Business

Special goods and services tax: Issues and concerns

By Dr Roshan Perera & Naqiya Shiraz

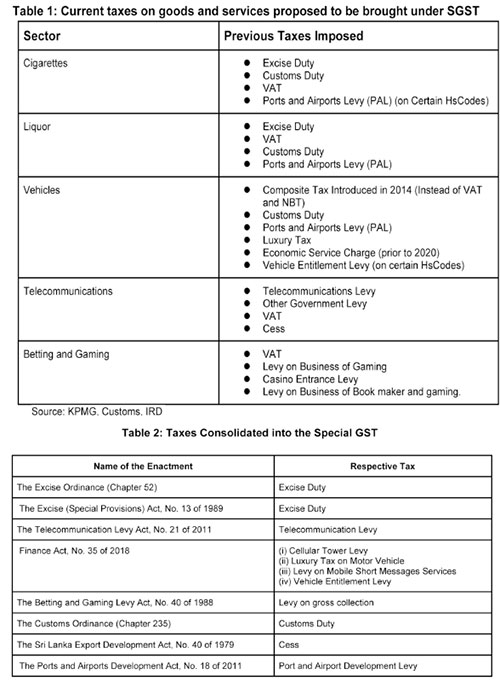

The new bill titled ‘Special Goods and Services Tax’ was published by gazette dated 07 January 2022.1 The Special Goods and Services Tax (SGST) was originally proposed in Budget speech 2021 but was not implemented. It has once again been presented in Budget 2022. The SGST aims to consolidate taxes on manufacturing and importing cigarettes, liquor, vehicles and assembly parts, while also consolidating taxes on telecommunication and betting and gaming (see table 1 for existing taxes on these products and table 2 for taxes consolidated into the SGST as per the schedule in the gazette). The rationale for this new tax as per the bill is “…to promote self-compliance in the payment of taxes in order to ensure greater efficiency in relation to the collection and administration on such taxes by avoiding the complexities associated with the application and administration of a multiple tax regime on specified goods and services.”

Given the multiplicity of taxes and the complexity of the current tax system as a whole, rationalising taxes is necessary to improve collection. However, whether the proposed SGST simplifies the tax system, while ensuring revenue neutrality or even improving revenue collection, needs to be carefully examined.

The SGST Bill is silent on the treatment of the existing VAT on these goods and services. However, according to the Value Added Tax (Amendment) Bill also gazetted on 07 January 2022,1 liquor, cigarettes and motor vehicles will be exempted from VAT while telecommunications and betting and gaming services will still be subject to VAT.

While the gazetted Bill sets out some of the features of the proposed SGST there are many important areas not covered in the Bill. These are expected to be gazetted as and when required by the Minister in charge.

Issues & Concerns

The motivation behind SGST is the simplification of the tax system. Although the objective of introducing the SGST is to improve efficiency by reducing the complexity of the tax system there are many issues and concerns with this proposed tax.

Revenue

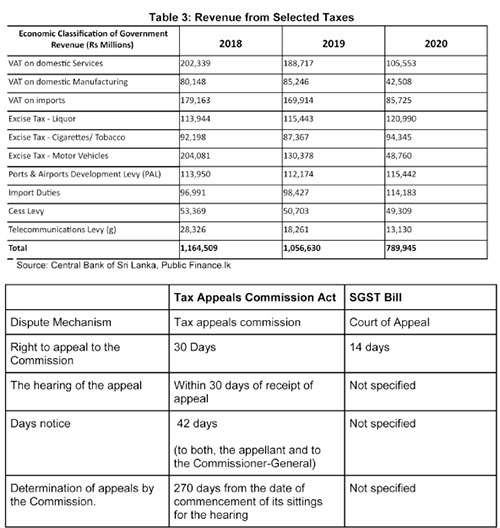

Tax revenue which was 13% of GDP in 2010, declined to 8% in 2020. Ad hoc policy changes and weak administration contributed to the decline in tax revenue collection. This continuous decline in tax revenue has led to widening fiscal deficits and increasing debt. One of the main reasons for the current macroeconomic crisis is low tax revenue collection. Hence, any change to the existing tax system should be with the primary objective of raising more revenue.

According to the budget speech the SGST is estimated to bring in an additional Rs. 50 billion in revenue in 2022.1 Revenue from taxes proposed to be consolidated under the SGST has significantly declined over the past 3 years. Given the already difficult macroeconomic environment, along with ad hoc tax policy changes raising the additional revenue estimated at Rs. 50 billion seems a difficult task.

Tax Base and Rate

For the SGST to raise taxes in excess of what is already being collected through the existing taxes, the rate and the base for the SGST needs to be carefully and methodically calculated. Further, the existing taxes have different bases of taxation. For instance the basis of taxation of motor vehicles is both on an ad valorem1 basis and a quantity basis while the basis of taxation of cigarettes and liquor is quantity.2 In light of this, the basis of taxation on which SGST isapplied becomes an issue. Having different bases and different rates for various goods and services would complicate the implementation of the tax These issues need to be carefully considered to ensure the new tax is revenue neutral or be able to enhance revenue collection.

Efficiency

One possible revenue benefit of this proposal is the inability to claim input tax credits on the sectors exempted from VAT. However, the issue is the cascading effect that would result where there would be a tax on tax with the end consumer paying taxes on already paid taxes. If the idea was to raise additional revenue by limiting tax credits, it would have been simpler to raise the tax rates on the existing taxes rather than introduce a new tax.

4. Administration

According to the bill, SGST will now be collected through a new unit set up under the General Treasury where a Designated Officer (DO) will be in charge of the administration, collection and accountability of the tax. The existing revenue collection agencies, such as the Inland Revenue Department (IRD) or the Excise Department will not be primarily responsible for the collection of this tax. By removing the IRD and Excise Department, a parallel bureaucracy will be created, at a time when public spending needs to be carefully managed. The General Treasury also has no previous experience and expertise in direct revenue collection. Weak administration is one of the key reasons for the low tax collection and success of this tax would depend on the strength of its administration.

In addition to the above mentioned concerns, as per the Bill the minister in charge of the SGST has been vested with the power to set the rates, the base and grant exemptions. Accordingly, Parliamentary oversight over fiscal matters is weakened under this proposed Bill.

It could also lead to a time lag between the gazetting and implementing of changes to the SGST (such as the rate, base etc) and obtaining Parliamentary approval for those changes.

Dispute resolution

The SGST Bill also focuses on the dispute resolution mechanism. Under the present tax system, with the enactment of the Tax Appeals Commission Act, No. 23 in 2011 the Tax Appeals Commission has the “responsibility of hearing all appeals in respect of matters relating to imposition of any tax, levy or duty”.1 The most recent amendment to the Tax Appeal

Commissions act (2013)1 seeks to address the large number (495) of cases pending before the Tax Appeals Commision2 by increasing the number of panels to hear the appeals.

Under the proposed SGST disputes will be handled through the court of appeal. However, the time period by which specific actions need to be taken is not provided in the bill. In addition, disputes have to be taken to the court of appeal. Hence, the entire process will be more time consuming. This could result in revenue lags and difficulties in revenue estimation until disputes are resolved.

Additionally, in the case that no valid appeal has been lodged within 14 days, any remaining payments would be considered to be in default. Thereafter, the responsibility is shifted to the Commissioner General of the IRD to recover the dues. Given the IRD is completely removed from the normal collection process, the rationale for bringing defaults under the IRD is not clear.

III. Policy Recommendations

As discussed, the SGST Bill has several limitations and much of this is due to the ambiguities in the Bill.

If the tax is implemented, the rate and basis of taxation needs to be revenue neutral to ensure tax collection is maximised and administrative costs minimised.

The rates, basis of taxation, exemptions etc should be specified in the Bill, as done in most other Acts. This would avoid the power for discretionary changes to the tax being placed in the hands of the minister in charge.

Given the already weak tax administration, it would be more sensible to strengthen the existing revenue collecting agencies and address the weaknesses in the existing system without creating a parallel bureaucracy.

In the case where VAT is consolidated into the proposed GST, the issue of cascading effect of input tax credits needs to be addressed. This is relevant particularly in the case of capital expenditure.

Given the critical state of revenue collection in the country the question to ask is whether this is the best time to introduce a new tax. Focus should be on fixing issues in the existing tax system to ensure revenue is maximised. The VAT is the least distortionary tax and it is the easiest to administer. Given these features it can be a very efficient revenue generator for a country. Therefore instead of introducing a new tax, capitalising on systems that are already in place and amending the VAT rate, threshold and exemptions may be a more practical solution to the revenue problem that the country is currently facing.

Dr. Roshan Perera is a Senior Research Fellow at the Advocata Institute and the former Director of the Central Bank of Sri Lanka.

Naqiya Shiraz is a Research Analyst at the Advocata Institute.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

Human resources remain the biggest challenge despite advanced logistics

Industry-wide cost pressures are also beginning to surface

In Sri Lanka’s pharmaceutical trade, the journey of a medicine does not end when it arrives at the port. It must still travel safely across the island – through regulated warehouses, temperature-controlled transport and complex distribution routes – before reaching the pharmacy shelf where patients need it.

That journey is increasingly being powered by Healthguard Distribution, the pharmaceutical logistics arm of Sunshine Holdings, whose expanding distribution network now plays a critical role in ensuring the reliable movement of medicines across the country.

At the centre of that network is the company’s Western Regional Distribution Centre (WRDC), a temperature-controlled logistics hub designed to support the safe storage and efficient distribution of pharmaceutical products across the Western Province.

Spanning nearly 18,920 square feet, the facility functions as a key node in the company’s islandwide distribution system. Originally acquired in 2008 to serve as the main warehouse for Swiss Biogenic Ltd., the site evolved alongside the company’s growing operations. Following a major upgrade programme that began in July 2024, the facility recommenced operations in July 2025 as a fully compliant regional distribution centre aligned with international quality standards.

According to Sunshine Pharmaceuticals and Healthguard Distribution Chief Executive Officer Shantha Bandara, the company’s logistics model is built around a simple but comprehensive concept.

“Our approach is ‘Port to Pharmacy’,” Bandara said during a recent media visit. “We collect pharmaceutical consignments from the Port of Colombo, clear them through Customs, store them under regulated conditions and then distribute them to pharmacies across the country. Importers and manufacturers do not have to worry about logistics – we manage the entire process.”

The distribution network today serves over 4,500 authorised pharmaceutical outlets, including pharmacies, hospitals, channeling centres, supermarkets and SPC Osusala outlets. Operations span 150 main towns and 466 sub towns, supported by 111 active delivery routes and seven regional distribution centres located across the island.

Within that system, the WRDC is the largest and among the most technologically advanced hubs.

The facility maintains strict cold-chain conditions for temperature-sensitive medicines. Its cold room capacity has been expanded from 15 cubic metres to 30 cubic metres, enabling compliant storage of products such as insulin within the required 2–8°C range. Online temperature monitoring systems operate across all storage zones while data loggers are used for insulin deliveries to ensure product integrity throughout the supply chain.

Delivery vehicles are also equipped with GPS tracking and temperature monitoring systems, allowing real-time visibility of shipments.

Automation and digital systems are increasingly shaping the operation. Software automation supports invoicing and customer credit verification, while sales teams use digital tools for order canvassing. The company’s enterprise systems provide real-time inventory and accounting visibility, supported by data dashboards used for operational decision-making.

To safeguard continuity, the facility is equipped with a high-capacity backup generator and dedicated on-site fuel storage, ensuring cold rooms, monitoring systems and warehouse operations remain functional even during power outages.

Behind the infrastructure is a workforce of 102 employees, supported by a specialised 15-member value-added services team trained in Good Distribution Practice (GDP), cold-chain management, safety and emergency response.

Yet despite the sophisticated logistics and infrastructure, Bandara told The Island that the most persistent operational challenge lies in human resources.

“We have the infrastructure, the logistics systems and the operational capability,” he noted. “However, maintaining the required number of skilled employees is an ongoing challenge because the labour market is constantly fluctuating. Our HR team is continuously recruiting and training to keep the workforce at the required level.”

Industry-wide cost pressures are also beginning to surface. Company officials noted that rising fuel prices could eventually affect transportation and electricity costs within the distribution chain, which may in turn influence pharmaceutical logistics expenses in the short term.

Still, the broader goal of the company remains unchanged – ensuring that medicines reach patients safely and on time.

From the moment a shipment arrives at the Port of Colombo to the point it reaches a pharmacy shelf, the process depends on precision logistics, regulatory compliance and operational discipline. For Sri Lanka’s healthcare supply chain, Healthguard Distribution’s growing network is becoming a key driver of that journey from port to pharmacy.

By Sanath Nanayakkare

Singer Sri Lanka, the nation’s foremost retailer of consumer durables, celebrates a truly historic milestone at the SLIM-KANTAR People’s Awards 2026, securing a prestigious triple victory while marking 20 consecutive years as the People’s Brand of the Year, an achievement made possible by the enduring trust and loyalty of Sri Lankan consumers.

This year, SINGER was honoured with yet another triple win with People’s Brand of the Year, Youth Brand of the Year and People’s Durables Brand of the Year at the awards ceremony. This remarkable recognition reflects the deep and lasting relationship the brand has built with Sri Lankans across generations, standing as a symbol of trust in homes across the island.

Janmesh Antony, Director – Marketing said: “This award belongs to our customers. Being recognised as People’s Brand for 20 years, alongside Youth and Durables Brand, reflects our commitment to staying relevant across generations.”

Mahesh Wijewardene, Group Managing Director said: “Twenty consecutive years as the People’s Brand is humbling and inspiring. This milestone strengthens our commitment to keeping customers at the heart of everything we do.”

When Arjuna Herath assumed duties as Chairman of the Board of Investment of Sri Lanka, he quite correctly sent a clear message: Sri Lanka intends to position itself as an investor-friendly destination. The message was reinforced during a visit by a high-level delegation from the USSri Lanka Business Council, where officials spoke of renewed confidence in the country’s economic trajectory.

The optimism is not without foundation. After years of crisis, Sri Lanka has begun to stabilize. Foreign direct investment crossed the psychological threshold of about US$1 billion in 2025, exports climbed to more than US$17 billion, and tourist arrivals reached record levels. These numbers suggest that international capital is once again willing to take a second look at the island. Yet statistics alone do not tell the whole story.

The deeper question facing policymakers in 2026 is whether that early interest can be sustained. For investors, confidence is rarely built on incentives alone; it rests on the expectation that rules will remain consistent once a project begins. In other words, predictability matters more than promises.

That tension between optimism and uncertainty is now emerging as the central theme in Sri Lanka’s investment narrative.

On the one hand, authorities are signaling reform and openness. On the other, several recent developments have reminded investors that implementation can still be uneven. One widely discussed case involved the proposed Ambuluwawa cable-car project in the hill country, where a cross-border investor withdrew after reportedly spending about US$3.5 million. The developer, Amber Adventures (Pvt) Ltd, had planned a US$12.75 million tourism venture but later said the project was halted despite earlier technical clearances from multiple agencies.

Regardless of where the merits of the dispute lie, the episode left a familiar impression in investment circles: timelines and approvals can appear uncertain once projects move from paper to construction.

A separate case in the renewable-energy sector has generated similar concerns. Policy resets and prolonged negotiations reportedly discouraged a major regional developer. Governments everywhere reserve the right to renegotiate contracts, but when processes appear open-ended, investors begin to factor in higher risk.

This is why policy certainty may be the most powerful – and least expensive – stimulus available to Sri Lanka in 2026.

The macroeconomic outlook already underscores this point. Analysts expect moderate growth in the range of about 3 – 4 percent this year, while the International Monetary Fund has projected roughly 3.1 percent, linking stronger expansion to steady reform implementation rather than new borrowing. In other words, execution matters more than announcements.

Institutional efficiency also plays a role. With more than a million cases pending in Sri Lanka’s courts, businesses often see legal delays as an additional cost of operating in the country. Reducing that backlog – particularly in commercial disputes – would signal that contracts and administrative decisions can be resolved within predictable timeframes.

Tourism offers another illustration. Visitor arrivals have surged, yet revenue growth has lagged because spending per traveller remains modest. Improving digital payments, mobility and dispute resolution may prove just as important as marketing campaigns if Sri Lanka hopes to extract greater value from the sector.

All in all, these signals reveal a simple truth. Sri Lanka does not necessarily lack investor interest; it risks losing momentum if processes remain uncertain.

For policymakers, the challenge therefore lies in bridging perception and practice. Codifying approval timelines, digitizing government services, and completing a handful of transparent public-private partnerships could quickly demonstrate that decisions in Sri Lanka are not only possible but reliable.

If that credibility gap is closed, the message delivered by the BOI chairman that Sri Lanka is open for business – will resonate far more strongly in global boardrooms. Because in frontier markets, the most valuable incentive is not a tax break or subsidy. It is certainty.

By Sanath Nanayakkare

Substandard coal deepens energy crisis, warns former CEB Chief

Sri Lanka, ICRC to develop unified national database for missing persons

Experts urge hydration and fruit intake amid heatwave

Healthguard Distribution powers Sri Lanka’s ‘Port to Pharmacy’ medicine supply chain

Fuel: Feints, hooks and rhetoric

Toward a people-friendly transport system in Sri Lanka

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoCIABOC questions Ex-President GR on house for CJ’s maid

-

News6 days ago

News6 days agoSri Lankan marine scientist Asha de Vos honoured at UNGA opening

-

News6 days ago

News6 days agoAustralian HC debunks misleading travel risk claims for Sri Lanka

-

News4 days ago

News4 days agoBailey Bridge inaugurated at Chilaw

-

Latest News6 days ago

Latest News6 days agoWednesdays declared a government holiday with effect from 18th March

-

News4 days ago

News4 days agoPay hike demand: CEB workers climb down from 40 % to 15–20%

-

News3 days ago

News3 days agoCIABOC tells court Kapila gave Rs 60 mn to MR and Rs. 20 mn to Priyankara

-

News7 days ago

News7 days agoFuel rationing begins: Police deployed as queues return