Features

The liberal centre lost, again. Will it ever learn?

By Uditha Devapriya

Victory may have many fathers, but defeat isn’t always an orphan. Just 24 hours after Donald Trump was declared as the 47th President of the United States, pundits and analysts are at it, trying to deconstruct perhaps one of the most consequential elections in US history and trying to find out what went wrong. The upshot of it is that yet another attempt at breaking the glass ceiling in the world’s supposed bastion of democracy has failed – though, unlike Hillary Clinton, Kamala Harris may return to the fight after the next five years are up. Until then, of course, a lot can happen. Not least of which, to the Democrats.

Victory may have many fathers, but defeat isn’t always an orphan. Just 24 hours after Donald Trump was declared as the 47th President of the United States, pundits and analysts are at it, trying to deconstruct perhaps one of the most consequential elections in US history and trying to find out what went wrong. The upshot of it is that yet another attempt at breaking the glass ceiling in the world’s supposed bastion of democracy has failed – though, unlike Hillary Clinton, Kamala Harris may return to the fight after the next five years are up. Until then, of course, a lot can happen. Not least of which, to the Democrats.

Since 1992, when George H. W. Bush lost to Bill Clinton, the Democratic Party has been pursuing, as a mantra, a policy of triangulation and squaring the circle. At each and every election, it touts its liberal centrist credentials and hangs on to them as though they will be a near-certain guarantor of victory. To his credit, Joe Biden swerved somewhat to the left – at least in certain aspects of Washington’s domestic economic agenda. Biden has been described as the most pro-worker American president since F. D. R.: no mean fit, even if the left-radical press takes issue with such praise.

What is pertinent is that, as the Biden presidency made clear, the Democrats’ shift to the left – real or imagined – could only be at the expense of its centrist charades. For better or worse, however, this was not a trade-off the party establishment were willing to take. From celebrity endorsements to lavishly funded National Conventions to carefully curated interviews, the Harris-Walz campaign signalled a return to the Democrats’ Clintonian roots: a policy of triangulation and of appeasing the moderates in the room. In the context of an increasingly polarising political landscape, however, this could achieve either of two things for the Democrats: a marginal victory, or a colossal loss.

At the last moment, the Republican rally at Madison Square Garden gave some hope to the Harris-Walz campaign. The rally was a naked display of wolf-whistling racism. But their response to it was, if not feeble, then predictable. Since 2016, when Trump announced his candidacy, liberals have constantly been using the fascist and Nazi label on his supporters. Whether or not the label fit, it became something of a thing to say.

What the Democrats should have understood, yet did not, is that their denigration of Trump and his supporters would enable a section of the Republican party itself to band together with them: a miniscule minority, but an influential segment nevertheless. That would give Trump’s campaign much needed fodder with which to both attack the Democrats and to claim themselves as the rightful heirs of the Republican Party. As Harris’s endorsement by Liz Cheney shows, this is exactly what happened.

People may have short memories, but sometimes memories don’t fade away that easily. It was certainly ironic that Harris found herself on the same podium as some of the most reviled GOPers from recent memory. The Cheneys called Trump an enemy of the country and the Constitution, likening him to a fascist demagogue.

Yet Cheney served as Vice President to one of the most questionable administrations in US political history, which not only passed the PATRIOT Act – an Act that Joe Biden and Barack Obama more or less approved of – but also whipped up the kind of Islamophobia and hatred of the Other, the kind of tax cuts and amnesties for the rich and powerful – that would distinguish the Trump presidency much later. As the liberal commentator Charles Blow put it in a New York Times op-ed in 2021, Liz Cheney herself began by endorsing if not supporting Trump’s initial actions – including his attacks on Hillary Clinton.

The Clintons, of course, must take some of the blame for what has befallen the Democratic Party. Yet from a certain perspective, they were also a product of their times in the same way Tony Blair was. Without overtly adulating him, it must be admitted that Bill Clinton saw through the largest peacetime economic expansion in US history. This is not an achievement Republicans can easily take away from him. But that expansion came at the expense of other priorities – most damnably, social welfare. As Clinton’s Labour Secretary, the sharp, intrepid Robert Reich put it in a speech which played a role in his dismissal from the administration, the then government’s pandering to financial interests, at the expense of workers and other deprived communities, could only fuel a popular backlash in the near-future.

The 2024 election signalled not the rise but the apotheosis of that backlash. In 2016, Democrats chastened by Trump’s victory could at least say he won the Electoral Colleges but not the popular vote. This time around, they don’t have even that consolation: Trump got six million more votes than Kamala Harris. When you consider that he achieved this even as Harris went around defending Israel, wooing “moderate” Republicans, and using the same talking points against her rival, and when every mainstream media platform predicted defeat of some kind for her rival, you realise just how bad things have got for her party.

In the 1990s, there were two distinct things which pointed to the rise of Trumpism. Robert Reich’s speech was one of them. The other was Joel Schumacher’s brilliant film Falling Down. It is ironic that almost exactly 30 years down the line – Reich made his speech in 1994, Schumacher’s film came out the previous year – we have progressed from bad to worse to much worse. In terms of responding to the moment and taking advantage of the opportune, there is no doubt that Trump has squared the circle. There is also no doubt that the old Democratic strategy of targeting the moderate has run its course. The question now is, what next? Or, to paraphrase Lenin, what is to be done?

Uditha Devapriya is a regular commentator on history, art and culture, politics, and foreign policy who can be reached at udakdev1@gmail.com.

Coal crisis far worse than first feared

Sri Lanka’s coal supply crisis is significantly deeper than previously understood, with senior engineers and energy analysts warning that a dangerous combination of reduced procurement volumes, rising coal consumption and shipment delays could place national power generation at serious risk.

Information reviewed by The Island shows that Lanka Coal Company (LCC) had originally planned to secure 2.32 million metric tons of coal for the relevant supply period to meet generation requirements at the Lakvijaya coal power complex.

Following procurement discussions, the final arrangement was to obtain 840,000 metric tons from Potencia, including a 10 percent optional quantity, and 1.5 million metric tons from Trident, equivalent to 25 vessels.

However, subsequent decisions resulted in the cancellation of four Potencia shipments, reducing that supplier’s volume to 627,000 metric tons. This brought the total expected procurement down to 2.16 million metric tons, creating an immediate 160,000 metric ton deficit, even before operational demand is considered.

“This is a major shortfall in any generation planning model,” a senior engineer familiar with coal operations said. “When stocks are planned to the margin, a reduction of this scale can have serious consequences.”

“This is a major shortfall in any generation planning model,” a senior engineer familiar with coal operations said. “When stocks are planned to the margin, a reduction of this scale can have serious consequences.”

Power sector sources said the deficit becomes more critical because coal consumption rates have increased by more than 10 percent, meaning larger volumes are now required to generate the same electricity output.

“In simple terms, the system is burning more coal for less efficiency,” an energy analyst told The Island. “That means the real shortage may be substantially larger than the paper shortage.”

Experts attributed the higher burn rate to ageing equipment, maintenance constraints and operating inefficiencies at the Norochcholai plant.

A third concern has now emerged in the form of shipment delays and possible unloading constraints, raising fears that even contracted supplies may not arrive in time to maintain safe reserve levels.

“If vessel schedules slip or unloading is disrupted, stocks can fall very quickly,” another senior engineer warned. “At that point, the country has little choice but to shift to costly thermal oil generation.”

Such a move would sharply increase electricity generation costs and place additional pressure on public finances.

Analysts said the convergence of three separate risks — procurement reductions, higher-than-expected consumption and delivery uncertainty — had created a serious energy planning challenge.

“This is no longer a routine procurement issue,” one industry observer said. “It has become a national power security issue.”

Calls are growing for authorities to disclose current coal inventories, incoming vessel schedules and contingency measures to reassure the public and industry.

With electricity demand expected to remain high and hydro resources dependent on rainfall, engineers caution that delays in addressing the coal gap could expose the country to avoidable supply disruptions in the months ahead.

By Ifham Nizam

LETTER

The capsizing of two boats in Lake Gregory on 19 April was merely an isolated incident. It has come as a stark and urgent warning that a far more serious tragedy is imminent unless decisive action is taken without delay.

Mayor of Nuwara Eliya, Upali Wanigasekera has publicly stated that stringent measures have been introduced to prevent similar occurrences. However, it must be noted that such measures are unlikely to yield meaningful results in the absence of a comprehensive regulatory framework governing Inland Water Adventure Tourism (IWAT) in Sri Lanka.

For decades, this sector has operated without any regulation. Despite repeated calls for reform, there remains no structured legal mechanism to oversee operational standards, safety compliance, or accountability. Consequently, there is chaos particularly in critical operational aspects of this otherwise vital tourism segment.

The situation in Lake Gregory is not unique. Other prominent inland tourism destinations, such as Kitulgala and Madu Ganga, face similar risks. Without urgent intervention, it is only a matter of time before a major calamity occurs, placing both local and foreign tourists in grave danger.

At present, there appear to be no enforceable legal requirements governing:

* The fitness for navigation of vessels

* Mandatory safety standards and equipment

* Certification and competency of boat operators

The display of permits issued by local authorities is often misleading. These permits function merely as revenue licences and should not be misconstrued as certification of compliance with safety or technical standards.

Furthermore, local authorities themselves appear constrained. The Nuwara Eliya Mayor is reportedly limited in his ability to enforce meaningful improvements due to the absence of legal backing. Compounding this issue is the proliferation of unauthorised operators at Lake Gregory, functioning with minimal oversight.

Disturbingly, there are credible concerns that some boat operators function under the influence of intoxicants, while enforcement authorities appear to maintain a lackadaisical stance. The parallels with the unregulated private transport sector are both evident and alarming.

In the absence of a proper legal framework, any victims of such incidents are left with no recourse but to pursue lengthy and uncertain claims under common law against individual operators.

The Minister of Tourism, this situation demands your immediate and personal intervention.

A robust regulatory framework for Inland Water Adventure Tourism must be urgently introduced and enforced. This should include licensing standards, safety regulations, operator certification, regular inspections, and strict penalties for non-compliance.

Failure to act now will not only endanger lives but also severely damage Sri Lanka’s reputation as a safe and responsible tourist destination.

The time for incremental measures has passed. What is required is decisive policy action.

Athula Ranasinghe

Public-Spirited Citizen

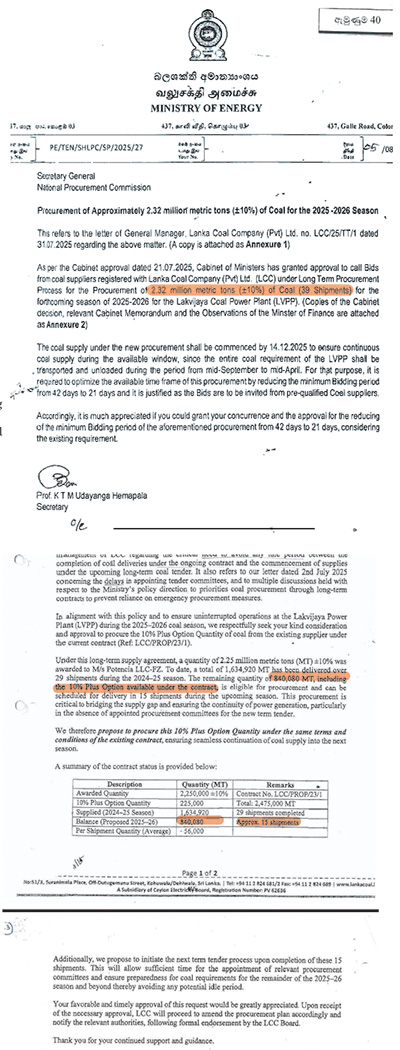

In an artful move that has wrongfooted its critics, the NPP government would seem to have orchestrated the resignation of Energy Minister Kumara Jayakody and Ministry Secretary Udayanga Hemapala, while simultaneously appointing a Special Presidential Commission of Inquiry to investigate whether any irregularities or unlawful actions have taken place in the business of importing coal for the Lakvijaya power station, by the state-owned Lanka Coal Company (Private) Limited. The Lanka Coal Company (LCC) had been created as early as 2008 under the Companies Act, following a cabinet decision in 2006, for the stated purpose of importing coal for power generation not only at Lakvijaya, but also other potential thermal power stations. The presidential COI could technically cover the entire lifespan of the LCC.

While the usual busybodies are busy raking the NPP government over substandard coal brought from South Africa by an Indian supplier who had not paid the full registration fee on time, the focus should really be on the performance of the LCC from its inception to the current sensation. The sole reason for the LCC’s being is to bring home about 40 +/- shiploads of coal that (at 60,000 Metric Tonnes of coal per shipload) for a total of approximately 2.25 million MT – the amount of coal that Lakvijaya requires for burning in one year to generate power at the full 900MW installed capacity.

Because of Lakvijaya’s location on the west coast, at Norochcholai, in the Puttalam District, without a proper harbour facility, the shipment is restricted to the six/seven-month non-monsoonal period – from September/October in one year to March/April the next. 40 +/- shiploads over six/seven months work out to six or seven ships a month. So, the company has the luxury of the other six/seven months (March/April to September/October) every year to plan, procure and deliver 2.25 million MT of coal to Lakvijaya, at competitive prices and to the required quality standards. Remember, it is not uranium we are importing, but coal. For one whole company that should be a QED (quite easily done) job – you would think. On the contrary, it has hardly been a QED.

The first question that comes to mind is whether a whole company is needed to arrange six to seven shiploads of coal a month for six months of the year. Now that a Presidential Commission of Inquiry (COI) has been set up, it would be interesting to see whether the Commission would also look into the reasons why the cabinet of ministers in 2006 decided to establish a new company for shipping coal. This was five years before the first phase of Lakvijaya power generation was completed in 2011 at one third (300MW) capacity, with full (900MW) generative capacity reached three years later in 2014. The construction of Lakvijaya had begun in 2006 and the LCC was created in 2007.

The country is familiar with all the construction delays and post construction problems of the storied power plant, but all the delays at the power plant should have given the LCC time to plan and put in place a streamlined mechanism for supplying coal. That has not been the case at all. That leads to other obvious questions – which are really about missing information regarding the sourcing and procurement of coal and ensuring its quality.

Sourcing and Procuring

First sourcing. It is generally known that the LCC has been importing coal from Australia, Indonesia, Russia – the world’s top three coal exporters, as well as South Africa. But there is no information on a supplier’s association with a particular country-source or the implications of switching from one country-source to another depending on the selection of a supplier. This information is not presented either in company documents (provided on its website and two annual reports (2017 & 2020) that are online) or in the audit reports including the most recent one which is also the most extensive one. As well, there is no source comparison by price or by quality – especially for the critical heating or calorific value, which is considered a “rank parameter” in quality evaluation of coal, and is fundamental to using coal in thermal power generation.

Point of Unloading: Lakvijaya Jetty

The second question or missing piece of information is about procurement. Every January, if I am not mistaken, the LCC calls for registration of suppliers based on past procurement experience, including conformance with quality standards, and corporate business performance. The LCC publishes the “Standard Values for Coal” for each year, which include the Gross Calorific Value (GCV, usually greater than 6,150 kcal/kg), moisture and material percentage contents, and grain sizes. These requirements are based on the manufacturer’s specifications, as they should be.

Registration applications are reviewed and approved for registration by cabinet-appointed committees mostly made up of senior CEB and relevant Ministry officials, and LCC and Lakvijaya representatives. What is not available is a historical record of registered suppliers, their quality history, and changes over time. This record could also include bid takers from among the registered suppliers, tender details and prices, and selected suppliers. The absence of such record and trend analysis would likely have been a factor in creating opportunities for alleged fraud, preferential selections and the compromising of quality standards.

The third question and concern is about the quality of imported coal, especially the minimum calorific value for efficient operation of the turbines. Far more than the other two, the quality issue has been front and centre in all the news about coal over the years, and it became the subject of some detailed analysis in the April 2026 Special Audit Report on Coal Procurement.

For the 2025/2026 coal supply, 26 registered suppliers were invited to bid on 18 August 2025, 11 of them responded, and their bids were opened on 15 September 2025. Quite a short window. Of the 11 bidders, only two had previously supplied coal exceeding the rejection threshold of 5,900 kcal/kg GCV; eight of them had both exceeded and fallen short of the threshold in their previous supplies; one did not exceed the threshold at all; and the last one did not provide any GCV information. The tender was awarded to Trident Chemphar Limited of India, whose past GCV record indicates supplying nearly 300,000MT of coal exceeding 5,900 GCV, and twice as much, nearly 600,000MT, under 5,900 GCV.

As noted in the Special Audit Report, Trident had not paid the full registration fee of $5,000 when bids were sent out on 18 August 2025 and should not have a received the invitation to bid. However, the LCC would seem to have found a way to have the tender documents sent to Trident, accept Trident’s late payment of the balance due of the registration fee, and have its registration ratified four days later on 22 August 2025. As the Audit Report has correctly observed, this was a violation of the principle of fairness in procurement, especially involving competitive bidding on a tender of substantial value.

Heat Quality and Testing

As I noted earlier, the LPP’s “Standard Values for Coal” stipulates a GCV (Gross Calorific Value) greater than 6,150 kcal/kg). A lower value of 5,900 kcal/kg is used as the benchmark to reject coal loads that fall below that value. In other words, the practice has been to use 6,150 kcal/kg as the quality standard for supply, rejecting loads that come under 5,900 kcal/kg, and making price adjustments for loads with GCV that fall between the two values. Lowering the tender threshold to 5,900 opens the door for accepting supplies under what (5,900) was earlier the rejection threshold as the new normal.

The lowering of the quality requirement before and after an apparent cabinet authorization came into effect 23 June 2023 apparently after a cabinet decision. Before June 2023, eligible suppliers should have supplied a minimum of one million MT in the previous 36 months, of which at least 50% (500,000 MT) should have equaled or exceeded the rejection threshold of 5,900 GCV. After June 2023, the business turnover was reduced from one million to half a million metric tonnes, and the quality amount was reduced from 500,000 MT to 100,000 MT. These changes came home to roost in the procurement of coal for the 2025/2026 period under the new (NPP) government.

As I have noted, the selected supplier, Trident Chemphar Limited of India, did not have a good record for heat quality supply, the company’s 36-month record indicating only one third of its supply exceeded the 5,900 GCV requirement. But it was still higher than the new, but lower, standard of a supply record of 100,000 MT exceeding 5,900 GCV. But worse was yet to come.

The Trident tender provides for only 1.5 million MT of coal and of the 2.32 million MT of coal required for 2025/2026. To procure the balance and to add redundancy to the main Trident supply (which is rather puzzling), the LCC initiated a second tender in January 2026 – interestingly, not for the full 800,000 MT balance, but only 300,000 MT of it. And the second competitive tender following all proper evaluation was awarded to Taranjot Resources (Pvt) Limited, also of India. Taranjot was one of the unsuccessful bidders in the August-September 2025 tender and had the distinction of being the only one who had recorded an entire 36-month supply of coal (100% of 1.1 million MT) under 5,900 GCV. Go Figure!

The price comparisons are also revealing. Trident’s price is $98.5 CFR per MT for a total price of $148 million (SLR 45 billion) for supplying 1.5 million MT of coal. Taranjot’s price for supplying 300,000 MT of coal is $142 CFR per MT for a total price of $42.6 million (SLR 13 billion). For comparison, Taranjot’s unit price was $105 CFR per MT, three months earlier, in the main tender that was awarded to Trident. Inexplicable as it is, this fixation to switch between term tenders and spot tenders has been demonstrated by the Lanka Coal Company from the time it started procuring coal for Lakvijaya. The reasons for this are another matter that the Presidential COI will hopefully look into.

To make matters worse, Trident’s actual supply turned out to be worse than its tender. The Special Audit Report provides the results of the quality tests on the coal that was supplied by Trident in its first nine shipments before 17 February 2026. There were three categories of tests performed over nine criteria, including the Gross Calorific Value (GCV) on samples taken from each shipment of coal – first at the Port of Loading, the Richards Bay Coal Terminal in South Africa, second at the Port of Discharge, and third in the Lakvijaya Laboratory – both in Puttalam, Sri Lanka.

The Port of Loading tests showed far better results on each criterion for each of the nine shipments than the Port of Discharge tests and the Laboratory tests. Specific to the GCV heat criterion, the South African tests showed the coal in seven of the nine shipments exceeded the standard value of 6,150 kcal/kg; one of them registered 6,053, just under standard value; and the other at 5,904, just above the rejection threshold. The discharge point tests in Sri Lanka showed none of the shipments meeting or exceeding the standard value (6,150), with only two exceeding 6,000 kcal/kg. The Laboratory test results were the worst, with every one of the nine shipments registering below the rejection threshold of 5,900 kcal/kg, with five of them between 5,000 and 5,500 kcal/kg, and the other four between 4,500 and 5,000 kcal/kg.

The discrepancies in the results should not be surprising given the rather shoddy arrangements for testing at the South African end. Although testing at the source is the supplier’s responsibility subject to LCC’s approval, it is reasonable to expect that after about 15 years in this business the LCC would have set up a pool of accredited testing agencies that it could draw from for each tender. The test agent, or a pool of them, should be identified in the tender to avoid shopping around after the award.

The Special Audit Report includes extensive calculations of the energy (kilowatt-hour) and cost implications of using low calorific coal. The calculations are based on a comparison with the supply of coal between 2020 and 2025. There were 194 shipments during that period, and all of them exceeded 6,000 kcal/kg GCV, with 139 out of 194 (72%) exceeding the standard value requirement of 6,150 kcal/kg. The country-sources of these shipments are not known, and there is no information about the tests conducted on samples from these shipments, including the consistency or discrepancy between test results from the three testing locations. Curiously, this period includes the 2023/2024/2025 years which came after the June 2023 changes in quality standards, but shipments in this period do not seem to have been adversely impacted by the June 2023 changes. This overlap is not identified or noted in the Audit Report.

The Report indicates that the average consumption of coal in the 2020-2025 period was 375 grams per kwh, in comparison to the higher average consumption rate of 444 gm/kwh estimated for the coal supplied by Trident, based on coal consumption and power generation information from Lakvijaya operators. The use of lower calorific coal triggers excessive coal consumption, inefficient power generation, and the need for alternative energy sources to compensate for the shortfall in coal power generation. The Audit Report estimates the cost of excessive coal consumption associated with Trident’s nine shipments to be SLR 2.24 million. At the same time, the supply agreement includes penalty for non-compliance which is estimated to be SLR 2.32 million. These estimates are useful indicators of the order of magnitude of losses when tenders go wrong. But they will be vigorously challenged if penalties are imposed or contract is terminated.

The current low calorific coal fiasco is not the first instance of tender sloppiness involving the Lanka Coal Company. There have been allegations of fraud when coal was purchased from Australia. In 2014, there was another controversy when after selecting a Singapore shipping company for supplying coal from Indonesia, the tender was altered to include a port of origin in Russia. In 2016, the Supreme Court declared a coal supply tender null and void and ordered it to be superseded by a new tender call. In 2017, then Minister of Power and Renewable Energy, Ranjith Siyambalapitiya, dissolved the entire LCC Board of Directors, over procurement malpractices between 2009 and 2016. While the NPP did inherit a mess, it also had enough time to review and rectify the tender process, to eliminate malpractices and live up to its own promises.

Savers squeezed by lower returns as liquidity surge eases borrowing costs

Procurement cuts, rising burn rates and shipment delays deepen energy threat

Banks alert customers to phishing attacks

ComBank expands agency banking network to 26 locations

Lake Gregory boat accidents: Need to regulate water adventure tourism

Arrest of Raju major breakthrough: Police

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News6 days ago

News6 days agoRs 13 bn NDB fraud: Int’l forensic audit ordered

-

News4 days ago

News4 days agoLanka faces crisis of conscience over fate of animals: Call for compassion, law reform, and ethical responsibility

-

News3 days ago

News3 days agoWhistleblowers ask Treasury Chief to resign over theft of USD 2.5 mn

-

News3 days ago

News3 days agoNo cyber hack: Fintech expert exposes shocking legacy flaws that led to $2.5 million theft

-

News7 days ago

News7 days agoChurch calls for Deputy Defence Minister’s removal, establishment of Independent Prosecutor’s Office

-

News4 days ago

News4 days agoUSD 2 mn bribe: CID ordered to arrest Shasheendra R, warrant issued against ex-SriLankan CEO’s wife

-

News4 days ago

News4 days agoParliament urged to probe questionable payment of USD 2.5 mn from Treasury

-

Opinion6 days ago

Opinion6 days agoMinisterial resignation and new political culture