Business

‘SL’s inflation reduced to single digit levels in 2023 along with restoration of price stability’

The Central Bank of Sri Lanka released the Monetary Policy Report – February 2024 in keeping with the requirements of the Central Bank of Sri Lanka Act, No. 16 of 2023. The content of this Report is mainly based on information that was considered by the Monetary Policy Board of the Central Bank of Sri Lanka in formulating the monetary policy decision during the January 2024 review.

This is the second Monetary Policy Report published by the Central Bank to provide forward-looking insights about the economy, particularly in terms of inflation and economic growth. The Report also aims to provide an assessment of risks to the projections on inflation and economic growth, considering the ongoing and expected developments of domestic and global fronts. Through this report, the Central Bank strives to improve its transparency and accountability by communicating the rationale for the recent monetary policy decisions of the Central Bank.

The key highlights of the Monetary Policy Report – February 2024

Sri Lanka successfully reduced inflation to single-digit levels in 2023 and restored price stability, after containing the historically highest inflation observed in 2022

Supported by corrective policies and structural reforms, economic activity gradually regained momentum in 2023

Monetary policy was relaxed on several occasions since June 2023 as inflation decelerated and inflation expectations remained anchored, while external sector pressures eased

Inflation may deviate from the target in the near term mainly due to the recent tax amendments and supply side disruptions, although such impact is likely to be short-lived.

Inflation is projected to stabilise around the targeted level of 5 per cent (year-on-year) over the medium term

Annual economic growth is expected to turn positive in 2024 and gradually reach its potential over the medium term

The Executive Summary of the Monetary Policy Report – February 2024 is given below:

The Sri Lankan economy progressed on the path towards restored macroeconomic stability in 2023 where inflation was brought down from its highest levels in history observed in 2022, to single-digit levels. Moreover, amidst uncertainties and challenging conditions following the worst crisis in the country’s history, economic activity resumed gradually, supported by the gradual easing of monetary policy and monetary conditions and the revival in the external sector.

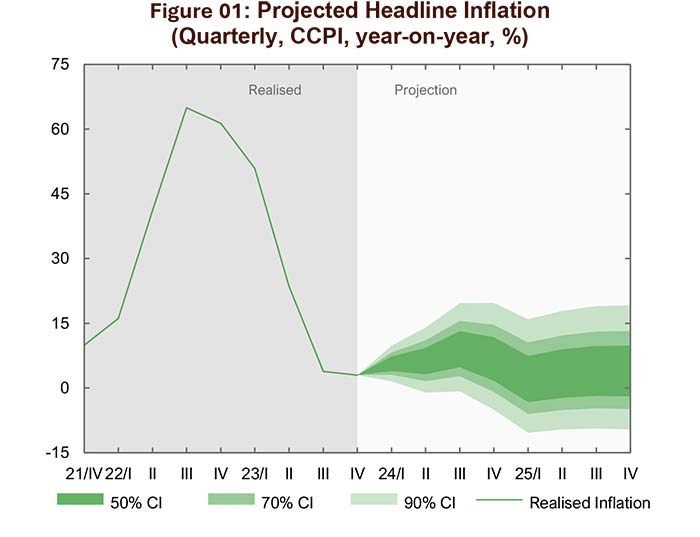

Corrective macroeconomic policies and the implementation of required structural reforms were instrumental in achieving domestic price stability, thereby reinforcing overall macroeconomic stability. Following the rapid disinflation observed in the first half of 2023, year-on-year headline inflation, as measured by the Colombo Consumer Price Index (CCPI), moderated to single-digit levels, dropping to as low as 1.3 per cent in September 2023 within a year since striking its peak.

Inflation accelerated somewhat to 4.0 per cent by end 2023 due to supply-driven factors and the dissipating effect of the favourable base. Core inflation based on the CCPI also moderated significantly during 2023, reflecting subdued underlying demand pressures.

Meanwhile, the domestic economy made a steadfast recovery in 2023 benefitting from the gradual return of overall macroeconomic stability with the implementation of long-term-oriented economic policies by the Government and related authorities. Moreover, the strong commitment to reviving the economy through the adoption of such policies helped improve investor sentiments.

Accordingly, with uncertainties dissipating and improvements observed on all macroeconomic fronts, the economy recorded an expansion in its activity in Q3-2023, after six consecutive quarters of contraction. Supported by the easing of monetary policy and improvement in domestic economic activity, an expansion in credit to the private sector was observed since mid-2023, and this momentum is expected to continue in the period ahead.

The Central Bank continued to relax monetary policy during the second half of 2023 as the economy reached a state of stability with inflation remaining low and inflation expectations remaining anchored, while external sector pressures eased. Following the rapid disinflation process, current inflation remains closer to the inflation target.

However, projections indicate a deviation of inflation from the target, primarily due to amendments to Value Added Tax (VAT) introduced in January 2024, before it retraces towards the target from around end 2024. This uptick in inflation is expected to be short-lived, thereby posing no significant threat to maintaining inflation at the targeted level of 5 per cent over the medium term. On the whole, risks to the near-term inflation projections are skewed to the upside, largely due to supply-side factors, while risks to medium-term inflation projections are balanced. Economic growth is expected to remain

subdued in the short term but is expected to recover gradually towards its potential. Risks to real economic growth projections are skewed to the downside both in the near term as well as in the medium term, as economic activity is susceptible to adverse developments on the global front that affect export recovery, as well as loss in productivity due to outmigration of skilled labour and structural impediments to growth.

(CBSL)

Business

Mercantile Investments strengthens foundation for growth with oversubscribed Rs. 1.1 Bn Rights Issue

Mercantile Investments & Finance PLC (MI Finance) has successfully concluded its Rights Issue, raising Rs. 1.1 billion in new capital. The Issue was oversubscribed, demonstrating a resounding confidence in the company’s strategy, performance, and long-term growth prospects, a company news release said.

As applications outpaced the initial share offering, the strong shareholder participation provided a firm endorsement of MI Finance’s direction and strengthened the foundation on which the company will build its next phase of growth.

The new fund infusion reinforces MI Finance’s capital base, enhances financial flexibility, and supports the company’s regulatory capital position. It also expands MI Finance’s capacity to serve customers and drives growth and expansion plans within Sri Lanka’s financial services sector.

With steadfast focus on long#term value creation, MI Finance is strongly positioned to seize new opportunities, continuing to deliver meaningful returns for customers, shareholders, and the economy.

Gerard Ondaatjie, Managing Director, MI Finance, expressed his appreciation for the continued trust and support placed in the organisation. He said “The strong response to our Rights Issue highlights confidence our shareholders place in MI Finance’s strategy and long-term vision. With a stronger financial foundation, we are well positioned to pursue new opportunities and deliver sustainable growth and lasting value for all stakeholders.”

The successful completion of the Rights Issue showcases MI Finance’s financial strength, the trust it commands and the commitment to sustainable, long-term growth as a stable and progressive financial institution.

First Capital Advisory Services (Pvt) Ltd acted as Advisor and Manager to the Issue, while SSP Corporate Services (Pvt) Ltd served as Registrar to the Issue.

“Maximise value of existing assets rather than build new infrastructure”

By Saman Indrajith ✍️

Hettiarachchige Francis Adhista Sonal Fernando, who recently received an Honorary Professorship in Aviation Management from the University of California, Berkeley (Global), becoming the first Asian and reportedly one of only five recipients worldwide, says Sri Lanka should prioritise aviation technology, airline development and tourism over costly airport expansion projects.

In an interview with the Sunday Island, Prof. Fernando, a former Director of Airport and Aviation Services (Sri Lanka) and an aviation professional with more than two decades of experience, outlined what he described as a more strategic approach to developing the country’s aviation sector.

Having worked across a broad spectrum of aviation disciplines including passenger services, cargo operations, flight Operations, Training, airline management and airport administration, Prof. Fernando said Sri Lanka’s future success depended less on constructing new infrastructure and more on maximising the value of existing assets.

Prof. Fernando said the honorary professorship was awarded in recognition of his contributions to the aviation industry and initiatives undertaken during his tenure at Airport and Aviation Services (Sri Lanka).

“My career has taken me through almost every department of the aviation industry, from checking in passengers and handling cargo to serving as a Pilot captain, flight instructor, chief executive officer and Director of Airport and Aviation Services (AASL). That breadth of experience is relatively uncommon in the industry,” he said.

According to Prof. Fernando, Sri Lanka’s aviation sector recovered rapidly following the COVID-19 pandemic because of efforts to develop specialised aviation services rather than relying solely on passenger traffic.

He said one of the key proposals negotiated during his tenure was the establishment of an air cargo hub at Mattala International Airport, which had the potential to transform the facility into a regional logistics centre.

Another initiative involved plans to establish an international aviation training centre at Jaffna’s Palaly Airport.

Prof. Fernando said discussions had been held with the Royal Jordanian Air Academy, which he described as one of the world’s leading aviation training institutions, to establish operations in Jaffna with several aircraft and a multi-million-dollar investment.

“The project had the potential to attract students from South India, Singapore and other countries while generating valuable foreign exchange earnings for Sri Lanka,” he said.

Prof. Fernando expressed reservations about current proposals for extensive airport expansion projects, arguing that existing airport infrastructure was adequate to meet the country’s needs for the foreseeable future.

“Based on current trends, our airport capacity is sufficient for the next 20 to 25 years. Before spending billions on additional infrastructure, we need to focus on developing the airline industry itself,” he said.

Drawing comparisons with global aviation success stories, he pointed to Qatar’s strategy of first building a strong national carrier before undertaking major airport expansion.

“Resources would be better invested in strengthening SriLankan Airlines, improving tourism infrastructure and enhancing security and discipline across the country,” he said.

Prof. Fernando also criticised what he described as the increasing “militarisation” of civil aviation administration, arguing that airports should provide a welcoming and passenger-friendly environment.

“Civil aviation should be open and stress-free. Airports are the first impression visitors receive of a country, and the experience should reflect that,” he said.

He said efforts had previously been made to create a more accessible and less intimidating atmosphere at the country’s main international airport.

The aviation expert also raised concerns about the Harassment and Humiliation treatment to some outbound travellers, particularly passengers who are travelling on a visit and holiday,

According to Prof. Fernando, passengers who possess valid travel documents should not be prevented from travelling based on assumptions regarding their intentions.

“If a traveller has a valid passport, visa and ticket, the authority to stop that person lies with airline staff and Immigration. Decisions should not be based on appearance or social background,” he said.

On tourism, Prof. Fernando said Sri Lanka should avoid attempting to replicate the models adopted by destinations such as Dubai and instead develop an identity rooted in its own strengths as an island nation.

“We cannot simply copy Dubai. The Maldives has succeeded not only because of its airport infrastructure but because of its discipline, security and the importance it places on visitors,” he said.

He argued that tourism promotion campaigns should focus more heavily on attracting high-spending travellers by showcasing the country’s premium tourism offerings.

“We should be promoting our luxury hospitality sector, gems, business-class travel and other high-value experiences. That is how we attract visitors who contribute significantly to the economy,” he said.

Looking ahead, Prof. Fernando said investment priorities should centre on advanced aviation technologies rather than additional buildings.

He cited Category III-C (CAT III-C) landing systems as an example of technology capable of significantly enhancing operational efficiency by enabling aircraft to land safely even in extremely poor visibility conditions.

“Such technology can improve airport performance and international competitiveness far more effectively than constructing another terminal building,” he said.

Prof. Fernando said the long-term success of Sri Lanka’s aviation industry would depend on informed leadership and strategic planning.

“What the industry needs are leaders who understand aviation and are committed to its development, rather than viewing it solely through the lens of construction and infrastructure projects,” he said.

Super Stars VFC emerged champions of the 21st consecutive nine-a-side football tournament organised by the Sri Lanka Soccer Masters’ Association, while Galle Legends FC finished as runners-up in the veteran football competition held recently at the Shalika Grounds, Narahenpita, and Campbell Park, Borella.

Association President Irshad Haq said the annual tournament attracted 34 teams from across the country and featured a total of 71 matches, underscoring the continued popularity of veteran football in Sri Lanka.

He noted that the tournament provided a competitive platform for former footballers to remain actively involved in the sport while fostering camaraderie among veteran players. Haq added that many former national-level footballers and recently retired players participated in the event, enhancing the quality of competition and offering spectators an opportunity to witness traditional football skills displayed at a high standard.

Runners up team with the Chief Guest

General Secretary Yoga Cruze said the tournament has become a landmark event on the local football calendar and continues to celebrate the contributions of former players to the sport. He said the Association remains committed to promoting veteran football and preserving the legacy of past football greats.

Tournament Committee Chairman P.G.P. Pieris said prize distribution and several special events were held during the tournament finale. The champions received cash awards together with a permanent trophy and the coveted challenge trophy, while the runners-up were also presented with cash prizes.

A special attraction at the event was an exhibition match involving veteran footballers over the age of 60. The match ended in a draw and the winner was decided by a coin toss.

Pieris said the tournament was organised not only to maintain competitive football among veterans but also to honour past legends of the game while providing fans with an entertaining and high-quality sporting spectacle.

Champions – Super Stars VFC: YML Jayathunga, Mohamed Iqbal, LAP Lakshitha, JR Pradeep Perera, M Mohamed Asmeer, SR Susil Pradeep, Mohamed Rikas, PR Sanjeewa Perera, MKJ Priyantha Perera, K Aruna Sampath, HMVR Perera (goalkeeper), RT Imtiyaz Raheem and WE Sarath de Alwis. Team Manager: Nazar Mohideen.

Runners-up – Galle Legends FC: PHN Pushpakumara, WA Nishantha, MS Fargan, BG Shiwanka, BPD Sudesh, MP Pradeep, HLR Jayalath, K Sirantha Kumara, ADD de Silva, AKR Priyanga and GAMA Indrajith.

Typhoon Noul makes landfall in China, with hundreds of thousands evacuated

Colombo Kaps down Dambulla Sixers by 21 runs

Kandy Royals win by 11 runs

Showers will occur in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Govt. launches EPF, ETF shake-up

SLPI concerned over the proposed Chartered Institute of Media Professionals of Sri Lanka

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Midweek Review5 days ago

Midweek Review5 days agoThree high-profile alleged suicides shaping key investigations

-

Features19 hours ago

Features19 hours agoMBS: The Man of the Last Laugh

-

News2 days ago

News2 days agoFort Magistrate orders arrest of MP Archchuna

-

Editorial2 days ago

Editorial2 days agoAn indictment of all parties

-

News5 days ago

News5 days agoCustoms asked to resume probe or face legal action

-

Features19 hours ago

Features19 hours agoA Landmark Gathering of Minds: The Ceylon Journal Roundtable Revives the Spirit of Intellectual Dialogue

-

Editorial6 days ago

Welcome bid to tackle rolling death traps

-

Life style18 hours ago

Life style18 hours agoA proud Sri Lankan voice in Australian Parliament