Business

Palm oil ban in Sri Lanka: Is it sustainable?

By Erandathie Pathiraja

Sri Lanka’s edible oil market has received considerable attention in recent weeks due to a series of events: the banning of palm oil importation in a bid to promote the coconut industry, detection of aflatoxins in imported coconut oil, importation of coconut kernel chips, issuing license for palm oil imports, and banning of oil palm cultivation.

The edible oil industry is important for Sri Lanka. Oils and fats are a major constituent of the typical Sri Lankan diet and a raw material in manufacturing, in particular the food manufacturing industry. According to the latest available data, there are around 5,057 establishments employing 332,828 workers in the formal food manufacturing sector which generate an annual output of approximately LKR 1.4 billion. This blog assesses the local edible oil market and its potential for import substitution.

Sri Lanka’s Edible Oil Market

The demand for domestic edible oils comes from two segments: households and industries. Data from the 2016 Household Income and Expenditure Survey (HIES) of the Department of Census and Statistics (DCS) show that an average household consumes 1.6 litres of fats and oils per month and the annual consumer demand is around 96,249 MT, with coconut oil being the main source of edible oil (Figure 1). Industrial demand in 2020 can be approximated to 167,372 MT.

This demand for edible oils in the country is met by locally produced oils as well as imported oils. Coconut oil and palm oil are the local edible oil sources. In 2020, total edible oil production was 44,326 MT. Coconut oil production was 19,759 MT which depends on annual coconut production. Crude palm oil and palm kernel oil production was 24, 567 according to the Coconut Development Authority (CDA). According to the CDA, the quantity of imported fats and oils in 2020 was 219,295 MT. A range of edible oils are imported to meet industrial demand and partially to meet household demand (Figure 2). The foreign exchange outflow in 2020 was LKR 37,378 million for edible oils imports.

Total edible oil supply during 2020 was 263, 621 MT both from local production (44, 326 MT) and imports (219,295). Around 83% of the requirement is met by imports, and industrial demand is nearly two-thirds of the total demand (Figure 3).

The available data show that it is difficult to meet the edible oil demand from the local supply. The average coconut production during the last five years was around 2,792 million nuts. Nearly 65-70% of the produce is consumed as fresh coconuts (1,800 million nuts). Processing industries utilise the remaining coconuts (around 1,000 million). Around 108,108 MT of coconut oil can be produced from 1,000 million nuts at the expense of export industries, yet 155,513 MT of excess demand has to be met. Palm oil is cultivated in 12,000 Ha which is expected to produce nearly 48,000 MT. Together, coconut and palm oil can be expected to supply 156,108 MT of edible oil, which is still short of 107,513 MT of oil required to meet the consumer and industry demand.

Way Forward

Given the current context, Sri Lanka cannot meet its edible oil demand as the coconut supply is not sufficient to meet the edible oil demand, and expansion of production is difficult in the short term. Imported edible oils are an essential ingredient in food manufacturing due to its unique properties and low cost. Therefore, facilitating importation is required to meet the local demand.

Sri Lanka spends around LKR 37 billion for edible oil imports, and looking for alternatives is a sensible solution. Rice bran oil is a potential byproduct of paddy milling and it does not demand extra land for cultivation. Sri Lanka has to invest in utilising this potential resource. Measures to achieve optimum productivity from existing coconut lands are vital to reduce oil imports.

By Hiran H. Senewiratne

The rupee has stabilised somewhat in recent weeks reflecting the impact of policy measures that have been taken thus far, Central Bank Governor Dr Nandalal Weerasinghe said.

“We will continue to closely monitor domestic and global developments for emerging risks and expect the monetary policy tightening carried out previously to transmit to the economy in the period ahead, Central Bank Governor Dr Weerasinghe said at the monthly monetary policy review meeting held at Central Bank head office yesterday.

He said that the CBSL stands ready to take appropriate measures to ensure that inflation stabilises around the 5 percent target, while supporting the economy to reach its potential over the medium term.

Amid those developments the Central Bank kept its Overnight Policy Rate (OPR) unchanged at 8.75 percent, it said in a statement, after considering the evolving conditions and outlook on the domestic and global fronts.

Dr Weerasinghe added: ‘Renewed tensions in the Middle East have resulted in a surge in global commodity prices, particularly petroleum. These developments are likely to dampen global economic prospects with potential spillover.

‘The current low level of inflation, at 1.6 percent year -on-year in February 2026, relative to the target of 5 percent provides sufficient space to accommodate the impact of higher energy prices and their spillovers on inflation.

‘Headline inflation accelerated to 6.8 percent in June 2026, mainly due to higher domestic energy and food prices.

‘Headline inflation is expected to remain above the target of 5% in the near term before gradually returning to the target level. Core inflation is also expected to increase and remain around the headline inflation target.

‘The Board arrived at the decision to maintain the overnight policy rate after carefully considering the evolving conditions and outlook on the domestic and global fronts.

‘Renewed tensions in the Middle East have resulted in a surge in global commodity prices, particularly petroleum. These developments are likely to dampen global economic prospects with potential spillovers to the domestic economy through multiple channels.

‘The monetary policy tightening in May 2026 and its gradual transmission to the real economy are expected to moderate credit growth and the buildup of demand pressures going forward.

‘The pressure on the external sector caused by the Middle East conflict has eased somewhat, although the outlook remains uncertain due to renewed tensions.

‘Since April 2026, the external current account recorded a deficit, mainly because higher fuel import costs widened the merchandise trade deficit and tourism earnings slowed down.

‘Going forward, import demand, including demand for motor vehicles, is expected to reduce in response to recent policy measures.

‘Meanwhile, workers’ remittances have remained strong so far in 2026. Gross Official Reserves stood at USD 6.45 bn at the end of June 2026, amid foreign debt service payments.’

By Ifham Nizam

The mosquito that spreads dengue is tiny. The financial burden it leaves behind is anything but.

As Sri Lanka grapples with its worst dengue outbreak in nearly a decade, the country’s free public healthcare system is absorbing a mounting financial shock that experts say could run into billions of rupees, even as the human toll continues to rise.

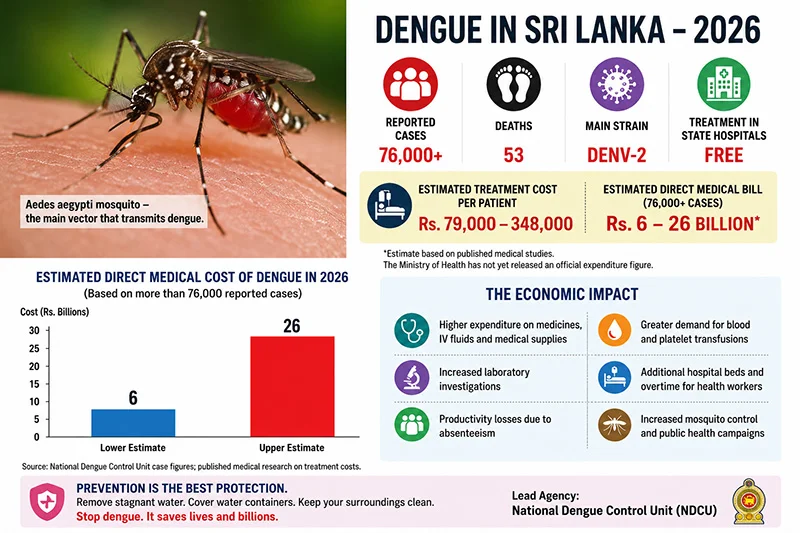

According to the National Dengue Control Unit (NDCU), more than 76,000 dengue infections and 53 deaths have been reported so far this year, making 2026 one of the most challenging years for dengue control in recent history.

The NDCU has warned that the outbreak is being driven largely by the highly virulent DENV-2 strain, while persistent rainfall, poor waste management and mosquito breeding in urban and semi-urban areas continue to fuel transmission.

Although the Ministry of Health has yet to publish an official estimate of the cost of treating dengue patients, the economic implications are becoming increasingly evident.

Published medical research estimates that treating a dengue patient costs between USD 239 and USD 1,056, depending on the severity of the illness. At an exchange rate of around Rs. 330 to the US dollar, this translates to approximately Rs. 79,000 to Rs. 348,000 per patient.

Applied to the more than 76,000 reported cases, the theoretical direct medical cost ranges from Rs. 6 billion to more than Rs. 26 billion. While many patients are treated as outpatients and therefore incur lower costs, the estimates underline the immense financial pressure being placed on Sri Lanka’s publicly funded healthcare system.

The National Dengue Control Unit has repeatedly urged the public to eliminate mosquito breeding sites, warning that hospitals alone cannot contain the outbreak without sustained community participation.

Health officials have intensified countrywide inspections, awareness campaigns and vector-control programmes as case numbers continue to climb.

Officials say hospitals have expanded dengue wards, increased bed capacity and deployed additional medical and nursing staff to cope with the surge in admissions.

The government has also mobilised Air Force drones to identify inaccessible mosquito breeding grounds while strengthening surveillance operations across high-risk districts.

The financial impact extends beyond the Ministry of Health. Families lose income when wage earners fall ill or parents stay home to care for infected children. Businesses suffer productivity losses, while schools experience increased absenteeism during peak transmission periods.

Sri Lanka’s previous major dengue epidemic in 2017 was estimated to have cost around Rs. 1.94 billion in healthcare and outbreak-control expenditure. With inflation, higher pharmaceutical prices and increased operational costs since then, health economists believe the financial burden of the current outbreak is likely to be substantially greater.

The outbreak also raises broader questions about climate resilience and public investment. Dengue is increasingly being recognised not merely as a seasonal health issue but as an economic challenge capable of straining government finances and slowing productivity.

For the National Dengue Control Unit, the message remains simple: prevention is far cheaper than treatment.

Every breeding site destroyed, every community clean-up campaign conducted and every household inspection completed reduces the need for costly hospital care.

As the monsoon continues to create favourable conditions for mosquito breeding, the NDCU warns that sustained public vigilance will determine whether the country’s health bill continues to climb—or begins to fall.

Business

Shantha Bandara reappointed SLCPI president as Chamber advances regulatory reform and patient access

The Sri Lanka Chamber of the Pharmaceutical Industry (SLCPI) announced the reappointment of Sunshine Healthcare Lanka Ltd. Director and Chief Executive Officer Shantha Bandara as its President for the 2026/27 term at the Chamber’s 65th Annual General Meeting held at Cinnamon Grand Colombo.

The event was graced by Dr. Hansaka Wijemuni, Deputy Minister of Health, as Chief Guest, together with government representatives, healthcare partners, past presidents, member companies and other industry stakeholders.

Bandara’s reappointment provides continuity to a reform-oriented agenda that has strengthened the Chamber’s governance, ethical standards and engagement with policymakers and regulators. His renewed mandate will focus on converting the progress made during 2025/26 into practical regulatory improvements that support the availability, accessibility and affordability of quality medicines in Sri Lanka.

SLCPI represents more than 70 pharmaceutical importers, manufacturers, distributors and retailers. Its members account for over 90% of Sri Lanka’s private pharmaceutical market, while the wider industry directly employs more than 80,000 people and indirectly supports nearly 400,000.

Reflecting on the past year, Bandara said the industry had operated amid sustained domestic and global pressure. Exchange-rate volatility, disruptions to international shipping routes, rising freight, insurance, fuel and electricity costs, and constrained consumer purchasing power placed significant pressure on pharmaceutical supply chains and business viability.

Despite these challenges, SLCPI continued to engage constructively with the Ministry of Health, the National Medicines Regulatory Authority and other stakeholders, presenting evidence-based recommendations on pharmaceutical pricing, import licence renewals and continuity of supply.

A major achievement during Bandara’s first term was the adoption of new Articles of Association following extensive consultation, legal review and member engagement. The revised Articles provide a stronger constitutional foundation for the Chamber, clarify governance structures and reinforce member rights and responsibilities.

More than 4,200 Israelis storm Al-Aqsa Mosque in Jerusalem

Feroza, Amin, Sandhu shine as Pakistan go 1-0 up against Sri Lanka

Colombo District Waste Management subcommittee convenes at Parliament

Government to coordinate Kotte Rajamaha Viharaya Sri Dalada Maha Perahera

Taskin Ahmed withdraws from LPL to prepare for Australia tour

US and Saudi Arabia announce nuclear cooperation deal

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features5 days ago

Features5 days agoTwo memorable excerpts from a former SLAF commander’s memoir

-

Business5 days ago

Business5 days ago‘Giving up was never an option’: The fisherman who fought back after losing millions in SL

-

Latest News5 days ago

Latest News5 days agoDavis cup Asia/Oceania Group IV 2026 to be held in Colombo from 20th to 25th July

-

Features5 days ago

Features5 days agoErdoğan’s New Republic

-

Life style5 days ago

Life style5 days agoTaste of the Swiss Alps comes to Colombo

-

News6 days ago

News6 days agoEvidence recorded in money laundering case against Yoshitha Rajapaksa

-

Midweek Review2 days ago

Midweek Review2 days agoThree high-profile alleged suicides shaping key investigations

-

News6 days ago

News6 days agoDengue outbreak gallops ahead: Infections surpasses 73,455, leaving 50 dead