try to get the advantage of having an older ball. We’ve got bowlers who bowl 140kph-plus, and we have Pat Cummins, who also reverses the ball. So we make sure to look after the ball in a way that will give us reverse.”

At 25, eight years into a serious cricket career, Malinga sees himself as a work in progress. He wants to work on his powerplay bowling. His variations, he thinks, still need some work. He’d like to play Tests, where his reverse swing could really stretch its legs. And, oh, he is still waiting to play that first World Cup.

Even here, his keen nose for opportunity leads him. He points out through the course of our conversation that where the three previous World Cups had been played with a new ball at either end being used right through the innings, the next World Cup, in 2027, will feature rules that seem at least partially designed to enhance reverse swing, an older ball more suited to the craft now available towards the end of the innings.

He isn’t even a sure-fire pick in Sri Lanka’s ODI XI just yet, so this is just a flicker of an opportunity for now. But having made the journey from the village of Opanayaka to the most raucous cricketing showpiece on the planet, Malinga knows just what to do with those.

[Cricinfo]

The death of the most important suspect in the Sri Lankan Airlines Airbus deal has drawn intense public speculation. Kapila Chandrasena the former CEO of the heavily loss-making national airline was found dead under circumstances that the police are still investigating.

He had recently been arrested by the Commission to Investigate Allegations of Bribery or Corruption in connection with the controversial Airbus aircraft purchase agreement signed in 2013. Police investigations are continuing into the cause of death and whether or not he committed suicide. The unresolved death brings to light the high stakes involved in accountability efforts of this nature.

The uncertainty surrounding Chandrasena’s death has revived public memories of other mysterious deaths linked to corruption investigations and public scandals. Among them is the death of Rajeewa Jayaweera, a former SriLankan Airlines executive and outspoken critic of the Airbus transaction. He was following in the tradition of his father, the late foreign service officer and public servant Stanley Jayaweera who mentored the younger generation in good governance practices and formed the group “Avadhi Lanka” along with icons such as Prof Siri Hettige. Rajeewa had written a series of articles exposing irregularities in the deal before he was found dead near Independence Square in Colombo in 2020. The CCTV cameras in that high security area were turned off. Questions raised at that time whether or not he had committed suicide were not satisfactorily resolved.

The controversy about the cause of Chandrasena’s death is diverting attention away from the massive damage done to the country by the SriLankan Airlines deal itself. The value of the aircraft agreement was close to the size of the International Monetary Fund bailout package that Sri Lanka desperately needed by 2023 in order to stabilise the economy after bankruptcy. Sri Lanka’s IMF Extended Fund Facility amounted to about USD 3 billion spread over four years. The comparison shows the scale of the losses and liabilities that irresponsible and corrupt decisions have imposed on the country and which must never happen again.

Wider Pattern

The corruption linked to the Airbus transaction came fully into the open only because of investigations conducted outside Sri Lanka. In 2020 Airbus agreed to pay record penalties of more than EUR 3.6 billion to authorities in Britain, France and the United States to settle global corruption investigations. Sri Lanka was identified as one of the countries where bribes had allegedly been paid in order to secure contracts. The Airbus deal involved the purchase of six A330 aircraft and four A350 aircraft valued at approximately USD 2.3 billion. Investigations showed that Airbus paid bribes amounting to nearly USD 16 million in order to secure the contract. According to court submissions, at least part of this money amounting to USD 2 million was transferred through a shell company registered in Brunei and routed through Singapore bank accounts linked to the late airline CEO and his wife.

The commissions involved in this deal may seem comparatively small compared to the overall value of the contracts but devastating in their consequences. But they also show that a few million dollars paid secretly to decision makers could lead to the country assuming liabilities worth hundreds of millions or even billions of dollars over decades. This is why corruption is not simply a moral issue. It is a direct economic assault on the living standards of ordinary people. Money lost through corruption is money unavailable for schools, hospitals, rural development and job creation. In the end the burden falls on ordinary citizens who are left to repay debts incurred in their name without receiving commensurate benefits in return.

The SriLankan Airlines transaction gives an indication of the wider pattern of corruption and misuse of national resources that has taken place over many years. This was not an isolated incident. There were numerous large scale infrastructure and procurement projects that imposed heavy debts on the country while enriching politically connected individuals and their associates. Other projects such as the Colombo Port City, Hambantota Harbour and highway construction reveal a similar pattern.

Less publicised but equally damaging scandals have involved fertiliser medicine and energy contracts. Investigations into medicine procurement in recent years uncovered allegations that substandard pharmaceuticals had been imported at inflated prices causing both financial losses and risks to public health.

Moral Renewal

The present government appears determined to investigate major corruption cases in a manner that no previous government has attempted. Those who ransacked and bankrupted the treasury need to be dealt with according to the law. There is considerable public support for efforts to recover stolen assets and ensure accountability.

In his May Day speech President Anura Kumara Dissanayake stated that around 14 corruption cases were nearing completion in the courts this very month and called upon the public to applaud when verdicts are delivered. Political opponents of the government claim that such comments could place pressure on the judiciary and blur the separation between political leadership and the courts. But the deeper public frustration that underlies the president’s remarks also needs to be understood.

The challenge facing Sri Lanka is twofold. The country must ensure that justice is done through due process and independent institutions. If anti corruption campaigns become politicised they can lose legitimacy. But if corruption and abuse of power continue without consequences the country will remain trapped in a cycle of economic decline and moral decay. Sri Lanka also needs to confront past abuses linked to the war period. There are allegations of kidnapping, extortion, disappearances and criminal activity in which members of the security forces have been implicated. Vulnerable sections of the population suffered greatly during those years. If political leaders turned a blind eye or actively connived in such crimes they too need to be held accountable under the law. Selective justice will not heal the country. Accountability must apply across the board regardless of political position, ethnicity or institutional power.

Sri Lanka has paid a very heavy price for corruption and impunity. The economic collapse of 2022 did not occur overnight. It was the result of years of bad governance, reckless decision making, abuse of power and the misuse of public wealth. If the country is to move forward the focus cannot be diverted by sensational speculation alone. Suspicious deaths and political intrigue may dominate headlines for a few days. But the larger issue is the system that enabled corruption to flourish without accountability for so long. The real national task is to end that system. Sri Lanka cannot build a prosperous future on a foundation of corruption and impunity. Unless those who looted public wealth are held accountable and the systems that enabled them are dismantled, the country risks repeating the same cycle again.

Jehan Perera

Gujarat Titans go No.1 after Rabada and Holder rout Sunrisers Hyderabad

Showers will occur in the Western, Sabaragamuwa, Central, North-western and Northern provinces and in Anuradhapura, Trincomalee, Galle and Matara districts

Ex-SriLankan CEO’s death: Controversy surrounds execution of bail bond

Law applies to all, regardless of power or influence – Prez

Sri Lanka and Belarus to sign several MoUs

Compensation paymentsto voluntary retirees in power sector to begin soon

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News7 days ago

News7 days agoMIT expert warns of catastrophic consequences of USD 2.5 mn Treasury heist

-

News4 days ago

News4 days agoLanka Port City officials to meet investors in Dubai

-

Editorial7 days ago

Editorial7 days agoClean Sri Lanka and dirty politics

-

News5 days ago

News5 days agoSLPP expresses concern over death of former SriLankan CEO

-

Editorial6 days ago

Editorial6 days agoThe Vijay factor

-

News12 hours ago

News12 hours agoEx-SriLankan CEO’s death: Controversy surrounds execution of bail bond

-

News5 days ago

News5 days agoPolice inform Fort Magistrate’s Court of finding ex-CEO of SriLankan dead under suspicious circumstances

-

Features6 days ago

Features6 days agoPalm leaf manuscripts of Sri Lanka – 1