Business

Telco and banking leaders in strategic partnership to empower SMEs in Sri Lanka

In a landmark move to drive digital transformation for small and medium-sized enterprises (SMEs), Dialog Enterprise, the corporate ICT solutions arm of Dialog Axiata PLC., has signed a Memorandum of Understanding (MoU) with Commercial Bank of Ceylon PLC, GlobalLinker, and Databox Technologies, on “Commercial Bank LEAP GlobalLinker”, an innovative web solution designed to empower entrepreneurs through digital marketing and e-commerce.

Dialog Enterprise, the premier digital innovation catalyst across various enterprise scales, joins forces with Commercial Bank as the technology partner for their e-commerce platform, Commercial Bank LEAP GlobalLinker, mobilizing the digital marketing sphere of SMEs in Sri Lanka. Together with GlobalLinker, a B2B business networking platform with commerce capabilities to make SME’s business digitally discoverable, and Databox Technologies, the managed service provider that ensures seamless integration and technical support, the partnership aims to set a new standard in the digital marketplace for SMEs in Sri Lanka.

Through this initiative, digital marketing and e-commerce facilities would be provided, enabling entrepreneurs to create their own e-stores, connect with each other, and engage in buying and selling locally and internationally. This network hub is specifically designed to cater to the unique needs of SMEs, providing them with the tools and support necessary to thrive in the digital economy. By leveraging the reach of the GlobalLinker platform, the endeavour aims to empower SMEs already on the platform, as well as new entrants, with advanced communication and digital technologies to further enhance their business capabilities.

Expressing enthusiasm about the collaboration, Navin Pieris, Group Chief Officer of Dialog Enterprise, stated: “We are thrilled to partner with such innovative, dedicated, and like-minded companies, working towards a common cause. This solution is a testament to our commitment to driving digital transformation and providing SMEs with the technology they need to compete and succeed in today’s digital landscape.”

While Sivasubramaniam Ganeshan, Assistant General Manager Personal Banking III / SME of Commercial Bank of Ceylon PLC, echoed the same exclaiming that: “This partnership is a significant step forward in empowering small and medium entrepreneurs. By creating a comprehensive digital marketplace, we are not only providing business loans but also enabling a robust ecosystem where SMEs can flourish. We look forward to seeing the positive impact this collaboration will have on the entrepreneurial community.”

Under the terms of the MoU, Dialog Enterprise will leverage its technological expertise to support the platform’s infrastructure, while Commercial Bank will spearhead market creation and onboarding of entrepreneurs. Entrusted with e-store creation, GlobalLinker will ensure the platform’s development and technical robustness, and Databox Technologies will provide managed services, with payment gateway integration, and ongoing technical know-how.

This partnership marks a significant milestone in the digital transformation journey for SMEs, offering them a powerful, user-friendly platform to expand their reach and grow their businesses.(Dialog Enterprise)

Business

Sri Lanka’s 2.3% inflation is a useful macro indicator, but it acts as a veil, says analyst

Disconnect between national statistics and household sentiment illustrated

Although official data points to a stable headline inflation rate of 2.3%, an independent economic analyst told The Island Financial Review that the public should look beyond this single figure.

Speaking on condition of anonymity, the analyst said, “That 2.3% is a crucial macroeconomic indicator for policymakers, but for the average household, it acts more like a veil. It obscures the sharply different economic realities in different sectors of the economy and, consequently, in different people’s lives.”

“You see, the aggregate is an average, a blend of everything from falling transport costs to soaring medical bills. But no family buys the ‘average’ basket. Your personal inflation rate is dictated by your unique spending pattern, and right now, those patterns are creating winners and losers in a low-inflation environment.”

He illustrated this by taking three contrasting Sri Lankan households.

“Consider a retired couple: their budget is dominated by healthcare, which is inflating at 4.2%, and perhaps occasional treats at restaurants, up 4.0%. For them, the cost of living is rising nearly twice as fast as the headline suggests. That 2.3% figure is of poor comfort to them.”

“Conversely, take a young professional who commutes; they are a direct beneficiary of the 0.9% deflation in transport. Their major expenses – fuel and vehicle maintenance – are supposed to be getting cheaper. Even if education inflation is high, it doesn’t affect them. This individual might feel almost no pinch, experiencing a personal inflation rate of about 1%. The headline number overstates their hardship.”

The analyst expressed his deepest concern for the typical family. “This is where the veil is most dangerous,” he said. “A family with school-going children is hit from multiple sides: Education at 3.9%, daily groceries at 3.3%, and clothing at 3.6%. The slight relief from cheaper transport is negligible against these heavy, non-negotiable expenses. Their budget is being squeezed relentlessly, a pressure the calm 2.3% aggregate completely masks.”

The analyst concluded that this sectoral divergence explains the disconnect between national statistics and household sentiment.

“When people hear ‘inflation is low and stable,’ but feel their wallet straining, it’s not ignorance. It’s because their personal basket is heavy with the sectors that are heating up – essential services, education, and food. The 2.3% is a useful indicator for the economy at large, but it should not blind us to the fact that many families are experiencing a much harder personal financial reality. Lifting that veil is key to understanding the true cost of living.”

by Sanath Nanayakkare

SLYCAN Trust convenes key forum on loss and damage funding

As Sri Lanka seeks funds as a climate-vulnerable nation, SLYCAN Trust convened a High-Level Forum on Climate Finance and Climate-Related Extreme Events in Colombo on January 20, 2026. The forum focused on improving access to finance for recovery and resilience, particularly following the severe impacts of Cyclone Ditwah in late 2025.

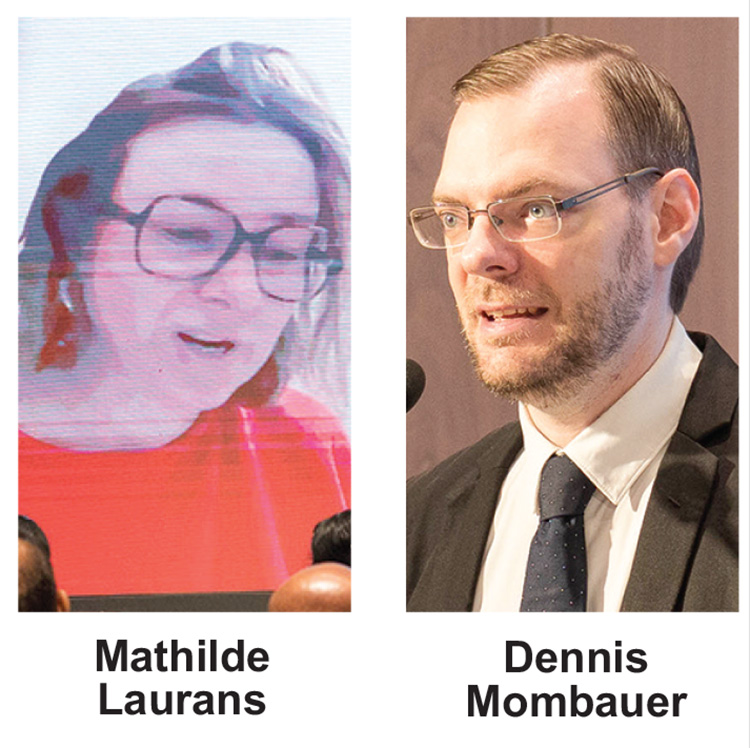

Dennis Mombauer, Director of Research and Knowledge Management at SLYCAN Trust, emphasised the urgency of building long-term resilience and addressing loss and damage.

“This Forum convenes key actors to identify pathways for accessing finance and managing climate risks,” he stated.

In a virtual keynote, Mathilde Laurans, Deputy Executive Director of the Fund for Responding to Loss and Damage (FRLD), announced that the fund opened its first call for proposals on December 15, 2025, with submissions accepted until June 15, 2026. “This milestone means that countries like Sri Lanka can now engage with us for support,” she said.

K.K.A. Chamani Kumarasinghe, Additional Director at Sri Lanka’s Climate Change Secretariat, highlighted the extensive damage caused by Cyclone Ditwah and stressed the need to strengthen response systems. She commended SLYCAN Trust for creating platforms that connect global climate processes with national priorities.

The forum included panel discussions with representatives from international climate finance institutions and technical experts, focusing on practical steps to enhance Sri Lanka’s climate resilience and improve local-level access to finance.

In the mist-veiled heart of Sri Lanka’s hill country, where Ella has earned global recognition as one of the island’s most photographed destinations, Browns Hotels & Resorts introduces a new chapter in experiential hospitality with Newburgh Ella – The Tea Factory Resort. Once a working tea factory, the century-old estate, originally established in 1903 by the legendary Scottish tea planter George Thomson, has been carefully transformed into a luxury resort, preserving its industrial character and historical soul while elevating it into an immersive experience. Set against dramatic mountain backdrops and defined by its iconic orange chimney, the resort commands world-famous views of the Ella Gap, framed by Ella Rock and Little Adam’s Peak — where landscape, legacy, and luxury converge.

On 30 January 2026, Newburgh Ella officially opened its doors to travellers from around the world with a ceremonial launch attended by Eksath Wijeratne, CEO of Browns Hotels & Resorts; Gangadaran Velsamy, General Manager of Newburgh Ella; Priyal Perera, Head of Projects and Procurement; Nishad Rajapakse, Manager – Engineering; along with key officials from Browns Hotels & Resorts. The event featured traditional regional performances and a ceremonial presentation of the first keycards to Newburgh Ella’s inaugural guests by the resort staff.

This unveiling marks the soft opening of Newburgh Ella, with the property currently progressing through its LEED and green certification processes. As part of its sustainability journey, the resort operates on a fully paperless concept, with digital check-in and digital menu systems in place, reinforcing Browns Hotels & Resorts’ commitment to responsible and future-ready hospitality.

Located on the Ella–Passara main road, near the Nine Arch Bridge and Pekoe Trail, Newburgh Ella features 41 thoughtfully designed rooms, categorised as Silver, Gold, and Bronze — inspired by the hierarchy of tea tips. The resort includes special family rooms, exquisite suites, and full wheelchair accessibility, offering inclusivity without compromise. Guests can witness sunrises and sunsets unfold directly from their rooms, framed by emerald vistas, connecting them to the rhythm of the hills.

Dining at Newburgh Ella celebrates the estate’s relationship with tea, land, and craft. 1903 – The Dining Room offers all-day dining with local and international flavours. Eastern Valley, an open-air restaurant, presents Pan-Asian cuisine, while Three Tips, the tea lounge, invites guests to savour the estate’s finest teas. The resort’s bar, George Thomson – The Founder’s Tavern, features specially curated beverage menus inspired by the region, reflecting the warmth of Browns hospitality. Together, these experiences offer the luxury of tea factory living, blending heritage, craft, and modern comfort.

Beyond its spaces, guests can explore Ella through curated experiences — from estate walks and visits to Ravana and Diyaluma Falls to scenic railway journeys. SKY, the resort’s observation deck, offers breathtaking vistas over tea-carpeted valleys and the world-famous Ella Gap.

Commenting on the launch, Eksath Wijeratne, CEO of Browns Hotels & Resorts, said:

“Tea is one of Sri Lanka’s most powerful global stories, and with Newburgh Ella, we wanted to honour that legacy while creating an experience that goes beyond aesthetics. Guests can connect with the very process, the people, and the land that give Sri Lanka tea its global recognition. At the same time, this project supports the local community, with many former factory staff now part of the resort team, ensuring heritage, sustainability, and hospitality thrive together.”

With the unveiling of Newburgh Ella – The Tea Factory Resort, Browns Hotels & Resorts continues to expand its portfolio of story-led destinations across Sri Lanka, inviting travelers to experience tea country differently — where the finest grade of tea meets the finest grade of stay, steeped in history, character, and heart.

-

- A Gold Tip Room at Newburgh Ella with a private balcony

-

- Eksath Wijerathne, Chief Executive Officer with Priyal Perera, Head of Projects and Procurement with Gangadaran Welasamy unveiling the property signage for Newburgh Ella

-

- Eksath Wijerathne, Chief Exceutive Officer of Browns Hotels and Resorts addressing the gathering

-

- An aerial view of Newburgh Ella – The Tea Factory Resort set against the hills of Ella

-

- A Silver Tip Room with the iconic Orange Chimney and the scenic Ella Gap in the background

Our focus is on economic stability through fiscal discipline, sustainable debt management, and reforms that enhance productivity and growth – PM

Spotless England meet unbeaten Australia in Under-19 World Cup semi-final

Kamindu in, Dhananjaya out as Sri Lanka flip-flop with T20 World Cup selection

China executes four more Myanmar mafia members

No decision yet on ICC meeting to discuss Pakistan boycott

Shoulder injury casts doubt over Eshan Malinga’s T20 World Cup

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Business5 days ago

Business5 days agoClimate risks, poverty, and recovery financing in focus at CEPA policy panel

-

Opinion4 days ago

Opinion4 days agoSri Lanka, the Stars,and statesmen

-

Business3 days ago

Business3 days agoHayleys Mobility ushering in a new era of premium sustainable mobility

-

Business3 days ago

Business3 days agoAdvice Lab unveils new 13,000+ sqft office, marking major expansion in financial services BPO to Australia

-

Business3 days ago

Business3 days agoArpico NextGen Mattress gains recognition for innovation

-

Business2 days ago

Business2 days agoAltair issues over 100+ title deeds post ownership change

-

Business2 days ago

Business2 days agoSri Lanka opens first country pavilion at London exhibition

-

Editorial3 days ago

Editorial3 days agoGovt. provoking TUs