Business

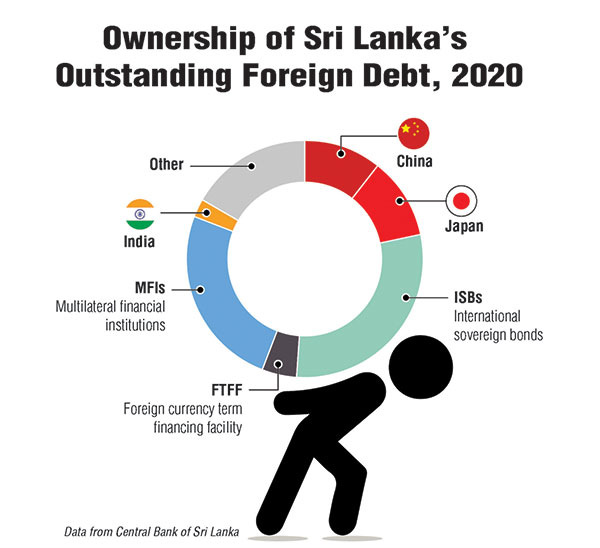

Sri Lanka’s Sovereign Foreign Debt: to restructure or not?

By Dr Dushni Weerakoon

Sovereign debt restructuring can be pre-emptive or post-default. A default is inherently costly as it can result in a sustained loss of access to capital markets. That leaves pre-emptive restructuring when a country deems itself unable to service outstanding debt.

The complex creditor landscape of today though makes governments reluctant to entertain sovereign debt restructuring. The landscape of sovereign borrowing has evolved from a small group made up of multilateral organisations, a few commercial banks, and the ‘Paris Club’ of rich countries to something much more complicated. In recent decades, emerging markets and developing economies have borrowed proportionately more from international bond markets with their dispersed private investors, and tapped new non-Paris Club lenders like China. From the sovereign’s perspective, this makes a potential debt restructuring operation particularly complicated.

The first step in any restructuring is calculating how much a country owes and to whom. This involves sharing detailed information on all categories of sovereign debt denominated in foreign currency, including collateralised liabilities and the debts of state-owned enterprises. The adoption of an IMF programme may be conditioned as a part of a restructuring to underwrite the data, economic plan and the promise of macroeconomic and fiscal supervision.

The first step in any restructuring is calculating how much a country owes and to whom. This involves sharing detailed information on all categories of sovereign debt denominated in foreign currency, including collateralised liabilities and the debts of state-owned enterprises. The adoption of an IMF programme may be conditioned as a part of a restructuring to underwrite the data, economic plan and the promise of macroeconomic and fiscal supervision.

Lenders will weigh the upfront losses of a debt standstill and restructuring against the total magnitude of

losses in the event of a default. In entering restructuring talks, though, they will also demand to do so on the principle of comparable treatment of creditors in any proposed debt reprofilings and restructurings. Lenders will be mindful that any relief offered does not give preferential treatment to other creditors, especially in the face of new geopolitical power rivalries. This would typically mean that a country in distress asks for debt relief from friendly governments to whom it owes money and then seeks a comparable deal from private lenders.

The Holdout Problem

Over the past decades, there has been progress in governance frameworks to deal with sovereign debt crises, but considerable gaps persist. In the COVID-19 era, the G-20 Common Framework for Debt Treatments apply only to low-income countries (LICs), and even then, do not compel the participation of private creditors. Emerging markets that have undergone debt restructuring most recently (e.g. Argentina and Ecuador) are categorised in academic research as countries with a track record of serial default – i.e. more than two default spells or episodes. Given research evidence that countries that have defaulted on their debt obligations in the past are more likely to default again in the future, creditors have an added incentive to enter into negotiations in such cases.

All told, with the creditor landscape transformed, debt restructuring is still very much a matter of ad hoc negotiations between a sovereign and its creditors.

The creditors are aware of their special legal protection that comes down to a question of money due but not paid. At the same time, creditors too have virtually no choice but to negotiate as there will be inadequate assets to satisfy every creditor’s claims even with a successful legal remedy. In the extreme, ‘vulture funds’ have used litigation as an investment strategy to buy the debt at a hefty discount and pursue full payment through the courts. Confronted with this reality, a negotiated resolution should appeal to both creditors and debtor country.

At the centre of such a coordinated effort will be creditor (especially bondholder) committees. The composition of such committees – inclusive of large institutional investors, hedge funds, etc. – is critical to obtain a relatively quick resolution. However, there are no guarantees of fast and efficient mechanisms, and countries still risk fighting creditor lawsuits from those who may hold out.

Such potential holdout creditors may not necessarily take the view that what is good for the many is always good for the few. A disgruntled holdout creditor has the leverage to cause disturbing headlines, especially when countries resume bond market access once again at some point. Holdout creditors can be reined in through exit consents – where a majority of holders can amend terms, or as more commonly used now, employ collective action clauses (CACs) in bond agreements to bind minority holders. In the latter case, a specified supermajority of holders (usually 75%) can bind a minority to the terms of a debt restructuring. But much depends on whether a debtor country’s outstanding stock of international sovereign bonds contains these clauses. Some countries have also adopted anti-vulture fund legislation that limits holdout creditor recovery as a deterrent.

Net Benefit Calculation

High uncertainty during a restructuring, and the risk of prolonged negotiations means debt restructuring is still the last resort, to be done only if you must. A restructuring is a costly exercise with reputational downsides, loss of market access and more expensive debt issuances, weighed down further by concerns about adverse legal implications. For policymakers, a decisive step can be taken after a careful net benefit calculation of whether a country’s economic conditions are likely to deteriorate further without a restructuring, or whether a timely restructure may reduce the total magnitude of upfront losses and return debt to a sustainable level at the lowest cost to both the country and its creditors.

Link to Talking Economics blog: https://www.ips.lk/talkingeconomics/2022/01/12/sri-lankas-sovereign-foreign-debt-to-restructure-or-not/

Dr Dushni Weerakoon is the Executive Director of the Institute of Policy Studies of Sri Lanka (IPS) and Head of its Macroeconomic Policy research. She joined IPS in 1994 after obtaining her PhD, and has written and published widely on macroeconomic policy, regional trade integration and international economics. She has extensive experience working in policy development committees and official delegations of the Government of Sri Lanka. Dushni Weerakoon holds a BSc in Economics with First Class Honours from the Queen’s University of Belfast, U.K., and an MA and PhD in Economics from the University of Manchester, U.K. (Talk with Dr Dushni – dushni@ips.lk)

By Ifham Nizam

The United Nations Development Programme (UNDP) and the Central Bank of Sri Lanka (CBSL) have strengthened their partnership to advance financial literacy across the country, with a renewed focus on empowering vulnerable communities, strengthening economic resilience and promoting sustainable development.

The two institutions formally launched the second phase of their collaboration recently, reaffirming their commitment to implementing Sri Lanka’s National Financial Literacy Roadmap (2024–2028), a cornerstone of the National Financial Inclusion Strategy (NFIS).

The partnership was marked by a meeting between Central Bank Governor Dr. P. Nandalal Weerasinghe and UNDP Resident Representative in Sri Lanka Ms. Azusa Kubota, together with officials from both organisations.

Building on technical support provided by UNDP during 2024 and 2025, the latest phase seeks to equip individuals, households and businesses with the knowledge required to make sound financial decisions, improve livelihoods and enhance resilience in an increasingly uncertain economic and climatic environment.

The initiative comes at a crucial juncture as Sri Lanka continues its economic recovery while grappling with climate-related challenges that disproportionately affect rural communities and small enterprises.

A key component of the programme will be strengthening the capacity of government outreach officers across all districts to deliver financial literacy training to rural populations and micro, small and medium enterprises (MSMEs).

The training will be based on the Financial Literacy Curriculum developed by the Central Bank, with UNDP supporting the enhancement of modules through the integration of climate-resilient financial management concepts.

The programme aligns closely with Sri Lanka’s Financial Literacy Roadmap and is expected to contribute significantly to improving financial knowledge and access across the country. It is supported by several development and private-sector partners, including the government of Japan, Chrysalis, VISA and Hirdaramani-Lacoste.

Speaking on the importance of the initiative, Central Bank Governor Dr. Weerasinghe said the partnership would help broaden the reach of financial literacy efforts while addressing emerging challenges such as climate-related financial risks.

“We particularly welcome the focus on strengthening financial resilience, climate-related financial preparedness, public awareness campaigns and capacity-building through Training-of-Trainers programmes, he said.

He noted that the initiatives would ensure that different segments of society gain access to practical financial knowledge and develop the skills necessary to foster responsible financial behaviour and improve their overall financial well-being.

UNDP Resident Representative Ms. Kubota underscored the critical role financial literacy plays in creating inclusive and resilient economies.

“Financial literacy is a critical foundation for inclusive and resilient economies. Through our partnership with the Central Bank of Sri Lanka, we have been working to empower individuals, particularly those most vulnerable, with the knowledge and tools needed to make informed financial decisions and build secure livelihoods, she said.

Marking an important milestone in Sri Lanka’s economic development, the National Export Development Plan (NEDP) for the period 2026–2030 was presented to President Anura Kumara Dissanayake on Tuesday morning (16) at the Presidential Secretariat.

The 2026–2030 National Export Development Plan (NEDP) is a key national programme formulated in line with the Government’s policy direction under the 2025 Budget. It aims to strengthen the country’s export sector and achieve export-led sustainable economic growth.

The strategic plan has been developed under the guidance of the Ministry of Industry and Entrepreneurship Development and the leadership of the Sri Lanka Export Development Board (EDB), with technical assistance provided through the Asian Development Bank’s (ADB) Policy-Based Lending (PBL) programme. It is the result of an extensive consultative process carried out in close collaboration with key government institutions, private sector stakeholders, and development partners.

The proposal submitted by the Minister of Industry and Entrepreneurship Development to recognise the “Sri Lanka National Export Development Plan 2026–2030” as the official strategic framework for export development and promotion in Sri Lanka was approved by the Cabinet of Ministers on 4 May 2026. The Plan reflects a broad consensus among government institutions, private sector experts, and international development partners.

In line with the national vision of “A Thriving Nation – A Beautiful Life”, the Plan has been formulated to enhance Sri Lanka’s export competitiveness and achieve an export revenue target of USD 36 billion by 2030.

The core vision of the Plan is to transform Sri Lanka into a competitive logistics and knowledge-based export hub serving regional and global markets. The strategy is based on two key interconnected pillars: “horizontals” and “verticals”, which together provide the foundation for strengthening export competitiveness, diversification, and sustainable growth.

The horizontal enablers, which support the growth and expansion of all priority sectors, include logistics and integrated hub operations, trade facilitation, trade finance and reforms in the business and investment environment, trade promotion and market linkages, quality management, standards, environmental, social and governance (ESG) capacity development, as well as entrepreneurship and innovation.

The Plan also identifies eight priority export sectors to enhance export diversification and value addition, and to position Sri Lanka more competitively in global markets. These include automotive components, mineral-based industries, rubber-based industries, maritime industries (including boat and shipbuilding), spices and concentrates, digital products and services, electrical and electronic equipment, and processed food and beverages.

The preparation of the Plan involved contributions from over 300 stakeholders, including government institutions, the private sector, civil society organisations and international development partners. Broad consensus was achieved through consultations held from October to December 2025 and workshops conducted in January 2026.

The Government expects that, with implementation supported by strong governance and monitoring framework, the Plan will elevate local products to international standards and ensure long-term economic stability and growth. It is further anticipated that the National Export Development Plan will serve as a key driver of Sri Lanka’s economic progress in the years ahead.

Minister of Labour and Deputy Minister of Finance and Planning Dr. Anil Jayantha Fernando, Minister of Industry and Entrepreneurship Development Sunil Handunnetti, Senior Additional Secretary to the President and Secretary to the Ministry of Energy Russell Aponso, Secretary to the Ministry of Industry and Entrepreneurship Development Thilaka Jayasundara, and Chairman of the Sri Lanka Export Development Board Mangala Wijesinghe were also present at the event.

[PMD]

The government’s decision to ban the export of mineral resources in raw form and place all future mineral exploration under state control has triggered fresh debate over how Sri Lanka should develop its untapped mineral wealth and attract foreign investment.

Announcing the new National Mineral Policy, Industry and Entrepreneurship Development Minister Sunil Handunnetti said the country had long failed to capture the full value of its mineral resources by exporting them with minimal processing.

“We will no longer allow mineral resources to leave the country in raw form,” the minister said, arguing that Sri Lanka must move towards value-added industries that generate greater economic returns.

A key feature of the new policy is the transfer of all mineral exploration activities to the state-run Geological Survey and Mines Bureau (GSMB). Under the new system, the GSMB will carry out exploration, publish geological data and subsequently invite investors to participate in commercially viable projects.

Handunnetti defended the move by citing what he described as the failure of the previous licensing regime. According to government figures, 471 exploration licences had been issued since 1993, but only 28 advanced to mining operations, with just 12 remaining active today. The minister alleged that some companies had used exploration licences to boost corporate valuations rather than develop actual mining projects.

He also stressed that mineral deposits located beneath privately owned land belong to the state and should be developed in the national interest.

However, the reforms are likely to attract close scrutiny from foreign investors seeking opportunities in Sri Lanka’s mineral sector.

An independent industry analyst said the policy’s emphasis on value addition is consistent with global trends, as countries increasingly seek to process critical minerals domestically rather than export raw materials.

“The more difficult question is whether a state-controlled exploration model can generate the confidence required by international investors,” the analyst said. “Investors will want access to reliable geological data, transparent licensing procedures and predictable regulations before committing significant capital.”

The analyst noted that the government’s plan to publish exploration data before inviting investment proposals could help improve transparency, but its success would depend on how scientifically the process is implemented.

Sri Lanka possesses commercially valuable deposits of graphite, mineral sands, ilmenite, rutile, garnet, silica and phosphate. As global demand for industrial and strategic minerals continues to grow, the new policy represents a significant test of whether stronger state involvement can translate geological potential into investment, industrial development and export earnings.

“The success of the strategy may ultimately depend on whether the government can balance tighter control over mineral resources with the policy certainty and commercial incentives that international investors typically seek,” the analyst said.

By Sanath Nanayakkare

Hundreds of cats stolen for food in Vietnam rescued by police, welfare group says

Canada-Netherlands ODI abandoned due to dangerous pitch in Toronto

Da Silva and Jangoo earn recalls for West Indies’ Tests against Sri Lanka

Spinners make it two in two for England

Messi hat-trick fires holders Argentina to win over Algeria at World Cup

UNDP, Central Bank deepen financial literacy drive to build economic resilience

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoCIABOC summons Yoshitha over his participation in British Navy training programme

-

Sports2 days ago

Sports2 days agoTharanga set for high-profile javelin clash in Ostrava

-

News5 days ago

News5 days agoJustice Minister responds to social media claims he represented Easter Sunday ringleader

-

Features3 days ago

Features3 days agoPolitics of protected species

-

News2 days ago

News2 days agoRelease of 2025 O/L results likely to be delayed

-

News4 days ago

News4 days agoCommonwealth lawyers urge Lanka to uphold rule of law

-

News2 days ago

News2 days agoTheft of USD 2.5 mn from Treasury: CoPF accused of complicity in NPP cover-up

-

News1 day ago

News1 day agoBeijing Capital Airlines to resume flights to Colombo signalling boost to tourism