Features

Stock market dynamics: Fundamentals, Expectations and Perceptions

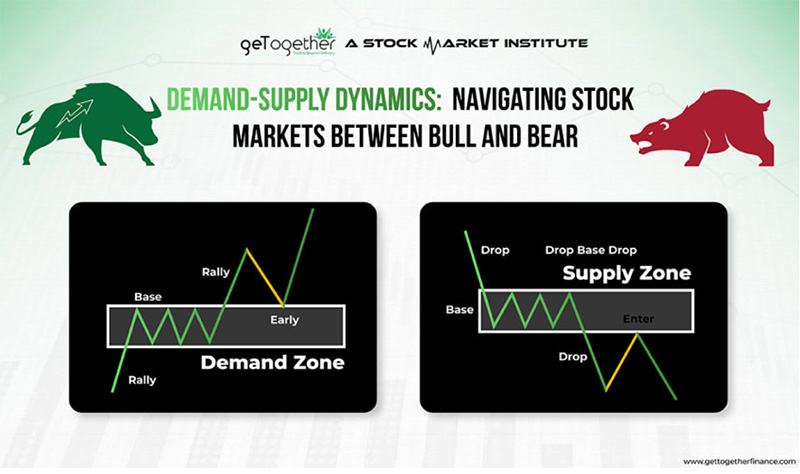

![]() The stock market serves as a nexus where millions of buyers and sellers converge to engage in transactions. At its core, each transaction represents an agreement between a buyer and a seller, with the central element being the price. This price is not static; it fluctuates continuously, reflecting the equilibrium between supply and demand.

The stock market serves as a nexus where millions of buyers and sellers converge to engage in transactions. At its core, each transaction represents an agreement between a buyer and a seller, with the central element being the price. This price is not static; it fluctuates continuously, reflecting the equilibrium between supply and demand.

The conventional belief posits that the interplay of supply and demand in the stock market is predominantly influenced by the fundamental factors inherent to individual companies. These factors encompass a range of critical aspects, including profitability, stability, future strategic plans, and the competency of management teams.

Consequently, share prices and index levels serve as barometers of the collective sentiment and expectations of market participants regarding the future trajectory of companies and the broader market. These prices are not mere numbers; rather, they represent a synthesis of myriad factors, including investors’ perceptions, assessments, and anticipations.

Expectations and perceptions

When buyers and sellers converge in the stock market, each transaction reflects not only the current value of a company but also the perceived future potential. As investors assess various factors, such as company performance, industry trends, economic indicators, and geopolitical events, they form expectations about how these factors will impact future earnings and growth prospects. And these perceptions often vary widely, reflecting diverse interpretations of available information and differing outlooks on the potential outcomes.

These perceptions are then manifested in the bids and asks that drive share prices and index levels. If investors anticipate robust growth and profitability for a company, they may bid up its share price, reflecting optimism and confidence in its future prospects. Conversely, perceived negative sentiment or concerns about the company’s outlook may lead to downward pressure on its share price.

Share prices and index levels, such as All Share Price Index (ASPI), serve as indicators of how investors collectively view the market. As they consider factors like the economy and global events, their expectations for future market performance are reflected in these measures. Essentially, they represent the combined opinions and outlooks of investors, incorporating both current information and future predictions. This consensus is always changing as new data emerges and sentiment shifts. Therefore, these indicators are not fixed but rather reflect ongoing discussions and reactions among market participants.

Long-term investing in the stock market entails placing perceived confidence in a company’s prospects over time. However, whether driven by past performance, societal concerns like climate change or political stability, or sheer speculative sentiment (short-term focused), buyers anticipate that share prices will increase.

However, these perceived expectations are not always realized, potentially prompting investors to become sellers. This decision, too, is often driven by the perception that anticipated prospects may not materialize as expected.

Future expectations serve as the linchpin for daily market activities, shaping the equilibrium of opinions on a company’s trajectory. Yet, share prices are not isolated from external influences; they reflect investors’ perceptions relative to the company’s performance and broader market sentiments. The pervasive fear of missing out often prompts investors to make impulsive decisions, chasing returns and disregarding rational assessments. However, smaller markets, like the Colombo Stock Exchange, have often been susceptible to manipulation by a select few prominent players, as noted by stock brokers, fund managers, and investment advisors.

When to enter the market

Interestingly, shares often rally ahead of economic upturns, creating a dissonance between market performance and day-to-day economic realities. Perception may paint a rosy picture, making investment decisions seem obvious in retrospect. However, market timing remains an arduous task, requiring foresight and conviction amid prevailing sentiments.

Learning from investment mistakes is pivotal for personal growth and financial success. Detaching ego from errors fosters introspection and prevents recurrence. Avoiding perception bias is imperative, as it distorts learnings of past decisions. Writing down experiences facilitates reflection and rational analysis, aiding in the development of effective investment strategies centered on disciplined processes.

Diversification; Risk management

Diversification, as advocated by Warren Buffett, offers protection against ignorance but remains a contentious subject. While concentrating investments in a single promising asset theoretically maximizes returns, it also heightens risks. Notably, founders or controlling shareholders wield informational advantages, contrasting with minority investors subject to regulatory disclosures. Hence, inherent risks accompany stock trading. The late Dr. Lalith Kotelawela, for instance, refrained from stock market involvement for himself and his companies, equating share trading with gambling.

Instances like Enron’s collapse underscore the multifaceted risks inherent in investing, from fraud to unforeseen macroeconomic upheavals. Diversification mitigates single-security risks, safeguarding portfolios against adverse events. However, ignoring diversification in pursuit of concentrated gains poses perilous consequences.

Overtrading, driven by short-term fixations and market noise, undermines long-term investment success. Emphasizing present circumstances overlooks the enduring impact of macroeconomic trends on market performance. Maintaining perspective and focusing on long-term fundamentals are crucial for navigating market volatilities and achieving sustainable growth.

Therefore, the stock market embodies the amalgamation of perceptions on expectations, sentiments, and uncertainties. Investors must recognize the transient nature of market dynamics, learning from past mistakes and adhering to disciplined investment strategies. While concentration may offer lucrative prospects, diversification remains a prudent risk management approach. Ultimately, maintaining a long-term perspective amidst short-term fluctuations is paramount for realizing enduring investment success.

Bear and Bull markets

The stock market, a bustling arena where investors and speculators converge, showcases a remarkable sensitivity to short-term stimuli. In pivotal market years, investors frequently succumb to timing mistakes, selling in the aftermath of bear markets and buying amid bull markets. Selling in bear markets and buying amid bull markets refers to a common behavioral pattern observed among investors.

During bear markets, characterized by declining stock prices and widespread pessimism, investors often feel compelled to sell their holdings out of fear of further losses. This behaviour is driven by a desire to mitigate losses and preserve capital. However, selling during bear markets can lead to missed opportunities for future gains, as markets often rebound after periods of decline.

Conversely, in bull markets, where stock prices are rising, investor perceptions tends to be optimistic, and confidence in the market is high. During these periods, investors are more inclined to buy stocks in anticipation of further price appreciation. This behaviour is driven by a fear of missing out on potential gains and a belief that the upward trend will continue. However, buying in bull markets can also be risky, as it may result in purchasing stocks at inflated prices.

Conclusions

Overall, the tendency to sell during bear markets and buy during bull markets can be attributed to emotional responses to market conditions, rather than rational decision-making based on fundamental analysis. As a result, investors may inadvertently buy high and sell low, thereby underperforming the market over the long term.

Furthermore, understanding the direct link between investment strategies and long-term goals is paramount. Properly defining goals enhances the alignment between assets and objectives, reinforcing the resilience of investment portfolios against short-term fluctuations.

Ultimately, gaining perspective on economic data and market movements is essential. While short-term fluctuations may induce anxiety, their significance in the grand scheme of long-term financial goals is often negligible. Just as recalling the minutiae of Central Bank actions from a decade ago holds little relevance today, current market gyrations are unlikely to alter the trajectory of well-defined investment strategies over the long term.

Finally, navigating the intricacies of the stock market demands a steadfast commitment to long-term investing principles. By transcending short-term noise and anchoring decisions on fundamental values and overarching goals, investors can weather market volatility and chart a course towards enduring financial success.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT University, Malabe. He is also the author of the “Doing Social Research and Publishing Results”, a Springer publication (Singapore), and “Samaja Gaveshakaya (in Sinhala). The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official policy or position of the institution he works for. He can be contacted at saliya.a@slit.lk and www.researcher.com)

Features

Old Politics returns via Writ Applications, New Politics emerges over Judicial Independence

by Rajan Philips ✍️

That warfare is a continuation of politics by other means has been an overused quote in Sri Lanka. In the present context, we might modify it to say that lawfare is also an extension of politics but by mostly the same means. The context for the current lawfare episode has been set up by the Writ Application filed by Retired Major General Suresh Sallay before the Court of Appeal, challenging his arrest and detention under the Prevention of Terrorism Act (PTA). He is a suspect in the renewed investigations of the 2019 Easter bombings, but has not been charged of any violation of the law. The burden of his writ application is that his arrest and detention under the PTA are unlawful and, therefore, he should be released.

A number of intervening writ applications have also ben filed before the Court both in support of and in opposition to Mr. Sallay’s application. The Court of Appeal has fixed a special date, August 4, to hear just the intervening petitions. With the exception of the petition filed Cardinal Malcolm Ranjith opposing Mr. Sallay’s application, all the other petitions I believe are in support of the application. Cardinal Ranjith’s petition is asking for the dismissal of Mr. Sallay’s writ application, for allowing that would “impede the ongoing Criminal Investigation Department (CID) investigations into the 2019 Easter Sunday bomb attacks.”

Those filing in support of Mr. Sallay include prominent figures in the country’s debates over nationalism and constitutionalism. A common theme in their petitions is that while they are not against any ‘lawful investigation’, they are sufficiently concerned to urge the Court to keep in mind – as reported in the newspapers – “the wider constitutional and societal implications arising from attempts to reshape the established narrative of the 2019 Easter Sunday attacks.” The supporting petitions are equally concerned about the space for the emergence of a counter-narrative – again, as reported – “unproven allegations have created a public narrative suggesting a wider conspiracy involving Sinhala Buddhist military and intelligence officers, contrary to the findings of the Supreme Court and the Presidential Commission.”

It is the broader contentions asserted in the petitions supporting Mr. Sallay’s application is what I am calling here as the return to old politics. It is of course not that old for it has been the dominant mode of politics until 2024, and it is raising its head in a substantive way for the first time after the election of the new NPP government. Left to court filings the old politics should wither away under the weight of evidentiary material and legal arguments that alone will ultimately hold sway in any and all court proceedings. But the old politics is having an inadvertent companion in what I see as emerging new politics, and the confluence of the two may create a new challenge for the still fledgling NPP government.

The shape of this new politics is evolving around the government’s controversial proposal to extend the age of retirement of judges by two years – from 63 to 65 for the Court of Appeal Judges and from 65 to 67 for the Supreme Court judges. The proposal that was first mooted for the judges of the two superior courts has since been extended to all judges. A case of the government compounding its own case, so to speak.

Not for the first time, the government would seem have mishandled its own situation by not being forthcoming and pro-actively explaining its intentions and the reasons for seeking to extend the age of retirement for judges. The politics of the matter is being shaped by too little sayings by the government and too much protesting by its critics. There is a veritable piling on about this matter that was never there in the past when government actions targeted the judiciary even more ominously than it would appear to be the case now. While the return of the old politics and the emergence of the new are not manifestly connected now, it is almost natural that they will find ways to be mutually reinforcing.

The politics of Writ Applications

The supporting and opposing petitions in the Suresh Sallay case are symptomatic of the great divide in the political universe, if not much of the country, over the status of investigations and their findings about the Easter attacks. While the supporting petitioners are convinced about the conclusiveness of all the previous investigations, inquiries and litigations, the Catholic Cardinal is speaking for those who are equally convinced of the inconclusiveness and the incompleteness off all the previous investigations and their findings.

Their contention is that what has been established so far is limited to the truth about the organizational planning and executions of the bombings, on the one hand, and the failure on the part of state officials to prevent those attacks in spite of being aware of prior intelligence warnings about the impending attacks. The missing part of the whole truth in this view is the possibility of prior contacts and even collusion between state officials and the perpetrators of the attack.

Those who assert the conclusiveness of all previous investigations conveniently ignore some salient facts. First, of the four presidential inquiries (the first two by President Sirisena and the last two by President Wickremesinghe) only one – the Presidential Commission of Inquiry headed by Janak de Silva produced some results. The other three were washouts. The Parliamentary Select Committee, which was opposed by President Sirisena and was boycotted by the Rajapaksas and the SLPP, produced a useful report and its findings became grounds for fundamental rights applications against state officials accused of negligence.

Second, it is incorrect and unfair to say that the Supreme Court has conclusively ruled on all aspects of the Easter attacks matter. The Court has only ruled on the 12 fundamental rights cases that were brought before it. There are over 90 cases in the lower courts, including 41 High Court cases and the main case in a High Court Trial-at Bar, and all of them have been dragging on for all these years with no end in sight. There might be new indictments and cases arising out of the new investigations under the NPP government.

Third, it is conveniently forgotten that the investigations that had a chaotic start under Maithripala Sirisena were completely stalled after Gotabaya Rajapaksa became President in November 2019. All of this was well known among those who were frustrated about the whole process and the total lack of progress. It was also known among others but they rather chose to remain faithful to “the established narrative of the 2019 Easter Sunday attacks.”

In a recent Court of Appeal hearing into the former President Gotabaya Rajapkas’s Writ Petition for a court order preventing his arrest, the government lawyers vigorously pushed back against what they called the suppression or misrepresentation of material facts by petitioner Rajapaksa pertaining to aspects of the Easter attacks. The upcoming hearing on the intervening writ applications in connection with Mr. Sallay’s main petition, will provide the forum for further contestations over material facts as well as other arguments that may not be quite material to the case.

Pertinent to the ‘old politics’ theme of this article, there will likely be allusions to the so called broader implications for the constitution, the state and of course the Sinhala Buddhist nation. The written submissions, as reported in the media, have already alluded to them. To be sure, and as has been noted by others, most inimitably by Punchi Putha in the 5th Column of the Sunday Times, there was no great intervening concern in the immediate aftermath of Suresh Sallay’s arrest in February, early this year. The political interest and invocations of Sinhala Buddhist nationalism came fast and furious only when the Easter lawfare gaze turned on Gotabaya Rajapaksa. Now the two are inseparable and there will be overlapping and mutually reinforcing allusions

For the NPP government that seems to have comfortably settled on its own illusory premise of a post-communal/post-racial Sri Lanka, the return of old politics will be another distraction. The NPP is politically too astute to miss the confluence of lawfare and politics in the writ applications for and against investigating the Easter attacks. Its grassroots grounding may prove to be a strong enough bulwark against the new arrival of the old communal politics. A bulwark that the Old Left and the new Liberals could not easily fall back on when they took the fight to communal politics and ethno-nationalist excesses. What should be a bigger concern for the NPP government is the emerging new politics that is formally predicated on the independence of the judiciary but can easily become part of a political pincer against the government.

The Politics of Judicial Retirement

To be sure, the current controversy over the age of retirement of judges is a self-inflicted problem for the government. The first indication is reported to have come from remarks made by President AKD himself to a gathering of the Judicial Officers Association and the High Court Judges Association, in early June. Although the main focus was on giving two year retirement extension to the Court of Appeal and Supreme Court judges, the President is reported to have expressed an intention to similarly extend the age retirement for all judges. While there was no reported response by those attending the meeting, the news about the President’s remarks spread like wildfire within legal circles.

Critics immediately pounced on the initiative as a ruse to extend the tenure of the current Chief Justice Padman Surasena who is due for retirement in December this year, in what would be a very short tenure (July 2025 to December 2026) for a Chief Justice anywhere else but has become the norm for Sri Lankan Chief Justices this century. That is another matter. The government has not formally responded to criticisms and according to the Bar Association of Sri Lanka (BASL), its letters on the matter to the President and the Minister of Justice remain unanswered. While being silent, the government is neither deaf nor blind to what is going on.

It is quite possible that the government feels self-assured by the lack of unanimity within the judicial and legal fraternities. A case in point is the variously reported July 11th Special General Meeting of the Judicial Services Association. The meeting unanimously voted against the government’s proposal but it was attended by only 65 of its 250 members. The meeting apparently lacked quorum and the Association’s President, Magistrate Pasan Amarasena, had resigned earlier protesting against the impropriety of the meeting itself. There are also mixed reports about the sentiments within the judicial fraternity and the reported reactions to the administrative discipline attributed to the current Chief Justice.

The government is also aware that its Easter lawfare is generally popular in the country. According to reports of a recent CPA survey, slightly over 50% of the people support the NPP government’s handling of the investigation into the Easter attacks, and support rises to nearly 60% among people under 30 years. So, the government may choose to turn a deaf ear to all the learned criticisms and carry on with its proposal by simply passing a constitutional amendment using its thumping parliamentary majority. A referendum is obviously not needed for this, but a Supreme Court ruling to that effect will likely be greeted by some critics as self-serving.

Such a course by the government is not at all beyond reproach. For it turns the old adage – there have been bad judges, there will be bad judges, but there are no bad judges – on its head by making present judges bad judges. And it creates the corrosive environment of disappointment and frustration among junior judges aspiring for promotions. While there are good reasons to extend the age of retirement systemically for the future, benefiting those currently in office is not a welcome formula.

At the same time the government may be handicapped by the limited pool of judicial officers from whom it has to make choices. The delay in filling the current vacancies in the Supreme Court may be the symptom of a more structural problem than political expediency. These are sensitive topics that no politician or government can loosely talk about. Not everyone is a Donald Trump. Only a properly ribboned presidential commission can weigh in on these matters.

In all the verbal brouhaha about retirement ages, hardly anything has been said about how the Supreme Court came to have as many as 16 judges and to have such quickfire turnovers of Chief Justices. In the US and other countries the average tenure of Supreme Court judges, especially Chief Justices, span multiple presidential terms and different presidents. A long span at the bench, as opposed to a rapid turnover is both necessary and conducive for facilitating judicial independence, stability and consistency.

On the other hand, changing Chief Justices every two years is not a recipe for judicial independence or stability. When a President can appoint more than two Chief Justices in one term, which aspiring Chief Justice is going to professionally inert about his promotional prospects? President Dissanayake has been in office for barely two years and he is set make his third Chief Justice appointment come December this year.

The 1978 Constitution (Article 119) prescribed that the Supreme Court shall consist of a Chief Justice and not less than six and not more than ten other judges. The expansion of the Supreme Court to 16 judges, and the Court of Appeal from 12 judges to 19 judges, came through a constitutional amendment but without anyone noticing or opining about. For it was sneaked in during the third reading of the 20th Amendment in October 2020, when Gotabaya Rajapaksa was President and Ali Sabry was the Minister of Justice.

Mr. Rajapaksa appointed five new Supreme Court judges in a single month, December 2020. In other times and in other places that would have been called packing the court. Of the current bench of 12 Supreme Court judges, seven are Gotabaya Rajapaksa appointees and five are Dissanayake appointees. Four of the latter were appointed in a single month in January 2025. Only the Chief Justice was appointed by a different president, President Sirisena, in January 2019.

As for Chief Justices, there were eight of them between 1948 and 1977, and six from 1977 to 2009. Since 2009, there have been nine more judges including the present Chief Justice, in a span of 17 years, an average of less than two years. The tally for Chief Justice appointments by Executive Presidents since 1977 indicates three by President Jayewardene, two by President Premadasa, one by President Kumaratunga, three by President Mahinda Rajapaksa (one of whom was impeached and removed), four by President Sirisena, none by President Gotabaya Rajapaksa, and two in two years by President Dissanayake.

What is not revealed by these tallies are the affronts that the judiciary and especially the Chief Justices have suffered at different times at the hands of the executive. To wit the summary sacking and rehiring of the entire Supreme Court by President Jayewardene in 1978 and again in 1983, and the singular impeachment of a Chief Justice by President Mahinda Rajapaksa in 2013. Seen against the backdrop of these blatant affronts, the current initiative to extend the retirement age of the Chief Justice and other judges could be seen as an unwelcome award. As for the attendant politics, there was hardly a whimper about the past affronts while there is a chorus of protests about the proposed award.

From the Pathfinder Collection

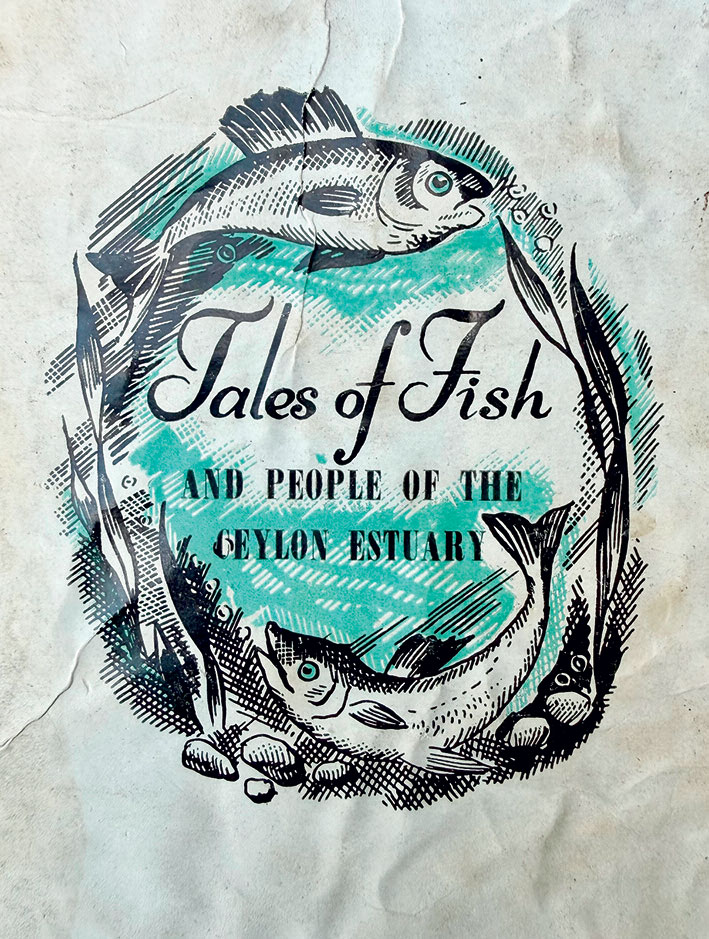

Published in Colombo in 1954, J. A. R. Grenier’s Tales of Fish and People of the Ceylon Estuary is a small masterpiece: an angling memoir rich in natural history, practical fishing knowledge and tender observation of the fishing communities whose lives were bound to the sea.

During the Covid lockdowns, my husband’s uncle Nimal Jayawardena began sorting through his extensive collection of books on wildlife, natural history, fishing and hunting. Boxes arrived at our house in batches. Unpacking, reading and cataloguing the books brought welcome pleasure to days otherwise marked by uncertainty, isolation and restrictions on movement.

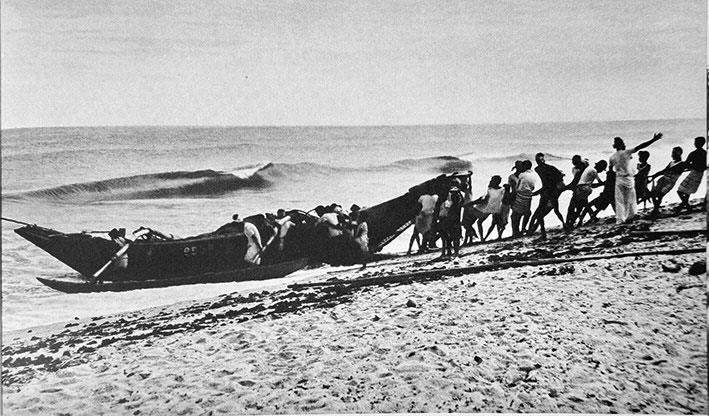

Fishermen hauling a fishing catamaran ashore after returning through the surf. Photograph by Reg Van Cuylenburg from Image of An Island – A Portrait of Ceylon (1962). Pathfinder Collection

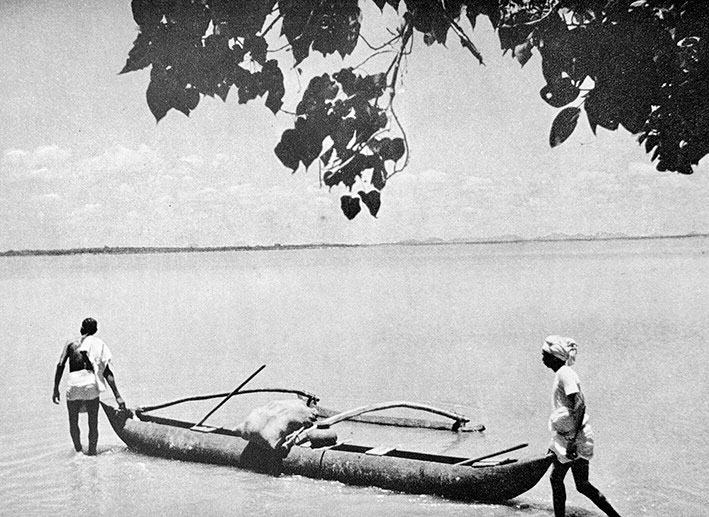

“What Will the Day Bring?” Canoe beside a tranquil estuary. Photograph by Lionel Wendt from Lionel Wendt’s Ceylon (1950). Pathfinder Collection

In one of the boxes, I noticed a slim volume in a plain white dust jacket. Spartan in appearance, its only adornment was a small circular medallion showing two fish swimming in a ring around a rocky estuarine scene. The design was rendered largely in black and white, with a muted greenish-blue wash. At its centre appeared a title that promised far more than the modest artwork: Tales of Fish and People of the Ceylon Estuary. The cover did not even bear the author’s name.

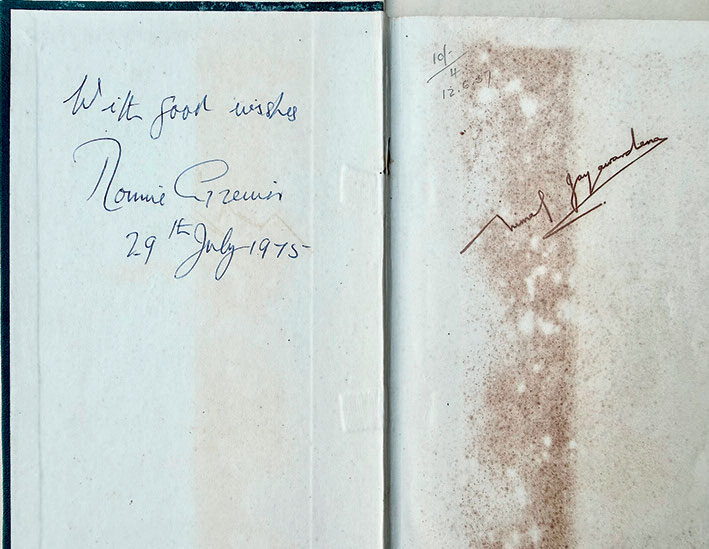

Inscription by J. A. R. Grenier to Nimal Jayawardena, dated 29 July 1975, with Jayawardena’s signature opposite. Pathfinder Collection. Author’s photograph

Detail from the dust jacket of Tales of Fish and People of the Ceylon Estuary (Colombo, 1954), showing the distinctive fish medallion. Pathfinder Collection. Author’s photograph

Out of curiosity, I opened this unassuming book and began to read. Within its weathered pages, a succession of worlds began to unfold: that of the recreational angler, for whom fishing was an absorbing passion; the natural world of Ceylon’s estuaries and their fish; the practical world of tackle, bait and technique; and, finally, the world of the fisherfolk, whose lives depended upon an intimate knowledge of the waters.

Portrait of a fisherman. Photograph by Reg Van Cuylenburg from Image of An Island – A Portrait of Ceylon (1962). Pathfinder Collection.

At only 155 pages, the book is divided into two parts: “Fish,” devoted to the angler, the estuary and the practical knowledge of fishing; and “The People,” in which Grenier turns to the fisherfolk themselves.

The mystery of the angler

Grenier begins with a question that must have been put to anglers in every generation: why devote so much time, money and effort to an occupation involving discomfort, uncertainty and frequent failure?

His book is, among other things, an extended answer to that question.

In this, he belongs to a centuries-old angling tradition, familiar from Izaak Walton’s The Compleat Angler, in which fishing is valued not merely for the catch but for the fellowship it creates and the intimacy with nature it permits. Grenier gives that tradition a distinctly Ceylonese expression.

For him, fishing satisfies the gambling instinct: every cast holds possibility, and every expedition begins with hope.

The appeal also lies in escape. The estuary is usually remote: there, Grenier writes, the river, “tired of being harassed by humanity along its banks, seeks solitude where it meets the ocean.”

Grenier describes the principal fish of the estuary and deep sea, their habits, feeding patterns and preferred habitats, observing how tide, season and weather shape their movements. He also preserves a detailed practical record of fishing: tackle, baits, traditional nets and fishing methods—knowledge accumulated through years of experiment, observation and conversation.

His discussion of angling is often enlivened by the companionship, banter and minor disputes of his fellow anglers. Grenier recalls an episode from A. H. Pertwee’s Ceylon Marine and Estuary Fishing. Notes on a Neglected Pastime, first published as a series of articles in The Times of Ceylon before appearing as a booklet in 1907. To convince doubters of the strength of Ringall bamboo rods, Pertwee staged a “Man versus Fish Competition” at the Calcutta swimming baths. The “fish” was Mr Mason, a powerful swimmer weighing more than ten stone—whom I cannot help imagining with a luxuriant handlebar moustache and a striped bathing costume. Harnessed to the line and given thirty feet of slack, he managed only seventy feet before Pertwee reeled him in foot by foot and finally “gaffed” him with a billiard cue.

From fish to people

Part Two, simply titled “The People,” is more than a change of subject; it alters the meaning of much that has come before.

Grenier opens by confronting the stigma attached at that time to Ceylon’s coastal fishing communities. Those who earn their living from the sea, he observes, are often judged by people who know little of the skill and endurance their work demands, or of the dangers they face. However sympathetic, the “land-encumbered” observer, as Grenier puts it, can never fully comprehend the rigours and terrors of the sea without having faced them.

The introductory chapter, titled “PRO” in capitals and quotation marks, makes Grenier’s regard for the fishermen unmistakable. They are the true professionals: men he came to admire and respect, and from whom he learned lessons extending far beyond fishing.

For the working fisherman, the sea governs every aspect of life. It provides his livelihood, but may also threaten his boat and his life. Danger, hardship and uncertainty are enduring conditions of his world. The sports angler by contrast chooses temporary discomfort and may return empty-handed but to a secure bed and meal.

Such conditions also help explain the fishermen’s reserve towards recreational anglers, whom they regard as outsiders whose inexperience may hinder the work and even jeopardise a catch. Grenier observes that a newcomer is fortunate if accepted within five years. Some of his happiest moments come when fishermen such as Jemma of the Kalu Ganga, Anthony of Negombo or Manuel of Mannar disclose a favoured fishing ground or allow him to join them in their boats.

Yet fishing can also produce a camaraderie capable of crossing barriers firmly maintained on land. Grenier’s acceptance is never assumed, but gradually earned through patience, shared experience and respect for the fishermen’s knowledge. An invitation into a boat or the disclosure of a closely guarded fishing ground signifies far more than access to better sport. It marks his admission into a fraternity.

From there, Grenier opens a window onto the fishermen and their communities through a succession of miniature biographies.

The “PROS”

There is Jemma, whom he calls the “King of estuary fishermen of Ceylon.” For thirty years he has fished at the mouth of the Kalu Ganga and knows every rock, obstruction and hidden danger in the estuary. So accustomed is he to sitting in his small canoe that, even on land, his legs creep beneath him into the same position when he becomes absorbed in conversation.

His tackle is modest but meticulously made. Grenier’s respect for his skill deepens when one of his seemingly fragile handmade lines lands a skate weighing some twenty pounds.

From Mannar comes Soosai, the shark hunter, whom Grenier describes as a “bronzed miracle of a man with limbs like jungle trees and shoulders as thick as a Dutch wall.” He lives amid the bones of his quarry.

Bemiya prefers the company of fish and animals to that of people and speaks only when necessary, yet has lovely names of his own for the fish he catches. His gift lies not so much in fishing with rod and line as in diving. His large, “plate-like” hands and long, double-jointed fingers seem made for work beneath the surface, where he moves with an ease he is denied on land.

Bemiya later disappears during a dangerous attempt to subdue a shark caught by his fellow fishermen. Grenier’s brief farewell to him is among the most affecting passages in the book.

The final and perhaps most powerful portrait is that of Anthony, the wise and kindly fisherman of Negombo who takes Grenier under his wing. Anthony teaches him not only how to fish, but also the fisherman’s code. Behind his patience and wisdom lies a history of personal loss.

The book closes with his account of the storm in which he lost his son. Boats remain at sea while the people on shore watch the horizon with the quiet dread born of bitter experience. Through Anthony’s recollection, Grenier evokes an entire village overtaken by grief, its cries of mourning rising against the gale and the breaking surf. Anthony bears his loss with a sad fatalism.

The sea, he tells Grenier, “makes us and breaks us.”

A society in transition

J. A. R. Grenier—known as Ronald—was born in Ceylon in 1912.

The world he evokes is that of late colonial and early post-independence Ceylon: government service, clubs, sporting friendships, coastal journeys and long-established personal networks, brought through fishing into close contact with communities bound by occupation, poverty and dependence upon the sea.

Moved by the book, I wanted to learn more about its author. My search led me to the website of his son, David Grenier, and to the life that lay behind its pages.

By the late 1950s, Grenier had concluded that his children’s prospects in Ceylon were uncertain. In 1959, his fourteen-year-old son David left for Australia with several family members, including his grandmother and aunts. Grenier followed three years later, in 1962.

The decision was practical and paternal, but came at great personal cost. According to David, his father knew before leaving that he would not be happy in the West and would dearly miss the ocean, the fish and the fishing people of Ceylon.

I had scarcely read those words before thinking, “he will never be happy there.” A few paragraphs later, David wrote that his father was never the same after the move.

Read with that knowledge, the book becomes not merely an account of fish and fisherfolk, but also a record of a landscape, a body of knowledge, and a way of life from which Grenier was soon to be separated.

The story of our copy

When I returned to our copy while preparing this article, I noticed that it bore an inscription by Grenier dated 29 July 1975. Puzzled, since I knew he had emigrated to Australia more than a decade earlier, I telephoned my husband’s uncle Nimal to ask about its circumstances.

Nimal recalled that Grenier had returned to Sri Lanka that year for a fishing journey “down memory lane” along the East Coast with their mutual friend Frank Kelly, who had also migrated to Australia.

In his younger days, Nimal had been an avid angler, deep-sea fisherman and sportsman who knew the eastern coastline and its jungles particularly well. Frank called at his house to borrow camping equipment for the expedition, and Grenier accompanied him.

By coincidence, Nimal was reading Tales of Fish and People of the Ceylon Estuary at the time. He brought the book downstairs and asked Grenier to sign it. The three men spent some time reminiscing about earlier days of fishing before Grenier and Kelly continued on their journey.

Nimal also knew Willie Obeysekera and Peter Jayawardena, fellow anglers whom Grenier thanks in the acknowledgements. After retiring, Peter worked as a guide for one of the family companies, based in Inginiyagala.

These connections place the book once again among the friendships and shared experiences from which it emerged. The inscription transforms our copy into a record of Grenier’s return—to waters, friendships and memories that had endured the years abroad.

Grenier in Australia

In later life, Grenier developed a rare and incurable illness that severely affected his health and wellbeing. He died in Queensland in 1988, aged seventy-five.

When I learnt of Grenier’s death, my thoughts returned to the hope he had once expressed for Bemiya: “I hope there are fish in the place he has gone to, for without them, he, like you and I, will never be happy.”

David later worked to preserve his father’s literary legacy, personally publishing Isle of Eden and Isle of Eden Revisited.

A forgotten Sri Lankan classic

Grenier’s work defies easy classification. It is a rare conjunction of fishing manual, angling memoir, natural history and social record. Within little more than 150 pages, he preserves an extraordinary body of knowledge about Ceylon’s estuaries: their fish, habitats, fishing methods, language and communities. It is, in effect, a compact cultural archive written in the form of an angling memoir, distinguished throughout by tenderness, restraint and quiet humanity.

Its appeal extends far beyond anglers. More than seventy years after its publication, there is still nothing quite like it. The book deserves to be read again.

Emeritus Prof Manouri P Senanayake ✍️

President, Servants of the Buddha

The seven weeks or ‘Sath Sathiya’ commences in the immediate aftermath of Vesak Full-Moon Poya Day and is spiritually important to Buddhists because of the deeply meditative aspects of this period in the Buddha’s Life. Spent in the vicinity of the Bodhi tree, each week has an identified location where a distinct occurrence of significance took place. This article reflects on the Blessed One meeting with two travelling merchants named Tapassu and Bhalluka – an encounter that has added many historic milestones and competing memorials to Buddhist history.

The two merchants, Tapassu and Bhalluka occupy a unique and renowned position throughout the Buddhist world as the First Two Disciples. They form the starting point of the Buddha Sasana i.e. Buddha’s dispensation which quickly expanded to a mammoth following. Twenty-six centuries later it is continuing to grow, drawing to its folds men and women of all ages and all walks of life without inducements. An occurrence seen in all parts of the world.

In the Tipitaka, Vinaya Pitaka, records the arrival of Tapassu and Bhalluka as two travelling tradesmen hailing from an area called Ukkala and makes mention of them offering to the Buddha a meal of cereal (possibly a gruel of barley) and honey balls. Their expression of interest in becoming the Buddha’s First Disciples and being recipients of hair relics following their request for a token to take away, are also mentioned. It is widely believed that these events took place in the seventh week.

The brevity of this account in the Pali Canon is in keeping with the Tipitaka’s main focus, which is the Teachings of the Doctrine (Dhamma) and Discipline (Vinaya), while details on the Life of the Buddha are relatively little. Narratives surrounding these events are however more extensive today and some are attributed to Commentarial literature. The items of food mentioned fulfil the long-lasting quality required for a long journey and Anguttara Nikaya states the merchants as caravanners.

‘Foundational Firsts’ that are credited to Tapassu and Bhalluka

Among the history-making events to the names of Tapassu and Bhallika that are worthy of recollection, are: being the first humans to meet the recently enlightened Buddha and donors of the first post-enlightenment meal, the first devotees (dayakes) who helped end the fast after attaining Buddhahood, the first humans to have heard the Buddha’s Teachings, the first to declare their confidence (shraddha) in the Buddha and the Dhamma, the first laymen to recite the Refuges which were Two-fold instead of the Triple Gem as this was prior to the existence of the Sangha. For this reason the two merchants are referred to as the first Dvevacika-sarana upasakes. The list also includes them as the first recipients of a Buddha relic for worship and the first to build a place of worship that enshrines relics. Irrespective of whether all of the above are correct or not, the confidence in the Buddha’s Teachings generated in the two merchants who asked for a sacred item to keep with them, is irrefutable.

Competing Memorials of Sites where the Hair relics are enshrined

In this backdrop, an important question that arises is, “Where were the hair relics enshrined?” However, no historical or sociological discussion on where the hair relics were enshrined by Tapassu and Bhalluka ends with no definitive single answer. It is widely believed that the relics were enshrined by the two merchants either in their homeland or in a place they travelled to. Interestingly, multiple regions or more specifically four countries claim ownership to the site where the relics were enshrined.

Each country has differing and even overlapping historical evidence to support their claim. The evidence varies from rock inscriptions and cave inscriptions to travelogues of explorers. Three of the sites claim to be in the homeland of Tapassu and Bhallika while one site (the one in Sri Lanka) is claimed as a place visited by the two travelling merchants. Furthermore, each site has evidence of a stupa or a brick covered mound where the hair relics could have been enshrined. The single common feature all these countries share is a rich Buddhist history.

The four main locations that are contenders for authenticity are listed here in no specific order. Balkh in Northern Afghanistan, was once the most active Buddhist centre in Central Asia and has been claimed to be the hometown of Bhalluka. That he had built a stupa enshrining hair relics is documented by the famous Chinese Buddhist traveller cum explorer Xuanzang who visited Afghanistan and India in the 6th century CE. It is well recognised that Buddhism reached Afghanistan (then Bactria) at a very early stage, along trade routes.

Another site is Tiriyaye in the North-East of Sri Lanka, a location close to the east coast of the island where an ancient seaport had thrived over several centuries attracting many ships – and very possibly merchants via the sea-route. Evidence of an ancient temple with archaeological evidence as a place of worship exits to date. Cave inscriptions dating back to 2nd century BCE testify to pilgrims from South India arriving at the site to “worship the shrine containing the relics placed by Tapassu and Bhalluka”. This is written in Sanskrit using an ancient Tamil script. The legend is that the two merchants left the casket containing the hair relics covered for safety at this site and went about their business. On return they found it difficult to remove and believing this to be a holy place had the relics enshrined at the site. Sri Lankan Buddhists believe the stupa called Girihanduseya which has been expanded over the years by various Kings, to either contain or had ‘once-contained’ the hair relics.

Orissa in India

also has a ruined stupa i.e. a brick-walled mound and the names of both Tapassu and Bhallika inscribed and visible near-by. Furthermore, most scholars believe Ukkala to be in the region of Orissa (today’s Odisha). This is in the eastern part of India, not too far from Uruvela and Bodh Gaya. Finally the Schwedagon Pagoda in Yangon, Myanmar is claimed to enshrine the hair relics. This beautiful Stupa of a golden hue is among the most revered places of worship in Myanmar. Tapassu and Bhalluka are said to have been from Myanmar.

In instances when historical and/or sociological evidence causes different communities to vie for ownership of a historical monument or object, the French term lieu de mémoire is used and is a concept that could resolve the confusion, with participation of all stake cholders. ‘Competing Memorials’ or a ‘Competition of Memories’ are also terms that frame such situations. In the case of these relics, there is no active conflict among the different claimants. Hence it appears that “the jury is still out” and will continue to remain so into the foreseeable future.

However, as no active conflict exists surrounding the above four claims “the jury that is still out” on this matter appears it will remain so.

Typhoon Noul makes landfall in China, with hundreds of thousands evacuated

Colombo Kaps down Dambulla Sixers by 21 runs

Kandy Royals win by 11 runs

Showers will occur in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Govt. launches EPF, ETF shake-up

SLPI concerned over the proposed Chartered Institute of Media Professionals of Sri Lanka

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Midweek Review5 days ago

Midweek Review5 days agoThree high-profile alleged suicides shaping key investigations

-

News2 days ago

News2 days agoFort Magistrate orders arrest of MP Archchuna

-

Editorial2 days ago

Editorial2 days agoAn indictment of all parties

-

News5 days ago

News5 days agoCustoms asked to resume probe or face legal action

-

Editorial6 days ago

Welcome bid to tackle rolling death traps

-

Opinion3 days ago

Opinion3 days agoUkraine’s power struggle spills on to the streets

-

News2 days ago

News2 days agoNational-level cybersecurity facility Lab established

-

News7 days ago

News7 days agoMerchant Shipping Secretariat probes bribery scandal