Business

Is wealth tax the solution to Sri Lanka’s low tax revenue collection?

By Sathya Karunarathne

Successive governments have run fiscal deficits. Inadequate revenue collection and unrestrained government expenditure have worsened the country’s fiscal position.

Tax revenue which averaged over 20% of GDP in 1990 has declined to under 10% of GDP in 2020. Ad hoc tax policy changes have significantly eroded the tax base. Weak tax administration has also contributed to the sharp decline in tax collection.

While tax revenue has contracted, government expenditure has ballooned over time. Today, government revenue is not sufficient even to meet its expenditure on salaries and wages and transfers and subsidies to households which include pension payments and social welfare payments such as Samurdhi.

In this context, there are various proposals put forward to raise government revenue. One proposal is the reintroduction of the wealth tax.

A wealth tax is expected to bridge the gap between the rich and the poor, achieving equality. This tax shifts the tax burden to affluent households, taxing an individual’s net wealth, which is the market value of total owned assets. Proponents of wealth taxation argue that this is a progressive system of taxation and is a more powerful tool in comparison to income, estate or corporate taxes as it addresses the issue of wealth concentration.

Moreover, a tax should ideally satisfy basic characteristics of taxation: it should not be distortionary; it should be fair, and it should not be difficult to collect.

The rationale for a wealth tax

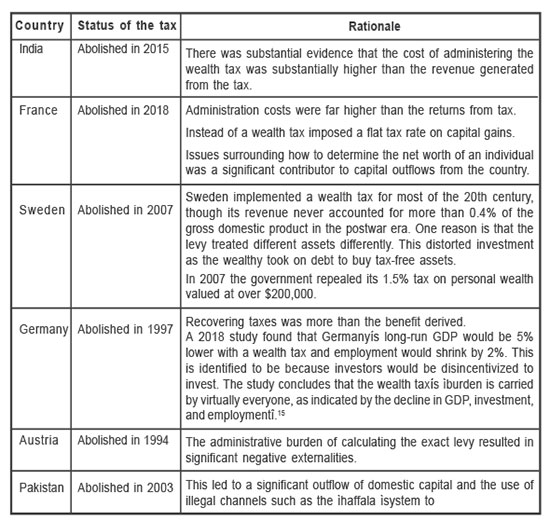

One of the earliest proponents of the wealth tax for developing countries was Nicholas Kaldor. Based on his recommendation, a wealth tax together with an income tax, expenditure tax and a gift tax were introduced in Sri Lanka in 1958.1 However, these new taxes yielded little revenue due to difficulties in determining the tax base and problems in administration. Following the recommendation of the Tax Commission in 1990,2 the government abolished the wealth tax from the year of assessment 1992/1993.3

Wealth taxes have mainly been implemented in European countries. In 1990, twelve countries in Europe had a wealth tax. Today, there are only three: Norway, Spain, and Switzerland. Several non-European countries have also imposed wealth taxes from time to time including such as Argentina, Bangladesh, Colombia, India, Indonesia, Pakistan

In recent times there has been renewed interest in wealth taxes. Presidential candidates in the US proposed various forms of a wealth tax. In the UK and France, there were proposals to impose “super taxes” on the rich. The primary justification was to address the increasing inequality in society.

Issues with a wealth tax

Despite renewed interest in the wealth tax as a progressive tax based on equity, it scores poorly on the criteria of efficiency, and administrative feasibility.4

Many factors have justified the repeal of wealth taxes in OECD countries. The reasons cited are related to efficiency costs, risk of capital flight particularly in light of increased capital mobility and wealthy taxpayers’ access to tax havens, failure to meet redistributive goals as a result of narrow tax bases, tax avoidance and evasion, high administrative and compliance costs compared to limited revenues (high cost yield ratio).5

To understand the efficiency costs of wealth taxes one can look at taxing a person’s wealth accumulated through savings. Despite the common consensus that taxing savings is an effective way to redistribute, a person’s saving decisions reveal little about their underlying lifetime resources and wellbeing. It only reveals their preference to consume tomorrow rather than today. Thereby a wealth tax imposes a tax on those who prefer to spend their money later as opposed to taxing the wealthy.6 Efficiency costs refer to the reduction of the welfare of the taxed individuals by more than $1 to generate $1 of revenue.7 Therefore, the efficiency cost of a wealth tax in terms of taxing savings is a reduction of future consumption that can be bought with earnings, reducing incentive to work for those who prefer to consume the proceeds later and reducing incentive for young people to save for their retirement.8

Capital flight is the possibility of holding assets outside of one’s resident country without declaring them.As wealth taxes are imposed on residents it increases the risk of the wealthy reallocating their assets to avoid taxation. Therefore a high tax burden encourages taxpayers to change their tax residence to a lower tax jurisdiction or tax havens.9

Both income-generating and non-income generating assets are taxed under wealth taxation. They can include land, real estate, bank accounts, investment funds, intellectual or industrial property rights, bonds, shares, and even jewellery, vehicles, art and antiques.10 However, this tax base for wealth taxes has often been narrowed through exemptions. These exemptions have been justified most commonly on the grounds of social concerns such as the negative social implications of taxing pension assets. Further liquidity issues (eg – farm assets), supporting entrepreneurship and investment (eg- business assets), avoiding valuation difficulties ( eg- artwork and jewellery) and preserving countries cultural heritage (eg – artwork and antiques) have also been cited as reasons for wealth tax reliefs. While some of these exemptions can be justified, they have led to the reduction of revenue raised from wealth taxes. They have also contributed to wealth taxes being less equitable as the wealthiest such as businesses benefit from these exemptions defeating the very purpose of imposing a wealth tax which is to meet its redistributive goals.11

Narrow tax bases in wealth taxation often leads to tax avoidance and evasion opportunities. For example, Spain’s 1994 wealth tax exemption for the shares of owner managers resulted in wealthy businesses reorganizing their activities to reap benefits of the exemption resulting in a significant erosion of the wealth tax base.12

Further, several other factors have also discouraged countries to sustain a wealth tax. They are namely, the difficulty in determining the tax base or what assets to be taxed, underreporting and undervaluation of assets, difficulty in measuring wealth taxes13, distinguishing between individuals who are asset rich but cash poor, the constant need to value assets and audit returns increasing administrative and enforcement costs .

Low revenue collection as well as the other reasons discussed have led to the abolishing of wealth taxes in most countries (See Table 1 for details) . Tax revenue from individual net wealth taxes in 2016 ranged from only 0.2% of GDP in Spain to 1.0% of GDP in Switzerland. Sri Lanka’s experience with wealth taxation was no different with the tax yielding low revenue as reported by the 1990 Tax Commission.14

Conclusion

Taxing the wealth of the rich to generate income and to eliminate economic inequality sounds promising in terms of political debate. However, wealth taxes have failed to generate adequate revenue, failed to meet redistributive goals as a result of narrow tax bases, proven to have high administrative and enforcement costs, resulted in tax evasion and avoidance due to underreporting and undervaluation of assets, increased the risk of capital flight and access to tax havens and may have contributed to the reduction of investment and employment.

Therefore, imposing a wealth tax may not be the ideal policy response to Sri Lanka’s low tax revenue, especially given the country’s previous experience with the tax yielding low revenue.

Sathya Karunarathne is the Research Analyst at the Advocata Institute and can be contacted at sathya@advocata.org. Learn more about Advocata’s work at www.advocata.org. The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute, or anyone affiliated with the institute.

The United Nations Development Programme (UNDP) and the Central Bank of Sri Lanka (CBSL) have strengthened their partnership to advance financial literacy across the country, with a renewed focus on empowering vulnerable communities, strengthening economic resilience and promoting sustainable development.

The two institutions formally launched the second phase of their collaboration recently, reaffirming their commitment to implementing Sri Lanka’s National Financial Literacy Roadmap (2024–2028), a cornerstone of the National Financial Inclusion Strategy (NFIS).

The partnership was marked by a meeting between Central Bank Governor Dr. P. Nandalal Weerasinghe and UNDP Resident Representative in Sri Lanka Ms. Azusa Kubota, together with officials from both organisations.

Building on technical support provided by UNDP during 2024 and 2025, the latest phase seeks to equip individuals, households and businesses with the knowledge required to make sound financial decisions, improve livelihoods and enhance resilience in an increasingly uncertain economic and climatic environment.

The initiative comes at a crucial juncture as Sri Lanka continues its economic recovery while grappling with climate-related challenges that disproportionately affect rural communities and small enterprises.

A key component of the programme will be strengthening the capacity of government outreach officers across all districts to deliver financial literacy training to rural populations and micro, small and medium enterprises (MSMEs).

The training will be based on the Financial Literacy Curriculum developed by the Central Bank, with UNDP supporting the enhancement of modules through the integration of climate-resilient financial management concepts.

The programme aligns closely with Sri Lanka’s Financial Literacy Roadmap and is expected to contribute significantly to improving financial knowledge and access across the country. It is supported by several development and private-sector partners, including the government of Japan, Chrysalis, VISA and Hirdaramani-Lacoste.

Speaking on the importance of the initiative, Central Bank Governor Dr. Weerasinghe said the partnership would help broaden the reach of financial literacy efforts while addressing emerging challenges such as climate-related financial risks.

“We particularly welcome the focus on strengthening financial resilience, climate-related financial preparedness, public awareness campaigns and capacity-building through Training-of-Trainers programmes, he said.

He noted that the initiatives would ensure that different segments of society gain access to practical financial knowledge and develop the skills necessary to foster responsible financial behaviour and improve their overall financial well-being.

UNDP Resident Representative Ms. Kubota underscored the critical role financial literacy plays in creating inclusive and resilient economies.

“Financial literacy is a critical foundation for inclusive and resilient economies. Through our partnership with the Central Bank of Sri Lanka, we have been working to empower individuals, particularly those most vulnerable, with the knowledge and tools needed to make informed financial decisions and build secure livelihoods, she said.

By Ifham Nizam

The government’s decision to ban the export of mineral resources in raw form and place all future mineral exploration under state control has triggered fresh debate over how Sri Lanka should develop its untapped mineral wealth and attract foreign investment.

Announcing the new National Mineral Policy, Industry and Entrepreneurship Development Minister Sunil Handunnetti said the country had long failed to capture the full value of its mineral resources by exporting them with minimal processing.

“We will no longer allow mineral resources to leave the country in raw form,” the minister said, arguing that Sri Lanka must move towards value-added industries that generate greater economic returns.

A key feature of the new policy is the transfer of all mineral exploration activities to the state-run Geological Survey and Mines Bureau (GSMB). Under the new system, the GSMB will carry out exploration, publish geological data and subsequently invite investors to participate in commercially viable projects.

Handunnetti defended the move by citing what he described as the failure of the previous licensing regime. According to government figures, 471 exploration licences had been issued since 1993, but only 28 advanced to mining operations, with just 12 remaining active today. The minister alleged that some companies had used exploration licences to boost corporate valuations rather than develop actual mining projects.

He also stressed that mineral deposits located beneath privately owned land belong to the state and should be developed in the national interest.

However, the reforms are likely to attract close scrutiny from foreign investors seeking opportunities in Sri Lanka’s mineral sector.

An independent industry analyst said the policy’s emphasis on value addition is consistent with global trends, as countries increasingly seek to process critical minerals domestically rather than export raw materials.

“The more difficult question is whether a state-controlled exploration model can generate the confidence required by international investors,” the analyst said. “Investors will want access to reliable geological data, transparent licensing procedures and predictable regulations before committing significant capital.”

The analyst noted that the government’s plan to publish exploration data before inviting investment proposals could help improve transparency, but its success would depend on how scientifically the process is implemented.

Sri Lanka possesses commercially valuable deposits of graphite, mineral sands, ilmenite, rutile, garnet, silica and phosphate. As global demand for industrial and strategic minerals continues to grow, the new policy represents a significant test of whether stronger state involvement can translate geological potential into investment, industrial development and export earnings.

“The success of the strategy may ultimately depend on whether the government can balance tighter control over mineral resources with the policy certainty and commercial incentives that international investors typically seek,” the analyst said.

By Sanath Nanayakkare

The Institute of Chartered Accountants of Sri Lanka (CA Sri Lanka) felicitated Ms. Samudika Jayaratna, the 42nd Auditor General of the Democratic Socialist Republic of Sri Lanka, at a special ceremony held on Thursday at the Institute.

The event was organised in recognition of her landmark appointment as the first woman to hold this distinguished constitutional office, as well as her decades of dedicated service to the nation’s public financial governance.

The ceremony reflected the accounting profession’s pride in one of its most accomplished members, who has attained the highest constitutional office in public audit. Ms. Jayaratna was warmly received by the President of CA Sri Lanka, Tishan Subasinghe, Vice President Ms. Anoji de Silva, members of the Council, and Chief Executive Officer Ms. Lakmali Priyangika.

A Fellow Member of CA Sri Lanka, Ms. Jayaratna’s appointment stands as a powerful testament to her exemplary professional journey spanning over 25 years. Her career has been defined by an unwavering commitment to excellence, integrity, and the highest standards of public accountability.

The felicitation ceremony drew a large and distinguished gathering, including Chartered Accountants and officials from the National Audit Office.

Complaint of custodial deaths and torture submitted to UN

India provides military stores worth USD 5.5 mn to SL

India promotes INR-LKR settlement mechanism

UK Trade Envoy here for high-level trade and investment engagements

Govt. failure to fill top two courts’ vacancies leaves Judiciary in a conundrum

UNDP, Central Bank deepen financial literacy drive to build economic resilience

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoCIABOC summons Yoshitha over his participation in British Navy training programme

-

Sports2 days ago

Sports2 days agoTharanga set for high-profile javelin clash in Ostrava

-

News5 days ago

News5 days agoJustice Minister responds to social media claims he represented Easter Sunday ringleader

-

News4 days ago

News4 days agoCommonwealth lawyers urge Lanka to uphold rule of law

-

Features3 days ago

Features3 days agoPolitics of protected species

-

News2 days ago

News2 days agoTheft of USD 2.5 mn from Treasury: CoPF accused of complicity in NPP cover-up

-

News1 day ago

News1 day agoBeijing Capital Airlines to resume flights to Colombo signalling boost to tourism

-

Features3 days ago

Features3 days agoOf Whales and Submarines: Sri Lanka’s Security Dilemma