Business

Special goods and services tax: Issues and concerns

By Dr Roshan Perera & Naqiya Shiraz

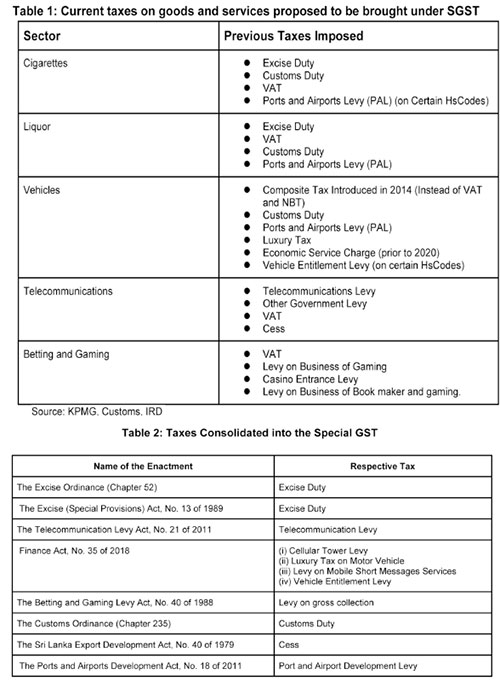

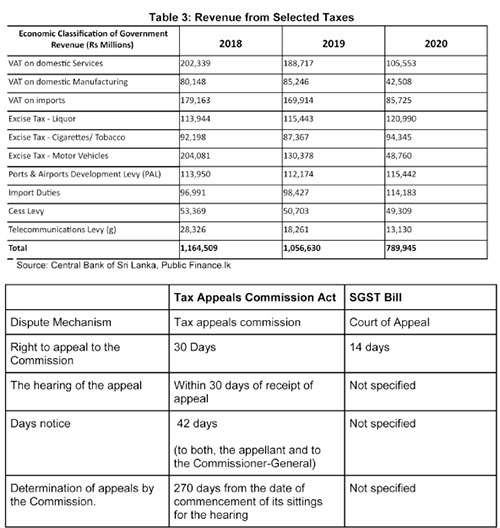

The new bill titled ‘Special Goods and Services Tax’ was published by gazette dated 07 January 2022.1 The Special Goods and Services Tax (SGST) was originally proposed in Budget speech 2021 but was not implemented. It has once again been presented in Budget 2022. The SGST aims to consolidate taxes on manufacturing and importing cigarettes, liquor, vehicles and assembly parts, while also consolidating taxes on telecommunication and betting and gaming (see table 1 for existing taxes on these products and table 2 for taxes consolidated into the SGST as per the schedule in the gazette). The rationale for this new tax as per the bill is “…to promote self-compliance in the payment of taxes in order to ensure greater efficiency in relation to the collection and administration on such taxes by avoiding the complexities associated with the application and administration of a multiple tax regime on specified goods and services.”

Given the multiplicity of taxes and the complexity of the current tax system as a whole, rationalising taxes is necessary to improve collection. However, whether the proposed SGST simplifies the tax system, while ensuring revenue neutrality or even improving revenue collection, needs to be carefully examined.

The SGST Bill is silent on the treatment of the existing VAT on these goods and services. However, according to the Value Added Tax (Amendment) Bill also gazetted on 07 January 2022,1 liquor, cigarettes and motor vehicles will be exempted from VAT while telecommunications and betting and gaming services will still be subject to VAT.

While the gazetted Bill sets out some of the features of the proposed SGST there are many important areas not covered in the Bill. These are expected to be gazetted as and when required by the Minister in charge.

Issues & Concerns

The motivation behind SGST is the simplification of the tax system. Although the objective of introducing the SGST is to improve efficiency by reducing the complexity of the tax system there are many issues and concerns with this proposed tax.

Revenue

Tax revenue which was 13% of GDP in 2010, declined to 8% in 2020. Ad hoc policy changes and weak administration contributed to the decline in tax revenue collection. This continuous decline in tax revenue has led to widening fiscal deficits and increasing debt. One of the main reasons for the current macroeconomic crisis is low tax revenue collection. Hence, any change to the existing tax system should be with the primary objective of raising more revenue.

According to the budget speech the SGST is estimated to bring in an additional Rs. 50 billion in revenue in 2022.1 Revenue from taxes proposed to be consolidated under the SGST has significantly declined over the past 3 years. Given the already difficult macroeconomic environment, along with ad hoc tax policy changes raising the additional revenue estimated at Rs. 50 billion seems a difficult task.

Tax Base and Rate

For the SGST to raise taxes in excess of what is already being collected through the existing taxes, the rate and the base for the SGST needs to be carefully and methodically calculated. Further, the existing taxes have different bases of taxation. For instance the basis of taxation of motor vehicles is both on an ad valorem1 basis and a quantity basis while the basis of taxation of cigarettes and liquor is quantity.2 In light of this, the basis of taxation on which SGST isapplied becomes an issue. Having different bases and different rates for various goods and services would complicate the implementation of the tax These issues need to be carefully considered to ensure the new tax is revenue neutral or be able to enhance revenue collection.

Efficiency

One possible revenue benefit of this proposal is the inability to claim input tax credits on the sectors exempted from VAT. However, the issue is the cascading effect that would result where there would be a tax on tax with the end consumer paying taxes on already paid taxes. If the idea was to raise additional revenue by limiting tax credits, it would have been simpler to raise the tax rates on the existing taxes rather than introduce a new tax.

4. Administration

According to the bill, SGST will now be collected through a new unit set up under the General Treasury where a Designated Officer (DO) will be in charge of the administration, collection and accountability of the tax. The existing revenue collection agencies, such as the Inland Revenue Department (IRD) or the Excise Department will not be primarily responsible for the collection of this tax. By removing the IRD and Excise Department, a parallel bureaucracy will be created, at a time when public spending needs to be carefully managed. The General Treasury also has no previous experience and expertise in direct revenue collection. Weak administration is one of the key reasons for the low tax collection and success of this tax would depend on the strength of its administration.

In addition to the above mentioned concerns, as per the Bill the minister in charge of the SGST has been vested with the power to set the rates, the base and grant exemptions. Accordingly, Parliamentary oversight over fiscal matters is weakened under this proposed Bill.

It could also lead to a time lag between the gazetting and implementing of changes to the SGST (such as the rate, base etc) and obtaining Parliamentary approval for those changes.

Dispute resolution

The SGST Bill also focuses on the dispute resolution mechanism. Under the present tax system, with the enactment of the Tax Appeals Commission Act, No. 23 in 2011 the Tax Appeals Commission has the “responsibility of hearing all appeals in respect of matters relating to imposition of any tax, levy or duty”.1 The most recent amendment to the Tax Appeal

Commissions act (2013)1 seeks to address the large number (495) of cases pending before the Tax Appeals Commision2 by increasing the number of panels to hear the appeals.

Under the proposed SGST disputes will be handled through the court of appeal. However, the time period by which specific actions need to be taken is not provided in the bill. In addition, disputes have to be taken to the court of appeal. Hence, the entire process will be more time consuming. This could result in revenue lags and difficulties in revenue estimation until disputes are resolved.

Additionally, in the case that no valid appeal has been lodged within 14 days, any remaining payments would be considered to be in default. Thereafter, the responsibility is shifted to the Commissioner General of the IRD to recover the dues. Given the IRD is completely removed from the normal collection process, the rationale for bringing defaults under the IRD is not clear.

III. Policy Recommendations

As discussed, the SGST Bill has several limitations and much of this is due to the ambiguities in the Bill.

If the tax is implemented, the rate and basis of taxation needs to be revenue neutral to ensure tax collection is maximised and administrative costs minimised.

The rates, basis of taxation, exemptions etc should be specified in the Bill, as done in most other Acts. This would avoid the power for discretionary changes to the tax being placed in the hands of the minister in charge.

Given the already weak tax administration, it would be more sensible to strengthen the existing revenue collecting agencies and address the weaknesses in the existing system without creating a parallel bureaucracy.

In the case where VAT is consolidated into the proposed GST, the issue of cascading effect of input tax credits needs to be addressed. This is relevant particularly in the case of capital expenditure.

Given the critical state of revenue collection in the country the question to ask is whether this is the best time to introduce a new tax. Focus should be on fixing issues in the existing tax system to ensure revenue is maximised. The VAT is the least distortionary tax and it is the easiest to administer. Given these features it can be a very efficient revenue generator for a country. Therefore instead of introducing a new tax, capitalising on systems that are already in place and amending the VAT rate, threshold and exemptions may be a more practical solution to the revenue problem that the country is currently facing.

Dr. Roshan Perera is a Senior Research Fellow at the Advocata Institute and the former Director of the Central Bank of Sri Lanka.

Naqiya Shiraz is a Research Analyst at the Advocata Institute.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

Sri Lanka Telecom PLC said its dollar reserves rose by around 30 percent in the first quarter of 2026, strengthening the group’s foreign currency position at a time when many Sri Lankan companies remain cautious about external payment risks and exchange-rate volatility.

Chairman of the SLT Group, Dr. Mothilal de Silva disclosed the increase during a post-results media briefing on May 19, following the release of the group’s first-quarter financial results, but declined to reveal the exact value of the reserves, describing the information as commercially sensitive.

“We do not disclose the exact figure because it could affect our negotiations with international suppliers and contractors,” he said in response to a question raised by The Island.

The stronger dollar liquidity comes as a strategic advantage for SLT-MOBITEL, whose operations remain heavily dependent on imported telecom infrastructure, including fibre-optic equipment, transmission hardware, mobile network systems and digital technology platforms largely priced in US dollars.

The improved reserve position is likely to provide the telecom group with greater flexibility in funding future network expansion, servicing foreign currency obligations and managing exchange-rate exposure in a sector closely tied to global technology supply chains.

The remarks came as SLT Group reported its strongest-ever quarterly operating profit and net earnings for the first quarter of 2026, supported by rising broadband demand and improved operational performance.

Group revenue rose 10.6 percent year-on-year to Rs. 30.8 billion, while operating profit surged 39.1 percent to Rs. 5.1 billion. Profit after tax increased 53.3 percent to Rs. 3.1 billion.

The company also highlighted continued investment in broadband and next-generation infrastructure, including the wider rollout of 5G services, as Sri Lanka’s telecom sector positions itself for higher data consumption and enterprise digitalisation.

Unlike many earnings announcements that focus primarily on revenue growth and profitability, SLT’s comments on foreign currency reserves may carry broader significance for investors monitoring corporate resilience in Sri Lanka’s still-fragile post-crisis recovery environment.

When The Island asked whether the Group’s profitability was sustainable amid a slow revenue growth environment, the SLT Group said revenue expansion remained challenging, but added that it had a robust strategy in place to sustain growth.

By Sanath Nanayakkare

…exporters gain little as deeper structural weaknesses persist

Sri Lanka’s weakening rupee is placing severe pressure on industries heavily dependent on imported raw materials, fuel, machinery, and spare parts, with small and medium enterprises (SMEs) facing the gravest threat to survival, according to Indhra Kaushal Rajapaksa.

Speaking to The Island Financial Review, Rajapaksa warned that while a depreciating currency may offer exporters temporary exchange gains, the broader economic impact is proving damaging across multiple sectors of the economy.

“Most businesses are struggling because Sri Lanka imports a significant portion of its industrial requirements. As the rupee weakens, costs rise sharply across the board,” he said.

Industries are responding through a combination of price increases, aggressive cost-cutting, delayed investments, and efforts to source cheaper alternatives. However, Rajapaksa stressed that many firms are operating under shrinking profit margins and mounting uncertainty.

“Companies are trying to survive by passing some costs to consumers, reducing operational expenses, and postponing expansion plans. But SMEs are under extreme pressure because they have limited reserves and weaker access to foreign currency,” he noted.

Rajapaksa observed that large corporates are better positioned to withstand currency shocks due to stronger balance sheets, export earnings, and greater financial flexibility. In contrast, smaller enterprises remain highly vulnerable to fluctuations in import costs and financing conditions.

He identified construction, vehicle imports, pharmaceuticals, electronics, logistics, and manufacturing industries reliant on imported inputs among the sectors worst affected by the rupee depreciation.

“These sectors depend heavily on foreign supplies. Every decline in the rupee immediately increases production and operating costs,” he said.

While export-oriented industries may appear to benefit from currency depreciation, Rajapaksa cautioned that the gains are often overstated.

“There is only a short-term conversion advantage when export earnings are brought back into rupees. But many exporters also depend on imported raw materials and machinery, so their own costs increase simultaneously,” he explained.

He added that the burden of currency depreciation ultimately falls on ordinary consumers through rising food prices, higher fuel and transport costs, more expensive imported goods, and accelerating inflationary pressures.

“Consumers are paying the price indirectly every day,” he said.

Rajapaksa acknowledged that some companies are attempting to localise supply chains and increase the use of domestic raw materials. However, he pointed out that Sri Lanka currently lacks the industrial scale and production capacity to fully replace imports competitively.

“There is growing interest in local sourcing, but Sri Lanka cannot produce everything locally at the required scale or cost efficiency,” he said.

The continued volatility of the currency is also affecting investor confidence, with businesses finding it increasingly difficult to plan ahead.

“Investors value stability. Frequent currency fluctuations create uncertainty and discourage both local and foreign investment,” Rajapaksa warned.

He called on the government to focus on stabilising the economy, strengthening foreign reserves, supporting SMEs and export industries, reducing unnecessary imports, encouraging local production, and ensuring consistent economic policies.

“Policy consistency is critical. Businesses need confidence to invest, expand, and create jobs,” he said.

Rajapaksa also cautioned that employment could suffer if economic pressures continue, particularly in import-dependent sectors and smaller businesses struggling to remain operational.

“Some export sectors may create opportunities, but it may not be enough to offset job losses elsewhere,” he observed.

Describing the current crisis as both cyclical and structural, Rajapaksa said Sri Lanka’s economic vulnerabilities extend beyond short-term currency movements.

“There are immediate pressures from both global and domestic financial conditions, but there are also deeper structural issues such as high import dependence, a narrow export base, and low productivity,” he said.

“Unless meaningful structural reforms are implemented, these problems will continue to recur.”

By Ifham Nizam

The Sri Lanka Institute of Marketing (SLIM), the country’s national body for marketing, successfully convened its Annual General Meeting (AGM) 2026 on 8th April 2026 at the iconic Galle Face Hotel.

The AGM marked a significant milestone in the Institute’s journey, as a new Council of Management and Executive Committee were formally appointed to steer SLIM into its next phase of growth. Building on the strong foundation laid during a transformative 2025, the AGM reflected both continuity and renewal, with an accomplished group of marketing professionals entrusted with leadership roles for the 2026/27 term. The event brought together SLIM members, industry leaders, and stakeholders, underscoring the Institute’s ongoing commitment to advancing the marketing profession in Sri Lanka.

At the helm of the newly appointed Council of Management is Enoch Perera, who assumes office as President. A seasoned marketing professional with extensive experience in international business, he currently serves as Assistant General Manager Marketing – International Business at PGP Glass Ceylon PLC. Joining him in key leadership roles are Manthika Ranasinghe as Vice President – Education and Research, and Rajiv David as Vice President – Events & Sustainability, both bringing with them strong industry expertise and strategic insight.

The Council is further strengthened by Asanka Perera and Nuwan Thilakawardhana as Joint Honorary Secretaries, Ms. Kaushala Amarasekara as Honorary Treasurer, and Dr. Rasanjalee Abeywickrama as Honorary Assistant Secretary. In addition, SLIM announced its Executive Committee for 2026/27, comprising a dynamic group of professionals representing diverse sectors of the marketing industry. The committee includes Channa Jayasinghe, Vijitha Govinna, Anuk De Silva, Sirimevan Senevirathne, Tharindu Karunarathne, Damith Jayawardana, Charitha Dias, Damith Pathiraja, Ms. Roshani Fernando, and Maduranga Weeratunga.

Alice Capsey 74 not out blazes trail in seven-wicket England win

Kolkata Knight Riders keep their IPL campaign alive with low-scoring win

Showers will occur at times in the Western, Sabaragamuwa Northern and North-western provinces and in Anuradhapura, Galle, Matara, Kandy and Nuwara-Eliya districts

Suspects involved in sureties controversy granted bail

Steps underway to safeguard Sri Lanka’s maritime heritage

CEJ’s landmark legal battles reshape Sri Lanka’s environmental justice landscape

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Features4 days ago

Features4 days agoSri Lankan Airlines Airbus Scandal and the Death of Kapila Chandrasena and my Brother Rajeewa

-

News5 days ago

News5 days agoLanka’s eligibility to draw next IMF tranche of USD 700 mn hinges on ‘restoration of cost-recovery pricing for electricity and fuel’

-

News4 days ago

News4 days agoKapila Chandrasena case: GN phone records under court scrutiny

-

News4 days ago

News4 days agoRupee slide rekindles 2022 crisis fears as inflation risks mount

-

Business4 days ago

Business4 days agoExpansion of PayPal services in Sri Lanka officially announced

-

Features6 days ago

Features6 days agoMysterious Death of United Nations Secretary General Hammarskjöld

-

News4 days ago

News4 days agoCourt orders further arrests in alleged USD 42 Mn NDB fraud case

-

Features1 day ago

Features1 day agoOctopus, Leech, and Snake: How Sri Lanka’s banks feast while the nation starves