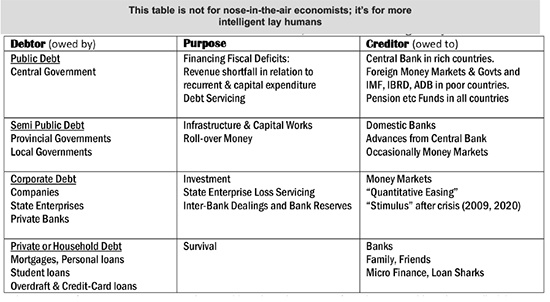

Features

Idiot’s guide to global and domestic debt

Immortal invisible god only wise

by Kumar David

“In light inaccessible hid from our eyes”, is a line from an 1867 hymn set to the tune of a Welsh ballad: it is not a quip about the mystery of global debt but it could well be. Economists don’t enlighten you on the nature and ubiquity of debt because they are muddled themselves. The eclectic hither and thither is recounted in The Economist’s ‘A new era of economics’ – 25 July 2020. There is no shared paradigm, laymen have to cogitate and pick up as best they can. Scientists, finicky about cause and effect cannot suppress the need to frame things in intelligible terms; see if you can pick up anything useful from this idiot’s guide to the ubiquity and explosion of global and domestic public and private indebtedness. Public or national refers to central and local governments. Private is corporate, non-central-bank, bank and household borrowing; the last includes mortgages, personal overdrafts and credit-card indebtedness.

There have been four stages in economic theology since the 1930s. The Keynesian gambit, the neoliberal (Friedman-monetarist) nightmare and the two post-2009 phases. Yes, two phases, the first till about 2018 and the second thereafter which accelerated with Covid-19. I say little on Keynesian macroeconomics or neo-liberalism; the former reigned from the Great Depression till the 1970s when it was invalidated by stagflation, and the latter, that is the neo-liberalism of Pinochet-Regan-Thatcher-IMF, gripped the world by the throat till the 1990s. The last nail in the coffin of dying neo-liberalism was the Great Recession (GR) of 2009-10; the last captain of that sinking ship, Tony Blair, earning himself the epithet Blatcherist. GR proved that unchecked free-market capitalism contained the germs of its destruction in its own DNA, collapsing under its own rationale.

The ratios vary from country to country. In the US Public Debt is about 100% of GDP but semi-Public Debt is small while Corporate and Private Debt are roughly 50% and 70% of GDP. In China Public Debt is not large (48% oh GDP) but Provincial Governments have run wild with infrastructure and waste, which summing up with household debt to over 200% of GDP. In Japan government, debt is 230% of GDP but corporate debt is below 10% and household debt is minimal. For Sri Lanka the big item is Public Debt; nearly 90% of GDP. It doesn’t sound bad, comparatively, but we don’t have the resources to service it.

A feature of the global economy since the 1990s is mounting debt, now astronomical public plus corporate debt, and in the run up to GR acute household mortgages. Strangely, no one asks: “If-all the world is in debt, who is the creditor? Who owns the loot? What the source?” Leaving aside the printing press, a substantive topic of this essay, there are two tangible sources; the enormous wealth accumulated in the hands of the ultra-rich (the “One-Percent”) and public savings in provident funds, social-security coffers and in Japan Post Office Savings accounts. The former is the surplus created by social labour appropriated by capital or siphoned into institutions called private equity, mutual and hedge funds and into mighty investment banks. Maybe half Lanka’s foreign debt is owned to these money-market funds, the other portion to multi-lateral agencies IMF, ADB and World Bank and foreign governments, mainly China and its state banking arms. The point I am driving is that the people of the poor half of the world are deeply in hock to the moguls of international finance capital, including the mighty One-Percent.

The first period of the post-GR phase which lasted for a little less than a decade was characterised in metropolitan centres by measures intended to revive economic growth. Credit was created by central banks (US Fed, EU’s ECB, Japan’s BoJ and limping along, the Bank of England) by the shipload and pumped out to Treasuries, or by purchases of corporate bonds, or shoved into bank vaults. The hope was that there would be investment, growth and employment. It fell flat on its face. Though employment did pick up a bit for reasons too long to detail here, production-capital did not take the ball and run. Instead finance took the money and put it into shares (equities), commercial property and Treasury Bonds, creating an asset bubble.

Central bank money did not go into economic activity; it was siphoned through the ultra-rich into the asset bubble, that is the rich got richer. For this reason, demand for goods and services did not grow (how many bottles of Premier Cru can a millionaire imbibe?). Sans demand, economic growth did not take off in the US, Europe or Japan, hence inflation was stuck below 2% and the economy did not fire up (if inflation escalates, the economy exudes full employment and output is near capacity-output they call it “heating up”). Economic misery in the lower orders created anger and populism (Occupy Movements and radical fundamentalisms). Outrage at the rich getting richer and everyone else getting poorer also triggered the Trump Base, the grip of Marine Le Penn, the popularity of Nigel French, Brexit, near fascists Hungary’s Victor Oban and Poland’s Andrzej Duda, and Hindutva’s Muslim-hating Amit Shah and Narendra Modi. In sum the first phase of post-GR intervention was neither an economic success nor was it politically soothing, it was a failure.

Enter the second post-GR stage starting in 2018 but fouled up and drowned by covid-19. The world’s ruling powers had to take note that growth was not picking up, political resentment was swelling, inflation doggedly low and interest rates peering into the moat of negativity. Then corona hit! It summoned gigantic “stimulus” packages; in the domain of economic theory four schools of were jostling for space.

MMT (Modern Monetary Theory)

MMT is really odd in the eyes of regular economists; I too find it difficult to digest. Were I to exaggerate but only a bit, the theory says print money, print as much as you like, it won’t and it can’t do harm. Governments should not break their heads about deficits, central banks should not let inflation fears hold them back, they should create stimulus money by the bathtub and pour it into investment markets; household should party late into the night. The argument is that by turbo charging the economy with cash, productive activity will take off and rising output will defeat the demon of galloping inflation. The more serious-minded supporters of this school want to keep it going only till inflation and growth pick up and unemployment falls sufficiently, then slacken. But I am not persuaded. When inflation hits it hits fast and hard. Governments and the unwary, soaked in debt, will be overwhelmed by rapidly rising interest rates which will drive them to bankruptcy. Going in search of a free lunch is never unproblematic.

Fiscal splurge driven strategies (FS)

The more conventional last-ditch efforts are Fiscal Splurge (FS) and Monetary Control (MC). The former is the de facto method employed, whether consciously named FS or not, in broke, crisis driven, debt wracked or plain basket economies. While these pejoratives do not all apply to Lanka, some do. The bottom line is that in poor countries with high populist expectations, or enjoying electoral democracy that can oust politicians, governments if they wish to survive, have no option but to resort to fiscal deficits. That is spend more than their revenues to keep the masses stoned, an alternative opiate to religion. In a debt-intoxicated country this means monetary policy and fiscal policy have to merge, the former becomes a service provider to the latter; Prof Laxman transmutes into front office receptionist for President and PM.

In the long-term fiscal profligacy has disastrous consequences that are so well-known that I don’t need to dwell on the it here.

Monetary control and manipulation (MC)

This is typical of the EU; the US is a mix of FS and MC. With MC power rests in the hands of the central bank not government, finance ministry or treasury – FS is the other way round. The prime example of MC is the European Central Bank, I dare say with the Bundesbank breathing down its neck, which drives a chariot whose lowly drays are individual EU governments. BoJ too is not a sub-contractor of the Japanese government. The Reserve Bank of India tried to talk big in the era of Raghuram Rajan but Governors and the Bank have since been cut down to size. Central banks in dominance use interest rates and money supply to manage inflation with an eye on the side turned towards employment and growth.

Restructuring (social concern or state-led)

This is an outlier in a discussion of how capitalist economies (including Scandinavian version) are struggling to cope with explosive debt, income and wealth gaps, and retain social instability. The two key concepts in understanding this fourth option are restructuring and involvement of the state. State-led, but market sensitive and capitalism-accommodative, one party China seems an obvious prototype but it is not an exemplar because this essay is focussed on capitalist (the majority) nations of the world. An imagined President Bernie Sanders Administration in the US is a hypothetical example of this option. I don’t need to explain how this will be different from the US we know, but the point of this essay is that US national debt is large and will be larger in the hypothetical case. At the moment in the debate about coping with a belly-up economy, staggering stimulus packages are on Congress’ table – the Republicans want to cap it at $2 trillion, Democrats to push it up to $3 trillion. Hypothetical Bernie and his Squad will make it larger.

Whatever the version, stimulus money will be part channelled to government (Treasury Bond purchase) and a comparable sum will be siphoned into corporate bonds and private assets. Soaring debt will undermine faith in America’s ability to measure up to its commitments and will damage faith in the dollar as the world’s reserve currency. Debt has come to stay in every corner, an unwelcome guest determined to hang on till there is a global transformation. Sri Lanka is a footnote to the story.

The world’s oldest constitutional democracy turned 250 on the Fourth of July, two weeks ago. It is a rather quirky coincidence that in the 250th year of its largely successful existence, America should be having as its president the most unfitting person in history, and that in keeping with the American trait for mixing serious purposes with fun and play, it should also be hosting perhaps the largest edition of the World Cup Football Tournament. The triple coincidence – the anniversary, Trump presidency and the World Cup – is not without some meaning.

The essence of the Trump presidency has been to recast America in the mould of Trump’s own vulgar and outlandish presuppositions about who belongs in America and what the rest of the world owes to America. Internal exclusions and external isolation have always been a part of American history, but Trump’s project has been to make them America’s sole and permanent purpose. Make America great again by making it more intolerant and more imperfect, as opposed to pursuing the country’s founding purpose of striving towards a “more perfect union.”

Trump is also giving a new meaning to America’s exceptional isolationism by slashing immigration, deporting American residents whom he and his Maga cabal don’t like for the vilest of reasons, withdrawing from global agencies that America created and closing down American agencies providing global services, imposing tariffs on every country and deeming them as payment for America’s past generosity under weak presidents, and threatening neighbours with annexation while militarily attacking others.

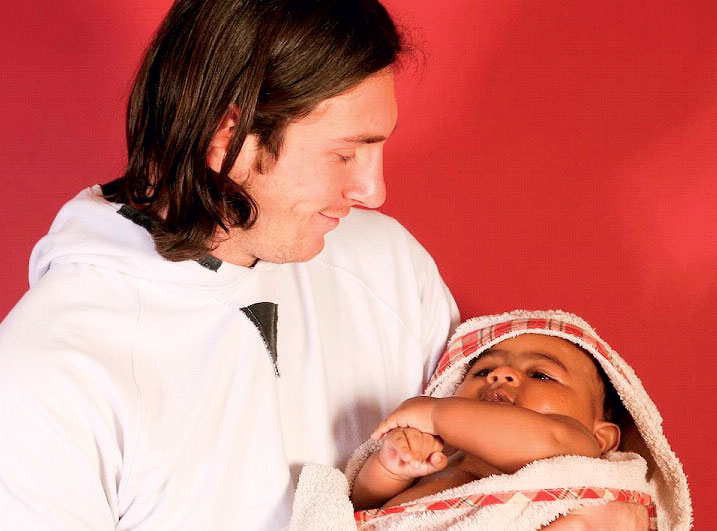

2007: Lionel Messi holding baby Lamine Yamal

He got his nose bloodied after listening to Netanyahu and starting a fight with Iran, made a fool of himself by first announcing that he will provide safe passage to ships through the Strait of Hormuz and charge them 20% of their cargo value, and immediately withdrawing it after being told that it was a lamebrained and impractical idea. The Iranian Foreign Minister tweeted that it is a good approach but 20% is too high! The reality is that Iran has effectively closed the strait again, after Trump said his ceasefire with Iran is over, and there is nothing the might of America can do about it – thanks solely to Trump.

The world, not to mention America, are back to where it was soon after February 28. And Trump is back to February 28, with more attacks on Iran while telling Israel to keep out of it and hoping that Iran will soon come to the table. The Iranian regime is insisting that it is Trump and not Iran who will have to blink first again. For the rest of the world and the people of America, fuel and fertilizer prices are again rising along with the prices of goods and services that depend on them.

Meanwhile, the Fourth of July marking America’s 250th Anniversary of American independence has come and gone. Every year, Americans cheer and celebrate the Fourth of July as a civic festival in their local communities. Families take their children to Washington, Philadelphia, Gettysburg and other historical sites to learn and appreciate their history. The state hardly gets involved and there are no military parades or flights of fighter jets. Trump changed it last year by holding a military parade in Washington but it did not excite anyone. The army had to go to extraordinary lengths to protect the city roads from cracking up while parading its massive tanks. This year Trump’s efforts to turn the 250th anniversary celebration into a personal vanity affair spectacularly backfired and what was becoming a national damp squib. Not so ironically, it was rescued by the 2026 World Cup tournament that began on Thursday, June 11 and will end on Sunday, July 19.

World Cup Down to the Wire

The 23rd FIFA World Cup hosted by America, Mexico and Canada with matches played in 16 cities – 11 in the US, three in Mexico and two in Canada – became a significant occasion for the US. It provided an antidote to Trump’s vain and unsuccessful usurpation of the country’s 250th anniversary, even as it became an occasion to show the world that there is still much more likeable about America in spite of all the ugly MAGA makeover that Trump has been giving it from the White House.

What is unique about America is that it is the first and the only immigrant country to become a superpower in world history. An open door country with a melting pot ethos, America has consistently struggled at every stage of its evolution to defy the homogeneity of the privileged, and to celebrate across-the-board heterogeneity in every aspect of the human condition. If the purpose of Trump’s presidency has been to break this arc of American history, the World Cup became an occasion to demonstrate that the arc will continue in spite of Trump.

The World Cup was an eye opener to both resident Americans and visiting football worshippers. Except for the Olympics sporting events, competitive sports in America are dominated by (American) Football, Baseball, Basketball and (Ice) Hockey, and the competitions are all limited to American teams along with some Canadian teams especially in Hockey. The extent of any international connection is limited to allowing players from Central America and Japan for Baseball, and from Canada and Eastern Europe for Hockey. In other words, American notions of exclusivity and self-sufficiency seamlessly extend to the world of sports from the universe of politics and economics.

The arrival of the World Cup, 32 years after America hosted its first and only World Cup in 1994, was an eye opener to American sports fans and the general public. This was international sports at their doorstep and an occasion to live through the experience of witnessing the world’s best exponents of the game fiercely displaying their talents in friendly competitions. The visiting fans who thronged the games brought life and diversity and retail spin offs to the cities where the games were played. The visitors to a person, both players and fans, were enthralled by the magnificence of America’s sporting facilities and the range of amusement and entertainment the host cities offered.

The tournament also became a smorgasbord of different nationalisms from around the world but manifesting pride and passion in support of national football teams and not boastful belligerence about national militaries. The teams were also more equal on the pitch than their governments are at the UN podium. The better teams of the day won in the end but every team made each game as competitive as it could. Small countries from West Asia, Africa and little Atlantic islands went boot-to-boot with European and South American giants and kept everyone guessing until the final whistle. The really big Asian countries – China, India, Indonesia etc. – could not qualify for admission, while Asia’s two industrial giants – Japan and South Korea – acquitted themselves well even though they were unlucky not to go beyond the group stage.

The team that America fielded should not have been allowed to represent the country based on Trump’s executive negation of all DEI (Diversity, Equity and Inclusion) programs in government and in federal hiring. But it did and the US team would have made the 1960s promoters of cross-racial ‘rainbow’ alliances proud. Similar rainbow teams have become the norm of almost all West European countries and England.

Players of colour have become superstars in western football teams and have quite clearly internalized natal nationalism as opposed to being assimilated by them. They are all descendants of birthright citizens of the old empires, a legal tradition that is more universal and anterior to the abolition of slavery and the 14th Amendment in the US, as Chief Justice John Roberts reminded the Trump Administration in overturning its executive order to end the recognition of birthright citizenship in America. A practice that is shared by three dozen countries.

The US Team at the World Cup began as a promising outfit playing with flair and freewheeling style and could have gone as far as the Quarter Finals to play Spain. The team was undone prematurely by Trump’s sleazy intervention with FIFA bosses to suspend the Red Card penalty ban of a US player, Folarin Balogun, for a foul he had committed in an earlier match. Trump’s role and the penalty suspension created a public uproar and in the upshot an inspired Belgium trounced the US whose players performed very poorly perhaps under the weight of the embarrassment that their President had inflicted on them.

The World Cup tournament itself is now down to the final match, the 104th of the tournament, on Sunday, July 19th, between the reigning World Cup champions, Argentina, and Spain, the current Euro Cup holders. The match for the Third Place will be played on Saturday (July 18), between France who lost 0-2 to Spain in a surprisingly one-sided game, and England who went down in a heartbreaking 1-2 defeat to Argentina after leading 1-0 up till five minutes before the final whistle.

The French were the tournament’s cracking team till they came up against Spain who had been belabouring until then. The English team had bestirred all of England back home with their gritty win against Mexico in its national stadium full of 85,000 spectators, but once again came up short in the penultimate game.

The final between Argentina and Spain will feature the 39 year old Argentinian maestro, Lionel Messi, looking to win his second World Cup, and the 19 year old Spanish prodigy, Lamine Yamal. The football internet is abuzz with a 2007 photograph showing then 20 year old Messi carrying Yamal as an infant during a photo session in Barcelona, Spain, where Messi played club football. On Sunday, in New York/New Jersey, they will face each other in a spirited encounter for the biggest prize in sports.

by Rajan Philips

These two excerpts from the forthcoming book, To Survive As One Nation, One People by Air Chief Marshal Oliver Ranasinghe. A Retired Commander of the Sri Lanka Airforce makes interesting reading. The first is of a sudden demand on the SLAF for emergency air support for the besieged Jaffna Fort when the only available helicopters were being prepared for a VVIP flight for UK PM Margaret Thatcher and her husband, Mark.

The second deals with ferying PM Rajiv Gandhi and his wife Sonia to Katunayake after a naval rating had hit Gandhi with a rifle butt.

In April 1985, the UK’s first female prime minister visited Sri Lanka to ceremonially declare open the Victoria Dam and Power Station built with aid under the patronage of Queen Elizabeth II. The completion of the project was a significant milestone for the Accelerated Mahaweli Development Programme, with the power station having an installed capacity of 210 MW. Two helicopters were stationed at Air Force Headquarters premises to fly the VVIPs at 6:30 a.m. on 12 April to Victoria Dam. I was Commanding Officer of the Helicopter Wing and assigned to fly Prime Minister Margaret Thatcher and her husband.

However, at around noon on the day before the flight, I got a desperate call from the Joint Operations Command (JOC) requesting that 250 troops be airlifted to the Jaffna Fort immediately, since “hot intelligence” had informed that the enemy had planned to attack the fort that night.

I did not have any helis in the Wing as all had been deployed throughout the North and East. The only other two serviceable helis were in the VVIP security cordon, standing by to fly Prime Minister Thatcher and the other VVIPs the next morning. According to VVIP flying procedures, the helis are kept for 48 hours before the flight within a security cordon which is well-guarded by guards and air dogs. No one is allowed to go witin the security cordon without the Commanding Officer’s approval.

I had to take a quick decision about whether to drop the troops using the two helis from the cordon and run the risk of having no heli to fly Prime Minister Thatcher the next morning. The alternative was to say “No,” to the Army and take the risk of losing hundreds of soldiers at the front, facing a humiliating defeat, loss of prestige, morale and losing the Jaffna Fort, which was the Army’s pride.

If the latter happened, our conscience would be inconsolable even today. When we were fighting the battle, we were one unit: Army, Navy, Air Force and Police. The Air Force was always there. We never said no. So, I took the decision to fly immediately to Jaffna to carry out the task using the two VVIP helis. I was taking a huge risk, jeopardizing my career in the Air Force, by disregarding the standing orders and removing the two helis from the VVIP cordon.

By 1:00 p.m., we took off from Katunayake for Jaffna, using the two VVIP helis without Air Force Headquarters approval. I was captaining one heli with Flight Lieutenant Lasantha Waidyaratne as my co-pilot. (He was the pilot who, a long time later on, landed a heli at Jaffna Fort in the impossible task code-named Operation Eagle.) Flight Lieutenant Tennyson Gunawardena was flying the other heli as captain. I had to fly as we did not have any pilots to spare.

From the Palaly airport, we flew with twenty-two passengers without seats, keeping within the maximum all-up weight, and headed into the Jaffna Fort, approaching with the wind and not headwind as usual, avoiding enemy guns.

By 5:30 p.m., Tennyson called me on the receiver transmitter unit and said, “Sir, it is raining heavily in Katunayake, and we have to go in bad weather in the night back to Katunayake. So can I leave now?” I said, “Okay,” and ensured the heli was made ready for the VVIP the next morning. In the meantime, I kept flying the balance troops.

I did not get down at all from the heli and refuelling, too, was done whilst I was sitting in the pilot’s seat. The Brigadier-in-Charge in Jaffna came up to the heli very late in the evening and told me that, if I couldn’t drop all troops that night, to do the balance first thing in the morning. I said, “No, I will drop all tonight as I have to fly back to Katunayake for a very important task.”

We dropped all 250 troops into the Jaffna Fort and, after refuelling at Palaly, left at around 10:00 p.m. to fly back to Katunayake. However, we got caught to heavy rain on the stretch from North of Mannar to Katunayake. The weather was so bad that we had to request radar assistance to steer to Katunayake. However, I decided to disregard radar advice and told my co-pilot to follow the coastline, just to be clear of obstacles such as high-tension wires. Helicopters do not fly in rainy weather, let alone bad weather, and definitely not at night, but we had no choice.

Lasantha, my co-pilot, swears that he has not done a bad weather flight of that nature, either before or since, in his flying career. In fact, he says that he matured as a pilot during the last hours of that flight!

At around midnight, we landed at Katunayake where the crew was ready to take the heli and clean it to VVIP standard, which they did throughout the night. I was relieved and happy that I could return to Katunayake the same night.

The next morning, we positioned the two helis by 6:30 a.m. at Air Force Headquarters premises to fly the VVIP. Prime Minister Margaret Thatcher and her husband, Mr.Denis Thatcher, had a safe and comfortable flight to Victoria and back. In fact, Mrs.Thatcher was fast asleep when we touched down in Colombo!

As the Commanding Officer of the No.4 Helicopter Squadron, I risked my life and career because I did not want the Jaffna Fort to fall into the enemy’s hands and lose Army lives. Also, I did not want to let down the VVIP and spoil the image of the Sri Lanka Air Force. If anything had gone wrong, obviously I would have been “thrown” in the sea. I believe such life and death situations reveal the inborn/emerging leadership potential of individuals.

This excerpt deals with flying Prime Minister Rajiv Gandhi and his wife, Sonia, to Katunayake after a naval rating on ab honour guard struck Gandhi with rifle butt.

In July 1987, I was out of the Helicopter Squadron and serving as Base Commander—Anuradhapura. The Commander of the Air Force called me one day and asked me whether I was still current on helis, and I said, “Yes.” He said, “I am sending a Bell 214 for you to do some flying training.” The next day, the heli arrived at Anuradhapura, and I got back into swing doing some flying training.

After two days, I was told to come to Katunayake to do a flight. I was told that I had to fly the visiting Indian Prime Minister, Rajiv Gandhi, from the Bandaranaike International Airport (BIA) to Galle Face and back. He was coming to sign the much-talked about “peace accord.” The Indian Prime Minister arrived at the BIA, and he was ferried to the Galle Face green, from where he was taken in a motorcade to President’s House to sign the Indo-Lanka Peace Accord.

Without taking much time, the motorcade returned to the Galle Face green. There was no panic. Rajiv Gandhi was smiling, but Sonia Gandhi helped Rajiv get in first, to the inner seat of the helicopter, and Sonia sat next to the window. If not for that, everything was normal.

I started up, switched on the VHF radio and contacted the Air Force Operations Room for take-off clearance. They told me that at the Navy’s Guard of Honour parade, there had been an incident targeting Rajiv Gandhi. That played havoc in my mind. I had to think that whoever planned and failed would have a “plan B,” and that would be to target the helicopter. Then I realized that, if so, both Rajiv Gandhi’s life and mine would be destroyed by “plan B.” That was my thinking. I had to save this VVIP, our state visitor. To do that, I had to make decisions on my own.

There was no one to tell me what to do. So, I took off in the most unexpected direction and avoided the usual route and followed a different route to BIA, whilst all the time being alert. Coming over BIA, I disregarded the usual approach procedure to the surprise of the Air Traffic Controllers and approached from the wrong direction and landed, but not in the designated landing place, to avoid a possible sniper or RPG attack.

The VVIP got off and walked away to the awaiting Indian Air Force aircraft. That relieved me of the tension of delivering the “precious cargo” in one piece.

(The book is distributed by the Vijitha Yapa Bookshop)

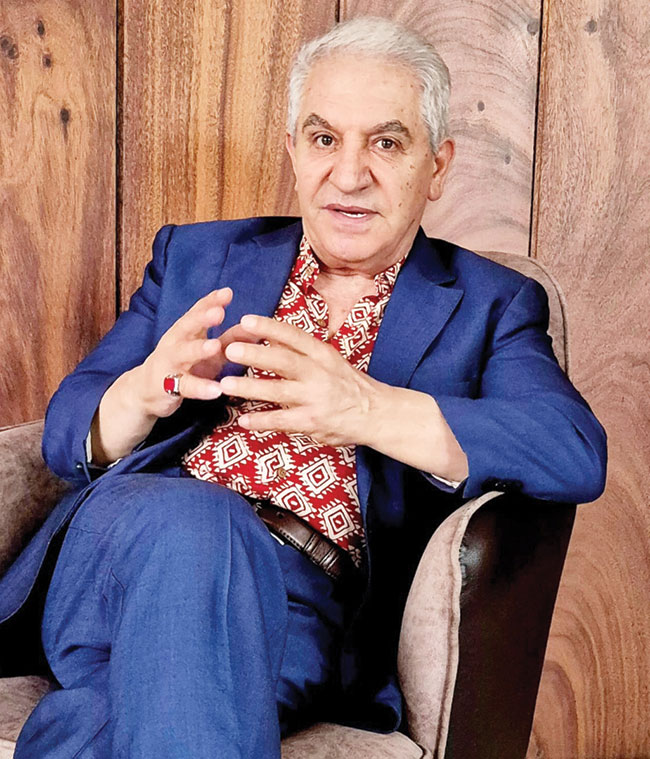

Spanish Israeli entrepreneur Simon Max Astandoust, a fourth-generation member of the renowned Astan fishing family, has endured years of legal battles, business setbacks and the loss of millions of dollars after investing in Sri Lanka’s fishing industry. Yet, despite the challenges, he has chosen to stay and rebuild.

In an interview with the Sunday Island, the founder and CEO of Seamax Ceylon (Pvt) Ltd speaks about his struggle, the restoration of his state-of-the-art factory vessel Astan II, and his plans to introduce cutting-edge seafood technology to Sri Lanka.

Q: You began operations in Sri Lanka in 2018. What was your original vision and investment?

A: We started operations in 2018 with an initial investment of around US$1 million. Over time, that investment grew into several million dollars because we believed Sri Lanka had enormous potential in the fishing industry.

My original intention was to develop a project through the Board of Investment (BOI) and introduce new technology to the country. However, the Government at the time encouraged us to work directly with it instead. We believed that this partnership would help us move forward faster and create something unique for Sri Lanka.

Overhauled Astan II

Our goal was to operate within the harbour and establish a modern fishing operation centred around advanced technology and sustainable seafood processing.

Q: What challenges did you face after starting operations?

A: Around eight to 18 months after we began our investment, COVID-19 hit. The pandemic created enormous difficulties. In countries such as Spain and the United States, governments provided financial support to help businesses survive. Here, the Government itself was facing a difficult economic situation and was unable to provide similar assistance.

Initially, we were told that there would be a grace period and that we would not be pressured for payments as long as we maintained our workforce and kept the operation alive. But later, that understanding changed, and demands for payments began despite the fact that we had a 15-year agreement.

That was the beginning of the major conflict.

Q: How did the change of Government affect your operations?

A: When a new Government came into power, the 15-year agreement signed with the previous administration was not recognized. The factory was closed and legal action was initiated against us.

This was extremely difficult because we had invested heavily based on a long-term agreement. We had built infrastructure, brought in technology and created employment opportunities.

During this period, while the vessel was caught up in legal disputes, a group of people attempted to take control of the ship. One of the most painful experiences was that some lawyers who had been working for us changed sides and supported those attempting to take the vessel.

Simon Max Astandoust

The legal battle continued for years and only concluded in 2025.

Q: Your vessel, Astan II, is central to your investment. What happened to it during this period?

A: Astan II is not just a fishing vessel. It is a huge factory vessel with a complete processing facility inside. It was designed to bring a completely new level of technology to Sri Lanka’s fishing industry.

Unfortunately, because it remained idle during the legal proceedings, it suffered significant damage. Ships cannot simply sit in a harbour for months or years without proper operation and maintenance. The Sri Lankan weather conditions are particularly harsh on vessels.

The vessel deteriorated badly, but after we regained control, we decided to completely restore it. It was overhauled.

Q: How much did the restoration cost and what work was involved?

A: The restoration cost approximately US$1.5 million and took about one year, beginning in 2025. The vessel was almost a complete rebuild. One of the biggest technical challenges was repairing the three generators. Because the harbour did not provide electricity, these generators had been running continuously to maintain the vessel. Over time, this caused significant wear and tear.

Finding replacement parts was another major challenge. Many of these parts are not imported into Sri Lanka, so every component had to be sourced from different countries and brought in individually.

A team of around 14 to 20 people worked on the restoration, including a Sri Lankan chief engineer and local professional deck crew. Their expertise and dedication were extremely important.

Today, the vessel is in brand-new condition.

Q: You mentioned that the absence of diplomatic representation made your struggle more difficult. Why?

A: I hold Spanish and Israeli citizenship, and neither Spain nor Israel has an embassy in Sri Lanka. Normally, when a foreign investor faces serious difficulties, an ambassador can engage with authorities and help protect the investor’s interests.

In my case, I had to face everything alone. I had to deal directly with government institutions and the legal system through my lawyers. Having diplomatic support would have made a significant difference. But ultimately, I had to rely on the courts and the legal process.

Fortunately, the maritime judges understood the complexity of the situation and the importance of maritime law. Their fair approach restored some of my confidence.

Q: Your vessel uses unique -70°C “Ultra-Fresh” technology. Can you explain how it works?

A: This is one of the most exciting parts of our project. The technology comes from Japan and is only about two years old. Traditional freezing methods often affect the quality of fish because the freezing process is slower and damages the texture. This technology works differently. It uses a glazing process where the fish is frozen from the outside, creating a protective layer.

Within approximately two hours, the fish is completely frozen. This process eliminates bacteria and preserves the quality of the fish.

When the fish is later defrosted using the correct method, it is almost exactly like fresh-caught fish from the ocean. The taste, texture and quality are preserved. At present, nobody else in Sri Lanka is carrying out this type of ultra-fresh freezing technology onboard a fishing vessel.

Q: What advantage will this technology give Sri Lanka?

A: Sri Lanka has excellent fishing resources, but we need to move beyond simply catching fish. The future is about value addition, quality control and accessing premium international markets.

With this technology, Sri Lanka can export seafood at a much higher value because customers will receive a product that maintains the quality of freshly caught fish.

This is not just about one company. It is about introducing a new concept to the country’s fishing industry.

Q: After everything you have experienced, why did you decide to continue investing in Sri Lanka?

A: I come from a family of fishermen. This is my fourth generation, and my son represents the fifth generation. Fishermen are not people who give up easily. The sea teaches you resilience. You face storms, difficulties and uncertainty, but you continue. Of course, there were moments when I lost faith. Losing millions of dollars and spending years in court is not easy for anyone.

But eventually, the justice system gave me confidence again. The maritime judges understood the situation and treated the case fairly. That showed me that there are people in Sri Lanka who understand the importance of protecting investment and respecting the law. That is why I decided to continue.

Many people told me that, despite the difficulties, the Sri Lankan judiciary would ultimately deliver justice. At the time, after years of uncertainty, it was difficult to know what the outcome would be. But in the end, that is exactly what happened. The courts examined the facts and delivered a fair judgment.

The maritime judges understood the complexity of the situation and the importance of maritime law. Their fair approach restored my confidence—not only in the legal system but also in Sri Lanka itself.

Q: What are your future plans for Seamax Ceylon?

A: Our plan is to expand significantly. We intend to bring two or three more large factory vessels to Sri Lanka, along with five local fishing vessels. We also plan to establish a new processing factory near the beach. However, this time we will work through the Board of Investment rather than entering into a direct agreement with the Government.

The BOI provides a structured framework for investors, and we believe this is the right way forward. My son Sam, who is the CEO of our US-based company, will also return to Sri Lanka to help introduce successful business concepts and support the next stage of development.

Q: What keeps you motivated after such a difficult journey?

A:The answer is simple: we do not give up. I come from a family of fishermen. This is my fourth generation, and my son represents the fifth generation. Fishermen understand struggle. You cannot control the ocean, but you learn how to survive. You face storms, difficulties and uncertainty, but you continue moving forward.

I have lost money, faced difficult times and experienced moments of disappointment. But I never stopped believing in the potential of Sri Lanka. One thing that gave me strength was the faith many people placed in the country’s judiciary. I was repeatedly told that the courts in Sri Lanka would deliver justice, and ultimately that belief was proven right. The maritime judges understood the situation and gave a fair decision based on the law.

That experience reminded me that, despite challenges, Sri Lanka has institutions and people who respect justice. That is why I decided not only to stay but also to invest again.

For me, this is not merely a business project. It is about resilience, trust and proving that when you believe in something, you continue fighting until you succeed.

by Saman Indrajith ✍️

Showers will occur in the Western, Sabaragamuwa and North-western provinces and in Kandy, Nuwara-Eliya, Galle and Matara districts

Former IGP’s death likely due to an accidental weapon discharge

Rosy Senanayake appears before CMC corruption probe commission

Cop suspended after sitting on female cop’s lap

Arrest warrants issued for Deputy Minister Eranga Gunasekara, MP Jagath Manuwarna

America at 250: Most unfitting President, Biggest World Cup Tournament

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

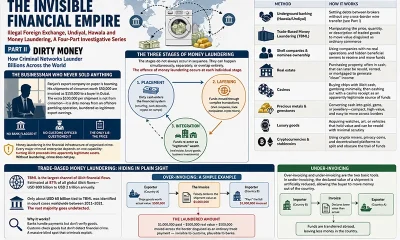

Features4 days ago

Features4 days agoDirty Money

-

Latest News22 hours ago

Latest News22 hours agoDavis cup Asia/Oceania Group IV 2026 to be held in Colombo from 20th to 25th July

-

News1 day ago

News1 day agoDengue outbreak gallops ahead: Infections surpasses 73,455, leaving 50 dead

-

News1 day ago

News1 day agoEvidence recorded in money laundering case against Yoshitha Rajapaksa

-

News2 days ago

News2 days agoMoney laundering case against Yoshitha, fixed for pre-trial conference

-

Midweek Review4 days ago

Midweek Review4 days agoThe sordid tale of theft and tragedy at Finance Ministry

-

Latest News5 days ago

Latest News5 days agoOil prices hit 1-month high as US-Iran attacks dim Strait of Hormuz outlook

-

Editorial2 days ago

Editorial2 days agoOverwhelming fire power and stubborn resilience