Business

SLT Group FY and 4Q 2023 results impacted by macro-economic challenges

Optimistic on future SLT-MOBITEL forecasts

The SLT Group’s financial results for the fourth quarter and financial year ending December 31, 2023, reflects a downturn in performance amidst a turbulent macro-economic environment in the country.

For 4Q 2023, SLT Group reported a year-on-year consolidated revenue degrowth of 7.5% amounting to LKR 26 billion compared to LKR 28 billion in 2022. The Group’s profits decline was attributed to reduced revenue, despite the efforts of cost optimization measures that resulted in a 5.9% reduction in Operating Expenses (Opex). Consequently, the Group saw a corresponding decline in operating profit, with both Profit Before Tax (PBT) and Profit After Tax (PAT) experiencing decreases in the quarter.

At SLT level, a 3.6% Opex reduction was posted for 4Q 2023 compared to 4Q 2022, attributed mainly to a well-managed cost reduction in staff costs. Further, SLT saw cost savings in other areas credited due to a reduction in advertising and activation costs, with repair and maintenance costs also decreasing during the latter part of 2023. However, these savings were outweighed by a fall in the top line and increase in depreciation, driving overall losses.

Offering a positive trend compared to 3Q 2023, the Group recorded a 13.2% reduction in Opex from 3Q to 4Q and a decrease in net losses from LKR 1.5 billion in 3Q to LKR 1.2 billion in 4Q. Moreover, the Group recorded an operating profit of LKR 549 million in 3Q 2023, followed by a surge to LKR 1.2 billion in 4Q 2023, indicating optimistic future forecasts.

Despite the performance decline over previous year, Mobitel showed a 3% growth in revenue and improvement in profitability parameters in the second half of 2023 over the first half of the year. The EBITDA reported a 9% growth and operating loss have reduced by 54% during the period as a result of company’s top line growth and cost optimization efforts.

Janaka Abeysinghe, CEO, SLT-MOBITEL noted, “Looking ahead, macro-economic uncertainty persists. Despite the year-on-year decline in profitability, we are optimistic and see encouraging signs for 2024. Our cost base is under continuous review and adjusted to match market conditions. Given these fundamental strengths, we believe we will overcome negatives in these challenging markets and are confident in driving the long-term profitability of the Group”. The Group remains committed to financial prudence and business continuity while hoping for improved economic forecasts ahead.

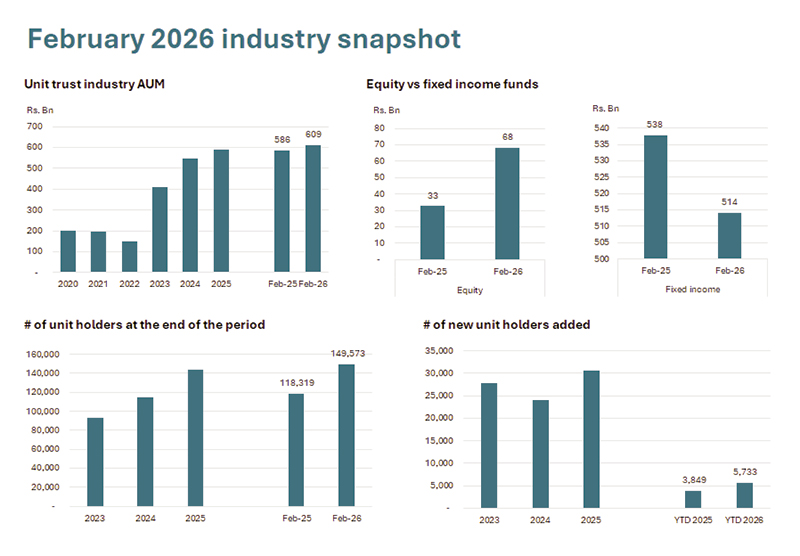

The unit trust industry of Sri Lanka reported assets under management (AUM) of Rs. 609 Bn, up 4.0% year-over-year and largely unchanged compared to the previous month. These assets are currently managed across 85 funds by 16 management companies.

AUM was supported by flows to equity-related funds, which doubled year-over-year to Rs. 68 Bn. Fixed income funds, on the other hand, declined by 4.4% year-over-year. In addition, since 2025, there has been a gradual shift from shorter-term instruments towards more medium to longer-term investment options, with inflows into open-ended income funds, open-ended equity index/sector funds, and open-ended growth funds (equity), alongside a decline in flows to money market funds.

During the month, the industry added 2,623 new unit holders, up 69.8% year-over-year, bringing the total number of unit trust investors to 149,573, which represents a 26.4% increase year-over-year.

Commenting on the February industry results, newly elected President of the Unit Trust Association of Sri Lanka (UTASL) and Director/CEO of Senfin Asset Management, Jeevan Sukumaran, stated: “The industry’s performance as at end-February 2026 reflects a degree of consistency, with continued activity in equity-related funds. We are also observing a gradual shift towards more balanced investment allocations across fund categories.”

He further noted: “As we move forward, our priority will be to build on this momentum by enhancing investor awareness, broadening access to unit trust products, and working closely with regulators and market participants to strengthen further the industry’s depth, resilience and long-term relevance within Sri Lanka’s financial landscape. In a dynamic market environment, maintaining a disciplined, long-term approach whilst reinforcing the resilience of the unit trust structure, with its focus on diversification and professional fund management, will remain key priorities for the industry.”

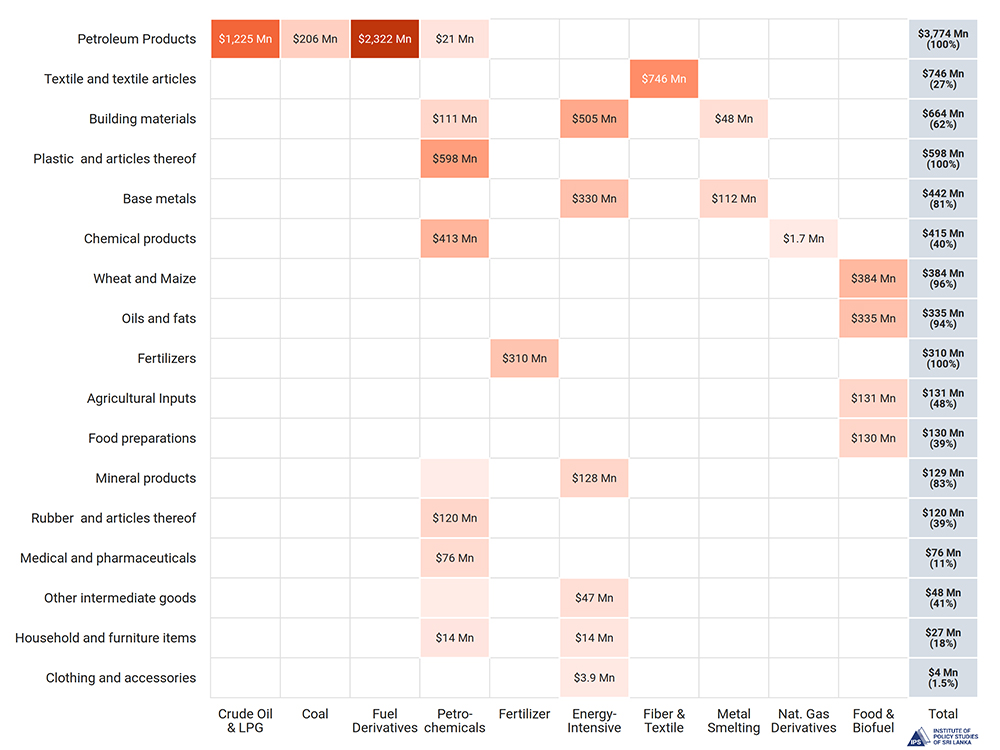

The supply shock in the commodity market directly affects 39.3% of imports of Sri Lanka, or USD 8.3 Bn, across 951 products.

The price shock extends beyond petroleum and petrochemicals to nitrogenous fertiliser, biodiesel alternatives like palm oil, and food, exerting pressure on food prices.

Currently, price pass-through and demand management are the best options, while easing regulatory barriers, such as licensing schemes, are necessary to ensure food security.

The closure of the Strait of Hormuz has unsettled global energy markets. According to the International Energy Agency (IEA), 20 Mn barrels of crude oil products were transported through the Strait in 2025, which accounted for a quarter of the world’s daily energy needs. The closure has driven fuel futures higher, with the Brent futures reaching USD 112 per barrel on 19 March 2026 . A phenomenon called “backwardation” is clearly visible in the fuel market, implying that spot market prices for “physical” fuel are significantly higher than futures prices for “paper” fuel.

The economic impact of the energy price shock can impact Sri Lanka through various channels, and if hostilities in oil-producing regions continue, the effects will intensify over time. The immediate impact stems from rising commodity markets, including not only fuel but also biodiesel feedstocks such as soybean, canola, and palm oil; petrochemicals; fertilisers that use liquefied natural gas (LNG) as a feedstock; and aluminium and base metals, which demand significant energy for smelting.

Against this background, this article examines the future prevalence of high fuel prices, Sri Lanka’s vulnerability, the impacts on foreign exchange outflows, and the necessary policy measures to mitigate the adverse effects.

High Fuel Prices and the Effects on Sri Lanka’s Import Basket

Given that a quarter of the global energy supply is disrupted, the current energy shock is unprecedented. After the Russian invasion of Ukraine, fuel prices rose above USD 100 per barrel in 2022, and they remained there for roughly 90 days. The high energy cost resulted in a high inflation episode in 2022-2023. As shown in Figure 2, by the end of 2023, energy prices had returned to and stabilised around the pre-invasion level. Notably, Russia’s share of the global energy market was about 11%, while the Hormuz crisis accounts directly for around a quarter of the global energy supply. The energy infrastructure damage so far has also been significant. Thus, high fuel prices may prevail if there is no swift resolution to the crisis. Sri Lanka should consider such a possibility.

Based on 2025 import data, 39.3% of Sri Lanka’s imports, or USD 8.3 Bn, are directly exposed to rising commodity prices. Of this, USD 3.7 Bn are petroleum products, including crude oil, liquid petroleum gas (LPG) and refined fuel. Currently, the fuel price shock is 38.9% when forward-curve movements in Brent futures are factored in. Additionally, energy-intensive base metals and crude oil-based products like plastics and synthetic fibres will be expensive in the world market. These are important intermediate imports for Sri Lanka’s manufacturing sector.

Since natural gas is a key raw material for urea, increasing urea prices, in turn, raises the costs of related agricultural commodities like wheat. As shown in Figure 3, Sri Lanka spent USD 310.1 Mn on fertiliser in 2025, while the import bill for wheat and maize was USD 384.1 Mn. The global increase in fuel prices has boosted demand for biodiesel feedstocks, putting pressure on oil and fat prices, including palm oil used for cooking. Soybean meal and maize are used in poultry feed, so price hikes will have direct nutritional effects on households, mainly through reduced protein intake.

If high prices persist, Sri Lanka’s import bill is likely to increase, as the price response can be inelastic in the short run, which is common for essential commodities with few substitutes. Using 2025 monthly import values and assuming a future fuel price shock equal to the futures market-reflected percentage increase, it is estimated that Sri Lanka’s import bill could rise by USD 1.9 Bn. This means Sri Lanka will incur a 23% increase in imports over the baseline of USD 8.3 Bn. However, the estimated value is at the upper-bound as it is assumed that Sri Lanka would consume the same quantity as in 2025. If high prices persist, adjustments across the entire economy will inevitably necessitate changes in quantity. Demand will contract when a high import price is passed on to consumers. Such a response can be quantified using product-level import demand elasticities. If higher prices lead to reduced demand, Sri Lanka’s import bill could fall by about USD 608 Mn relative to the baseline. However, such a reduction would mainly occur if energy use adjusts in line with longterm demand patterns. This estimate also does not account for wider, economywide adjustments to higher import prices. Under a full demandadjustment scenario, the overall effect would therefore be a net reduction of USD 608 Mn.

Policy Options for Sri Lanka

Although inflationary pressures remain a serious concern for Sri Lanka in the post-Hormuz crisis period, a transparent pass-through of the supply shock to price levels is a suitable policy. While memories of recent high-inflation episodes are still vivid, the Hormuz crisis and the 2022-2024 sovereign debt crises are fundamentally different events. The elevated inflation during 2022-2024 was driven by structural changes in fiscal and monetary policy. Policy implementations such as cost-reflective utility pricing, energy price pass-through, and a floating exchange rate were introduced sequentially, leading to higher inflation. The economy was moving toward reforms to address multiple distortions introduced by a low interest rate and a controlled exchange rate regime.

In the current crisis, significant price shocks from corrective policies are not anticipated. Instead, inflationary pressure resulting from the Hormuz disruption is an external, supply-side shock primarily transmitted through the prices of imported fuel, rather than via domestic policy reversals. Since high airfares and rising shipping fuel costs may impact foreign exchange inflows, managing the reserve position becomes crucial. In this context, restricting fuel consumption is essential while ensuring available fuel is allocated primarily for industrial use.

A fiscal response that suppresses the price signal, such as reducing taxes on certain imported goods, might not be suitable at the moment, as it could boost demand for very costly imported products like fuel. The analysis shows that the import bill can rise substantially if a high price prevails without a quantity adjustment. Notably, under the current framework, such import demands are transmitted to the exchange rate, which can further increase inflationary pressures. However, Sri Lanka should consider easing import licensing schemes for animal and poultry raw materials as global market prices rise, to facilitate imports and secure food supply. Temporarily removing the existing Special Commodity Levy (SCL) on corn imports should also be considered. These products incur small reserve outflows but play a larger role in the country’s protein nutrition.

By Dr Asanka Wijesinghe, Research

Fellow, Institute of Policy Studies of Sri Lanka

The Australian High Commissioner, Matthew Duckworth, hosted a pivotal ‘Thought Leadership’ educational session titled ‘ConnectEd” at his residence in Colombo recently, focusing on disaster recovery efforts following Cyclone Ditwah. This event was part of a series organized by the Australian Trade, Investment & Education division, aimed at fostering discussion on pressing issues in Sri Lanka.

The discussion aimed to reflect this ambition, inviting participants to share their insights and engage with expert speakers. Attendees were encouraged to voice their questions and contribute their perspectives, fostering a collaborative environment for learning and growth.

“As we approach 80 years of bilateral relations between Australia and Sri Lanka, this exchange highlights the enduring value of our partnership built on dialogue and trust. Today, we focus on recovery and rebuilding in the aftermath of Cyclone Ditwah. Effective recovery requires collaboration across various sectors to ensure that we not only address immediate needs but also build resilience over time. I encourage everyone here to actively engage in our discussions, as your expertise is invaluable to shaping a stronger future together, the Australian High Commissioner said in his opening remarks at the event.

He further noted that “this session is being held under Chatham House Rules, which I hope fosters a frank, open, and constructive exchange. A vital aspect here is uniting Australian and Sri Lankan thought leaders, reflecting our longstanding partnership and aligning discussions with Sri Lanka’s broader priorities and ambitions”.

‘ConnectEd’ event was coordinated by Ms. Sandy Seneviratne, Director of Education for the Australian Government based in Colombo. The session brought together key stakeholders to address the challenges and strategies involved in recovering from natural disasters. The dialogue was enriched by insights from notable panelists, Prof. (Ms.) Udayangani Kulatunga, Department of Building Economics at the University of Moratuwa, Sri Lanka, specializing in disaster risk reduction, construction management, and performance measurement and Professor Pat Rajeev, Chair, Department of Civil and Construction Engineering from Swinburne University of Technology in Australia. Lauren Nicholson, Second Secretary for Development at the Australian High Commission moderated the session.

By Claude Gunasekera

SC finds Keheliya, others, guilty of violating FRs of public through corrupt drug procurement deal

Sajith nudges govt. to follow India’s example in giving relief to consumers by slashing taxes on fuel

Expect hot weather until end of May

SLRCS steps in to help Lankans to reconnect with loved ones in West Asia

Minister Jayakody indicted in Colombo High Court over alleged corruption

Court of Appeal orders fresh trial into the murder of TNA MP Raviraj

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News3 days ago

News3 days agoSenior citizens above 70 years to receive March allowances on Thursday (26)

-

Features5 days ago

Features5 days agoTrincomalee oil tank farm: An engineering marvel

-

News1 day ago

News1 day agoEnergy Minister indicted on corruption charges ahead of no-faith motion against him

-

News2 days ago

News2 days agoUS dodges question on AKD’s claim SL denied permission for military aircraft to land

-

Features5 days ago

Features5 days agoThe scientist who was finally heard

-

Business2 days ago

Business2 days agoDialog Unveils Dialog Play Mini with Netflix and Apple TV

-

News3 days ago

News3 days agoCEB Engineers warn public to be prepared for power cuts after New Year

-

Sports1 day ago

Sports1 day agoSLC to hold EGM in April