Features

Tariffs as business deals?

From White House to Wall Street:

![]() I am going to examine the financial market repercussions of President Donald Trump’s 2025 tariff policies, focusing on equities, bonds, derivatives, and interest rates. It explores how asymmetric information and alleged insider trading influenced market dynamics, highlighting the challenges posed to market integrity and investor confidence.

I am going to examine the financial market repercussions of President Donald Trump’s 2025 tariff policies, focusing on equities, bonds, derivatives, and interest rates. It explores how asymmetric information and alleged insider trading influenced market dynamics, highlighting the challenges posed to market integrity and investor confidence.

In 2025, President Donald Trump’s administration implemented a series of tariffs targeting major trading partners, including China, Canada, and Mexico. These policies aimed to protect domestic industries but resulted in significant volatility across global financial markets. The sudden shifts in trade policy introduced uncertainty, affecting various asset classes and raising concerns about the exploitation of insider information.

In response to escalating market turmoil and international pressure, President Trump announced a 90-day deferral on certain tariffs, via social media on April 9, 2025. However, the announcement’s ambiguity led to continued market instability.

Pre-Tariff Market Conditions

(February 2025)

In February 2025, US financial markets were experiencing relative stability. The S&P 500 was trading near record highs, buoyed by strong corporate earnings and positive economic indicators. Interest rates remained steady, with the 10-year Treasury yield hovering around 3.9%, reflecting moderate inflation expectations and a balanced economic outlook. The CBOE Volatility Index (VIX), a measure of market volatility, was subdued, indicating investor confidence.

Impact on Financial Markets

Equities and Traditional Investment Strategies

The announcement of tariffs led to a sharp decline in US stock markets. Major indices, such as the Dow Jones Industrial Average and the Nasdaq Composite, experienced significant losses, with the Nasdaq entering bear market territory after a 5.82% drop. The traditional 60/40 investment strategy, allocating 60% to equities and 40% to bonds, proved ineffective during this period, as both asset classes suffered losses due to rising bond yields and falling stock prices (Figure 1).

Market Indices (S&P 500, Nasdaq, Dow Jones): Major crashes occurred on April 3–4, 2025, following the tariff imposition. Slight recovery or stabilisation followed Trump’s deferral tweet on April 9, but markets dipped sharply again on April 10 (Table 1).

Market Reaction to Tariff Imposition

(April 2–5, 2025)

* April 3, 2025: The S&P 500 plummeted by 4.88%, the Nasdaq Composite fell by 5.97%, and the Dow Jones Industrial Average declined by 3.98%. The Russell 2000 entered bear market territory, dropping over 20% from its recent peak.

* April 4, 2025: Markets continued their downward trajectory. The S&P 500 fell an additional 5.97%, the Nasdaq Composite decreased by 5.82%, and the Dow Jones Industrial Average dropped by 5.50%.

* April 5, 2025: The newly imposed tariffs officially took effect, further exacerbating market volatility and investor uncertainty.

* Over this period, US stock markets lost approximately $6.6 trillion in value, marking the largest two-day loss in history.

Market Response to Tariff Deferral

(April 9–11, 2025)

* April 10, 2025: Despite the deferral, the S&P 500 declined by approximately 15%, and long-term Treasury bonds faced significant selling pressure. The US dollar weakened, and gold prices surged as investors sought safe-haven assets.

* April 11, 2025: Consumer sentiment plummeted, with the University of Michigan Consumer Sentiment Index dropping to 50.8, the second-lowest level since records began in 1952. This decline reflected widespread economic pessimism amid the ongoing trade tensions.

Bond Market and Interest Rates

The bond market reacted to the tariffs with increased yields, reflecting investor concerns about inflation and economic growth. The US 10-year Treasury yield rose to 4.358%, indicating expectations of higher interest rates. This rise in yields contributed to the decline in bond prices, further challenging traditional investment strategies.

10-Year Treasury Yield: Climbed steadily from 3.9% to 4.358% (April 2–21), suggesting increased inflation expectations and risk premium. The bond market experienced significant fluctuations during this period. Therefore, investors demanded higher returns for perceived increased risk. This rise in yields indicated expectations of higher inflation and potential economic slowdown due to the tariffs. (Table 2).

Derivatives and Market Volatility

The derivatives market, including options and futures, experienced heightened volatility in response to tariff announcements. The CBOE Volatility Index (VIX), often referred to as “Wall Street’s fear index,” spiked to its highest level since 2020, closing at 45.31 points. This surge in volatility presented both risks and opportunities for investors, particularly those with access to timely information.

VIX Volatility Index: Rose from 19 on April 2 to a peak of 45.31 on April 4, indicating extreme market fear. The VIX spiked to 45.31, its highest level since 2020, indicating heightened market anxiety (Table 3).

Asymmetric Information and Insider Trading Allegations

Allegations of insider trading emerged during the tariff saga, highlighting concerns about asymmetric information. Congresswoman Marjorie Taylor Greene faced scrutiny for stock transactions made shortly before tariff announcements, including purchases in companies like Amazon and Tesla, and the sale of Treasury bills. While Greene denied insider knowledge, the timing of these trades raised questions about the potential exploitation of non-public information (The Times, 2025).

Additionally, unusual trading patterns in S&P 500 futures preceding major policy shifts suggested possible insider activity. Although direct evidence linking these trades to White House insiders remains inconclusive, the patterns underscore the challenges in detecting and preventing insider trading in policy-driven markets (Los Angeles Times, 2025).

Tariff Decisions as Business Deals

While tariffs are typically seen as instruments of trade policy aimed at protecting domestic industries or rebalancing trade deficits, the Trump administration’s 2025 tariff imposition and abrupt deferral appear less rooted in strategic policy and more akin to short-term market manipulations. These decisions unfolded not through institutional processes or legislative debates, but rather through presidential tweets and sudden reversals, strongly suggesting a deal-making mindset characteristic of business negotiations rather than public governance.

The Role of Asymmetric Information and Market Elites

Insider trading is traditionally associated with illegal access to non-public corporate information. However, in this case, asymmetric political information—known only to a select few close to power—may have created an opportunity to profit.

Market actors with proximity to decision-makers, or even sophisticated algorithms tied to social media monitoring, could have anticipated the tariff deferral.

Billionaire investors and influencers like Elon Musk, who maintain both financial influence and political access, are often speculated to benefit from such opaque decision-making environments. The quick reversal of tariffs led to a surge in tech stocks, many of which form the core holdings of large institutional investors, hedge funds, and elite entrepreneurs.

For example: The Nasdaq rebounded by 1.5% following the deferral tweet. Options trading volumes spiked on tech-heavy indices, indicating pre-positioning by well-informed actors. Reports from Bloomberg and Reuters noted unusual activity in Tesla call options shortly before the deferral (Reuters, 2025; Bloomberg Markets, 2025).

A Business Deal Mindset

Trump’s own language underscores the deal-making philosophy. The President tweeted that the tariffs were a “strong hand in negotiations” and “paused for talks with China”, using terms more common in corporate boardrooms than diplomatic channels. This rhetoric, combined with the lack of institutional transparency, raises serious concerns about the manipulation of public policy for private gains.

In this light, the administration’s behaviour is not reflective of classical economic policy objectives like comparative advantage or strategic protectionism. Instead, it aligns with the wealth-maximising tactics of a private enterprise, where the aim is to control narrative, timing, and volatility to benefit select stakeholders.

Conclusions

More critically, the Trump tariff saga of 2025 blurs the lines between public policy and private profit. The opacity, erratic timing, and informal communication channels—particularly via presidential tweets—suggest that these were less about coherent trade strategies and more akin to orchestrated business maneuvers. The reactive movements of major indices, coupled with unusual options trading patterns and speculative capital flows, indicate that market elites likely capitalised on volatility, benefiting from privileged access or predictive positioning based on asymmetric information.

This raises serious concerns about market integrity and the ethical boundaries between governance and profiteering. When financial markets are left vulnerable to abrupt and opaque political actions, especially ones lacking institutional oversight, the door opens to manipulation, insider trading, and erosion of public trust.

In sum, the 2025 Trump tariff episode serves as a cautionary tale—one that highlights the dangers of politicising economic policy, the vulnerabilities of global markets to personalised decision-making, and the importance of upholding the foundational principles of fairness, transparency, and accountability in modern financial systems.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT University, Malabe. He is also the author of the “Doing Social Research and Publishing Results”, a Springer publication (Singapore), and “Samaja Gaveshakaya (in Sinhala). The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official policy or position of the institution he works for. He can be contacted at saliya.a@slit.lk and www.researcher.com)

When the strait shuts:

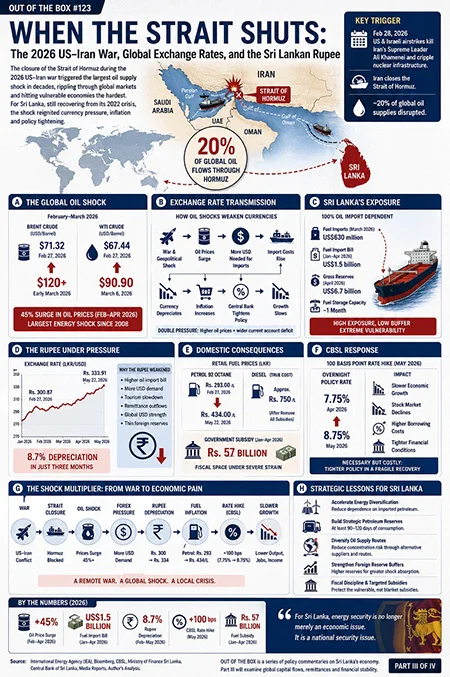

In the early hours of February 28, 2026, the world changed. Joint United States and Israeli airstrikes on Iran, meticulously planned, devastatingly executed, killed Supreme Leader Ali Khamenei, destroyed large swathes of Iran’s nuclear infrastructure, and triggered the most consequential military confrontation in the Middle East since the Iraq War. What followed was not merely a regional conflict. It was an economic earthquake felt from the trading floors of New York to the fuel queues of Colombo.

In the early hours of February 28, 2026, the world changed. Joint United States and Israeli airstrikes on Iran, meticulously planned, devastatingly executed, killed Supreme Leader Ali Khamenei, destroyed large swathes of Iran’s nuclear infrastructure, and triggered the most consequential military confrontation in the Middle East since the Iraq War. What followed was not merely a regional conflict. It was an economic earthquake felt from the trading floors of New York to the fuel queues of Colombo.

We are going to examine how a war fought in the Persian Gulf rewrote exchange rates across the global economy, and why a small island in the Indian Ocean, still recovering from its own financial near-death experience four years ago, found itself once again staring into an economic abyss.

From Maximum Pressure to Maximum Destruction

On February 28, the strikes began. The operation was vast and transformative. Iran’s air defences were systematically destroyed. Its missile production facilities were crippled. And its political leadership was decapitated. In response, Tehran did something it had always threatened but never done: it closed the Strait of Hormuz.

That decision, to block the 21-mile-wide waterway through which approximately 20% of global oil supplies flow, set off a chain of economic consequences that no government, central bank, or multilateral institution had fully stress-tested for.

The Oil Shock and What It Did to Currency Markets

The numbers tell the story with stark clarity. Brent crude, which had been trading at $71.32 per barrel on February 27, jumped 8% to $77.24 in the first two trading days of the conflict. Within a week, following the declaration that the Strait was “closed,” WTI crude surged more than 35%, the biggest weekly gain since the futures contract began in 1983, ending the week at $90.90. Brent climbed 28% to $92.69 in the same period. By early March, Brent had surged past $120 per barrel. The International Energy Agency characterised it as the “largest supply disruption in the history of the global oil market.”

This was not merely an oil price story. Oil is the world’s most foundational commodity, priced in US dollars, embedded in the cost of virtually every manufactured good, agricultural product, and service. When oil prices surge by 45%, as they did between February and April 2026, the consequences ripple through exchange rates with a logic that is both mechanical and unforgiving.

For oil-importing emerging market currencies, the mathematics were brutal. When oil prices rise in dollars and a country pays for oil in dollars, there are two simultaneous pressures on the exchange rate. First, the country must acquire more dollars to pay for the same volume of imports, increasing demand for the greenback and putting downward pressure on the domestic currency. Second, higher oil prices widen the current account deficit, removing the trade-balance support that usually anchors currencies. This double blow struck Asian, African, and Latin American currencies with particular force. Gasoline prices rose in 106 countries in the three weeks following the start of the conflict. The European Central Bank postponed planned interest rate cuts, raised its inflation forecast, and cut its growth projections.

Oil exporters told a different story. The Gulf states, Saudi Arabia, the UAE, Kuwait, saw windfall revenues at the very moment their physical infrastructure was under threat. Iran’s strikes on Saudi Arabian oil refineries and energy facilities injected volatility into the already fractured GCC calculus: higher oil revenues on one hand, higher security costs and diplomatic complexity on the other.

The Ceasefire and Its Limits

After five weeks of fighting, Pakistan and China delivered a joint peace initiative on March 31, 2026. On April 7–8, the United States and Iran agreed to a two-week ceasefire, with Iran committing to reopen the Strait of Hormuz. Markets reacted with violent relief. The S&P 500 and Nasdaq surged 3–4% in futures markets overnight. Oil prices fell nearly 25% from their peak. Equities that had slid 8–12% from pre-conflict highs began recovering.

But the ceasefire was “relief, not resolution.” The Strait of Hormuz remained at just 5% of pre-conflict shipping traffic five weeks after the ceasefire announcement. Supply chains do not unsnarl overnight. On May 7, the United States conducted further airstrikes on military sites in southern Iran and Tehran following Iranian targeting of US warships. A memorandum of understanding, intended to bring the conflict to a formal end within 60 days, was announced by mediators on June 14, with signing set for June 19. As of this writing, the conflict has not been formally resolved and nuclear negotiations are expected to begin under the framework.

Goldman Sachs projected that under an adverse scenario, 10 weeks of disruption and infrastructure damage, Brent could peak at $160 per barrel before settling at $115 in the fourth quarter of 2026. Even the base case of $105–115 per barrel through mid-year represents a sustained energy shock with no parallel in the post-2008 global economy.

Sri Lanka: The Compound Vulnerability

Sri Lanka has a particular relationship with oil price shocks that is unlike almost any other country of its size. It imports 100% of its oil. Its domestic energy infrastructure is built almost entirely around petroleum products. Its foreign exchange reserves, rebuilt painstakingly from near-zero during the 2022 crisis to $6.46 billion by the time the NPP government assumed office, have since grown sluggishly reaching only $6.87 billion by early 2026, a modest gain that offered little buffer against a shock of this magnitude, remain thin relative to the country’s import requirements. And it routes the overwhelming majority of its oil imports through the Strait of Hormuz.

Sri Lanka has a particular relationship with oil price shocks that is unlike almost any other country of its size. It imports 100% of its oil. Its domestic energy infrastructure is built almost entirely around petroleum products. Its foreign exchange reserves, rebuilt painstakingly from near-zero during the 2022 crisis to $6.46 billion by the time the NPP government assumed office, have since grown sluggishly reaching only $6.87 billion by early 2026, a modest gain that offered little buffer against a shock of this magnitude, remain thin relative to the country’s import requirements. And it routes the overwhelming majority of its oil imports through the Strait of Hormuz.

When that strait closed in March, 2026, Sri Lanka’s exposure was immediate, structural, and arithmetically severe. The fuel import bill jumped 74.7% year-on-year to US$630 million in March, 2026, alone. Reserves fell 3.8% to approximately $6.7 billion after the country spent $1.5 billion on fuel imports in the first four months of the year. Sri Lanka’s monthly storage capacity covers only one month of consumption, making it acutely vulnerable to supply disruptions that persist beyond a few weeks.

The exchange rate impact was direct and rapid. The Sri Lankan rupee, which had traded at approximately Rs. 300 to the US dollar at the start of 2026, fell sharply from early March. The currency tumbled 8.7% from its pre-conflict level within weeks. By late May 2026, commercial bank selling rates stood at approximately Rs. 334 per dollar, a 5.4% year-to-date depreciation against the greenback.

Every rupee of depreciation compounds the damage: a dollar-priced barrel of oil that cost Rs. 21,300 at Rs. 300/$ costs Rs. 23,700 at Rs. 334/$, before accounting for the price rise in the barrel itself.

The compounding of the exchange rate depreciation on top of the oil price surge created a fuel price crisis that has no precedent in the post-2022 recovery period. Petrol 92 at CEYPETCO stations, which stood at Rs. 293 per litre 12 weeks before, had risen to Rs. 434 per litre by late May, a 48% increase in the space of three months. The true import and distribution cost of diesel was approximately Rs. 750 per litre, requiring a government subsidy of Rs. 57 billion over a three-month period to keep pump prices at Rs. 407.

The Central Bank’s Painful Choice

The Central Bank of Sri Lanka faced the classic emerging market dilemma that oil shocks create: a currency under pressure from capital outflows and import costs, combined with inflation driven by energy prices, in a context where raising interest rates to defend the currency would choke off the economic recovery that the country had barely begun.

On May 26, 2026, the CBSL made its call. It raised the overnight policy rate by 100 basis points to 8.75%, its first monetary tightening in three years, and the largest single hike since the depths of the financial crisis in March 2023. Seven out of twelve economists polled by Reuters had predicted only a 25-basis-point move. The shock was deliberate: the CBSL was signalling that price stability had been elevated over growth promotion.

The consequences were immediate. The Colombo Stock Exchange fell 0.8% on the day of the announcement. Growth forecasts were cut, from 4.2% to 3.0% by at least one major equity research firm. The Central Bank Governor acknowledged that the 4–5% growth projection for 2026 was now achievable only “at the lower band.” Capital Economics observed that the rate hike “highlights the country’s vulnerability to the crisis in the Middle East, and is unlikely to be the last unless the crisis subsides soon.

More encouragingly, BMI (a Fitch Solutions unit) projected that the rupee could recover to Rs. 320 per dollar by year-end, on the assumption that the Iran war concludes by June and oil prices ease. An IMF board meeting was scheduled to approve a $700 million tranche to Sri Lanka under the ongoing $2.9 billion programme, a lifeline that, if disbursed, would provide critical reserve support.

The Broader Lesson

What the 2026 Iran war has demonstrated, with a clarity that no academic model can replicate, is that geopolitical shocks are not symmetric in their exchange rate effects. The same event that provides a windfall for oil exporters imposes a compound penalty on oil importers, and the penalty is largest for countries whose currencies are weakest, whose reserves are thinnest, whose import dependence is highest, and whose recovery from previous crises is most recent.

Sri Lanka is, in 2026, the canonical case study. It has done almost everything right since 2022: restructured its debt, rebuilt reserves, maintained an IMF programme, restored exchange rate stability, and begun recovering economically. None of that inoculated it against an exogenous shock of this magnitude. The rupee’s 8.7% fall from pre-conflict levels, the $1.5 billion fuel import bill in four months, the 100-basis-point emergency rate hike, these are the costs a small, import-dependent, oil-importing island economy pays when the world’s energy arteries are severed by war.

There is a policy lesson embedded in these numbers. Sri Lanka’s energy vulnerability, its total dependence on imported fossil fuels routed through a single geopolitical chokepoint, is not merely an economic problem. It is a national security problem. The Strait of Hormuz is not a permanent fixture of reliable global trade. The 2026 war has proven, at enormous cost, that it can be closed. Any serious national energy strategy must treat that closure not as a tail risk but as a planning scenario.

The hard work of diversifying energy sources, accelerating renewable capacity, building strategic petroleum reserves, and reducing the share of petroleum in the import bill is not merely desirable. Since February 28, 2026, it has become existential.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT, Malabe.

Views expressed in this article are personal.)

When discussions turn to Sri Lanka’s freshwater fish diversity and the urgent need to conserve it, attention is often focused on rivers, streams, reservoirs and water quality.

Yet scientists are increasingly finding that what happens on the land surrounding these waterways can be just as important as what happens in the water itself.

A recent study led by researcher Janamina Bandara of the Wildlife Conservation Society, Galle, together with researchers Sudath Nanayakkara and Sahan Randeniya, highlights how changes in forest cover caused by human activities can significantly influence freshwater fish populations in the hill streams surrounding the Sinharaja rainforest.

Their research sheds light on a relatively understudied aspect of tropical freshwater ecosystems—how alterations to vegetation cover, particularly through commercial cultivation such as tea and cardamom plantations, affect fish communities inhabiting headwater streams.

Hidden Riches of Tropical Streams

Forest plant saplings

Sri Lanka’s freshwater ecosystems are globally recognised for their remarkable biodiversity and high levels of endemism. However, despite their ecological significance, many ecological processes operating within these habitats remain poorly understood.

“Freshwater ecosystems in the tropics harbour extraordinary biodiversity, but many of the ecological relationships within these systems are still not fully documented,” researcher Janamina Bandara told The Island.

The study focused on sub-montane streams in the Sinharaja landscape, examining how varying levels of forest cover influence freshwater fish assemblages.

Researchers investigated whether fish communities differed between streams flowing through relatively undisturbed forests and those surrounded by modified vegetation resulting from agricultural activities.

Spotlight on a Critically Endangered Species

Leaf litter bay / Restoration activities

Particular attention was given to the critically endangered Rakwana loach (Schistura madhavai), a highly restricted endemic fish species first described from the Suriyakanda-Rakwana region.

Commonly referred to as a hill-stream loach, the species inhabits clear, fast-flowing streams and is considered highly sensitive to environmental disturbances.

According to Bandara, while broad community-level analyses did not reveal dramatic differences across all fish populations, species-specific responses painted a very different picture.

“Our findings show that Schistura madhavai exhibits a clear preference for streams flowing through intact forest habitats,” he explained. “The species becomes less common in areas where surrounding vegetation has been altered by human activities.”

Why Forests Matter to Fish

Forests bordering streams play multiple ecological roles. They regulate water temperature by providing shade, contribute organic matter that supports aquatic food webs, stabilise stream banks and help maintain water quality.

When these forests are removed or replaced with plantation crops, the resulting environmental changes can cascade through freshwater ecosystems.

Bandara noted that altered forest cover can influence water chemistry, microclimatic conditions, stream-bed composition and the availability of food resources.

“As riparian vegetation changes, a series of environmental conditions within the stream also change. Sensitive species such as Schistura madhavai appear particularly vulnerable to these shifts and may gradually disappear from modified habitats,” he said.

The research suggests that even subtle changes in habitat structure can have disproportionate impacts on species with narrow ecological requirements.

The Importance of Looking Beyond Numbers

Schistura madhavai

One of the most intriguing findings of the study is that ecosystem degradation may not always be apparent when scientists assess entire fish communities collectively.

In some instances, environmental variables appeared to have little effect on overall fish abundance or diversity. However, when individual species were examined separately, clear patterns emerged.

For example, variations in the amount of detritus—organic matter that accumulates on stream beds and serves as a vital food resource—did not significantly affect the overall fish assemblage. Yet for certain species, including habitat specialists, such changes proved critically important.

“This highlights a key conservation challenge,” Bandara said. “If we only look at total fish numbers or community-wide patterns, we may overlook serious declines occurring among environmentally sensitive species.”

Indicator Species as Ecological Sentinels

The findings underscore the importance of using so-called “indicator species” in environmental monitoring programmes.

Indicator species are organisms whose presence, absence or abundance reflects the health of an ecosystem. Because they respond rapidly to environmental change, they can provide early warnings of ecological degradation.

The Rakwana loach appears to fit this role exceptionally well.

“Species with narrow habitat requirements often act as ecological sentinels,” Bandara observed. “Monitoring them can provide a much clearer picture of ecosystem health than relying solely on broad biodiversity assessments.”

For conservation practitioners, this means that protecting sensitive endemic species may also help safeguard entire freshwater ecosystems.

Restoring Streamside Forests

Perhaps the study’s most important conservation message concerns the restoration of degraded riparian forests—the vegetation growing alongside streams and rivers.

Researchers argue that restoring these streamside habitats should be a priority in freshwater biodiversity conservation efforts.

Healthy riparian vegetation provides shade, reduces erosion, filters pollutants, enhances habitat complexity and supports the intricate ecological interactions upon which aquatic life depends.

“The restoration of degraded riparian forests is likely to be one of the most effective conservation measures for protecting freshwater biodiversity,” Bandara emphasised.

Such efforts could prove particularly valuable in landscapes where agricultural expansion has fragmented natural habitats.

Awareness sessions

A Broader Lesson for Conservation

The study offers a timely reminder that freshwater conservation cannot be achieved by focusing exclusively on water bodies themselves. The surrounding landscape matters immensely.

From the mist-laden streams flowing down the Sinharaja foothills to the countless rivulets nourishing Sri Lanka’s river systems, the fate of freshwater biodiversity is intimately linked to the health of adjacent forests.

As conservationists grapple with accelerating habitat loss and climate-related pressures, the research demonstrates that protecting and restoring forest cover may be just as important as safeguarding the streams themselves.

In the case of the elusive Rakwana loach, the message is clear: save the forest, and you may save the fish.

For Sri Lanka’s unique freshwater biodiversity, that lesson could not be more important.

By Ifham Nizam

Sri Lankans have reason to take satisfaction in their country’s latest international achievement. Sri Lanka has climbed 14 places in the 2026 Global Peace Index to rank 67 in the world out of 163 countries that were assessed. At a time when global peacefulness is reported to be at its lowest level since the inception of the Index, and when more countries are experiencing deterioration than improvement, Sri Lanka’s progress stands out. The ranking reflects the country’s recovery from nearly three decades of war, its efforts to strengthen political stability and public security, and its resilience in overcoming the economic and political crises of recent years. The Global Peace Index assesses the strength of institutions, societal safety and security, and the capacity of societies to manage conflict peacefully.

The challenge is to consolidate the gains that have been made and address those unresolved issues that continue to cast a shadow over the country’s future. It is in this context that two recent announcements by the government assume particular significance. Foreign Minister Vijitha Herath has announced that the Prevention of Terrorism Act (PTA), one of the most controversial laws in the country, will be repealed and replaced within two months. A report prepared by a committee appointed to make recommendations has already been handed over to him. According to the minister, the new legislation, to be known as the State Prevention of Terrorism Act, incorporates recommendations from civil society and is intended to comply with international standards on counter terrorism.

At the same time, Justice and National Integration Minister Harshana Nanayakkara has reaffirmed the government’s commitment to uncovering the truth about missing persons. During a visit to the Chemmani mass grave excavation site in Jaffna, he stated that the excavations should be completed expeditiously so that justice can be done and assured that the necessary resources have been allocated for the task. The excavations are taking place under judicial supervision with the participation of forensic experts, archaeologists, lawyers and representatives of the Office on Missing Persons. These commitments made by the government address two of the most contentious issues that have troubled Sri Lanka for decades. They also suggest that the government believes the country is now in a position to deal with difficult questions from its past rather than postpone them indefinitely.

After Breakthroughs

The timing of the pledge to repeal the PTA is particularly noteworthy. For many years successive governments promised to replace the law but failed to do so. Sri Lanka undertook to repeal it in 2017 as part of its commitments linked to retaining GSP Plus trade concessions by the European Union. Yet despite repeated assurances the law remained in force. The question therefore arises as to why the government now appears determined to act. One possible explanation is that the Easter Sunday investigations have reached a decisive stage. The investigation into the bombings that killed more than 260 people in 2019 appears to have made significant breakthroughs. If these investigations continue along their present course, it is possible that accountability will extend beyond those who directly carried out the attacks to those who may have facilitated, enabled or been part of a wider criminal conspiracy.

There is broad agreement within society that those who masterminded the dastardly Easter bombing must be held accountable and that the victims deserve the truth and justice. However, it is important that the process by which responsibility is determined is seen by the public to be fair, lawful and impartial. If those accused are convicted following a transparent judicial process that respects due process and the rule of law, the outcome is far more likely to gain acceptance across society. This is where the repeal of the PTA becomes important. A transition from a law associated with prolonged detention and exceptional powers to one that is more consistent with human rights standards would strengthen rather than weaken the legitimacy of the investigations. Accountability obtained through a process that is visibly fair will be more durable and less vulnerable to allegations of political motivation or selective justice.

The Chemmani excavations may also provide an example of how such credibility can be built. The process is taking place under judicial supervision and in full public view with the participation of independent experts. Whatever conclusions emerge, and follow up action is decided on, the process itself should command respect because it is transparent and accountable. The same principles can be applied to the Easter Sunday investigations. Public confidence is strengthened when investigations are conducted openly, when legal safeguards are respected and when the rights of both victims and accused persons are protected. The significance of these investigations may extend beyond the tragedy itself. There is likely to be an overlap between those who are eventually found responsible for the Easter Sunday conspiracy and elements of the state apparatus that exercised power during the final stages of the war.

Setting Precedent

For many years Sri Lanka has struggled to address allegations of wartime abuses. The issue has remained politically sensitive because it touches upon the conduct of those who were regarded by many as wartime heroes. Yet if the Easter Sunday investigations establish that senior officials can be investigated and held accountable when evidence warrants it, an important precedent will have been set. Once the deck is cleared through the Easter Sunday investigations and the judicial process that follows, it may become less difficult to address allegations relating to wartime abuses, including those connected to sites such as Chemmani where evidence is now being painstakingly uncovered. This would also strengthen Sri Lanka’s position internationally.

Since the end of the war in 2009, the country has remained under varying degrees of scrutiny by the United Nations Human Rights Council. In October 2025, the Council renewed the mandate of the Office of the High Commissioner for Human Rights to continue collecting and preserving evidence relating to past violations. The next review of Sri Lanka is due in September this year. The government now has an opportunity to demonstrate that Sri Lanka is capable of addressing difficult issues through its own institutions and according to its own democratic values. The commitments to repeal the PTA and to pursue investigations into missing persons can be seen in that light. Those who were victimized query as to what happened to their loved ones and to the information they know full well they entrusted to the government authorities and to the commissions of inquiry that were appointed. These are opportunities to show that accountability and national ownership can go hand in hand.

Reconciliation requires the difficult task of remembering truthfully. Too often Sri Lanka has sought stability by postponing difficult questions. Yet unresolved grievances do not disappear. They persist across generations and continue to shape political attitudes and communal relationships. Sri Lanka’s rise in the Global Peace Index is an achievement worth celebrating. But the true measure of peace is not only the absence of conflict. It is the presence of justice, trust and confidence in public institutions. The government’s commitments on PTA repeal, the Easter Sunday investigations and the search for truth regarding the disappeared suggest an awareness that old approaches have run their course. The government has an opportunity to break with the patterns of the past. The test now lies in implementation.

by Jehan Perera

Animal Welfare Draft Bill to be Gazetted

Legal provisions on marking voters using indelible ink during elections removed

Showers will occur in the Western, Sabaragamuwa and North-western provinces and in Galle, Matara, Kandy and Nuwara-Eliya districts

Court vacancy row throws Parliament into turmoil; sittings disrupted

Climate, pollution, forest loss now hitting economy: BASL chief

GSP+ in jeopardy: GL

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoCreditor receives USD 2.5 mn as Lankan public bears loss from theft of Treasury funds

-

News4 days ago

News4 days agoCreditor not yet paid

-

News4 days ago

News4 days agoConsumers bearing 22% tax burden despite 18% VAT claim: Dr. Harsha de Silva

-

Opinion6 days ago

Opinion6 days agoBeyond diagnosis: A strategic design for 7% growth by 2029 (Part I)

-

Opinion5 days ago

Opinion5 days agoSriLankan Airbus struck by lightning

-

Features3 days ago

Features3 days agoNanda Pethiyagoda Wanasundara as three generations of family saw her

-

Latest News3 days ago

Latest News3 days agoSooryavanshi thumps fastest List A fifty as India A win tri-series

-

Editorial3 days ago

Editorial3 days agoFuel crisis: Beyond price debate