Business

Rupee volatility exposes deeper structural weaknesses, says fintech industry leader

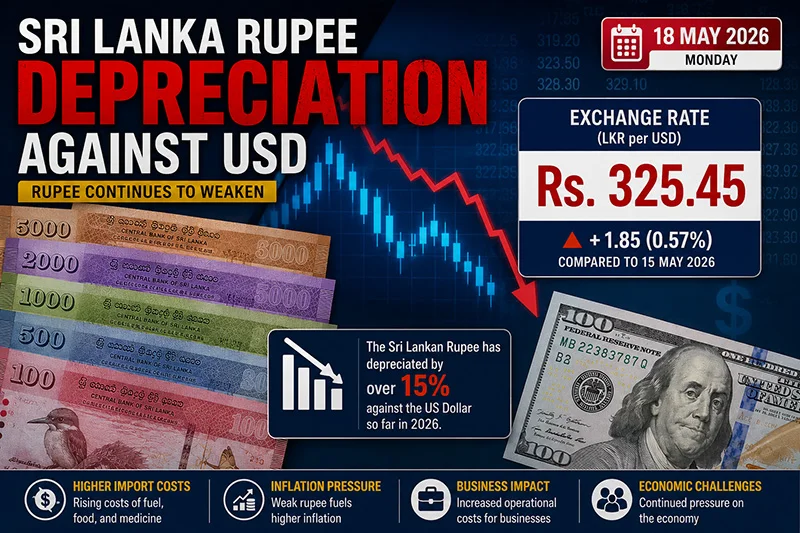

The continued depreciation pressure on the Sri Lankan rupee is exposing deep-rooted structural weaknesses within the economy, while simultaneously creating limited opportunities for export-oriented sectors, according to Rajkumar Kanagasingam.

Kanagasingam warned that while some export industries may temporarily benefit from a weaker currency, the broader economic strain caused by rising import costs, inflationary pressures, and investor uncertainty continues to weigh heavily on businesses and consumers alike.

Speaking to The Island Financial Review, he said local industries are struggling to absorb rising costs linked to imported raw materials, machinery, fuel, and intermediate goods as the rupee remains under pressure.

“Local industries are coping through cost-cutting measures, selective price increases, tighter inventory management, and delaying certain capital investments,” he said. “Many businesses are also exploring alternative suppliers and improving operational efficiency to manage rising import-related costs.”

He noted that import-dependent sectors are among the hardest hit by currency depreciation, particularly construction, transport, pharmaceuticals, manufacturing, and food imports, where businesses face mounting operational expenses and shrinking margins.

At the same time, Kanagasingam observed that export-oriented sectors such as apparel, tea, IT services, tourism, and businesses promoting local substitutes may gain some competitive advantage from the weaker rupee, as foreign exchange earnings translate into higher rupee revenues.

“A weaker rupee can improve the competitiveness of export-oriented sectors by increasing rupee earnings from foreign exchange,” he explained. “However, the benefits may be partially offset by higher imported input costs, energy expenses, and broader economic pressures.”

He stressed that small and medium-scale enterprises (SMEs) remain significantly more vulnerable than larger corporates during periods of currency instability.

“SMEs generally have limited financial buffers, less access to foreign currency, and weaker bargaining power,” he said. “Larger corporates are typically better positioned to manage exchange rate fluctuations through stronger reserves, export earnings, and diversified financing options.”

Kanagasingam added that consumers are ultimately carrying much of the burden created by rupee depreciation, with higher prices increasingly visible across food, transport, utilities, imported goods, and daily services.

“In many cases, increased business costs are gradually passed on to consumers,” he said, warning that sustained currency weakness could continue to fuel inflationary pressure across the economy.

He also pointed to a growing shift among local manufacturers toward localization and import substitution as businesses attempt to reduce reliance on imported inputs.

“There is growing interest in strengthening domestic supply chains and local production,” he noted. “However, Sri Lanka still faces challenges in terms of industrial scale, technology, and the availability of locally sourced raw materials.”

According to Kanagasingam, persistent currency volatility also undermines investor confidence and complicates long-term industrial planning.

“Currency fluctuations create uncertainty for investors, particularly in areas such as pricing, financing, debt servicing, and long-term project planning,” he said. “Greater exchange rate stability generally improves investor confidence and supports long-term industrial growth.”

He urged policymakers and the Central Bank to prioritize macroeconomic stability, foreign reserve strengthening, export expansion, energy efficiency, and targeted support for SMEs in order to cushion the impact of exchange rate volatility.

“The priority should be maintaining macroeconomic stability, strengthening foreign reserves, supporting export growth, improving energy efficiency, encouraging local production, and providing targeted support for SMEs,” he said. “Consistent and predictable policy measures are also essential to strengthen investor confidence.”

Kanagasingam further cautioned that prolonged rupee depreciation could eventually lead to job losses in sectors heavily dependent on imports.

“Prolonged depreciation could place pressure on import-dependent industries, potentially leading to reduced production, delayed expansion, and job losses, particularly among smaller businesses and vulnerable sectors,” he warned.

Describing the current exchange rate situation as more than a temporary market adjustment, Kanagasingam said Sri Lanka must address its long-standing structural vulnerabilities if it hopes to achieve lasting currency stability.

“It reflects both short-term external pressures and deeper structural challenges within the economy,” he said. “These include high import dependence, limited export diversification, debt-related pressures, and the need for stronger foreign exchange generation over the long term.”

Economic analysts note that the rupee’s trajectory in the coming months will remain closely tied to external debt management, reserve accumulation, export performance, remittance inflows, and broader investor sentiment surrounding Sri Lanka’s economic recovery efforts.

By Ifham Nizam

The weekly Colombo Tea Auction concluded with offerings increasing to 6.5 million kilogrammes, a marginal rise from the previous week’s 6.4 million kilogrammes. However, the market witnessed a significant pullback from key international buyers, leading to a subdued trading atmosphere and declining prices across several categories.

Industry sources reported a noticeable lack of interest from shippers to the traditional markets of the United Kingdom and the European continent. While shippers to the Commonwealth of Independent States (CIS) and the Middle East maintained a presence, their participation was described as selective and at lower price levels. Buyers from Japan and China also operated at reduced levels, with South African shippers showing minimal engagement.

This cautious stance from the shipping community cast a shadow over the Ex-Estate sector, which offered 1.0 million kilogrammes. The overall quality of teas in this category was described as relatively uninteresting, leading to a weakening of prices. In the Western High Grown category, prices for the best available BOP/BOPF grades declined by Rs. 20 to 40 per kilogramme, while the plainer varieties saw a drop of about Rs. 20 per kilogramme. A fair quantity of these teas remained unsold due to a lack of suitable bids.

Nuwara Eliya teas attracted little to no interest, with the majority of offerings remaining unsold. Uda Pussellawa BOPs weakened further by up to Rs. 50 per kilogramme, while the corresponding BOPFs struggled to maintain their previous price levels. In the Uva region, BOPs saw prices fall by Rs. 50 per kilogramme, though the BOPF varieties were relatively more stable. The High and Medium Grown CTC teas continued to be a weak feature, with many lots unsold and those that were sold recording a price drop of Rs. 20 to 40 per kilogramme. Off-grades and dust grades also experienced a sluggish market, with fair volumes remaining unsold.

In contrast to the gloom in the High Growns, the Low Grown sector, which totalled approximately 2.7 million kilogrammes, met with more encouraging demand. The Leafy and Semi-Leafy categories saw fair demand, while the Tippy and Premium categories were met with good interest. While some well-made varieties in the Leafy catalogues remained firm, many other grades experienced easier prices. However, the Tippy catalogue saw high-priced FBOPs holding firm and the FF1s generally becoming dearer. The Premium catalogue, featuring tippy teas, also met with good demand and saw prices appreciate overall.

Based on Forbes & Walker Tea Brokers comments

By Sanath Nanayakkare

The Asian Development Bank (ADB) has formally entered into its first partnership with the International Committee of the Red Cross (ICRC), marking a significant step towards integrating humanitarian action with long-term development efforts in fragile and conflict-affected regions across Asia and the Pacific.

A Letter of Intent establishing the collaboration was signed on June 10 by ADB Vice-President for Sectors and Themes Fatima Yasmin and ICRC Director-General Pierre Krähenbühl. The agreement provides a framework for coordinating programmes, exchanging knowledge on emerging humanitarian challenges, promoting innovation and sharing best practices through joint events and publications.

The partnership brings together ADB’s development expertise and financing capabilities with the ICRC’s operational experience and access to communities affected by conflict and violence.

Highlighting the significance of the initiative, ADB President Masato Kanda wrote on X on June 17 that the partnership would help strengthen resilience in fragile and conflict-affected areas.

“By bringing together ADB’s longer-term development perspective with ICRC’s humanitarian field presence and operational experience, we can better support people affected by conflict and violence,” Kanda said.

Speaking at the signing ceremony, Yasmin said today’s interconnected challenges require development institutions to move beyond traditional approaches.

“The ICRC brings trusted access to affected communities and credibility in environments that ADB alone cannot easily reach,” she said.

Krähenbühl described the agreement as an important step towards bridging humanitarian assistance and long-term development, adding that it could create opportunities for joint responses in fragile settings across the region.

A Sri Lankan socio-economist told The Island Financial Review that the partnership reflects a growing recognition among development institutions that conflict, fragility and climate-related shocks are becoming major constraints on economic progress.

“Traditionally, development banks focused on long-term infrastructure and economic projects while humanitarian agencies addressed immediate crises. This partnership seeks to connect those two worlds by reducing vulnerability before crises deepen,” he said.

Prime Residencies, the real leader in the modern real estate, and a subsidiary of Prime Group, officially marked the commencement of construction on its latest ultra-luxury residential development, THE GOLF, with its groundbreaking ceremony held at the project site on Lake Drive, Colombo 8. The event brought together key stakeholders and project partners to mark the ceremonial breaking of the ground, signalling that a vision long in the making is currently under construction.

Cricket journalist and broadcast legend Qamar Ahmed dies aged 88

Stafanie Taylor, spinners help West Indies overcome Scotland threat

Showers will occur at times in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Thirty-five killed as gunmen attack Niger’s biggest airport

Creditor receives USD 2.5 mn as Lankan public bears loss from theft of Treasury funds

Former Minister Nalin raises defence of double jeopardy

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News4 days ago

News4 days agoRelease of 2025 O/L results likely to be delayed

-

Sports4 days ago

Sports4 days agoTharanga set for high-profile javelin clash in Ostrava

-

Features5 days ago

Features5 days agoPolitics of protected species

-

News3 days ago

News3 days agoBeijing Capital Airlines to resume flights to Colombo signalling boost to tourism

-

News4 days ago

News4 days agoTheft of USD 2.5 mn from Treasury: CoPF accused of complicity in NPP cover-up

-

News6 days ago

News6 days agoCommonwealth lawyers urge Lanka to uphold rule of law

-

Opinion4 days ago

Opinion4 days agoDecoding Trump’s 12.5% “Forced Labor Tariff” on Sri Lanka

-

Features2 days ago

Features2 days agoKilling of Colombo’s ancient trees — a warning on UN’s World Desertification Day – 17 June