Features

The permeance of global debt

Lanka will subsist on a diet of perpetual debt

by Kumar David

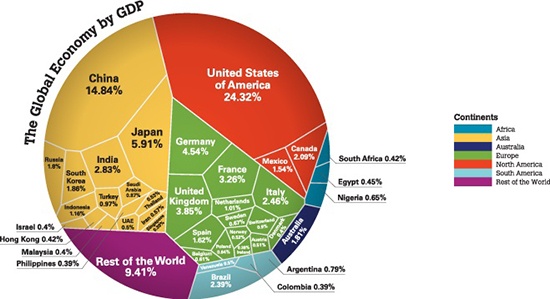

The thesis of this essay, conveyed within my 1,700 word-mandate, is that the world economy has entered a phase of near universal debt. Lanka’s inexorable overload of domestic and foreign debt is part our own making part footnote of the global story. Everywhere, mighty USA and European Union included, the state is mired in debt that will not vanish so long as Finance Capital (FC) rules the world. The surpluses created by economic activity are amassed by a few institutions and individuals. Thomas Piketty drew attention to inequity of wealth and income. The market capitalisation of the world’s largest 2,000 companies is $100 trillion, but the value of all the property (land, houses, other fixed assets) of the poorer 50% of the world’s population is just $10 trillion. The heft of bank balance sheets, private-equity, mutual and hedge funds, pension & social welfare coffers, sovereign wealth funds and holdings of personal wealth, leave one dumb struck by their magnitude. FC rules the world.

Recently, post the 2009 recession, Central Banks including especially the Fed in the US expanded money supply not by billions but by trillions. Governments issued bonds, that is borrowed from FC’s (money-market) gigantic holdings to splurge on fiscal deficits or “sold” Treasury Bonds to Central Banks, which printed money (electronically) to “buy” on never-never terms. Debts to Central Banks will never be repaid, simply rolled over in perpetuity. Central Banks also ‘Quantitative-Eased’ hundreds of billions to banks and private funds to lubricate asset purchases (equities and property) which merely ballooned an asset price bubble and exacerbated wealth inequality. I don’t want to stud this piece with statistics which readers will find easily enough on the Internet and will limit myself to three numbers. The US national (government) debt of $26.5 trillion exceeded US GDP during 2020 and will not decline in the foreseeable future – in Japan it’s 230%. Second, global government debt is $60 trillion but global GDP in nominal (not PPP) terms is $75 trillion. The third point is that the total debt of non-financial corporations, globally, is about 95% of global GDP according to the IMF.

Recently, post the 2009 recession, Central Banks including especially the Fed in the US expanded money supply not by billions but by trillions. Governments issued bonds, that is borrowed from FC’s (money-market) gigantic holdings to splurge on fiscal deficits or “sold” Treasury Bonds to Central Banks, which printed money (electronically) to “buy” on never-never terms. Debts to Central Banks will never be repaid, simply rolled over in perpetuity. Central Banks also ‘Quantitative-Eased’ hundreds of billions to banks and private funds to lubricate asset purchases (equities and property) which merely ballooned an asset price bubble and exacerbated wealth inequality. I don’t want to stud this piece with statistics which readers will find easily enough on the Internet and will limit myself to three numbers. The US national (government) debt of $26.5 trillion exceeded US GDP during 2020 and will not decline in the foreseeable future – in Japan it’s 230%. Second, global government debt is $60 trillion but global GDP in nominal (not PPP) terms is $75 trillion. The third point is that the total debt of non-financial corporations, globally, is about 95% of global GDP according to the IMF.

A nominal currency (not PPP) comparison

This essay is intended for my non-specialist readers and the data gives a broad idea of magnitudes and distributions. It is not easy to gauge indebtedness of financial institutions as reliable data is hard to come by. And it is meaningless to tot up household debt globally because $1,000 has a different meaning for say the denizens of the USA as against an Indian or an Indonesian. The idea I would like you to take away is not only that States and Corporations are deeply mired in debt, but more important things will get worse not better in the 2020s decade. This is commonplace in countries where productivity is low and which will never export enough to cover imports plus investment for capital projects plus surpluses to accommodate graft for the political classes. But I put basket cases to a side to deal with chronic diseases of the mighty. I cannot within the confines of this essay deal with the US, the EU and China, the big three whose capital shapes the world, and I have to limit this essay mainly to the US

Classical Keynesianism held that when demand and employment were low and economic activity in decline, the state should intervene and prime the pump with monetary and fiscal injections. ‘Monetary’ means to hold interest rates down and lend (print) to would-be investors; fiscal stimulus is big spending by governments to build infrastructure and create employment. Roosevelt’s New Deal helped but it was really WW2 (capitalism loves wars, armaments production and sales) that did the trick. In theory, economic revival should allow the government to recoup its outlay via higher taxes and duties. The “Keynesian multiplier” was said to be greater than one. It worked in the glorious boom from 1945-1970 when capitalism shone and socialist ideas were put away in a dog-box. But Keynes-Thought lost its shine after the oil-shocks of the 1970s and welfare capitalism slumped into Stagflation – economic growth was stuck in the mud; high inflation could not be reduced and high unemployment persisted. The world did not learn a lesson and turn against capitalism. On the contrary, there came neo-liberalism; Regan, Thatcher, Pinochet and JR slashing welfare, smashing trade unions, privatising and swinging political philosophy to the far right. Except Pinochet, mostly within the bounds of democracy unlike ultra-right populism today.

The gurus of neo-liberalism like Heinrich Hayek, Robert Barro and Robert Lucas, theorised that the Keynesian-multiplier was less than one. Barro father of the now discredited ‘rational expectations theory’ said that if the state spent more, people will realise that higher taxes were on the way and would spend less, erasing the hoped for increase in demand. Nothing of the sort is happening today; reality has stood ‘rational expectations’ on its head. The US housing market is rising because of low interest rates (interest rates are negative in Japan). Consumer spending remains undamped without engendering inflation because the US consumer is tapping into a global, mainly Asian, dirt cheap by US prices, one-billion worker labour-market churning out goodies for pampered North American and European consumers. Inflation in the Eurozone is negative; Japan is in perpetual deflation. Fifteen dollars per hour! An Asian or south of the US-border worker will be lucky to take home $15 (LKR 2800) a day. What Barro and his ilk failed to take into account was much-integrated global goods, services and labour markets. US inflation stays stubbornly low because producers for the US market de facto pay minimal wages to their producers (workers). In any case governments and Central Banks can’t stimulate the economy in perpetuity, you can’t defy gravity forever.

The gurus of neo-liberalism like Heinrich Hayek, Robert Barro and Robert Lucas, theorised that the Keynesian-multiplier was less than one. Barro father of the now discredited ‘rational expectations theory’ said that if the state spent more, people will realise that higher taxes were on the way and would spend less, erasing the hoped for increase in demand. Nothing of the sort is happening today; reality has stood ‘rational expectations’ on its head. The US housing market is rising because of low interest rates (interest rates are negative in Japan). Consumer spending remains undamped without engendering inflation because the US consumer is tapping into a global, mainly Asian, dirt cheap by US prices, one-billion worker labour-market churning out goodies for pampered North American and European consumers. Inflation in the Eurozone is negative; Japan is in perpetual deflation. Fifteen dollars per hour! An Asian or south of the US-border worker will be lucky to take home $15 (LKR 2800) a day. What Barro and his ilk failed to take into account was much-integrated global goods, services and labour markets. US inflation stays stubbornly low because producers for the US market de facto pay minimal wages to their producers (workers). In any case governments and Central Banks can’t stimulate the economy in perpetuity, you can’t defy gravity forever.

Demand is slack in advanced countries because the one percent rich can only splurge that much on consumer goods and prefer to invest in assets, and secondly production companies are risk-averse in the face of Asian competition hence domestic investment in manufacturing remains weak. The pre-COVID picture was bleak since state revenue was slack in the rich world due to slow growth, and it was falling in the US thanks to Trump’s tax handouts to the rich. Post-COVID expenditure has risen even further due to large expenses on medical and subsistence grants and unemployment payments. Hence pressure for trillion-dollar stimulus packages. The end point is that substantial fiscal deficits have become a permanent feature. In the US for example the fiscal deficit for 2020 and 2021 taken together will be three to five trillion dollars. There is no way out except to borrow-print-hold interest rates low or negative, and live with debt for eternity. Eurozone stimulus will be hundreds of billions per years for many more years. This nexus of extra-loose monetary policy and unescapable fiscal deficit blurs the divide between monetary and fiscal policy; they merge. Government borrowing without constraint has got a new name, Modern Monetary Theory (MMT). Adherents of MMT dismiss concerns that excess borrowing will induce inflation or will bring countries to the brink of an abyss. They have no fear that if interest rates go up governments will have to default or that the financial system will die in convulsions.

I need to repeat the thesis that underpins my essay before moving on: The world economy has entered a period of universal debt – government, corporate and household. I now need to say a few words about high-finance in China; I am avoiding the term finance-capital (FC) when dealing with China because how financial interactions will unfold in the context of a state-led economy cannot be foreseen yet.

High-finance is moving into China on a not insignificant scale. I am on tenuous ground, but I make a ball-park guess that about 10% of global high-finance is networked with China – add 5% to 10% if Hong Kong is included. True, New York, London, Tokyo and Frankfurt dominate bank, investment-fund and equity-market capital. High-finance however is on the move; asset managers (BlackRock and Vanguard), giant investment banks (JP Morgan Chase) and others are setting up shop in China (HSBC is already there), and Ant Group’s Hong Kong stock market launch later this year will be the largest ever IPO, eclipsing Saudi oil giant Aramco’s recent listing. Let us imagine that global high-finance has a quarter of its roots in the PRC by 2030. Remember that China took over as manufacturing workshop of the world in 20 years from 1980 to 2000; finance is a great deal more fluid than industry.

High-finance will be affected if the reach of China’s financial sector becomes even half as big as its global manufacturing. Some of the influences that will underpin change in the decade of the 2020s are easy to discern. The stranglehold of the US dollar as world reserve currency and mechanism of payment will need to be broken. Within five years an alternative global payments system and a currency based on two or three of the following, gold, yuan, yen, Euro and US$, will need to be initiated. (The US is the only country that can run eternal deficits, print mountains of money and export its economic problems because the world remains hungry for dollars till the value of the dollar declines). Second, the world needs other payments mechanism to overcome the US stranglehold known as sanctions – Cuba, Iran, Hong Kong, China, Venezuela, Turkey and Russia are among affected countries. Third, Belt & Road expenditure will be facilitated by an alternative global currency and banking and payments mechanisms.

A few words about Lanka before I sign off. The merging of monetary and fiscal policy is already advanced. Prof Lakshman’s task is to stay on the phone borrowing from whoever will lend and burning the midnight oil ensuring that the printing presses keep rolling. We are familiar with Lanka’s Central Bank borrowing billions again and again from China, India, the IMF or money-markets to repay China, India, the IMF or money-markets, again and again! Debt keeps growing as interest compounds while capital indebtedness persists. The balance of payments will remain in the red if not forever, for the foreseeable future. I don’t know it can be reversed both because governments need to survive politically and there is no big-enough feasible economic strategy. I am certain China, India, Japan and the US will not let us sink on the balance of payments issue since none of them wants a chaotic and anarchic country in this geographic location. For this reason I do not see sudden collapse but slow irreversible decline.

This essay has turned into heavy reading; I feel sorry for myself. No one pays attention to well researched stuff that is not simple to skim and digest. Anything on the Sinhala-Tamil brawl or derogatory of persons, regimes or regime-opponents draws stampeding crowds. Oh well, what to do!

Beyond Stabilisation:

“Development is not about where you are today, but where you can be tomorrow if you make the right investments today.” – Lee Kuan Yew

The first part of this article yesterday (18) asked what growth model Sri Lanka should pursue.

The second seeks to show how to achieve it; how much investment is needed; where it should go, and how progress should be measured. It should move decisively from economic philosophy to economic architecture or from Economic Diagnosis to Economic Engineering.

Introduction: The Missing Growth Blueprint

Sri Lanka’s economic debate has reached an important turning point.

For three years, policymakers, economists, international institutions, and business leaders have focused primarily on stabilization. Inflation has been controlled, foreign reserves have improved, debt restructuring has progressed, and government revenue has increased significantly.

These achievements were necessary. But they are not sufficient.

The question facing Sri Lanka today is no longer whether the economy can be stabilized. The more important question is whether the country can transform itself into a dynamic, investment-driven, export-oriented economy capable of achieving sustained growth of 7% by 2029.

This requires moving from economic diagnosis to economic engineering.

Engineering demands numbers, targets, institutions, timelines, and accountability.

The challenge is therefore straightforward:

What investment strategy can lift Sri Lanka from a 3-4% growth path to a 7% growth path by 2029?

How Much Investment Is Needed To Reach 7% Growth?

Economic growth does not occur by declaration. It requires investment.

Historically, countries that achieved sustained growth rates above 6% maintained investment levels of approximately 30-35% of GDP. Sri Lanka currently invests considerably less (i.e., 27%) than this benchmark.

Assuming Sri Lanka’s real economy (currently US$88 billion) reaches approximately US$100 billion by 2029, total annual investment requirements could exceed US$30 billion. Given current investment levels, the country may need an additional US$8-10 billion annually in productive investment by the end of the decade. This investment cannot come solely from government spending.

A realistic financing framework could include:

· Domestic private investment – 40%

· Foreign direct investment – 30%

· Public infrastructure investment – 20%

· Development finance and PPPs – 10%

The real policy challenge is not simply attracting more investment.

It is attracting the right investment.

Which Sectors Can Generate 7% Growth?

Sri Lanka cannot achieve 7% growth through tourism alone, nor through agriculture alone.

Growth must be diversified across several strategic sectors.

Export Manufacturing & import substitution such as Green Energy (2.0 percentage points)

Manufacturing should become the largest contributor to future growth.

Priority sectors include:

· Electronics assembly

· Medical devices

· Rubber-based products

· Engineering components

· Boat building

· Food processing

Integration into Asian production networks could dramatically expand manufacturing exports.

Information Technology And Knowledge Services (1.0 percentage point)

Sri Lanka already possesses strong human capital advantages.

The country can expand:

· Software development

· Artificial intelligence applications

· Business process outsourcing

· Financial technology services

· Professional consulting exports

· Tourism And Hospitality (1.0 percentage point)

The objective should be quality rather than quantity.

Higher-value tourism can generate greater foreign exchange earnings without excessive environmental pressure.

Logistics And Maritime Services (1.0 percentage point)

Sri Lanka’s geographical location remains one of its greatest assets.

Port development, shipping services, logistics hubs, and regional distribution centres could create a powerful growth engine.

Agriculture And Dairy Modernisation (0.5 percentage point)

Modern agriculture should focus on productivity rather than acreage expansion.

Dairy development alone could reduce imports while increasing rural incomes.

Innovation And Entrepreneurship (0.5 percentage point)

A stronger startup ecosystem (i.e, Entrepreneurs and innovators, Investors and venture capital funds, Banks and financial institutions, Universities and research centers , Government agencies and policies, Business incubators and accelerators, Legal, accounting, and consulting services) could become a significant source of future growth and employment.

Collectively, these sectors could generate the foundations for a 7% growth trajectory.

Why RCEP Could Add One To Two Percentage Points To Growth

One of the most under-discussed opportunities in Sri Lanka’s economic future is regional integration. The Regional Comprehensive Economic Partnership (RCEP) encompasses some of the world’s fastest-growing economies and production networks. The success stories of Vietnam, Malaysia, and Thailand demonstrate that participation in regional value chains often matters more than domestic market size.

RCEP membership or deep integration could generate benefits through:

Greater Market Access

Sri Lankan exporters would gain improved access to rapidly expanding Asian markets.

Increased Foreign Direct Investment

Investors frequently prefer locations connected to large trade agreements.

Technology Transfer

Regional production networks facilitate knowledge diffusion and technology acquisition.

Supply Chain Participation

Sri Lanka could specialise in selected components, services, and logistics activities rather than atte

mpting complete industrial self-sufficiency.

The strategic significance of RCEP extends far beyond trade.

It represents a gateway into the economic architecture of Asia.

The National Growth Dashboard 2026-2029

One weakness of Sri Lankan policymaking has been the absence of measurable national performance indicators.

A National Growth Dashboard should be publicly reported every quarter.

Growth Indicators

· GDP growth rate

· Per capita income growth

· Labour productivity growth

Investment Indicators

· Total investment as a percentage of GDP

· Foreign direct investment inflows

· Public infrastructure investment

Export Indicators

· Total exports

· High-value export share

· Export diversification index

Innovation Indicators

· Research expenditure

· Patents registered

· Startup creation

Human Capital Indicators

· Graduate employment rates

· Technical skills certification

· Labour force participation

Rural Development Indicators

· Agricultural productivity & Extensive cooperatives

· Dairy self-sufficiency ratio

· Rural household income

What gets measured gets managed. What is not measured is usually ignored.

Lessons from Singapore: Strategic Investment Targeting

Singapore never relied on chance.

It deliberately identified sectors capable of transforming the economy and directed institutions, incentives, infrastructure, and education towards those priorities.

The country’s Economic Development Board became one of the most successful investment agencies in the world.

The lesson for Sri Lanka is clear:

Investment promotion must become strategic rather than reactive.

The country should actively pursue investors in sectors aligned with national growth priorities.

Lessons from Vietnam, Ireland, South Korea, And New Zealand

Vietnam

Vietnam teaches the importance of export-oriented manufacturing and integration into regional value chains.

Ireland

Ireland demonstrates how education, foreign investment, and technology can transform a small economy into a global innovation hub.

South Korea

South Korea illustrates the power of long-term industrial policy, export discipline, and technological upgrading.

New Zealand

New Zealand provides lessons in agricultural productivity, governance quality, and value-added exports.

The common lesson from all four countries is simple:

Growth was planned, targeted, measured, and relentlessly pursued.

None relied on policy improvisation.

Why Sri Lanka Remains Trapped In Economic Diagnosis

Sri Lanka has no shortage of economic diagnoses.

For decades economists have identified:

· weak exports,

· low productivity,

· inadequate investment,

· poor innovation,

· Governance weaknesses.

The diagnosis has remained remarkably consistent.

Yet implementation has remained weak.

Three factors explain this.

First

Policy discontinuity across governments.

Second

A tendency to prioritise short-term political considerations over long-term economic strategy.

Third

The absence of a national consensus on the desired economic model.

Countries succeed when political parties compete over implementation.

Sri Lanka often debates fundamentals repeatedly without resolving them.

The Need For A National Economic Transformation Compact

Achieving 7% growth cannot be the responsibility of a single government.

It requires a national compact involving:

· Government

· Opposition

· Private sector

· Universities

· Trade unions

· Development partners

The objective should be a shared commitment to a growth strategy extending beyond electoral cycles.

Economic transformation requires consistency.

Investors place capital where policies are predictable and institutions are credible.

The greatest gift Sri Lanka can provide to investors is confidence in policy continuity.

Summary

Sri Lanka’s next challenge is not stabilisation but transformation.

To achieve sustained growth of 7% by 2029, the country may require an additional US$8-10 billion in productive investment annually.

Growth should be driven by six strategic sectors:

· Export manufacturing

· Information technology and knowledge services

· Tourism and hospitality

· Logistics and maritime services

· Agriculture and dairy modernisation

· Innovation and entrepreneurship

Regional integration through RCEP could add one to two percentage points to long-term growth by improving market access, attracting investment, and integrating Sri Lanka into Asian supply chains.

A National Growth Dashboard should monitor progress through measurable indicators and improve policy accountability. Most importantly, Sri Lanka must move beyond diagnosing economic problems and begin engineering practical solutions.

Conclusion

History will not judge Sri Lanka by how successfully it emerged from the crisis of 2022. History will judge whether the country used that crisis as a platform for transformation.

The choice facing Sri Lanka is stark.

One path leads to recurring cycles of stabilisation, modest growth, debt accumulation, and periodic crises. The other leads to investment-led growth, export expansion, technological upgrading, and deeper integration with Asia.

The difference between these two futures is not luck. It is strategy.

The time has come for Sri Lanka to stop asking why growth is insufficient and start designing the institutions, policies, and investments required to achieve it.

Economic diagnosis has served its purpose. The next chapter must be economic engineering. Only then can Sri Lanka transform recovery into prosperity and aspiration into achievement.

I believe this second article is potentially more important than the first because it introduces something largely missing from Sri Lanka’s policy discourse: a quantified growth framework linking investment → sectors → exports → RCEP integration → measurable outcomes. It shifts the debate from “what is wrong?” to “what exactly must be done, by whom, and by when?”—which is where genuine policy innovation begins.

*The writer, among many, served as the Special Advisor to the Office of the President of Namibia from 2006 to 2012 and was a Senior Consultant with the UNDP for 20 years. He was a Senior Economist with the Central Bank of Sri Lanka (1972-1993). He can be reached via asoka.seneviratne@gmail.com

by Prof. Asoka S. Seneviratne

Features

Maritime security cooperation with India – A strategic imperative for Sri Lanka’s sovereignty and progress

As a retired Senior Superintendent of Police with decades of experience in intelligence, counter-terrorism, and strategic security coordination, I have repeatedly seen how short-sighted decisions undermine long-term national resilience. The adage “penny wise, pound foolish” perfectly encapsulates Sri Lanka’s vulnerabilities exposed during the 2022 economic collapse. Austerity measures, delayed reforms, and isolationist tendencies conserved minor resources in the moment but inflicted catastrophic costs in stability, public trust, and security capacity. Today, as we consolidate recovery under the National People’s Power government, embracing deeper maritime security cooperation with India stands as a wise counter to such false economies, investing prudently now to safeguard our sovereignty, economy, and peace for generations.

The 2002 Norway-brokered Ceasefire Agreement (CFA) with the LTTE is now a closed chapter in our history. Formally abrogated by the government in 2008, it paved the way for the decisive military victory in 2009 that ended three decades of separatist terrorism. Its present status is one of hard-earned reflection: a reminder of the perils of fragile truces without genuine political will, but also of the enduring success of intelligence-led, whole-of-government strategies that delivered a unified Sri Lanka.

Post-2009, with no active internal armed conflict, our security focus has evolved to hybrid and transnational threats, drug trafficking, IUU fishing, arms smuggling, terrorist financing, and great-power manoeuvring in the Indian Ocean. The 2022 crisis, however, tested this peace. Fuel shortages, power blackouts, and protest strains diverted naval and police resources, highlighting how economic fragility directly erodes maritime domain awareness and operational readiness.

India’s role as the indispensable first responder during that crisis, extending nearly USD 4 billion in credit lines, currency swaps, and essential supplies, prevented total collapse and laid the groundwork for today’s elevated partnership. What began as economic solidarity has matured into structured defence cooperation.

The landmark April 2025 MoU on Defence Cooperation, signed during Prime Minister Narendra Modi’s visit to Colombo, represents a pivotal shift. This five-year framework, the first comprehensive bilateral defence pact in decades, building on the 1987 Indo-Sri Lanka Accord, institutionalizes training, equipment support, joint exercises, intelligence sharing, and maritime operations. It directly counters the “pound foolish” risks of under-investment that plagued our 2022 response.

Maritime security is the linchpin. Sri Lanka’s vast Exclusive Economic Zone (EEZ) and position astride critical sea lanes make it a natural hub, and a potential chokepoint, for regional stability. Threats like narcotics smuggling through porous sea routes, illegal fishing by foreign vessels, and potential infiltration demand robust monitoring. India has stepped up decisively: operationalising the Maritime Rescue Coordination Centre (MRCC) for the Sri Lanka Navy in 2024, supporting Indian aircraft surveillance from Trincomalee, and facilitating regular hydrographic surveys and ship visits. Annual exercises like SLINEX-2025 have enhanced naval interoperability, with joint patrols and drills reinforcing rule-based maritime order. Participation in the Colombo Security Conclave (CSC), alongside Maldives, Mauritius, Bangladesh, Seychelles, and others, extends this into practical multilateralism focused on Maritime Domain Awareness (MDA), counter-terrorism, cyber security, and disaster response.

From an intelligence practitioner’s lens, honed at the State Intelligence Service Counter Terrorism Desk and during high-profile event security for CHOGM and World Cups this cooperation amplifies our HUMINT and technical capabilities without sacrificing autonomy. Shared information through platforms like the Information Fusion Centre-Indian Ocean Region (IFC-IOR) closes gaps that economic crises widen. It echoes our LTTE defeat: proactive, collaborative disruption of threats before they escalate. Post-Easter Sunday 2019 lessons on inter-agency coordination find new expression in these bilateral mechanisms, reducing vulnerabilities to hybrid warfare, disinformation, and economic espionage.

Critics may invoke sovereignty concerns or past sensitivities, but pragmatism demands we reject penny-wise isolation. The 2025 MoU includes termination clauses for flexibility, ensuring decisions remain Colombo-driven. Diversification is key: balancing ties with India alongside China (via BRI projects), Japan (drones and hydrography), the US, UK, and Gulf partners prevents over-dependence while maximizing gains. The CSC framework exemplifies inclusive, non-exclusionary regionalism, precisely the model needed to navigate Indo-Pacific dynamics.

Economically, maritime security underpins recovery. Secure sea lanes boost tourism, fisheries, and trade, sectors devastated in 2022. Joint capacity building (over 1,200 annual training slots for Sri Lankan forces) and blue economy initiatives create jobs and resilience, averting future “pound foolish” collapses. In a climate-vulnerable nation, cooperation on sustainable fisheries and disaster response further mitigates risks.

Sri Lanka must assertively embrace and lead multilateral Indo-Pacific cooperation as the indispensable driver of its long-term progress, security, and sovereignty. The hard lessons of the 2022 crisis leave no room for hesitation: penny-wise short-termism must give way to pound-wise strategic vision. We should fully operationalize the India defence MoU through sustained joint and intelligence fusion, while elevating the Colombo Security Conclave into a robust, action-oriented Indo-Pacific platform for maritime domain awareness, counter-trafficking, cyber resilience, and humanitarian response.

Sri Lanka is uniquely positioned to play a bridging leadership role, convening island nations, advancing inclusive initiatives under frameworks like the Indo-Pacific Oceans Initiative, and fostering minilateral and multilateral ties that include India, the Quad partners, ASEAN, and other responsible actors, without compromising our traditional non-alignment.

Bipartisan political consensus on these pillars, insulated from electoral politics, is urgent and non-negotiable. Isolationism invites exploitation and repeats past failures; assertive multilateral leadership in the Indo-Pacific secures our sea lanes, rebuilds economic vitality, strengthens interfaith harmony, and honours the sacrifices that delivered victory over terrorism in 2009. By championing such cooperative architectures, Sri Lanka transforms its strategic geography from vulnerability into enduring strength. The moment demands bold action, our nation’s destiny, regional stability, and future generations require nothing less.

( 34 sources )

Mahil Dole, SSP (Retired), is fthe former Head of the Counter-Terrorism Division of the State Intelligence Service of Sri Lanka, and has served as Head of the Sri Lankan Delegation at three BIMSTEC Security Conferences. With over 40 years of experience in policing and intelligence, he writes on regional security, interfaith relations, and geopolitical strategy.

This opinion draws on public records and professional experience. The views expressed are personal.

By Mahil Dole

Superintendent of Police (Retd.) and Former Member,

Sri Lanka Wakfs Board (Served Additional Terms)

Colombo, June 2026

When Dudley Senanayake died in 1973, nearly 1.8 million people lined the streets of Colombo to say goodbye to their much-loved leader. In a country of 12 million, that was one in every seven persons. It wasn’t a state-mobilised crowd or a political rally. They were mostly farmers from the Dry Zone who worked on the lands he had irrigated, teachers who benefitted from his school expansion scheme, civil servants, traders, students—ordinary people who walked for hours just to stand in silence as his cortege passed.

They came because they had never seen him act like a ruler. He lived like one of them: refusing special queues, apologising for accidental bumps, paying for things himself, treating political opponents with respect. For many, it was the first time they had grieved a leader they had never met personally, but whose decency they trusted. His funeral became less about death and more about a public reaffirmation that integrity in politics was possible, and that the people had noticed it.

The reluctant heir

Dudley was born under an auspicious sign. His father, D. S. Senanayake was at a temple ceremony in Bothale, Mirigama, when the news came. The temple astrologer predicted a great future for the child. History proved him right, though not in the way most expected. Dudley’s greatness lay not in how much power he wielded, but in how little he clung to it.

Dudley left S. Thomas’ College, Mount. Lavinia, as its best all-round student—equally at home in classrooms, on the cricket field, the football pitch, on the rugby grounds and the athletic track. At Cambridge, he won a Blue in cricket and earned degrees in Natural Sciences and Law. He returned to practise law, and entered politics only because his father persuaded him to do so. Public life was not his ambition; it became his duty.

As Prime Minister four times, twice in the 1950s and twice in the 1960s; his signature is on the irrigation schemes and agricultural programmes that fed the Dry Zone. But those who met him remember something more: his humanity.

The man without pretension

The following information was shared by Dr. Karunasena Kodithuwakku and the late Rukman Senanayake during informal conversations.

When the Queen of England, Queen Elizabeth II and the British Parliament decided to confer a Knighthood (the title ‘sir’) on Hon Dudley Senanayake in the 1950’s and informed him accordingly, Dudley declined the Honour graciously, declaring “I prefer to be known as plain Dudley Senanayake like now, rather than as ‘Sir Dudley Senanayake.”

Dudley with JRJ

In Kandy during his third term, Dudley accidentally bumped into a senior government valuer in the corridor of Queen’s Hotel. Before the man could speak, Dudley apologised. Later that day at the YMBA foundation stone laying ceremony, officials joked that they expected a larger donation from him. He opened his cheque book, looked at it, and said, “Give me the cheque I gave. Rs. 250? That’s my brother’s signature. I don’t have even that much.”

He had his hair cut at a salon in Colpetty. When the head barber tried to move him ahead of the queue, Dudley said, “No, no, I will wait for my turn.”

A senior politician from Kegalle visited him urgently in 1965. The secretary told him to be at Woodlands before 7 a.m. When Dudley saw him, he invited him to breakfast. The man was overwhelmed. “I can’t believe how I am welcomed here,” he said. “At my former leader’s house, I’m not even allowed to sit on a low bench.”

Dudley was however careful to protect the dignity of the country that he represented. As Prime Minister, he received an invitation to the Royal Coronation of Queen Elizabeth II in 1953. After accepting the invitation with due honour, Dudley went to England and was staying in a hotel when a high official of the British government paid him an unexpected visit. This was to appraise him of a change in plans.

“Hon. Prime Minister, I’m sorry to inform you that a difficulty has arisen regarding providing you with a separate horse carriage as informed earlier. Would you please share a carriage with Hon. (so and so) of Africa and grace the occasion?” Dudley was very annoyed, and told the official “Please inform your government that I expect a separate horse carriage to be provided for me too, just like for all the other Leaders as promised. Otherwise, I would consider it an insult to my country and will return to my country immediately without attending the Royal event.” It is reported that the British government promptly complied with Dudley’s request.

Simplicity that disarmed everyone

Even as Prime Minister, Dudley refused the trappings of office. One day in 1965-70 he told his security not to follow him and drove his Triumph Coupe alone to Mirissa. He spent the day photographing the beach and drove back safely. The police kept watch from a distance. Another morning he set off for Nuwara Eliya for a round of golf, again asking his security officers to stay back. A few hours later they found him at Ramboda Pass, sitting on a culvert smoking his pipe, the radiator of his car boiling over. He was relieved to see them and asked them to take him for his game—in their vehicle.

Traffic police once chased a speeding car only to find the PM at the wheel, pipe in hand. On Galle Road, he spotted an old friend at a bus stop, stopped the official car, and said, “Hey, what are you doing here? Jump in!” He took the man to Woodlands for tea and snacks, then drove him to Fort Railway Station himself. The friend was a Tamil gentleman who had captained Royal when Dudley captained S. Thomas’. Titles meant nothing to him.

Dudley

His humour was self-deprecating. At an All Ceylon Agricultural Officers Association AGM, the president pleaded with him and Minister M.D. Banda to “breed and recruit” more officers for the five-year plan. Dudley replied, “You all know I am not capable of breeding humans. You’ll have to ask the Honourable Minister—he’s already produced seven children!” The hall erupted in laughter.

A leader remembered

The day after the 1970 election defeat, party members went to see him in their numbers. Our family too was amongst them. He came up to our mother and said softly, “I’m very sorry, Mrs. Banda.” Even in defeat, his first thought was for others, especially for people like M.D. Banda, who had never lost an election before.

Dudley drew crowds not with slogans, but with sincerity. He never asked people to lower themselves to meet him. He met them where they were. In an age of political theatre, he was simply, stubbornly, decent.

During the period 1965-1970, when Dudley was Prime Minister, the Opposition led by Madam Sirima Bandaranayake, made allegations against Robert Senanayake (Dudley’s brother) regarding certain Foreign Exchange issues in Parliament. Dudley got up and urged the Speaker to

a. Appoint a Parliamentary select committee to investigate the allegations against his brother.

b. Appoint a Member of Parliament from the Opposition as its Chairman

c. Appoint the majority of the Select Committee members also from the Opposition.

According to the findings of the Select Committee and as reported to Parliament later, Robert Senanayake was completely exonerated. The entire leadership of the Opposition apologised profusely to Dudley.

An important point about this episode is a statement made by Dudley himself in Parliament prior to appointing the Select Committee. He declared that if his brother was found guilty of having indulged in any malpractice by word or deed, he (Dudley) would forthwith resign as PM.

That is why Sri Lanka remembers him not as a politician, but as “the gentleman Prime Minister.”

On 19 June, the day of his birthday, it is heartening to remember that such leadership once walked amongst us.

(The writer is the late Minister M.D. Banda’s eldest son.)

By Gamini Leeniyagolla

Asia’s richest man Ambani announces what could be India’s biggest share sale

Educational equipment Provided to University Students through the President’s Fund

Fears for US-Iran deal as talks delayed by Israeli strikes on Lebanon

BCCI secretary hints at early start to IPL 2027

Cricket journalist and broadcast legend Qamar Ahmed dies aged 88

Stafanie Taylor, spinners help West Indies overcome Scotland threat

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoRelease of 2025 O/L results likely to be delayed

-

Sports5 days ago

Sports5 days agoTharanga set for high-profile javelin clash in Ostrava

-

Features6 days ago

Features6 days agoPolitics of protected species

-

News4 days ago

News4 days agoBeijing Capital Airlines to resume flights to Colombo signalling boost to tourism

-

News5 days ago

News5 days agoTheft of USD 2.5 mn from Treasury: CoPF accused of complicity in NPP cover-up

-

News7 days ago

News7 days agoCommonwealth lawyers urge Lanka to uphold rule of law

-

Opinion5 days ago

Opinion5 days agoDecoding Trump’s 12.5% “Forced Labor Tariff” on Sri Lanka

-

Features3 days ago

Features3 days agoKilling of Colombo’s ancient trees — a warning on UN’s World Desertification Day – 17 June