Business

Is wealth tax the solution to Sri Lanka’s low tax revenue collection?

By Sathya Karunarathne

Successive governments have run fiscal deficits. Inadequate revenue collection and unrestrained government expenditure have worsened the country’s fiscal position.

Tax revenue which averaged over 20% of GDP in 1990 has declined to under 10% of GDP in 2020. Ad hoc tax policy changes have significantly eroded the tax base. Weak tax administration has also contributed to the sharp decline in tax collection.

While tax revenue has contracted, government expenditure has ballooned over time. Today, government revenue is not sufficient even to meet its expenditure on salaries and wages and transfers and subsidies to households which include pension payments and social welfare payments such as Samurdhi.

In this context, there are various proposals put forward to raise government revenue. One proposal is the reintroduction of the wealth tax.

A wealth tax is expected to bridge the gap between the rich and the poor, achieving equality. This tax shifts the tax burden to affluent households, taxing an individual’s net wealth, which is the market value of total owned assets. Proponents of wealth taxation argue that this is a progressive system of taxation and is a more powerful tool in comparison to income, estate or corporate taxes as it addresses the issue of wealth concentration.

Moreover, a tax should ideally satisfy basic characteristics of taxation: it should not be distortionary; it should be fair, and it should not be difficult to collect.

The rationale for a wealth tax

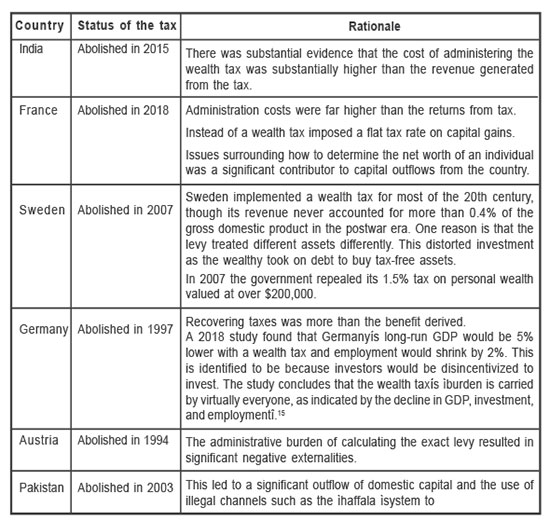

One of the earliest proponents of the wealth tax for developing countries was Nicholas Kaldor. Based on his recommendation, a wealth tax together with an income tax, expenditure tax and a gift tax were introduced in Sri Lanka in 1958.1 However, these new taxes yielded little revenue due to difficulties in determining the tax base and problems in administration. Following the recommendation of the Tax Commission in 1990,2 the government abolished the wealth tax from the year of assessment 1992/1993.3

Wealth taxes have mainly been implemented in European countries. In 1990, twelve countries in Europe had a wealth tax. Today, there are only three: Norway, Spain, and Switzerland. Several non-European countries have also imposed wealth taxes from time to time including such as Argentina, Bangladesh, Colombia, India, Indonesia, Pakistan

In recent times there has been renewed interest in wealth taxes. Presidential candidates in the US proposed various forms of a wealth tax. In the UK and France, there were proposals to impose “super taxes” on the rich. The primary justification was to address the increasing inequality in society.

Issues with a wealth tax

Despite renewed interest in the wealth tax as a progressive tax based on equity, it scores poorly on the criteria of efficiency, and administrative feasibility.4

Many factors have justified the repeal of wealth taxes in OECD countries. The reasons cited are related to efficiency costs, risk of capital flight particularly in light of increased capital mobility and wealthy taxpayers’ access to tax havens, failure to meet redistributive goals as a result of narrow tax bases, tax avoidance and evasion, high administrative and compliance costs compared to limited revenues (high cost yield ratio).5

To understand the efficiency costs of wealth taxes one can look at taxing a person’s wealth accumulated through savings. Despite the common consensus that taxing savings is an effective way to redistribute, a person’s saving decisions reveal little about their underlying lifetime resources and wellbeing. It only reveals their preference to consume tomorrow rather than today. Thereby a wealth tax imposes a tax on those who prefer to spend their money later as opposed to taxing the wealthy.6 Efficiency costs refer to the reduction of the welfare of the taxed individuals by more than $1 to generate $1 of revenue.7 Therefore, the efficiency cost of a wealth tax in terms of taxing savings is a reduction of future consumption that can be bought with earnings, reducing incentive to work for those who prefer to consume the proceeds later and reducing incentive for young people to save for their retirement.8

Capital flight is the possibility of holding assets outside of one’s resident country without declaring them.As wealth taxes are imposed on residents it increases the risk of the wealthy reallocating their assets to avoid taxation. Therefore a high tax burden encourages taxpayers to change their tax residence to a lower tax jurisdiction or tax havens.9

Both income-generating and non-income generating assets are taxed under wealth taxation. They can include land, real estate, bank accounts, investment funds, intellectual or industrial property rights, bonds, shares, and even jewellery, vehicles, art and antiques.10 However, this tax base for wealth taxes has often been narrowed through exemptions. These exemptions have been justified most commonly on the grounds of social concerns such as the negative social implications of taxing pension assets. Further liquidity issues (eg – farm assets), supporting entrepreneurship and investment (eg- business assets), avoiding valuation difficulties ( eg- artwork and jewellery) and preserving countries cultural heritage (eg – artwork and antiques) have also been cited as reasons for wealth tax reliefs. While some of these exemptions can be justified, they have led to the reduction of revenue raised from wealth taxes. They have also contributed to wealth taxes being less equitable as the wealthiest such as businesses benefit from these exemptions defeating the very purpose of imposing a wealth tax which is to meet its redistributive goals.11

Narrow tax bases in wealth taxation often leads to tax avoidance and evasion opportunities. For example, Spain’s 1994 wealth tax exemption for the shares of owner managers resulted in wealthy businesses reorganizing their activities to reap benefits of the exemption resulting in a significant erosion of the wealth tax base.12

Further, several other factors have also discouraged countries to sustain a wealth tax. They are namely, the difficulty in determining the tax base or what assets to be taxed, underreporting and undervaluation of assets, difficulty in measuring wealth taxes13, distinguishing between individuals who are asset rich but cash poor, the constant need to value assets and audit returns increasing administrative and enforcement costs .

Low revenue collection as well as the other reasons discussed have led to the abolishing of wealth taxes in most countries (See Table 1 for details) . Tax revenue from individual net wealth taxes in 2016 ranged from only 0.2% of GDP in Spain to 1.0% of GDP in Switzerland. Sri Lanka’s experience with wealth taxation was no different with the tax yielding low revenue as reported by the 1990 Tax Commission.14

Conclusion

Taxing the wealth of the rich to generate income and to eliminate economic inequality sounds promising in terms of political debate. However, wealth taxes have failed to generate adequate revenue, failed to meet redistributive goals as a result of narrow tax bases, proven to have high administrative and enforcement costs, resulted in tax evasion and avoidance due to underreporting and undervaluation of assets, increased the risk of capital flight and access to tax havens and may have contributed to the reduction of investment and employment.

Therefore, imposing a wealth tax may not be the ideal policy response to Sri Lanka’s low tax revenue, especially given the country’s previous experience with the tax yielding low revenue.

Sathya Karunarathne is the Research Analyst at the Advocata Institute and can be contacted at sathya@advocata.org. Learn more about Advocata’s work at www.advocata.org. The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

Sri Lanka’s first and largest coal-fired power complex at Norochcholai is staring at mounting financial losses running into millions of rupees as low-quality coal imports, rejected shipments and unusable stockpiles disrupt operations and expose deep flaws in coal procurement, power sector and environmental experts warned yesterday.

Energy sector sources told The Island Financial Review the economic damage has already begun, with rejected coal stocks, delayed payments and declining plant efficiency forcing the system to absorb losses from under-performance, additional handling costs and the risk of turning to more expensive backup generation.

Insiders estimate that continued reliance on sub-standard coal could result in tens of millions of rupees in losses per day, once reduced output, higher fuel burn and maintenance costs are factored in.

At the centre of the controversy is a recent coal shipment procured by the Lanka Coal Company (LCC), which has come under intense scrutiny after laboratory tests reportedly showed ash content of around 21%, far exceeding the 16% maximum allowed under tender conditions.

While parliamentary debate has focused narrowly on whether the coal meets the required calorific value, experts stress that excessive ash alone is sufficient grounds for outright rejection, regardless of calorific performance.

The situation worsened after coal stocks at the Norochcholai Coal-Fired Power Complex were recently rejected, leaving shipments in limbo and payments withheld. Power sector officials say this has resulted in logistical losses, demurrage risks and operational uncertainty, while existing low-quality coal stockpiles continue to deteriorate in storage.

“Coal that does not meet specifications is not just unusable — it becomes a financial liability, a senior electrical engineer said.

High-ash coal reduces boiler efficiency, increases fly ash generation and accelerates wear on ash handling systems, electrostatic precipitators and boilers — translating into higher maintenance costs and forced outages. Industry analysts warn that these hidden costs ultimately find their way into CEB losses or consumer tariffs.

Environmental Scientist Hemantha Withanage warned that accepting or burning such coal would push Norochcholai into a new environmental crisis, with serious consequences for communities in Norochcholai, Puttalam and surrounding areas.

“This is not just about calorific value. High ash coal means significantly more fly ash, Withanage told The Island Financial Review. “With low moisture and excessive ash, particulate matter spreads easily, contaminating air, soil and water. This is a massive ecological threat that will directly affect public health.”

He stressed that fly ash contains toxic heavy metals and fine particulates linked to respiratory illness and long-term environmental degradation. “If tender conditions are ignored, the cost will be paid by communities, not the suppliers, Withanage said.

Critics say the crisis exposes serious weaknesses in coal procurement oversight, with questions now being raised about supplier selection, quality verification and accountability. They argue that repeatedly importing low-quality coal — only to reject it or burn it at reduced efficiency — amounts to systemic mismanagement of public funds.

By Ifham Nizam

In a groundbreaking initiative, Insurance Regulatory Commission of Sri Lanka (IRCSL), announced an ambitious mission aimed at transforming the insurance industry into a cornerstone of national economic resilience and social stability.

To address this, the IRCSL will launch a nationwide education campaign titled “Insurance for All: For a Secure Future,” focusing on enhancing financial literacy across the country said Dr. Ajith Raveendra De Mel, the newly appointed Chairman IRCSL. Few sample events have already commenced last year in Matara, Jaffna and Kilinochchi that have set a strong precedent for future initiatives. “The positive response from participants highlighted the strong need for direct engagement and community-level awareness,” he said.

The IRCSL has also partnered with the Ministry of Education to integrate insurance literacy into the national curriculum, starting as early as Grade 5. This initiative aims to embed core concepts of risk management and financial protection, preparing students for future roles in the insurance industry. Complementing educational efforts, the IRCSL is also hosting an Inter-University Quiz Competition focused on insurance and financial literacy, aiming to engage university students and cultivate future thought leaders in the sector. Additionally, an e-Newsletter will keep stakeholders informed about industry updates and regulatory developments.

Dr. De Mel emphasized that this transformation it is not just about increasing insurance penetration, currently at a mere 1.1%, but about fostering a financially literate society where every citizen, family, and business is shielded from unforeseen risks. He said “Our mission is to cultivate a fully insured, financially literate, and future-ready society. The journey ahead involves profound regulatory, technological, and educational reform to create a modern, transparent, and robust regulatory environment that earns public trust while promoting innovation and sustainable growth in the industry.”

He pointed out the critical need for awareness, noting that many Sri Lankans perceive insurance as complex or exclusive to the wealthy. “We need to change how people think about insurance. Our goal is to make it simple, relatable, and accessible to everyone, particularly in rural and underserved communities,” he explained. The IRCSL will collaborate closely with the Insurance Association of Sri Lanka (IASL), the Sri Lanka Insurance Brokers Association (SLIBA), and the Sri Lanka Insurance Institute (SLII) to ensure that the message of financial preparedness reaches all corners of the nation. As Sri Lanka stands on the brink of an insurance transformation, Dr. De Mel’s vision promises a secure future driven by informed financial decisions and enhanced protection against life’s uncertainties.

The IRCSL is also focusing on digital transformation, enhancing operational excellence within the insurance sector. Key initiatives include establishing a Centralized Motor Insurance Database to improve transparency and efficiency in motor insurance, and advancing health insurance through digital integration, including standardized disease coding and electronic health records.

To ensure global competitiveness, the IRCSL is benchmarking against international best practices. A recent study tour to India has provided valuable insights into implementing risk-based supervision and capital frameworks, as well as developing accessible insurance products for underserved communities.

As the IRCSL approaches its 25th anniversary, it emphasizes the importance of staff development and alignment with other financial regulatory bodies to maintain high professional standards. The upcoming OECD/ADBI Roundtable on Insurance and Retirement Savings in Asia will further position Sri Lanka as a leader in insurance discussions, fostering regional collaboration and innovation.

by Claude Gunasekera

LAUGFS Life Sciences, in collaboration with the Medical Research Institute (MRI), Colombo, has launched Sri Lanka’s first-ever publicly driven allergy awareness wristbands, a groundbreaking initiative aimed at improving patient safety and preparedness in medical emergencies. The wristbands provide essential information about drug sensitivities, allowing healthcare professionals to respond quickly and effectively when time is critical.

The official handover ceremony featured distinguished medical experts, including Dr. Dhanushka Dassanayake, Consultant Immunologist and Head of the Department of Immunology – MRI, Dr. Rajiva De Silva, Senior Consultant Immunologist – MRI and Dr. Prabath Amerasinghe, Deputy Director – MRI, marking a historic milestone in patient care in the country.

Commenting on the initiative, Dr. Rajiv Perera, CEO of LAUGFS Life Sciences, said, we are proud to partner with the Medical Research Institute to launch Sri Lanka’s first-ever publicly driven allergy awareness wristbands. This initiative underscores our commitment to patient-centric healthcare by providing critical information that can save lives during emergencies. We believe that thoughtful collaborations like this can have a meaningful impact on patient safety, and we look forward to expanding the program to cover additional drugs and allergens, further advancing healthcare standards across the country.

Lanka Premier League draft set to take place on March 22

Trump to meet Venezuelan opposition leader Machado at the White House

Festival advance for government officers to be increased

Providing underutilized lands/properties to suitable investors for optimal utilization.

Implementation of the National Fisheries and Aquaculture Policy

Expressions of Interest called to develop selected locations within the Pelawatte Sugar Factory premises

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News3 days ago

News3 days agoSajith: Ashoka Chakra replaces Dharmachakra in Buddhism textbook

-

Business3 days ago

Business3 days agoDialog and UnionPay International Join Forces to Elevate Sri Lanka’s Digital Payment Landscape

-

Features3 days ago

Features3 days agoThe Paradox of Trump Power: Contested Authoritarian at Home, Uncontested Bully Abroad

-

Features3 days ago

Features3 days agoSubject:Whatever happened to (my) three million dollars?

-

News3 days ago

News3 days agoLevel I landslide early warnings issued to the Districts of Badulla, Kandy, Matale and Nuwara-Eliya extended

-

News3 days ago

News3 days agoNational Communication Programme for Child Health Promotion (SBCC) has been launched. – PM

-

News3 days ago

News3 days ago65 withdrawn cases re-filed by Govt, PM tells Parliament

-

Opinion5 days ago

Opinion5 days agoThe minstrel monk and Rafiki, the old mandrill in The Lion King – II