Business

Sri Lanka needs ‘bridge financing’ to last next six months, says Indrajit Coomaraswamy

by Sanath Nanayakkare

Sri Lanka needs to take steps on getting to a framework programme with the IMF, restructure its external debt and bring some bridge financing to last for next six months until negotiations with the IMF on external debt is completed,”former central bank governor Dr. Indrajit Coomaraswamy said recently, at a forum hosted by CT CLSA.

“IMF won’t be able to transact with Sri Lanka until we fix the unsustainable situation in the country,” he said.

Dr. Coomaraswamy highlighted the fact that IMF may include fiscal consolidation in a programme of debt restructuring for Sri Lanka.

CT CLSA, a leading capital market service provider that offers investment banking, stockbroking and wealth management services , conducted the forum on the timely topic ‘ The IMF and the Order of Priorities for Reforms.”

Elaborating on the topic, he said, “In fact, we have a solvency problem on our external debt. Trying to treat it as a cash flow problem and addresing it with short-term measures may create a bigger problem. However, we are beginning to see light at the end of the tunnel due to the policy measures taken by the government recently. Now having approached the IMF, and the government considering some external debt restructuring; we are shifting to the right path, but this is going to be tough.”

“Interest rates are about to rise. As per previous levels where inflation was high, 91-day treasury bill yield was 16%, SLFR was 12% and SDFR was 10.5%. According to former deputy governor of the central bank, Dr. W. A. Wijewardena, the interest rates are expected to double from the current levels.”

Responding to a question on the upward movement of the exchange rate, he said, “I think we could have taken measures to reduce the imbalance between demand and supply of foreign exchange before letting the exchange rate float.”

Referring to domestic debt, Dr. Coomaraswamy said,”We should not suggest or ever take into consideration to restructure our domestic debt. If we restructure the domestic debt, it will lead to serious undermining of the stability of the financial system. Such a situation may not help Sri Lanka in meeting its commitments with external creditors.”

“In fact, the crisis was two years in the making from the time the government cut taxes after the presidential election The country’s banking system is highly exposed to sovereign debt because in recent years, the banking system provided for bridging the budget deficit of the country. And therefore, if there is any restructuring of domestic debt, the impact of such a move could spill over to the balance sheets of the banks and would likely create a crisis in the financial sector. And some of the banks would be affected in the event of external debt restructuring. However, this effect could be managed through regulatory programmes of the central bank. The only way to solve this problem on a sustainable basis is to create a primary surplus in the budget,” he emphasised.

“All creditors of Sri Lanka would seek equality of treatment, and therefore, multilateral debt; namely, World Bank, ADB and the little bit of IMF debt should not be restructured. If it were to be restructured, those institutions could stop their operations in Sri Lanka, and even their financing in the pipeline may not be disbursed.”

“Bilateral debt, mainly OECD which is West + Japan are part of the Paris Club. As China and India are not part of the Paris Club, one of the possibilities for us is to see whether we are eligible for B20 framework earmarked for low-income countries. [B20 proposes to consider the issue of public debt management within the international financial architecture reform].

Dr. Dushni Weerakoon, the Executive Director of the Institute of Policy Studies of Sri Lanka (IPS) was also a panelist at the CT CLSA forum.

When she was asked how Sri Lanka should put the reforms in a particular order to be implemented, she said,”We no longer can afford sequential reforms. What is most critical for Sri Lanka in terms of its economic outlook is to gain some sense of macro stability as a first priority.”

“We are currently witnessing a clear shift in policy. We have to work on several fronts simultaneously with well-coordinated action on three fronts; namely, monetary policy front, exchange rate front and fiscal front. We have entered a monetary policy tightening cycle. The moves of the central bank led to a market-driven exchange rate. But the fiscal side is missing. As long as this is neglected the progress made on monetary and exchange rate fronts will not bring stability. This will put pressure on other two fronts.”

“There is slowness on fiscal adjustment maybe because it’s difficult to do it. Fiscal adjustment will require to raise taxes on the revenue side, and the spending side will require to freeze expenditures. Clear communication of these reforms to the general public is important as these changes should not create more social unrest. The way to do this could be that greater sacrifices would have to be made by those who have greater ability to pay taxes. The richer segment of the Sri Lankan population may have to bear a larger burden of the tax adjustments”.

“On the expenditure side, government spending may have to be frozen and public sector wages and salaries may also have to undergo changes. In such a context, there will be the need to try as much as possible to provide social safety nets for needy segments. It could be provided by implementing a cash transfer programme to reduce the potential social unrest.”

“The other reforms include State Owned Enterprise (SOE) reforms, labor market reforms and banking sector reforms,” she said.

When asked about the possible scenario of debt restructuring with debt to equity swaps, she said,” The possible cost of that is; you will face a prolonged negotiating process with the threat of legal action on the country. Unlike in the past, now our creditor landscape is huge. Our creditors are mostly based in the U.S., and then we have bilateral debt providers such as China and India. we will have to bring all these stakeholders to a common ground and ensure equality of treatment.”

“Another risk is that we need to know that the bonds issued by Sri Lanka has clauses where the majority of the bond holders can buy the minority. If not, there could be a hold off problem where we may have to face legal consequences.”

“The recent debt restructuring of Ecuador and Argentina only had restructuring of interest rate adjustments and maturity extensions and did not receive a haircut,” she pointed out.

Sri Lanka for the first time in 63 years achieved a Rs. 21.9 billion surplus in the primary balance of the fiscal account during the first 10 months of 2017. The country recorded a primary surplus of 0.6 percent of GDP in 2018, the second year running. Dr. Indrajit Coomaraswamy was the governor of the central bank at that time.

Miwayz, Sri Lanka’s newest and most anticipated lifestyle and smart mobility platform, has officially announced its grand launch.

Signaling a major shift in the country’s ride-hailing and delivery ecosystem. the platform went live from Sunday, 12th July with an unprecedented milestone: securing a trusted community of 25,000+, eagerly awaiting passengers within an incredibly short pre-launch window.

For Sri Lankan consumers who have long sought greater transparency and safety, and for drivers seeking fair compensation, Miwayz enters the market not just as an app, but as a community-driven answer to modern commuter challenges.

Facing the Realities of the Road: Addressing Driver Pain Points

For years, the backbone of Sri Lanka’s urban transport—its hardworking three-wheeler and motorcycle drivers—has operated under immense financial strain. Traditional ride-hailing industry have long extracted predatory commission rates ranging from 15% to 25% on every single ride, severely squeezing driver take-home pay. Coupled with highly unpredictable daily incomes and skyrocketing vehicle maintenance and fuel costs, drivers have increasingly felt reduced to mere transactional numbers on a screen.

To address these pain points directly, Miwayz has introduced a highly disruptive, driver-centric economic model:

- 0% Commission & Zero Subscription Fees: Registered driver-partners will enjoy 0% commission cuts and zero-value subscription fees for their first three months of operation, allowing them to take home 100% of their hard-earned fares.

- The Industry’s Lowest Flat Subscription: Post-launch promotional period, Miwayz will transition drivers to the industry’s lowest flat rate daily/monthly subscription model, completely eliminating percentage-based commission structures. This ensures predictable operational costs and maximized income stability.

Tapping into a Massive Market

The launch of Miwayz arrives at a critical juncture for Sri Lanka’s massive urban transport market. According to the Western Province Road Passenger Transport Authority (RPTA), there are currently over 250,000 registered three-wheelers operating as active passenger transport services in the Western Province alone.

Furthermore, latest vehicle population statistics from the Department of Motor Traffic (DMT) reveal that Sri Lanka has over 1.20 million motor tricycles (three-wheelers) and more than 5.17 million motorcycles (bikes) registered nationwide.

By positioning itself as a fair-play platform for this immense pool of micro-entrepreneurs, Miwayz is set to capture a dominant share of the daily commuting market, starting in Colombo and rapidly expanding across the province.

A Foundation Built on Mutual Trust

In a market where trust is the ultimate currency, Miwayz’s rapid acquisition of a combined 25,000+ strong pre-registered base represents a significant vote of confidence from local users.

“We did not want to launch with just an app and a hope; we wanted to launch with a community that believed in our vision from day one,” said the CEO of Miwayz, Nalliah Thayaparan. “To have over 25K trusted driver partners and passengers in our ecosystem before our official launch is the ultimate validation. It proves that Sri Lankans are ready for a platform built on mutual respect, honesty, and fair value.”

Going Beyond the Usual: The Miwayz Promise

Miwayz is engineered specifically to address the daily pain points of Sri Lankan commuters and drivers through three core pillars:

- Total Price Transparency & Best Fair Rates: Passengers will benefit from upfront, highly reliable fare estimates with zero hidden costs, unexpected surges, or predatory price hikes. Miwayz guarantees the best, standard distance-to-fare ratios in the market, ensuring complete peace of mind.

- Uncompromising Safety: To protect both riders and driver-partners, Miwayz features strictly verified profiles, real-time live trip tracking, and a dedicated 24/7 localized support team ready to assist at any moment.

- Everyday Convenience & Passenger Perks: Designed as an all-in-one lifestyle companion, the platform integrates seamless ride-hailing options with everyday essentials, including the upcoming rollout of Miwayz Food featuring local culinary favorites. To celebrate the launch, passengers will receive an exclusive 50% discount on their first 5 rides during the first three months of operation.

Strategic Powerhouse Collaboration with Dialog Axiata

To enhance the overall mobility experience for both passengers and driver-partners, MiWayz has entered into a strategic partnership with Dialog Touch, Sri Lanka’s leading fleet and fuel management platform. The collaboration introduces innovative payment and rewards capabilities that deliver greater convenience to riders while creating tangible value for driver-partners.

Through this partnership, Dialog Touch users can now seamlessly use their Touch Card as a payment method within the MiWayz app, enabling a fast, secure, and cashless payment experience for every journey. In addition, MiWayz driver-partners will benefit from fuel vouchers powered through the Dialog Touch platform, a first-of-its-kind rewards initiative introduced by Touch to recognize and support drivers with meaningful savings on fuel expenses.

Long-Term Support Alliance with TVS

To match its digital strength with on-the-ground sustainability, MiWayz has secured a pivotal strategic partnership with TVS. Focused entirely on providing long-term operational support to the platform’s growing driver-partner community, TVS is introducing immediate, tangible cost-saving benefits on the road. Under this landmark alliance, registered MiWayz driver-partners will gain exclusive access to:

- Exclusive Discounts on Spare Parts: Deep cost reductions on essential vehicular components to reduce overall maintenance costs.

- Specialized Vehicle Services: Tailored, high-priority maintenance and repair services at TVS Own Service Centers

- Valuable Vehicle Trade-In Offers: Highly attractive trade-in opportunities allowing drivers to upgrade their vehicles easily and sustainably.

Representing the alliance, Geethal Anthony, CEO – TVS Lanka (Pvt) Ltd remarked, “We are incredibly proud to partner with MiWayz on this journey of sustainable urban empowerment. At TVS, we believe that true market innovation comes from putting tangible value back into the hands of the community. By providing long-term support structures—specifically through exclusive discounts on spare parts, specialized services, and accessible trade-in options—we are ensuring that driver-partners can significantly lower their operational overheads. This partnership sets a new benchmark for shared economic growth and corporate responsibility in Sri Lanka’s mobility landscape.”

Investing Directly in People: The Direct Reinvestment Model

In a progressive move, Miwayz is channeling its core resources directly into the pockets of its users and partners through a long-term Direct Reinvestment Model.

Rather than focusing on short-term market noise, the company is redirecting its operational capital to create sustained, long-term value additions:

- For Driver-Partners: Enhanced welfare programs, sustainable financial incentives, and long-term professional development pathways that elevate their livelihoods alongside TVS’s operational discounts.

- For Passengers: Consistent loyalty rewards, highly competitive daily pricing structures, and community-driven promotions that provide tangible economic relief in their daily travel budgets.

“We believe the best way to grow is not by plastering billboards, but by enriching the lives of the people who use our platform,” the CEO added. “By investing directly in our drivers and passengers, we are building a sustainable, loyal ecosystem that benefits Sri Lanka for the long haul.”

Availability

The Miwayz passenger and driver applications are now officially available for download on the iOS App Store and Google Play Store. Commuters and drivers across Sri Lanka are invited to download the app today to experience mobility and lifestyle convenience their way.

About Miwayz

Miwayz is a next-generation, community-first lifestyle and smart mobility platform based in Sri Lanka. Committed to elevating the urban travel experience, Miwayz combines advanced ride-hailing technology, transparent pricing, robust safety standards, and merchant delivery ecosystems to create a fairer, more efficient way for communities to connect, move, and thrive.

The secondary market yield curve remained broadly stable during the past week as subdued trading activity persisted around the Treasury Bond auction. Meanwhile, weighted average yields at the weekly Treasury Bill auction recorded declines across all tenors, First Capital Research stated in its latest weekly report.

According to the report, secondary market activity opened on a cautious note with selling interest emerging ahead of the T-Bond auction, causing a slight upward adjustment in yields amid moderate trading volumes. As the week progressed, investor participation remained muted, with market participants largely staying on the sidelines in anticipation of the auction, keeping the yield curve broadly unchanged.

Following the successful completion of the bond auction, the market witnessed mixed sentiment, with selling pressure concentrated at the short end and buying interest emerging in longer-dated maturities. However, activity remained subdued, and the yield curve largely held its ground through the weekend.

At the Treasury Bond auction held on July 13, 2026, the Public Debt Management Office (PDMO) successfully raised the full offered amount of LKR 150.0 billion. This comprised LKR 70.0 billion through the 2030 maturity, LKR 50.0 billion through the 2034 maturity, and LKR 30.0 billion through the 2037 maturity, at weighted average yields of 11.57%, 12.04%, and 12.58%, respectively.

Similarly, at the weekly Treasury Bill auction held on July 15, 2026, the PDMO raised the full offered amount of LKR 120.0 billion. The 3-month, 6-month, and 12-month bills raised LKR 55.0 billion, LKR 35.0 billion, and LKR 30.0 billion, respectively. Weighted average yields declined across all tenors, with the 3-month bill easing by 8 basis points (bps) to 10.13%, the 6-month bill by 3 bps to 10.27%, and the 12-month bill by 1 bp to 10.20%.

On the external front, the Sri Lankan Rupee (LKR) depreciated against the US Dollar, closing the week at LKR 336.3/USD compared to LKR 334.7/USD seen previously. Market liquidity within the banking system expanded significantly, starting the week at LKR 125.89 billion and closing higher at LKR 157.19 billion.

Thus the market data may highlight a clear divergence between short-term liquidity comfort and long-term caution, which points toward a gradual steepening of the yield curve in the near term.

The emergence of buying interest in longer-dated maturities (2034 and 2037) shows that institutional investors are eager to lock in double-digit yields while liquidity is high. This institutional support will likely place a temporary ceiling on long-term rates.

The mild depreciation of the rupee (moving to LKR 336.3/USD) acts as a cautionary counter-signal. If the currency continues to face pressure, it could limit how far short-term yields can fall, flattening the curve back out.

The Colombo Stock Exchange (CSE) witnessed a quiet trading session on Friday, with the benchmark All Share Price Index (ASPI) edging marginally lower down by 42.16 points or 0.20% to close at 21,405.41.

Market turnover remained thin, coming in at Rs. 0.72 billion (approximately US$ 2.2 million), reflecting a general lack of investor participation as most sectors encountered downward pressure.

A total of 31.94 million shares changed hands across 13,397 trades, resulting in a negative market breadth where declining counters outpaced gainers 127 to 91. Blue-chip counters Sampath Bank PLC (SAMP), Lanka IOC PLC (LIOC), and John Keells Holdings PLC (JKH) anchored the day’s market turnover, while a notable off-market crossing was recorded in Chevron Lubricants Lanka PLC (LLUB). Trading volume in SAMP alone was highly concentrated, accounting for 12% of the day’s total turnover.

Sector performance remained mixed, with the Banking sector emerging as the most actively traded, posting a modest gain of 0.18%. The Health Care Equipment & Services sector secured the spot as the day’s best performer, rising by 0.55%.

Conversely, the Household & Personal Products sector faced the steepest decline, dropping 1.95% to finish as the worst-performing sector of the day. In terms of individual movements, Blue Diamonds Jewellery Worldwide PLC [Voting] (PINS.N) led the gainers, advancing by 6.11%, while Agstar PLC (AGPL.N) emerged as the top loser, shedding 9.09%.

By Hiran H. Senewiratne

MIWAYZ redefines Sri Lankan urban mobility with landmark launch

Iran accuses US of striking critical infrastructure as war intensifies

President meets with Department of Prisons Officials

Prioritize Vocational Education in future Education Planning – President

Davis cup Asia/Oceania Group IV 2026 to be held in Colombo from 20th to 25th July

Navy brings fisherman in distress off Pothuvil, ashore

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features7 days ago

Features7 days agoPrison riots and politics: NPP’s biggest challenge and Sri Lanka’s biggest opportunity

-

Features4 days ago

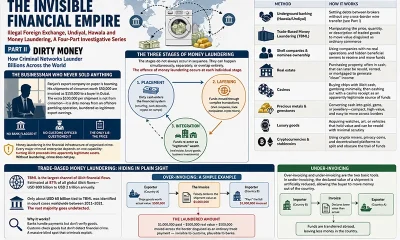

Features4 days agoDirty Money

-

Sports7 days ago

Sports7 days agoThe banker who rescued Sri Lankan cricket

-

Editorial7 days ago

Editorial7 days agoMuch ado about crime: Fish or cut bait

-

Features7 days ago

Features7 days agoMore on Saudi Arabia: ARAMCO and beyond

-

News2 days ago

News2 days agoMoney laundering case against Yoshitha, fixed for pre-trial conference

-

News22 hours ago

News22 hours agoDengue outbreak gallops ahead: Infections surpasses 73,455, leaving 50 dead

-

News22 hours ago

News22 hours agoEvidence recorded in money laundering case against Yoshitha Rajapaksa