Business

‘NSB posts exceptional results amidst woes’

Generating a record-breaking profit for the year NSB records sensational performance beating all the odds during a pandemic which had a wide-ranging impact of the Bank, employees, customers and economy. our continued focus on financial resilience enables us to remain strong and achieve a solid performance. The performance of the Bank over the year was characterized by strength and resilience. The Bank recorded its highest ever profit for the year with a Profit Before Tax (PBT) of Rs. 28.4Bn which marks an increase of 81.4% from Rs. 15.6Bn recorded in the same period last year, while the PAT was Rs. 22.1Bn, with an increase of 118.8% from Rs. 10.1Bn in 2020.

Gross Income of the Bank grew by 5.8% to Rs. 134.9 Bn during the year from Rs. 127.5Bn recorded in the corresponding period, last year. During the period under review, the interest income has increased by 7.3% to reach Rs. 131.4Bn, while the interest expense has decreased by 12.3% to Rs. 76.8Bn due to the prevailing lower interest rate regime which leads to lower interest expenses for the deposits as well as borrowings despite the substantial growth in the deposit base during the period considered. The increase in interest income together with the considerable reduction in interest expenses supported Net Interest Income (NII) to surge by 56.6% to Rs. 54.6Bn against Rs. 34.9Bn stood during the same period last year. Consequently, Net Interest Margin (NIM) clocked in 3.71% at the end of 2021 recording the highest during the ten years period and higher against the 2.77% reported as at the same period last year.

Net Fee and commission income grew by 11.2% to Rs. 2.8Bn from Rs. 2.6Bn mainly driven by the increase in fee and commission income due to conversion/renewal of the existing loans to reduced interest rates as well as increased foreign remittances and coupled with fees generated through digital platforms to where the customers shifted under social distancing and health guidelines. The increase both in NII and Non-Interest Income led the total Operating Income to record a rise of 45.6% to Rs. 57.9Bn at the end of year 2021. Operating expenses during the period of 2021, rose by 23.3% to Rs. 19.1Bn compared to the corresponding period of the previous year, which is mainly attributable to the increased personnel expenses owing to the provisions made for the Collective Agreement due in 2021. Meanwhile, the Bank’s cost to income ratio decreased to 33.29% at the end of the year 2021 compared to 39.28% reported in the year 2020.

Impairment charges during the period under review decreased to Rs. 4.3Bn by 11.7% compared to the same period last year. The Bank has carried out a prudent approach when calculating the impairment charges, considering that the outbreak of Covid-19 has caused disruption in business and economic activities, along with the uncertainty and volatility prevailing in the global and local economy and other holistic factors. However, the gross NPL ratio increased to 2.97% compared to 2.79% reported in the same period last year mainly owing to the to the reclassification of some loans and advances under debt and other instruments.

The Bank generated a Return on Equity (RoE) of 33.92% and Return on Assets (RoA) of 1.93% at the end of 2021. The total asset base of the Bank grew at 15.8% to reach Rs. 1.58Tn against the Rs.1.36 Tn reported as at the end of December 2020 mainly contributed by the growth in customer deposits, which increased by 15.5% to Rs. 1.43 Tn compared to the deposit base reported at the end of December 2020. There is an increase in the pattern of saving of the customers despite the impact of Covid 19 on the economy and lifestyle of the customers. During the period under review, the Bank has mobilized Rs.192.6 Bn and continued the momentum of mobilizing low-cost funds during the period under review by mobilizing Rs.46.7 Bn.

Loans and advances witnessed only an increase of 4.3% to Rs. 538.9Bn over the last year December figure of Rs. 516.8Bn underpinned by the conversion of Rs.59.4 Bn loans and advances under the “Debt Instruments”. However, without taking the converted loans into consideration, the total loans and advances demonstrated a growth of 17.8%, triggered by personal loans as well as loans to State Owned Enterprises (SOEs).

Complying with the direction of the Central Bank of Sri Lanka (CBSL), the capital position of the Bank remained strong and stood well above the revised minimum statutory requirements imposed by the regulator consequent to the COVID-19 pandemic. The Tier 1 Capital and Total Capital ratios stood at 18.60% and 20.83% respectively at the end of 2021 well above the statutory requirements of 8.00% and 12.00% respectively. The leverage ratio of 8.92% too was well above the minimum requirement of 3.0%.

To foster a saving culture among all Sri Lankans that comes from all segments of the society, and work towards financial and digital inclusion, we focus on strengthening our digital as well as physical footprint. the Bank has increased its branch network to 261 branches along with 292 ATMS and 92 CRMs as of 31.12.2021. Further, the Bank has introduced a mobile payment system under the brand name of “NSB Pay” App to encourage customers to accomplish their daily banking needs safely and efficiently providing an uninterrupted service to the customers during these difficult times.

The ICRA Lanka Limited has assigned the Bank with the issuer rating of [SL] AAA with Stable Outlook, on the back of 100% ownership of Government of Sri Lanka (GoSL) and the 100% explicit guarantee provided by the GoSL for the money deposited with the Bank and the interest thereof through the National Savings Bank Act. The Bank has been awarded the 5th most valuable brand in Sri Lanka by the Brand Finance Lanka Ltd with a brand value of USD 166Mn. The Bank has also been recognized as one of the 10 Most Admired Companies in Sri Lanka in 2021 by the International Chamber of Commerce Sri Lanka (ICCSL), in collaboration with the Chartered Institute of Management Accountants (CIMA).

NSB contributes immensely to the wellbeing of the citizens of the country and the development of the economy as one of the biggest lenders in the Banking sector. Whilst facilitating the growth in national home ownership, opening a pathway towards economic security and mobility for thousands of customers, the Bank operates as one of the biggest lenders to the Government and the second largest holder of Government securities. Further, the Bank is an enthusiastic partner in the Government’s long-term infrastructure and socioeconomic development projects, in addition to contributing to the General Treasury by way of taxes, levies, fees, and dividends.

The opening weeks of 2026 are offering a glimmer of cautious hope for the business community weary from years of economic turbulence and steep financing costs. The Central Bank’s latest weekly economic indicators signal more than just macroeconomic stability. They point to early signs of a long-awaited trend; a measurable dip in borrowing costs.

“If sustained, this shift could transform steady growth into a robust, investment-led expansion,” a senior economist told The Island Financial Review.

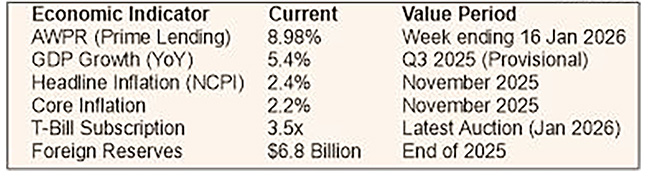

The benchmark Average Weighted Prime Lending Rate (AWPR) declined by 21 basis points to 8.98% for the week ending 16 January, according to the Central Bank.

“For entrepreneurs and CEOs, this is not just another statistic. It could mean the difference between postponing an expansion and hiring new staff. Across boardrooms, the hope is that this marks the start of a sustained downward trend that holds through 2026,” he said.

When asked about the instances where Treasury Bills are not fully subscribed by the investors, he replied,” Treasury Bill yields remained broadly stable, with only minimal movement across 91-day, 182-day, and 364-day tenors. Strong demand was clear, with the latest T-Bill auction oversubscribed by about 3.5 times. This sovereign-level stability creates room for the gradual easing of commercial lending rates, allowing the Central Bank to nurture a more growth-supportive monetary policy.”

Replying to a question on how he views the inflation numbers in this context, he said, “The year-on-year increase in the National Consumer Price Index stood at a manageable 2.4% in November, with core inflation at 2.2%. Such an environment should allow interest rates to fall without sparking a price spiral. For businesses, it means the real cost of borrowing adjusted for inflation, and it is becoming more favourable for them. While consumers still face weekly price shifts in vegetables and fish, the broader disinflation trend gives policymakers leeway to keep credit affordable.”

Referring to the growth trajectory, he mentioned, “With GDP growth provisionally at 5.4% in the third quarter of 2025 and Purchasing Managers’ Indices signalling expansion in both manufacturing and services, the economy is in a growth phase. However, to accelerate this momentum businesses need capital at lower cost to modernise machinery, boost export capacity, and spur innovation. Affordable credit is, therefore, not merely helpful, it is essential to shift growth into a higher gear.”

In conclusion , he said,” The coming months will be watched closely, because for Sri Lankan businesses, a sustained decline in borrowing costs isn’t just an indicator; it’s the foundation for growth. There’s hope that this easing in the cost of money will prevail through most of the year.”

By Sanath Nanayakkare ✍️

Mercantile Investments & Finance PLC has expanded its national footprint to 90 branches with a new opening in Tangalle, reinforcing its commitment to community accessibility. The trusted non-bank financial institution, with over 60 years of service, now supports diverse communities across Sri Lanka with leasing, deposits, gold loans, and tailored lending.

This physical expansion aligns with significant financial growth. The company recently surpassed an LKR 100 billion asset base, with its lending portfolio doubling to Rs. 75 billion and deposits growing to Rs. 51 billion, reflecting strong customer trust. It maintains a low NPL ratio of 4.65%.

Chief Operating Officer Laksanda Gunawardena stated the branch network is vital for building trust, complemented by ongoing digital investments. Managing Director Gerard Ondaatjie linked the growth to six decades of safeguarding depositor interests.

With strategic plans extending to 2027, Mercantile Investments aims to convert its scale into sustained competitive advantage, supporting both customers and Sri Lanka’s economic progress.

A glaring omission in the Board of Investment’s (BOI) Negative List is allowing duty-free imports of fully fabricated aluminium products, severely undercutting Sri Lanka’s domestic manufacturers, according to a leading industry association.

The Aluminium Fabricators Association of Sri Lanka (AFASL) warns that this policy failure is threatening tens of thousands of jobs, draining foreign exchange, and stifling local industrial capacity.

“This has created an uneven playing field,” the AFASL said, adding that BOI-approved developers gain cost advantages over local fabricators, while government revenue and foreign exchange are lost through imports of products already made in Sri Lanka.

The core of the issue lies in a critical policy gap. While raw aluminium extrusions are protected on the BOI’s Negative List – which restricts duty-free imports – finished products like doors, windows, and façade systems are not. Furthermore, the list’s lack of specific Harmonised System (HS) codes allows these finished items to be imported under varying descriptions, slipping through duty-free.

This loophole, the AFASL argues, disadvantages a robust local industry that employs over 30,000 people directly and indirectly. Supported by five local extrusion manufacturers, a skilled NVQ-certified workforce, and a well-established glass-processing sector, the industry has been operational since the 1980s.

The association highlights that the damage extends beyond fabrication. The imported systems often include glass, hinges, locks, and accessories, all of which are produced locally, thereby cutting off demand across the entire domestic value chain. Small and medium-sized enterprises (SMEs), a segment government policy aims to support, are feeling the impact most acutely.

Since May 2025, the AFASL has been engaged in talks with the BOI, Finance Ministry, and Industries Ministry. Their key demand is to include specific HS codes on the Negative List and to list fabricated aluminium doors, windows, and curtain wall systems under HS Code 7610 to close the loophole.

While welcoming supportive recommendations from the Industries Ministry to add these products to an updated Negative List, the AFASL sounded a note of caution. It warned that proposed reductions in the CESS levy could further incentivise imports, undermining the sector’s recovery from the economic crisis.

The association also pointed to an inequity in the current framework. With most subsidies withdrawn, BOI-registered property developers continue to benefit from duty-free imports, while locally made products remain subject to heavy taxes for the general population.

The AFASL is urging policymakers to align investment incentives with national industrial policy, protect domestic manufacturing, and ensure fair competition across the construction supply chain to safeguard an industry vital to Sri Lanka’s economy.

By Sanath Nanayakkare ✍️

At least six killed in Pakistan as fire rips through Karachi shopping mall

Chile declares ‘state of catastrophe’ as deadly wildfires menace cities

At least 21 killed in Spain after crash involving high-speed trains

U – 19 World Cup: Mahboob, Sadat star for Afghanistan against West Indies

U – 19 World Cup: Rew, Mayes lead England to victory

Mitchell, Phillips centuries trump Kohli’s as New Zealand win first-ever ODI series in India

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Editorial1 day ago

Editorial1 day agoIllusory rule of law

-

News2 days ago

News2 days agoUNDP’s assessment confirms widespread economic fallout from Cyclone Ditwah

-

Business4 days ago

Business4 days agoKoaloo.Fi and Stredge forge strategic partnership to offer businesses sustainable supply chain solutions

-

Editorial2 days ago

Editorial2 days agoCrime and cops

-

Features1 day ago

Features1 day agoDaydreams on a winter’s day

-

Editorial3 days ago

Editorial3 days agoThe Chakka Clash

-

Features1 day ago

Features1 day agoSurprise move of both the Minister and myself from Agriculture to Education

-

Business4 days ago

Business4 days agoSLT MOBITEL and Fintelex empower farmers with the launch of Yaya Agro App