Business

HNB yet again delivers sustainable business performance

Group PBT Rs 12 Bn; Bank Rs 10.9 Bn

Group PAT Rs 9.8 Bn; Bank Rs 9.1 Bn

Hatton National Bank (HNB PLC) continued to demonstrate resilience amidst volatile conditions, posting a Profit Before Tax (PBT) of Rs 10.9 Bn and a Profit After Tax (PAT) of Rs 9.1 Bn. The Group profits also improved in line, with PBT and PAT at Rs 12 Bn and Rs 9.8 Bn respectively.

The loan book recorded a growth of 8.6% over the past 12 months to June 2021. Despite same, the reduction of over 280 bps in AWPLR over the same period resulted in a 10.6% YoY drop in 1H interest income, to Rs 48.1 Bn. Strong CASA mobilization efforts led to a 27.1% YoY growth in the CASA base which improved to Rs 405.5 Bn as at end of June 2021. This growth together with the low deposit rates, contributed to a 20.4% YoY drop in interest expenses to Rs 25 Bn. Accordingly, Net Interest Income for the first half 2021 exhibited a 3.2% YoY growth to Rs 23.2 Bn.

Fee and Commission income continued its uptrend in 2021 increasing to Rs 4.4 Bn, a 27.7% YoY growth over the corresponding six months in 2020, a period in which considerable disruption to business activities were witnessed. Card and Trade businesses were key contributors towards this growth, while fees from digital banking also improved significantly driven by higher level of adoption.

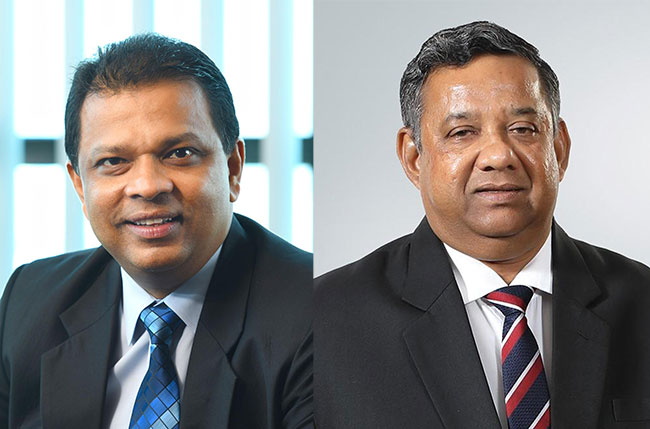

Mr. Nilanth De Silva Chairman of HNB PLC commented that “The operating environment has continued to be uncertain with a multitude of challenges for the Nation and the Industry for almost two years. The re-emergence of higher numbers of COVID positive patients and the fast spread of the Delta variant, threaten macro fundamentals and industry dynamics. We greatly appreciate the efforts expended by the authorities in rapidly rolling out the vaccinations across the country which is the most sustainable solution in winning the war against COVID. In this backdrop I would like to place on record my sincere appreciation to all our stakeholders for their continued patronage and especially our staff for their untiring efforts and unwavering commitment in serving our valuable clients”.

Bank recorded an exchange gain of Rs 3.4 Bn during 1H 2021 relative to Rs 1.5 Bn in the first six months of 2020 due to the depreciation of the Rupee and lower swap volumes.

The Gross NPA ratio of the Bank improved during the first six months of 2021 to 4.25% in comparison to a deterioration of nearly 50 bps witnessed during 1H 2020. The Bank made an impairment charge of Rs 6.3 Bn for the 1H 2021 compared to the impairment of Rs 9.1 Bn in the corresponding period of 2020. The higher impairment charge in the previous year was largely on account of the rising NPAs and the Sovereign downgrade in April 2020. The Bank reassessed the uncertainties in the operating environment, and continued to improve the Management Overlay in the impairment provisions for this period. HNB’s total impairment against the NPA base remained over 100% as at end of 1H 2021.

The Bank was successful in containing the increase in Operating Expenses to 5.2% YoY, despite the Operating Expenses for 1H 2020 being 6% below the corresponding period of 2019. This together with the healthy growth of 13.3% YoY in Total Operating Income resulted in an improvement of 289 bps in Cost to Income ratio which stood at 37.4% as at end of June 2021.

Commenting on the overall performance, Jonathan Alles, Managing Director /CEO of HNB PLC stated that “HNB has yet again demonstrated resilience, stability and strength in a highly volatile environment. We are proud to have crossed the Rs 1 Trillion landmark in deposits which clearly demonstrates the continued trust and confidence placed in us by our customers. We remain the best capitalized bank among domestic systemically important banks, which has been further bolstered by the Basel III compliant debenture issue which was over-subscribed on day one. Our asset quality continues to be ahead of the industry while our liquidity levels are well above the statutory levels.

This has been possible through our relentless focus on ensuring that we remain on a solid foundation built on strong governance, risk management and compliance, which has enabled us to intensify our transformation efforts on Digitalization, Process Efficiency and People Development in our pursuit to be future ready.”

“As a responsible D-SIB, supporting revival and sustainability of our customers, has also been a key priority for us. We have continued to grant moratoriums to customers under stress over the past two years and have provided necessary working capital financing through CBSL schemes and our own funds. We extended grants to 200 microfinance clients to support recovery of their business operations.”

Alles further commented that “Sri Lanka is at a crucial juncture and a national level action plan is the need of the hour to revive the economy. As a true ‘partner in progress’ for the Nation and its people, HNB has supported National development over a century by financing micro and SME clients, funding infrastructure development projects, facilitating international trade and remittances and having stood by our customers during most challenging times, HNB remains committed to play a pivotal role in rebuilding Sri Lanka.”

In line with the reduction in Corporate Tax Rate to 24% from 28%, the current tax liability and the deferred tax asset as at end 2020 were reassessed. Accordingly, the effective tax rate for the period improved compared to the corresponding period of 2020. PAT of Rs 9.1 Bn translated to a Return on Assets of 1.4% and a Return on Equity of 13.2%. Strong second quarter growth facilitated a 3% expansion in the loan book during the first half to Rs 839 Bn. Total deposits increased to Rs 1.032 Trillion as at end of 1H 2021 recording a growth of 6.7%. The Bank is also among the best capitalized and most liquid in the industry as demonstrated by a Tier I Capital Adequacy Ratio of 15.31%, Total Capital Adequacy Ratio of 18.42%, a Liquid Coverage Ratio of 273.7%, and a Loan to Deposit ratio 81.2%. The CASA ratio also stood at 39.3% as at end of 1H 2021. Total assets expanded by 3.5% in the six months ended June 2021 to Rs 1.337 Trillion, while Group assets grew to Rs 1.417 Trillion.

All Group companies complemented the Bank in enabling the Group to post a PAT of Rs 9.8 Bn and a profit attributable to shareholders of Rs 9.5 Bn.

Accordingly, the Group recorded a ROA and ROE of 1.4% and 12% respectively.

Domestic macrofinancial conditions strengthened further in 2025, supporting continued credit expansion, although external vulnerabilities remained a concern. Credit growth accelerated markedly, with total credit extended by banks and Finance Companies (FCs) rising by end-2025. The financial sector’s exposure shifted further toward the private sector, driven by strong private sector credit growth, while exposure to the public sector contracted reflecting ongoing fiscal consolidation.

Despite the decline, government-related exposure remains sizeable. Financial intermediation improved, as reflected by the continued rise in the banking sector’s credit-to-deposits ratio. However, the credit-to-GDP gap widened further into the positive territory of the credit cycle, underscoring the importance of maintaining vigilance over the potential build-up of systemic risk within the financial sector. Global uncertainties, including geopolitical conflict in the Middle East, volatility in commodity prices, and adverse weather conditions, could pose downside risks to credit quality of the financial sector. Against this backdrop, sustained fiscal consolidation and the strengthening of external sector buffers will remain essential to safeguarding macrofinancial stability.

Credit growth in the banking sector accelerated significantly by end-2025, supported by accommodative monetary policy, improved macroeconomic conditions, and strong credit demand. Gross loans and receivables expanded by 21.4% year-on-year, a substantial increase compared to the 4.1% growth recorded at end-2024. This expansion was broad-based, driven by multiple economic sectors including financial services, trade, consumption, lending to overseas entities, construction, and manufacturing. A notable development was the sharp rise in outstanding credit to the financial services sector, which grew by 148.0% year-on-year, reflecting increased funding requirements of the FCs sector amid heightened credit demand. Alongside this expansion, the quality of loan portfolios improved, with the stage 3 loans ratio declining to 9.7% at end-2025 from 12.3% at end-2024, marking the first return to single digits since the second quarter of 2022.

Sri Lanka’s small and medium enterprise (SME) sector, already grappling with post-crisis fragility, is facing a fresh wave of uncertainty as escalating tensions linked to a US-led conflict involving Iran begin to ripple through the global economy.

Industry analysts warn that the fallout—primarily driven by rising global oil prices, supply chain disruptions, and currency pressures—could severely strain the backbone of Sri Lanka’s domestic economy.

Energy sector experts say the most immediate impact is being felt through fuel price volatility. With Sri Lanka heavily dependent on imported petroleum, any disruption in Middle Eastern oil flows has a direct bearing on local costs.

“Even a marginal increase in global crude prices translates into a significant burden for Sri Lanka,” an energy sector analyst said. “For SMEs, this is critical because energy and transport costs form a large share of their operating expenses.”

Small-scale manufacturers, transport operators, and food producers are among the hardest hit. Rising diesel and petrol prices have already pushed up distribution costs, while electricity tariffs are expected to come under pressure if the crisis persists.

Economists also point to the risk of renewed instability in the power sector. Higher fuel costs could increase generation expenses, potentially leading to tariff hikes or supply constraints—both of which disproportionately affect smaller businesses.

“SMEs do not have the financial buffers that larger corporates possess,” an economist noted. “Any disruption in power supply or sudden increase in tariffs directly erodes their profitability.”

Meanwhile, inflationary pressures are beginning to dampen consumer demand. As the cost of living rises, households are cutting back on discretionary spending—dealing a blow to retailers, small restaurants, and service providers.

“Demand contraction is a silent killer for SMEs,” a market analyst explained. “When consumers tighten their belts, it is the small businesses that feel it first and most severely.”

Compounding the situation are disruptions in global shipping and logistics. Heightened tensions in key maritime routes have led to increased freight charges and delays, affecting import-dependent industries.

Construction-related SMEs and small manufacturers reliant on imported raw materials are particularly vulnerable, with many reporting rising input costs and uncertain delivery timelines.

At the same time, pressure on the Sri Lankan rupee is adding to the strain. Global uncertainty has strengthened the US dollar, making imports more expensive and increasing the cost of servicing foreign currency-denominated loans.

“Currency depreciation is a double blow,” an economic policy expert said. “It raises input costs while also tightening liquidity conditions for businesses.”

Tourism, another critical sector supporting thousands of SMEs, is also at risk. Any escalation in Middle Eastern tensions tends to undermine global travel confidence, potentially slowing arrivals to Sri Lanka.

By Ifham Nizam

The Federation Internationale de [Automobile (FIA), the global governing body for motor sport and the federation for mobility organisations worldwide, together with FIA Region II (Asia-Pacific) and the Automobile Association Philippines (AAP), hosted road safety leaders from across Asia-Pacific in Manila the second seminar of the FIA Safe Mobility 4 All & 4 Life programme.

According to the World Health Organization, road traffic injuries remain a major challenge across Asia-Pacific, with the South-East Asia and Western Pacific regions accounting for more than half of global road traffic fatalities,’ highlighting the urgent need for coordinated action.

Developed by the FIA, in collaboration with the United Nations Institute for Training and Research (UNITAR) and with the support of the FIA Foundation, the FIA Safe Mobility 4 All and 4 Life programme aims to support local authorities and organisations with training, mentorship, and evidence-based actions to improve road safety for all users.

Delivered through a mix of in-person seminars, online learning and mentorship, this FIA University initiative brings FIA Member Clubs and government authorities together to build capacity, learn side by side, and develop practical road safety projects that drive meaningful change with guidance from international experts.

Sessions explored how youth engagement, urban development and innovation support the Sustainable Development Goals and the Decade of Action for Road Safety, while encouraging participants to apply data-driven strategies and share knowledge and expertise across the FIA network.

Delegates from 16 FIA Region II (Asia-Pacific) Member Clubs and government representatives from across 15 countries in the region took part in the seminar, including Australia, Bangladesh, Cambodia, India, Indonesia, Japan, Kyrgyzstan, Mongolia, Nepal, the Philippines, Singapore, Sri Lanka, Thailand, Uzbekistan and Vietnam.

Devapriya Hettiarachchi, Secretary, Automobile Association of Ceylon invited K Chandrakumara, Deputy Director /General (IRSTM), Road Development Authority (RDA) to take part in the programme, highlighting the strengthened partnership between the Club and the Philippine government to launch initiatives aimed at saving lives on the road.

King Charles praises ‘living bridge’ with Nigeria at glitzy banquet

Our objective is to ensure that the Commission to Investigate Allegations of Bribery or Corruption operates as an independent institution, free from any external influence – PM

Showers above 50 mm can be expected at some places in the Central, Sabaragamuwa and Uva provinces and in Ampara district.

Oil nears $110 a barrel after gas field strike

Iran’s intelligence minister Esmail Khatib killed in air strike

Heat Index at ‘Caution Level’ in the Western, Sabaragamuwa, North-central, Southern and North-western provinces and in Monaragala, Mannar, Vavuniya and Mullaitivu districts

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Business3 days ago

Business3 days agoBrowns EV launches fast-charging BAW E7 Pro at Rs. 5.8 million

-

Life style4 days ago

Life style4 days agoFrom culture to empowerment: Indonesia’s vision for Sri Lanka

-

News1 day ago

News1 day agoCIABOC questions Ex-President GR on house for CJ’s maid

-

Opinion6 days ago

Opinion6 days agoM. D. Banda: Memories of Appachchi – II

-

Business5 days ago

Business5 days agoSri Lanka Institute of Information Technology raises the bar for academic excellence

-

Latest News4 days ago

Latest News4 days agoQR code system will be implemented for fuel with effect from 06.00 a.m. today (15th)

-

News2 days ago

News2 days agoAustralian HC debunks misleading travel risk claims for Sri Lanka

-

News5 days ago

News5 days agoCrypto loopholes funnel Lankan funds abroad