Business

Reform or perish, it’s not too late

Sri Lankan economy in historic crisis

By K.D.D.B Vimanga and Naqiya Shiraz

The Sri Lankan economy faces a historical crisis. The root causes are the twin deficits. First, the persistent fiscal deficit – the gap between government expenditure and income. Second, the external current account deficit – the gap between total exports and imports. The problems have been festering for too long. Without urgent reforms, the crisis could easily morph into a full-blown debt crisis.

Sovereign debt workouts are extremely painful for citizens. A mangled debt restructuring can perpetuate the sense of crisis for years or even decades. A return to normal economic activity may be delayed, credit market access frozen, trade finance unavailable.

With the global pandemic, these are unusual and difficult times. The next five years are going to be crucial for the country. The problems can no longer be avoided and should be faced squarely. The journey ahead is going to be painful but the longer these are delayed the worse the problem becomes and the magnitude of the damage compounds.

With the global pandemic, these are unusual and difficult times. The next five years are going to be crucial for the country. The problems can no longer be avoided and should be faced squarely. The journey ahead is going to be painful but the longer these are delayed the worse the problem becomes and the magnitude of the damage compounds.

State of the Economy

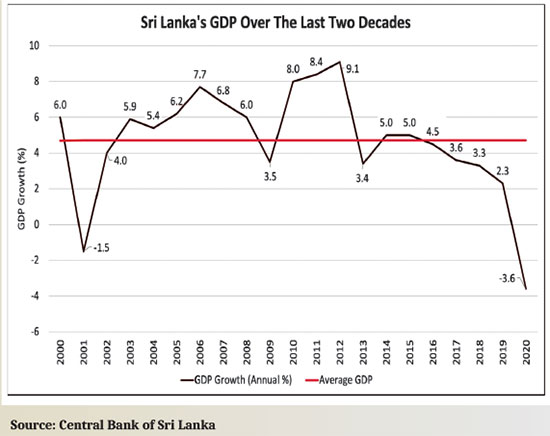

The new government inherited a fragile economy, battered by the Easter attacks of 2019, the constitutional crisis of October 2018 and the worst drought in 40 years in 2017. With the pandemic in 2020 Sri Lanka’s economy shrank by 3.6% with all sectors of the economy contracting.

Yet, the pandemic is not the sole cause – it only accelerated the decline of Sri Lanka’s economy that was weak to begin with. The country has long been plagued by structural weaknesses, with growth rates in the last few years even below the average growth rate during the war. Mismanaged government expenditure coupled with a long term decline in revenue have characterised Sri Lanka’s fiscal policy. As of 2020 total tax as a percentage of GDP fell to just 8%, while recurrent expenditure increased.

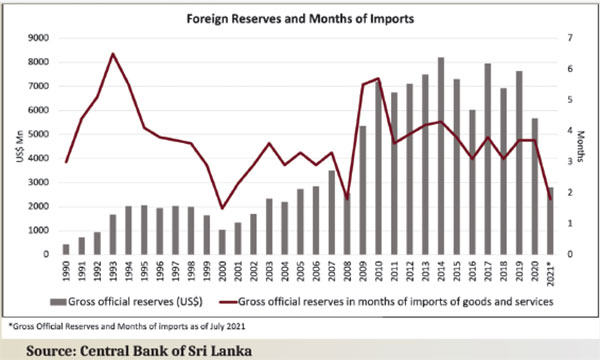

Borrowing to finance the persistent budget deficits is proving to be unsustainable. Total government debt rose to 101% of GDP in 2020 and has grown since. Sovereign downgrades have shut the country from international debt markets. The foreign reserves declined from US$ 7.6 bn in 2019 to US$ 5.7bn at the end of 2020 and to US$ 2.8 bn by July 2021. This level of reserves is equivalent to less than two months of imports. With future debt obligations also in need of financing, the situation is dire.

The import restrictions placed to combat this foreign exchange crisis have failed to achieve their purpose and are doing more harm than good. imports rose 30% in the first half of 2021 compared to 2020 despite stringent restrictions.

The problem lies not in the trade policy but in loose fiscal and monetary policy that has increased demand pressures within the economy, drawing in imports and leading to the balance of payments crisis and consequently the depreciation of the currency.

Measures by the Central Bank to address this by exchange rate controls and moral suasion have caused a shortage of foreign currency leading to a logjam in imports.

Fundamental and long-running macroeconomic problems were intensified by the pandemic.Import restrictions, price and exchange controls do not address the real causes.

Treating symptoms instead of the underlying causes is a recipe for disaster.

The continuation of such policies will lead to the deterioration of the economy, elevate scarcities, disadvantage the poor who are more vulnerable and in the long run lead to even higher prices and lower output due to lack of investment.

Sri Lanka’s GDP growth over the last decade has been alternating between short periods of high growth and prolonged periods of low growth. This is a result of the state-led, inward looking policies of the last decade.

A comprehensive reform agenda must be built around five fundamental pillars:

i) fiscal consolidation – The need to manage government spending within available resources and to reduce debt are paramount. Revenue mobilization must improve but the control of expenditure cannot be ignored. Budgetary institutions must be strengthened and there must be reviews not only of the scale of spending but also the scope of Government.

ii) Much of government expenditure is rigid – the bulk comprises salaries, pensions and interest so reducing these is a long term process. Reforming State Enterprises, especially in the energy sector and Sri Lankan Airlines is less difficult and could yield substantial savings. Continued operation of inefficient and loss-making SOE’s is untenable under such tight fiscal conditions. Financing SOE’s from state bank borrowings and transfers from government reduces the funds available for vital and underfunded sectors such as healthcare and education. Excessive SOE debt also weakens the financial sector and increases the contingent liabilities of the state. Therefore SOE reforms commencing with improving governance, transparency, establishing cost reflective pricing and privatisation are necessary. This can take a significant weight off the public finances and by fostering competition contribute to improvements in overall economic productivity.

iii) Tighten monetary policy and maintain exchange rate flexibility. Immediate structural reforms include, Inflation targeting, ensuring the independence of the central bank by way of legislation and enabling the functioning of a flexible exchange rate regime. Further significant attention has to be placed on the financial sector stability with a cohesive financial sector consolidation plan, with special emphasis on restructuring of SOE debt.

iv) Supporting trade and investment. Sri Lanka cannot achieve economic growth without international trade which means linking to global production sharing networks. Special focus has to be given to reducing Sri Lanka’s high rates of protection which creates a domestic market bias in the economy along with measures to improve trade facilitation and attract new export oriented FDI.

Attempts to build local champions supported by high levels of protection have

(a) diverted resources away from competitive businesses,

(b) created a hostile environment for foreign investment,

(c) been detrimental to consumer welfare,

(d) dragged down growth

v) Structural reforms to increase productivity and attract FDI – Productivity levels in Sri Lanka have not matched pace with the rest of the growing economies. The reforms mentioned above are extensively discussed in Advocata’s latest publication “Framework for Economic Recovery”.

Sri Lanka stumbled into the coronavirus crisis in bad shape,with weak finances; high debt and widening fiscal deficits. It no longer has the luxury to delay painful reforms. Failure to do so will not only jeopardize the economy; it could even spawn social and humanitarian crises.

Naqiya Shiraz is the Research Analyst at the Advocata Institute and can be contacted at naqiya@advocata.org.K.D.D.B. Vimanga is a Policy Analyst at the Advocata Institute. He can be contacted at kdvimanga@advocata.org.

CEAT Kelani Holdings has been adjudged the Best Tyre Manufacturer in the ‘Component Manufacturer’ Category at the country’s inaugural Automobile Industry Awards presented by the Automobile Industry Council (AIC) of Sri Lanka, in a significant endorsement of the company’s leadership in the country’s fast-evolving vehicle assembly sector.

The awards were presented at Temple Trees at a ceremony attended by government ministers, senior public officials, industry leaders and stakeholders from across Sri Lanka’s automobile ecosystem. Conceived as a national platform to recognise excellence, innovation and sustainability, the awards evaluate performance across criteria including technology, market impact, customer satisfaction and industry leadership.

CEAT Kelani’s recognition reflects its commanding position in the Original Equipment (OE) tyre segment, where the company supplies tyres for more than 90% of the vehicles assembled in Sri Lanka. Having entered the local vehicle assembly industry in 2012 with its first OE tyre supply, CEAT has rapidly established itself as the preferred tyre partner for assemblers, supplying over 150,000 OE tyres annually across a diverse range of vehicles including cars, SUVs, motorcycles, scooters, buses and commercial vehicles.

Today, CEAT tyres are fitted as original equipment on more than 30 locally assembled vehicle models spanning 11 global brands, underscoring the confidence placed in the company’s product quality, consistency and performance.

The company’s leadership in this segment is reinforced by its achievement of IATF 16949:2016 certification, making it the first tyre manufacturer in Sri Lanka to secure this globally recognised automotive quality standard. This certification affirms CEAT Kelani’s capability to meet the stringent requirements of international automotive OEMs while optimising supply chain efficiency and reliability.

CEAT tyres supplied to vehicle manufacturers undergo rigorous validation processes and have demonstrated superior performance across key parameters such as safety, durability, braking efficiency, ride comfort and noise reduction. Low rolling resistance and minimal vibration further enhance driving efficiency and user experience, aligning with global expectations of modern mobility solutions.

Beyond its industrial impact, CEAT Kelani also contributes significantly to the national economy. By manufacturing tyres locally, the company helps conserve valuable foreign exchange through import substitution, while sourcing 100% of its natural rubber requirements domestically, supporting the livelihoods of more than 10,000 rubber cultivator families.

The Automobile Industry Council, the apex body representing Sri Lanka’s automobile sector, was established under the joint leadership of key government ministries and operates as a private-sector-led, not-for-profit organisation. Its mandate includes driving sustainable growth, strengthening industry competitiveness and fostering collaboration between public and private stakeholders.

Reinforcing its commitment to delivering premium lifestyle value and rewarding experiences to its customers, the Commercial Bank of Ceylon has unveiled a significant enhancement to its Max Loyalty Rewards platform, enabling its cardholders to convert reward points into airline miles through a strategic integration with the national carrier’s ‘FlySmiLes’ programme and the frequent flyer programmes of other airlines.

Effective immediately, holders of Commercial Bank Premium and Platinum credit cards and Elite debit cards can seamlessly convert their accumulated Max Loyalty Rewards Points into FlySmiLes miles, unlocking faster access to flights and travel privileges with SriLankan Airlines.

The upgrade also encompasses other international frequent flyer programmes, broadening the global travel options available to eligible cardholders by extending the reach of the platform across multiple international travel networks, the Bank said.

The move represents a decisive step in elevating the everyday utility of credit and debit card spend, allowing routine transactions to translate directly into meaningful travel rewards. With SriLankan Airlines expected to be the preferred choice for the majority of customers, the partnership with the national carrier anchors the proposition, offering both familiarity and tangible value in the conversion of points to miles.

To mark the launch, Commercial Bank is offering a highly competitive promotional conversion rate of six Max Loyalty Rewards Points to one FlySmiLes mile, valid through 31st December 2026. The Bank said this market-leading rate significantly accelerates the journey from daily spend to international travel, enhancing the appeal of the Bank’s card portfolio.

Commenting on this latest development, Hasrath Munasinghe, Chief Operating Officer of Commercial Bank, said the enhancement reflects the Bank’s continued focus on delivering differentiated value to its customers. “Max Loyalty Rewards points are among the most valuable benefits offered to our cardholders, turning everyday spending into rewarding experiences,” he said. “Commercial Bank is also the first and only Bank to offer Max Loyalty Rewards points to both credit and debit cardholders, extending these benefits beyond credit cards. By partnering with SriLankan Airlines and other global carriers, we have significantly strengthened the Max Loyalty Rewards platform. Our cardholders can now think beyond conventional rewards and convert their everyday spending into memorable travel experiences. This is about enabling them to go further, more often, with greater ease.”

The airline miles conversion feature is available at no additional cost to eligible cardholders, with no enrolment or processing fees. Access is fully integrated into the existing Max Loyalty Rewards platform, allowing users to log in with their current credentials, view balances, and convert points instantly alongside standard merchant redemptions.

C.W. Mackie PLC has appointed Mangala Perera as its new Group Chief Executive Officer (Group CEO), strengthening its senior management team with an experienced corporate leader with over 26 years of cross-industry experience.

Perera, who has served as a Director of C.W. Mackie PLC since April 2, 2012, currently holds the position of Executive Director – Group Chief Operating Officer of the company. He has held senior roles in marketing and general management both locally and internationally.

In addition to his responsibilities at C.W. Mackie PLC, Perera serves as Managing Director of Sunquick Lanka (Private) Limited and holds directorships at Sunquick Lanka Properties (Private) Limited, Kelani Valley Canneries Limited, Ceymac Rubber Company Limited and Ceytra (Private) Limited. He is also a Non-Executive Director of Phoenix Industries Limited.

Perera’s academic and professional credentials span multiple disciplines, including a Master’s degree in Financial Economics from the University of Colombo, a BSc (Hons.) Special Degree in Marketing Management from the University of Sri Jayewardenepura and a Postgraduate Diploma in Business and Financial Management from the Institute of Chartered Accountants of Sri Lanka.

He is also a visiting lecturer in Postgraduate Studies in Management at the University of Colombo and the University of Kelaniya, and contributes to several national-level project committees and professional judging panels as an active marketing practitioner.

Beyond the corporate sector, Perera has been involved in sports administration and previously served as President of the Sri Lanka Mercantile Volleyball Federation, where he played a key role in promoting volleyball and beach volleyball in Sri Lanka.

The company said the appointment reflects its continued focus on strengthening leadership and driving future growth.

Govt. seeks INTERPOL assistance to bring Basil Rajapaksa back

Ravi warns against attempts to stir communal tensions over Easter attacks probe

AG undertakes High Court Judge will not be summoned over Yoshitha Rajapaksa case

Rs. 75 million worth of ‘Kush’ seized at BIA

Eknaligoda disappearance case hearing fixed for June 26

Dengue cases exceed 44,000

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoRelease of 2025 O/L results likely to be delayed

-

Sports6 days ago

Sports6 days agoTharanga set for high-profile javelin clash in Ostrava

-

News5 days ago

News5 days agoBeijing Capital Airlines to resume flights to Colombo signalling boost to tourism

-

News6 days ago

News6 days agoTheft of USD 2.5 mn from Treasury: CoPF accused of complicity in NPP cover-up

-

Features4 days ago

Features4 days agoKilling of Colombo’s ancient trees — a warning on UN’s World Desertification Day – 17 June

-

Opinion6 days ago

Opinion6 days agoDecoding Trump’s 12.5% “Forced Labor Tariff” on Sri Lanka

-

Opinion6 days ago

Opinion6 days agoPalm leaf manuscripts of Sri Lanka – Part V

-

News1 day ago

News1 day agoCreditor not yet paid