Business

LOLC General Insurance and Ananda College OBA sign MoU to promote the first ever Lifestyle Motor Insurance Product ‘Honours’

LOLC General Insurance PLC (LOLC GI), recognised as the fastest-growing General Insurance company within the large and medium companies, has entered into a Memorandum of Understanding (MoU) with the Ananda College Old Boys’ Association (ACOBA) to enable members to promote the unique, first-ever lifestyle motor insurance product, the ‘Honours’ loyalty programme.

The signing of the MoU took place recently during a press conference at the Ananda College Sath Mahala premises. Gracing the occasion were Kithsiri Gunawardena, Group Chief Operating Officer of LOLC Group and Director/Chief Executive Officer of LOLC General Insurance PLC and Bimal Wijayasinghe, Executive President of Old Boy Association of Ananda College.

The ‘Honours’ loyalty programme with rich rewards is applicable for all LOLC GI Motor Policy holders.

Ananda College Old Boys’ Association (OBA) was established in 1908 and includes over 10,000 members. Based on the agreement, OBA members will endorse LOLC GI’s new motor lifestyle loyalty program ‘Honours’ showcasing its seamless and delightful experiences which offer real value.

The Loyalty programme is structured across four (04) tiers with membership levels of Bronze, Silver, Gold and Platinum offering holders continuous rewards and benefits every day. All LOLC GI Motor Policyholders will receive valuable discounts and benefits through the loyalty partner network – Channel 17 (CH17).

Customers can accumulate ‘Honours’ loyalty points while transacting with any of the merchants within the network and are free to redeem points through selective partners or during their policy renewal. Additionally, ‘Honours’ enables its policyholders to donate the accumulated points to LOLC’s humanitarian programme.

LOLC General Insurance PLC is a fully owned subsidiary of the LOLC Group, among Sri Lanka’s largest and most diversified conglomerates with operations in 22 countries in Asia, Africa and the Middle East. At present, LOLC General Insurance is classified as a large-sized company and the 5th largest General Insurer and 4th largest Motor Insurer in Sri Lanka.

The company was recognized as the fastest to achieve the Rs. 7 Billion milestones within the General Insurance industry. During 2021, LOLC General Insurance recorded a premium income growth of 19.2% which was the highest growth recorded by a mid/large sized company in the General Insurance industry and reported paid claims of Rs. 2.5 Billion.

Reaffirming its people-centric approaches demonstrated during the past few years, LOLC General has received multiple awards including for ‘Best General Insurance Company of the Year’ at the 3rd Emerging Asia Insurance Awards 2021, Asia’s Best Employer Brand Awards 2021, and was also ranked amongst the Top Nation’s Most Popular Service Providers by LMD.

Cargills Food and Beverage Ltd. through its brands KIST and Knuckles, has signed a Memorandum of Understanding (MoU) with Clean Ocean Force Lanka (COF) to adopt Crow Island Beach for one year, reinforcing its commitment to long-term coastal conservation in Sri Lanka.

This pioneering initiative is designed to protect and preserve the coastal environment through several key measures, including the removal of plastic and other pollutants from the beach and surrounding coastal area. As part of the adoption programme, the beach will be maintained daily with the support of dedicated beach caretakers, while also supporting their livelihoods by providing meaningful income opportunities.

Marking the partnership and in celebration of World Recycling Day, a coastal clean-up programme was conducted at Crow Island Beach to remove plastic and other manmade pollutants. Volunteers from Cargills, Clean Ocean Force Lanka, the Interact Club of Colombo, the Colombo Municipal Council and the Women’s Force of COF Negombo (Sri Vimukthi Association) participated in the clean-up with support from the Marine Environment Protection Authority (MEPA), the Sri Lanka Police Environmental Division and the Ministry of Local Government and Environment as well as the Crow Island Beach Park Society.

Jerome Fernando, Chairman & Co-founder of Clean Ocean Force Lanka said that, “Marine & Coast Conservation demands a unified front. Our unique Public-Private-People Partnership model is the cornerstone of our mission, and today, we are thrilled to welcome Cargills (Ceylon) PLC as a vital partner in this journey adopting the Crow Island Beach for the next one year. This collaboration will not only amplify our efforts to eliminate plastic and manmade pollutants from our beaches, but also reinforce our commitment to empowering marginalized communities through sustainable livelihood opportunities. Cargills’ deep-rooted dedication to environmental sustainability and community wellbeing perfectly aligns with our vision.”

Jagath Gunasekara, General Manager of MEPA added, “The Marine Environment Protection Authority consistently promotes active private sector engagement in marine and coastal conservation, as well as pollution control initiatives. This approach aligns closely with our Beach Caretaker Programme. We are pleased to collaborate with Cargills (Ceylon) PLC in the adoption of Crow Island Beach through our long-standing partnership with Clean Ocean Force Lanka.”

During the event, Knuckles also launched Sri Lanka’s first tethered bottle cap, introducing a packaging innovation aimed at improving plastic waste management and supporting recycling efforts. The tethered cap is designed to remain attached to the bottle after opening, reducing the likelihood of caps being discarded separately. Bottle caps are among the most commonly littered plastic items globally and frequently enter landfills and waterways due to their small size and low collection rates.

Speaking on the initiative, Arjuna Kumarasinghe, Managing Director of Cargills Food & Beverage Ltd., said, “Cargills has always believed in taking responsibility for the communities and environments around us. By adopting Crow Island Beach, we’re able to work closely with our partners and local volunteers to protect this part of our coastline. Launching the tethered bottle cap is another way we’re addressing plastic waste and making recycling easier for everyone.”

The Central Bank is keeping its overnight policy rates unchanged, adopting a cautious stance amid uncertainty over the inflationary impact of energy prices due to the Middle East crisis.

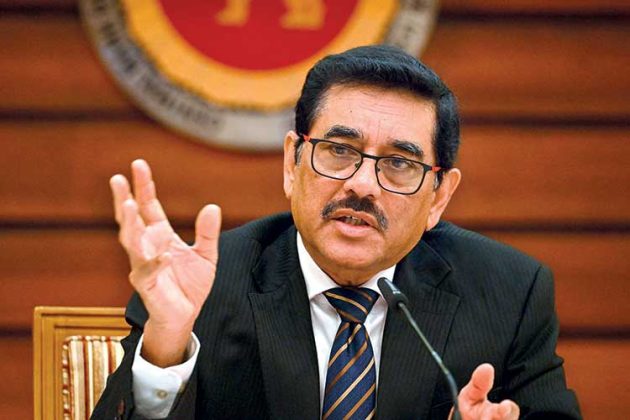

‘We maintained the overnight policy rate at 7.75 percent, considering low inflation and a restrained approach on the fallout of the US-Israeli war on Iran, Central Bank Governor Dr Nandalal Weerasinghe said.

The Governor made these remarks yesterday at a press briefing held at the Central Bank head office in Colombo to announce the monthly monetary policy stance.

Dr Weerasinghe added: ‘Inflation is now expected to reach the Central Bank’s target of 5 percent in the second quarter of 2026, after Sri Lanka raised fuel prices by about 35 percent this month.

‘However, spillovers from the ongoing conflict could weigh on domestic economic activity in the period ahead should the conflict be prolonged.

‘The rates were steady since last May as the nation recovers from a 2022 financial crisis driven by a severe dollar shortage.

‘Supported by a US$ 2.9 billion programme with the IMF, Sri Lanka posted a strong economic recovery last year, growing by 5 percent and now targeting growth between 4 percent and 5 per cent in 2026.

‘What stands out is that they see space for inflation to rise because of energy prices but still stay contained.

‘From now to June, underlying economic momentum has the space to keep pace despite the disruption because domestic liquidity and credit has been quite substantial as well.

‘An IMF team will arrive in Colombo on Friday for the combined fifth and sixth reviews of the bailout.

‘Furthermore, Gross Official Reserves increased to US$ 7.3 billion at end February 2026 and the Central Bank purchased a substantial amount of foreign exchange from the market in the first two months of the year.

‘However, the ongoing conflict in the Middle East poses risks to Sri Lanka’s external sector outlook, particularly through energy, tourism, trade and remittance flows, although the overall magnitude of the impact remains uncertain.

‘While the Sri Lanka rupee remained relatively stable in early 2026, some depreciation pressures were observed following the onset of the Middle East conflict, similar to the exchange rates of regional peers.

‘Meanwhile, the Monetary Policy Board remains prepared to implement appropriate policy measures to ensure that inflation stabilizes around the target, while supporting the economy to reach its potential.’

By Hiran H Senewiratne

Dialog Television, Sri Lanka’s #1 Pay-TV service provider, has announced the latest upgrade to its smart entertainment lineup with the Dialog Play Mini, featuring seamless access to global streaming platforms including Netflix, Apple TV and YouTube, alongside the Dialog Play entertainment ecosystem for a unified viewing experience. Previously known as the ViU Mini, the device has now been reintroduced as the Dialog Play Mini, reflecting the evolution of Dialog’s digital entertainment platform under the Dialog Play brand.

The Dialog Play Mini transforms any television into a smart 4K entertainment hub by enabling hybrid multi-platform streaming across leading global and local content platforms, delivering a smoother, more intuitive viewing experience. Whether enjoying Netflix originals, Apple TV exclusives, or local favorites, households can now experience world-class entertainment in one compact device.

The Dialog Play Mini brings a streamlined, user-friendly experience to any home setup. Its single numeric-keypad remote controls both the TV and the device, offering simplicity and convenience for everyday viewing. With multiple connectivity options including Wi-Fi, hotspot, LAN, or wingle, the device ensures uninterrupted entertainment even in areas without smart TVs or advanced broadband setups.

Bridging the gap between entry-level set-top boxes and premium Android TV devices, the Dialog Play Mini offers a plug-and-play smart experience. Supported by Dialog’s nationwide service network, local warranty, and after-sales care, it delivers a reliable, feature-rich entertainment experience for Sri Lankan homes.

“With Dialog Play Mini, entertainment becomes more directly accessible for every Sri Lankan home – with or without a Smart TV,” said Lim Li San, Group Chief Operating Officer of Dialog Axiata PLC. “By bringing Netflix, Apple TV, YouTube, and Dialog Play together in one compact 4K-ready device, we’re redefining home entertainment through simplicity, innovation, and the power of connectivity.”

The Dialog Play Mini is now available at Dialog Experience Centers and authorized retailers islandwide. To purchase online, please visit

https://dialog.lk/dialog-play-mini

A strong Technical and Vocational Education and Training (TVET) system equips individuals with practical, relevant, and future-oriented skills helping to innovate responsibly towards a greener and sustainable future – PM

PM reviews progress of the committee appointed for the establishment of a National Nursing University

UN votes to recognise enslavement of Africans as ‘gravest crime against humanity’

Meta and YouTube found liable in landmark social media addiction trial

Showers expected in the Western and Sabaragamuwa provinces and in Galle and Matara districts after 2.00 pm.

Heat Index at ‘Caution level’ in the Western, Sabaragamuwa, Southern and North-western provinces and in Anuradhapura, Mannar, Vavuniya and Monaragala districts

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News2 days ago

News2 days agoSenior citizens above 70 years to receive March allowances on Thursday (26)

-

Features4 days ago

Features4 days agoTrincomalee oil tank farm: An engineering marvel

-

News7 days ago

News7 days agoCIABOC tells court Kapila gave Rs 60 mn to MR and Rs. 20 mn to Priyankara

-

Features7 days ago

Features7 days agoScience and diplomacy in a changing world

-

Features4 days ago

Features4 days agoThe scientist who was finally heard

-

News2 days ago

News2 days agoJapanese boost to Sri J’pura Hospital, an outright gift from Tokyo during JRJ rule

-

News2 days ago

News2 days agoCEB Engineers warn public to be prepared for power cuts after New Year

-

News6 days ago

News6 days agoColombo, Oslo steps up efforts to strengthen bilateral cooperation in key environmental priority areas