Features

A simple lesson in arithmetic on electricity sector

By Eng. Parakrama Jayasinghe

parajayasinghe@gmail.com

In February this year, I published an article titled, Sri Lankan Electricity Sector – The Headless Chicken (https://www.ft.lk/columns/Sri-Lankan-electricity-sector-The-headless-chicken/4-730564), and that was before Sri Lanka faced an unprecedented shortage of transport fuels, and long queues. The damage caused to the economy by diverting some 75% of the oil supplies to electricity generation is yet to be properly assessed. Therefore any observer including the smallest electricity consumer would agree with the above assessment, considering the sorry state that the once proud electricity sector has deteriorated to. This is by no means a sudden problem, but a repetition year after year even giving a new interpretation to what is meant by “Emergency Power”.

That Sri Lanka is subject to a dry spell every year from January to April does not require elaboration. However, the Ceylon Electricity Board (CEB) has chosen to ignore this reality and continues to do nothing to anticipate or mitigate the recurring problem year after year. Its solution has been to deploy costly emergency power generation, using imported oil. ignoring the very high cost of generation and as happened this year and the grave impact on the transport sector.

With the good fortune of more than usual rainfall, lasting beyond the southwest monsoon, the use of oil for power generation has been minimal over the past several months and the power cuts, too, have been limited to two hours per day. But, how long will that euphoria of ample hydro power last? Is there any possibility at all of the January to April dry spell not materialising?

The abyss facing us in a few short months

Maybe, Sri Lankans have already forgotten the miles long fuel queues. This story is set to be repeated in early 2023, too, with the Chairman of CEB, having already approved 100 MW of emergency power. In the meanwhile, the new long-term electricity generation plan (LTEGP 2023-2042 ) recently discussed at a public stake holder meeting proposes addition of 320 MW of emergency power now given a new name of “Short Term Supplementary Power”, nevertheless operated using expensive oil imported using the meager dollars resources, borrowed from increasingly reluctant lenders.

Sri Lanka paid a hefty sum in demurrages for the shipment of crude oil recently, which was lying in the out harbour for 56 days due to lack of dollars to pay for it. Where are the dollars coming from to pay for the proposed emergency power once the rains cease? The grave question of adequate supplies of coal to keep Norochcholai operational is hanging above us which will make the situation unbearable.These are the circumstances which prompted the tittle of this article.

The numbers game

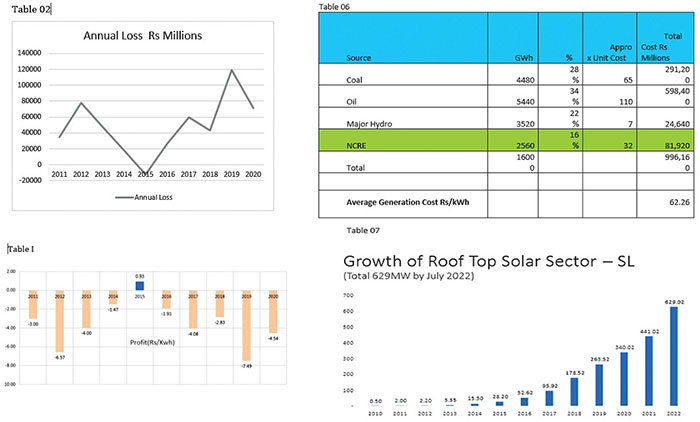

The CEB is fond of pinning the blame on the government for the continual losses they make year after year, claiming that its income is based on tariffs determined by others, and they are inadequate to cover the costs. This is only part of the story. The average income to the CEB thereby was about Rs 16.50 per unit whereas the average cost of generation continued to increase and was of the order of Rs 23.00 per unit before Covid-19 and the subsequent economic meltdown. As such the CEB losses kept mounting, as shown in Tables 1 and 2.

The annual losses per unit borne by the consumers

The Accumulated loss over this 10 year period is Rs. 484 Billion, with the rare instance of marginal profit in the year 2015.All of these losses were covered by the Treasury or are accumulated as bad debts in the two state banks and the CPC. This in other words means that the consumers at all levels have in reality paid an additional amount for every unit consumed.

However, why didn’t the CEB, or the Ministry of Power and Energy, or even the Treasury ask why the cost of generation cannot be lowered?So, my first lesson in Arithmetic is this; if ‘A’ is the cost of generation and ‘B’ the income, and if A >> B resulting in a negative value for C being the loss, and if A cannot be increased at will, why not lower B?

The CEB’s answer would be to say that its proposals for adding more coal power which in their books is the cheapest source of electricity was not permitted. The fact that coal is to be imported with dollars and the rupee continued to be depreciated and we have no control on the price of coal, does not enter into their reasoning. This is to be expected as their long term generation plans are based on the assumption that the price of coal does not change and the rupee does not depreciate. With that kind of mindset it is futile to continue this discussion with the CEB. Obviously they are also blind to the vast strides made the world over, where by many cheaper options for power generation have now been commercialized. Is this driven by pure ignorance, or willful misinterpretation of the realities of the sector or just lack of competence of the CEB engineers making decisions, are the unanswered questions, but with the net result of the present calamity faced by the nation.

The role of the Ministry of Power and Energy and the Treasury

But what about their superiors in the Ministry of Power and the custodians of the public purse in the Treasury? Do they, too, lack the simple knowledge in evaluating this equation and asking the obvious questions? In fact, I would lay the greater blame on the Ministry and the Treasury, for permitting the CEB to perpetrate this deception year after year, with total disregard for the interest of the country and its people. This blame is not limited to the present admiration, but must be laid at the feet of all previous regimes who also turned a blind eye on this problem for whatever reason.

The net result of this collective lack of accountability and blatant violation of responsibilities has been the current disaster and the even greater disaster waiting to unfold shortly. The disaster that would occur in early 2023, as the price of coal has sky rocketed and the best price quoted in the recent tender was $ 325 per ton. As such the line on coal has now got to be removed from the category of low cost generation in the CEB projection. (See Tables 03 and 04)

The Relative Costs prevailing prior to 2020 shown above clearly shows that even then the cheapest option was RE. This is the historical data before Sri Lanka faced the current crisis. However, it is interesting to see below the analysis of actual cost of coal power issued by the PUCSL in 2020. The myth of cheap electricity has been clearly debunked. Matters have worsened since then. The estimates revealed at the recent TV programme are shown below. The recent news items in Economy Next (22nd Nov 2022) tells the true story

” CEB loses Rs 108 bn up to August 22″

(See Table 05) With both escalated purchase prices of oil and coal the true cost of coal power would now reach over Rs 65 /kWh and that of oil over Rs 120/kWh, the prognosis for the next year is indeed alarming. Of the many NCRE options, which averaged only Rs 14.81 , well below the average income of the CEB, the true cause of this alarming loss is clear from the above chart.

It is time for the next lesson.

It is quite on the cards that the CEB loss will exceed Rs. 150 Billion for the year 2022. Thus based on the expected generation less than 15,000 GWhThe loss per kWh = 150,000,000,000/ 15,000,000,000 = Rs 10.00

This is not included in the monthly electricity bill even after the increased consumer tariff.So who bears this cost? You guessed it. The consumers including those consuming a mere 30 units a month and up to those consuming 3000 units a month in equal measure.

What awaits us round the corner?

In this light it was a breath of fresh air to note that Sri Lanka managed even for a few days with very little oil based generation in the past months, courtesy of the weather gods. However, this euphoria will be short lived and the rains are already dwindling. The damage is worsened by the fact that the cost of generation using oil and coal has reached such levels , so that any right minded admiration would shut down such plants immediately and seek whatever sustainable means of bridging the gap. (See Table 06)

Estimated generation cost for year 2023

These numbers are generally in line with those presented in the TV programme where the cost was predicted as Rs 900 Billion.So I dare not perform the next calculation of the loss per kWh which the consumers will have to bear albeit indirectly. That is unless something rational is done without any further delay.

The options available

Fortunately for Sri Lanka we have ample means of doing so, which does not result in continuous drain of Dollars and has the benefit of many other economic advantages. More details of these options have been submitted to the officials who hopefully would advise their political masters of the lack of any other alternative. This is where the third lesson in arithmetic becomes important. It was revealed that based on the current projections the total cost for the CEB in year 2023 is estimated as Rs 900 Billion. They cannot hope to get even 50% of that even with the recent 75% increase in consumer tariff resulting in a projected loss of over Rs. 450 Billion.

Who will bear this cost? What will that do to our balance of payments and the parity rate if it is also to be funded by the treasury? We will be entering a positive feed back loop in financial terms, the result of which the CEB engineers talking about stability of systems should understand.But what are those who are expected to mange the energy sector and more importantly the treasury which has blindly covered all the massive losses incurred by the CEB in past will at least now take some decisive actions.

Having wasted many years by obstructing the development of the Renewable Energy Sector, the options for any short term interventions are now limited to the Roof Top Solar systems. It is on record that with the help of the Surya Bala Sangraamaya which provided some degree of safety against those hellbent on disrupting it, some 650 MW of roof top solar has been now grid connected. Even now adding a further 100 MW at least in the next six months is technically possible if the authorities can do another simple sum in Arithmetic. (See Table 07)

It is seen that the average cost of generation would now be around Rs 62.00 per unit, if the present price of coal and oil stays and the rupee does not deteriorate any further. Also considering that what is even more important to consider is the availability of FOREX for the import of coal and oil, the decision on the tariff payable for the Roof Top solar, being the only short term solution should be against the cost of generation using coal and oil.

In this regard the industry experts have made detailed submissions that, under prevailing financial and economic considering the viable tariff to attract any investor to this sector would be Rs 50.00 – Rs 60.00 per unit based on size of installation. Naturally this could come down as hopefully the Sri Lankan economy improves in the coming years. But can we afford to wait till then. The alternative is to use emergency power costing more than double. So the simple question to be asked is , which number is higher?

Cost of Solar RT of Rs 50.00 per kWh or Cost of Coal of Rs 65.00 per kWh, (If we manage to buy some coal, which too is in doubt), and Cost of Solar RT of Rs 50.00 per kWh or Cost of Oil of Rs 120.00 per kWh Isn’t there any one at the CEB, PUCSL, or the Ministry of Power or The Ministry of Finance who can do these simple sums?

Unless there is some sanity even at this late hour to realize that the CEB must secure it energy by focusing on the facilitation of the indigenous, renewable sources of energy, which does not depend on imported fuels of any kind, Sri Lanka is rushing towards a disaster on unimaginable proportions in a few short months. Don’t be surprised if a further consumer tariff increase is round the corner and worse still the possible resumption of the petrol and diesel queues before long.

(Part III in a series on Sri Lanka’s tourism stagnation.)

![]() Every SLTDA (Sri Lanka Tourism Development Authority) press release now leads with the same headline: India is Sri Lanka’s “star market.” The numbers seem to prove it, 531,511 Indian arrivals in 2025, representing 22.5% of all tourists. Officials celebrate the “half-million milestone” and set targets for 600,000, 700,000, more.

Every SLTDA (Sri Lanka Tourism Development Authority) press release now leads with the same headline: India is Sri Lanka’s “star market.” The numbers seem to prove it, 531,511 Indian arrivals in 2025, representing 22.5% of all tourists. Officials celebrate the “half-million milestone” and set targets for 600,000, 700,000, more.

But follow the money instead of the headcount, and a different picture emerges. We are building our tourism recovery on a low-spending, short-stay, operationally challenging segment, without any serious strategy to transform it into a high-value market. We have confused market size with market quality, and the confusion is costing us billions.

Per-day spending: While SLTDA does not publish market-specific daily expenditure data, industry operators and informal analyses consistently report Indian tourists in the $100-140 per day range, compared to $180-250 for Western European and North American markets.

The math is brutal and unavoidable: one Western European tourist generates the revenue of 3-4 Indian tourists. Building tourism recovery primarily on the low-yield segment is strategically incoherent, unless the goal is arrivals theater rather than economic contribution.

Comparative Analysis: How Competitors Handle Indian Outbound Tourism

India is not unique to Sri Lanka. Indian outbound tourism reached 30.23 million departures in 2024, an 8.4% year-on-year increase, driven by a growing middle class with disposable income. Every competitor destination is courting this market.

This is not diversification. It is concentration risk dressed up as growth.

How did we end up here? Through a combination of policy laziness, proximity bias, and refusal to confront yield trade-offs.

1. Proximity as Strategy Substitute

India is next door. Flights are short (1.5-3 hours), frequent, and cheap. This makes India the easiest market to attract, low promotional cost, high visibility, strong cultural and linguistic overlap. But easiest is not the same as best.

Tourism strategy should optimize for yield-adjusted effort. Yes, attracting Europeans requires longer promotional cycles, higher marketing spend, and sustained brand-building. But if each European generates 3x the revenue of an Indian tourist, the return on investment is self-evident.

We have chosen ease over effectiveness, proximity over profitability.

2. Visa Policy as Blunt Instrument

3. Failure to Develop High-Value Products for Indian Market

There are segments of Indian outbound tourism that spend heavily:

* Wedding tourism: Indian destination weddings can generate $50,000-200,000+ per event

* Wellness/Ayurveda tourism: High-net-worth Indians seek authentic wellness experiences and will pay premium rates

* MICE tourism: Corporate events, conferences, incentive travel

Sri Lanka has these assets—coastal venues for weddings, Ayurvedic heritage, colonial hotels suitable for corporate events. But we have not systematically developed and marketed these products to high-yield Indian segments.

For the first time in 2025, Sri Lanka conducted multi-city roadshows across India to promote wedding tourism. This is welcome—but it is 25 years late. The Maldives and Mauritius have been curating Indian wedding and MICE tourism for decades, building specialised infrastructure, training staff, and integrating these products into marketing.

We are entering a mature market with no track record, no specialised infrastructure, and no price positioning that signals premium quality.

4. Operational Challenges and Quality Perceptions

Indian tourists, particularly budget segments, present operational challenges:

* Shorter stays mean higher turnover, more check-ins, more logistical overhead per dollar of revenue

* Price sensitivity leads to aggressive bargaining, complaints over perceived overcharging

* Large groups (families, wedding parties) require specialised handling

None of these are insurmountable, but they require investment in training, systems, and service design. Sri Lanka has not made these investments systematically. The result: operators report higher operational costs per Indian guest while generating lower revenue, a toxic margin squeeze.

Additionally, Sri Lanka’s positioning as a “budget-friendly” destination reinforces price expectations. Indians comparing Sri Lanka to Thailand or Malaysia see Sri Lanka as cheaper, not better. We compete on price, not value, a race to the bottom.

The Strategic Error: Mistaking Market Size for Market Fit

India’s outbound tourism market is massive, 30 million+ and growing. But scale is not the same as fit.

Market size ≠ market value: The UAE attracts 7.5 million Indians, but as a high-yield segment (business, luxury shopping, upscale hospitality). Saudi Arabia attracts 3.3 million—but for religious pilgrimage with high per-capita spending and long stays.

Thailand attracts 1.8 million Indians as part of a diversified 35-million-tourist base. Indians represent 5% of Thailand’s mix. Sri Lanka has made Indians 22.5% of our mix, 4.5 times Thailand’s concentration, while generating a fraction of Thailand’s revenue.

This reveals the error. We have prioritised volume from a market segment without ensuring the segment aligns with our value proposition.

These needs are misaligned. Indians seek budget value; Sri Lanka needs yield. Indians want short trips; Sri Lanka needs extended stays. Indians are price-sensitive; Sri Lanka needs premium segments to fund infrastructure.

We have attracted a market that does not match our strategic needs—and then celebrated the mismatch as success.

The Way Forward: From Dependency to Diversification

Fixing the Indian market trap requires three shifts: curation, diversification, and premium positioning.

First

, segment the Indian market and target high-value niches explicitly:

, segment the Indian market and target high-value niches explicitly:

* Wedding tourism: Develop specialised wedding venues, train planners, create integrated packages ($50k+ per event)

* Wellness tourism: Position Sri Lanka as authentic Ayurveda destination for high-net-worth health seekers

* MICE tourism: Target Indian corporate incentive travel and conferences

* Spiritual/religious tourism: Leverage Buddhist and Hindu heritage sites with premium positioning

Market these high-value niches aggressively. Let budget segments self-select out through pricing signals.

Second

, rebalance market mix toward high-yield segments:

* Increase marketing spend on Western Europe, North America, and East Asian premium segments

* Develop products (luxury eco-lodges, boutique heritage hotels, adventure tourism) that appeal to high-yield travelers

* Use visa policy strategically, maintain visa-free for premium markets, consider tiered visa fees or curated visa schemes for volume markets

Third

, stop benchmarking success by Indian arrival volumes. Track:

* Revenue per Indian visitor

* Indian market share of total revenue (not arrivals)

* Yield gap: Indian revenue vs. other major markets

If Indians are 22.5% of arrivals but only 15% of revenue, we have a problem. If the gap widens, we are deepening dependency on a low-yield segment.

Fourth

, invest in Indian market quality rather than quantity:

* Train staff on Indian high-end expectations (luxury service standards, dietary needs)

* Develop bilingual guides and materials (Hindi, Tamil)

* Build partnerships with premium Indian travel agents, not budget consolidators

We should aim to attract 300,000 Indians generating $1,500 per trip (through wedding, wellness, MICE targeting), not 700,000 generating $600 per trip. The former produces $450 million; the latter produces $420 million, while requiring more than twice the operational overhead and infrastructure load.

Fifth

, accept the hard truth: India cannot and should not be 30-40% of our market mix. The structural yield constraints make that model non-viable. Cap Indian arrivals at 15-20% of total mix and aggressively diversify into higher-yield markets.

This will require political courage, saying “no” to easy volume in favour of harder-won value. But that is what strategy means: choosing what not to do.

The Dependency Trap

Every market concentration creates path dependency. The more we optimize for Indian tourists, visa schemes, marketing, infrastructure, pricing, the harder it becomes to attract high-yield markets that expect different value propositions.

Hotels that compete on price for Indian segments cannot simultaneously position as luxury for European segments. Destinations known for “affordability” struggle to pivot to premium. Guides trained for high-turnover, short-stay groups do not develop the deep knowledge required for extended cultural tours.

We are locking in a low-yield equilibrium. Each incremental Indian arrival strengthens the positioning as a “budget-friendly” destination, which repels high-yield segments, which forces further volume-chasing in price-sensitive markets. The cycle reinforces itself.

Breaking the cycle requires accepting short-term pain—lower arrival numbers—for long-term gain—higher revenue, stronger positioning, sustainable margins.

The Hard Question

Is Sri Lanka willing to attract two million tourists generating $5 billion, or three million tourists generating $4 billion?

The current trajectory is toward the latter, more arrivals, less revenue, thinner margins, greater fragility. We are optimizing for metrics that impress press releases but erode economic contribution.

The Indian market is not the problem. The problem is building tourism recovery primarily on a low-yield segment without strategies to either transform that segment to high-yield or balance it with high-yield markets.

We are building on sand. The foundation will not hold.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT, Malabe. The views and opinions expressed in this article are personal.)

Understanding Sri Lanka through the India AI Impact Summit 2026

Artificial Intelligence (AI) has rapidly moved from being a specialised technological field into a major social force that shapes economies, cultures, governance, and everyday human life. The India AI Impact Summit 2026, held in New Delhi, symbolised a significant moment for the Global South, especially South Asia, because it demonstrated that artificial intelligence is no longer limited to advanced Western economies but can also become a development tool for emerging societies. The summit gathered governments, researchers, technology companies, and international organisations to discuss how AI can support social welfare, public services, and economic growth. Its central message was that artificial intelligence should be human centred and socially useful. Instead of focusing only on powerful computing systems, the summit emphasised affordable technologies, open collaboration, and ethical responsibility so that ordinary citizens can benefit from digital transformation. For South Asia, where large populations live in rural areas and resources are unevenly distributed, this idea is particularly important.

People friendly AI

One of the most important concepts promoted at the summit was the idea of “people friendly AI.” This means that artificial intelligence should be accessible, understandable, and helpful in daily activities. In South Asia, language diversity and economic inequality often prevent people from using advanced technology. Therefore, systems designed for local languages, and smartphones, play a crucial role. When a farmer can speak to a digital assistant in Sinhala, Tamil, or Hindi and receive advice about weather patterns or crop diseases, technology becomes practical rather than distant. Similarly, voice based interfaces allow elderly people and individuals with limited literacy to use digital services. Affordable mobile based AI tools reduce the digital divide between urban and rural populations. As a result, artificial intelligence stops being an elite instrument and becomes a social assistant that supports ordinary life.

Transformation in education sector

The influence of this transformation is visible in education. AI based learning platforms can analyse student performance and provide personalised lessons. Instead of all students following the same pace, weaker learners receive additional practice while advanced learners explore deeper material. Teachers are able to focus on mentoring and explanation rather than repetitive instruction. In many South Asian societies, including Sri Lanka, education has long depended on memorisation and private tuition classes. AI tutoring systems could reduce educational inequality by giving rural students access to learning resources, similar to those available in cities. A student who struggles with mathematics, for example, can practice step by step exercises automatically generated according to individual mistakes. This reduces pressure, improves confidence, and gradually changes the educational culture from rote learning toward understanding and problem solving.

Healthcare is another area where AI is becoming people friendly. Many rural communities face shortages of doctors and medical facilities. AI-assisted diagnostic tools can analyse symptoms, or medical images, and provide early warnings about diseases. Patients can receive preliminary advice through mobile applications, which helps them decide whether hospital visits are necessary. This reduces overcrowding in hospitals and saves travel costs. Public health authorities can also analyse large datasets to monitor disease outbreaks and allocate resources efficiently. In this way, artificial intelligence supports not only individual patients but also the entire health system.

Agriculture, which remains a primary livelihood for millions in South Asia, is also undergoing transformation. Farmers traditionally rely on seasonal experience, but climate change has made weather patterns unpredictable. AI systems that analyse rainfall data, soil conditions, and satellite images can predict crop performance and recommend irrigation schedules. Early detection of plant diseases prevents large-scale crop losses. For a small farmer, accurate information can mean the difference between profit and debt. Thus, AI directly influences economic stability at the household level.

Employment and communication reshaped

Artificial intelligence is also reshaping employment and communication. Routine clerical and repetitive tasks are increasingly automated, while demand grows for digital skills, such as data management, programming, and online services. Many young people in South Asia are beginning to participate in remote work, freelancing, and digital entrepreneurship. AI translation tools allow communication across languages, enabling businesses to reach international customers. Knowledge becomes more accessible because information can be summarised, translated, and explained instantly. This leads to a broader sociological shift: authority moves from tradition and hierarchy toward information and analytical reasoning. Individuals rely more on data when making decisions about education, finance, and career planning.

Impact on Sri Lanka

The impact on Sri Lanka is especially significant because the country shares many social and economic conditions with India and often adopts regional technological innovations. Sri Lanka has already begun integrating artificial intelligence into education, agriculture, and public administration. In schools and universities, AI learning tools may reduce the heavy dependence on private tuition and help students in rural districts receive equal academic support. In agriculture, predictive analytics can help farmers manage climate variability, improving productivity and food security. In public administration, digital systems can speed up document processing, licensing, and public service delivery. Smart transportation systems may reduce congestion in urban areas, saving time and fuel.

Economic opportunities are also expanding. Sri Lanka’s service based economy and IT outsourcing sector can benefit from increased global demand for digital skills. AI-assisted software development, data annotation, and online service platforms can create new employment pathways, especially for educated youth. Small and medium entrepreneurs can use AI tools to design products, manage finances, and market services internationally at low cost. In tourism, personalised digital assistants and recommendation systems can improve visitor experiences and help small businesses connect with travellers directly.

Digital inequality

However, the integration of artificial intelligence also raises serious concerns. Digital inequality may widen if only educated urban populations gain access to technological skills. Some routine jobs may disappear, requiring workers to retrain. There are also risks of misinformation, surveillance, and misuse of personal data. Ethical regulation and transparency are, therefore, essential. Governments must develop policies that protect privacy, ensure accountability, and encourage responsible innovation. Public awareness and digital literacy programmes are necessary so that citizens understand both the benefits and limitations of AI systems.

Beyond economics and services, AI is gradually influencing social relationships and cultural patterns. South Asian societies have traditionally relied on hierarchy and personal authority, but data-driven decision making changes this structure. Agricultural planning may depend on predictive models rather than ancestral practice, and educational evaluation may rely on learning analytics instead of examination rankings alone. This does not eliminate human judgment, but it alters its basis. Societies increasingly value analytical thinking, creativity, and adaptability. Educational systems must, therefore, move beyond memorisation toward critical thinking and interdisciplinary learning.

AI contribution to national development

In Sri Lanka, these changes may contribute to national development if implemented carefully. AI-supported financial monitoring can improve transparency and reduce corruption. Smart infrastructure systems can help manage transportation and urban planning. Communication technologies can support interaction among Sinhala, Tamil, and English speakers, promoting social inclusion in a multilingual society. Assistive technologies can improve accessibility for persons with disabilities, enabling broader participation in education and employment. These developments show that artificial intelligence is not merely a technological innovation but a social instrument capable of strengthening equality when guided by ethical policy.

Symbolic shift

Ultimately, the India AI Impact Summit 2026 represents a symbolic shift in the global technological landscape. It indicates that developing nations are beginning to shape the future of artificial intelligence according to their own social needs rather than passively importing technology. For South Asia and Sri Lanka, the challenge is not whether AI will arrive but how it will be used. If education systems prepare citizens, if governments establish responsible regulations, and if access remains inclusive, AI can become a partner in development rather than a source of inequality. The future will likely involve close collaboration between humans and intelligent systems, where machines assist decision making while human values guide outcomes. In this sense, artificial intelligence does not replace human society, but transforms it, offering Sri Lanka an opportunity to build a more knowledge based, efficient, and equitable social order in the decades ahead.

by Milinda Mayadunna

The visit by IMF Managing Director Kristalina Georgieva to Sri Lanka was widely described as a success for the government. She was fulsome in her praise of the country and its developmental potential. The grounds for this success and collaborative spirit go back to the inception of the agreement signed in March 2023 in the aftermath of Sri Lanka’s declaration of international bankruptcy. The IMF came in to fulfil its role as lender of last resort. The government of the day bit the bullet. It imposed unpopular policies on the people, most notably significant tax increases. At a moment when the country had run out of foreign exchange, defaulted on its debt, and faced shortages of fuel, medicine and food, the IMF programme restored a measure of confidence both within the country and internationally.

Since 1965 Sri Lanka has entered into agreements with the IMF on 16 occasions none of which were taken to their full term. The present agreement is the 17th agreement . IMF agreements have traditionally been focused on economic restructuring. Invariably the terms of agreement have been harsh on the people, with priority being given to ensure the debtor country pays its loans back to the IMF. Fiscal consolidation, tax increases, subsidy reductions and structural reforms have been the recurring features. The social and political costs have often been high. Governments have lost popularity and sometimes fallen before programmes were completed. The IMF has learned from experience across the world that macroeconomic reform without social protection can generate backlash, instability and policy reversals.

The experience of countries such as Greece, Ireland and Portugal in dealing with the IMF during the eurozone crisis demonstrated the political and social costs of austerity, even though those economies later stabilised and returned to growth. The evolution of IMF policies has ensured that there are two special features in the present agreement. The first is that the IMF has included a safety net of social welfare spending to mitigate the impact of the austerity measures on the poorest sections of the population. No country can hope to grow at 7 or 8 percent per annum when a third of its people are struggling to survive. Poverty alleviation measures in the Aswesuma programme, developed with the agreement of the IMF, are key to mitigating the worst impacts of the rising cost of living and limited opportunities for employment.

Governance Included

The second important feature of the IMF agreement is the inclusion of governance criteria to be implemented alongside the economic reforms. It goes to the heart of why Sri Lanka has had to return to the IMF repeatedly. Economic mismanagement did not take place in a vacuum. It was enabled by weak institutions, politicised decision making, non-transparent procurement, and the erosion of checks and balances. In its economic reform process, the IMF has included an assessment of governance related issues to accompany the economic restructuring process. At the top of this list is tackling the problem of corruption by means of publicising contracts, ensuring open solicitation of tenders, and strengthening financial accountability mechanisms.

The IMF also encouraged a civil society diagnostic study and engaged with civil society organisations regularly. The civil society analysis of governance issues which was promoted by Verite Research and facilitated by Transparency International was wider in scope than those identified in the IMF’s own diagnostic. It pointed to systemic weaknesses that go beyond narrow fiscal concerns. The civil society diagnostic study included issues of social justice such as the inequitable impact of targeting EPF and ETF funds of workers for restructuring and the need to repeal abuse prone laws such as the Prevention of Terrorism Act and the Online Safety Act. When workers see their retirement savings restructured without adequate consultation, confidence in policy making erodes. When laws are perceived to be instruments of arbitrary power, social cohesion weakens.

During a meeting between the IMF Managing Director Georgeiva and civil society members last week, there was discussion on the implementation of those governance measures in which she spoke in a manner that was not alien to the civil society representatives. Significantly, the civil society diagnostic report also referred to the ethnic conflict and the breakdown of interethnic relations that led to three decades of deadly war, causing severe economic losses to the country. This was also discussed at the meeting. Governance is not only about accounting standards and procurement rules. It is about social justice, equality before the law, and political representation. On this issue the government has more to do. Ethnic and religious minorities find themselves inadequately represented in high level government committees. The provincial council system that ensured ethnic and minority representation at the provincial level continues to be in abeyance.

Beyond IMF

The significance of addressing governance issues is not only relevant to the IMF agreement. It is also important in accessing tariff concessions from the European Union. The GSP Plus tariff concession given by the EU enables Sri Lankan exports to be sold at lower prices and win markets in Europe. For an export dependent economy, this is critical. Loss of such concessions would directly affect employment in key sectors such as apparel. The government needs to address longstanding EU concerns about the protection of human rights and labour rights in the country. The EU has, for several years, linked the continuation of GSP Plus to compliance with international conventions. This includes the condition that the Prevention of Terrorism Act (PTA) be brought into line with international standards. The government’s alternative in the form of the draft Protection of the State from Terrorism Act (PTSA) is less abusive on paper but is wider in scope and retains the core features of the PTA.

Governance and social justice factors cannot be ignored or downplayed in the pursuit of economic development. If Sri Lanka is to break out of its cycle of crisis and bailout, it must internalise the fact that good governance which promotes social justice and more fairly distributes the costs and fruits of development is the foundation on which durable economic growth is built. Without it, stabilisation will remain fragile, poverty will remain high, and the promise of 7 to 8 percent growth will remain elusive. The implementation of governance reforms will also have a positive effect through the creative mechanism of governance linked bonds, an innovation of the present IMF agreement.

The Sri Lankan think tank Verité Research played an important role in the development of governance linked bonds. They reduce the rate of interest payable by the government on outstanding debt on the basis that better governance leads to a reduction in risk for those who have lent their money to Sri Lanka. This is a direct financial reward for governance reform. The present IMF programme offers an opportunity not only to stabilise the economy but to strengthen the institutions that underpin it. That opportunity needs to be taken. Without it, the country cannot attract investment, expand exports and move towards shared prosperity and to a 7-8 percent growth rate that can lift the country out of its debt trap.

by Jehan Perera

Fair weather except for a few showers in the Southern province and in Rathnapura and Monaragala districts after 2.00 p.m

X-Press Pearl disaster fuels global call to classify plastic pellets as hazardous

Foreign Minister Herath decries deadlock in global disarmament

CoPF orders officials to establish legal framework for Rs. 200 for estate workers daily attendance allowance

Colombo drives nearly half of Lanka’s TB cases: Officials

Fonseka clears Rajapaksas of committing war crimes he himself once accused them of

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features3 days ago

Features3 days agoWhy does the state threaten Its people with yet another anti-terror law?

-

Features3 days ago

Features3 days agoReconciliation, Mood of the Nation and the NPP Government

-

Features3 days ago

Features3 days agoVictor Melder turns 90: Railwayman and bibliophile extraordinary

-

Features2 days ago

Features2 days agoLOVEABLE BUT LETHAL: When four-legged stars remind us of a silent killer

-

Features3 days ago

Features3 days agoVictor, the Friend of the Foreign Press

-

Latest News5 days ago

Latest News5 days agoNew Zealand meet familiar opponents Pakistan at spin-friendly Premadasa

-

Latest News5 days ago

Latest News5 days agoTariffs ruling is major blow to Trump’s second-term agenda

-

Latest News5 days ago

Latest News5 days agoECB push back at Pakistan ‘shadow-ban’ reports ahead of Hundred auction