Business

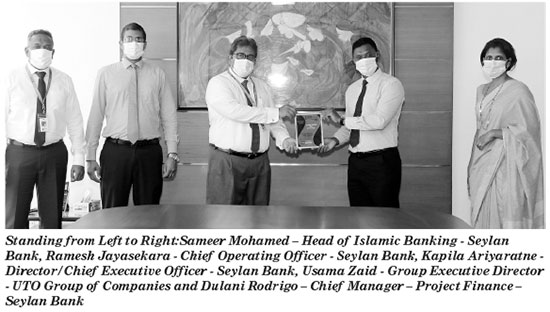

Seylan Bank’s Islamic Banking Wins Gold at SLIBFI Awards 2019 and Bronze at IFSSA Awards 2020 for Islamic Finance Deal of the Year

Seylan Bank PLC’s Islamic Banking Unit has placed Sri Lanka prominently in the world of Islamic Finance, securing the joint Gold Award for Deal of the Year 2019 at the recently concluded Sri Lanka Islamic Banking and Finance Industry (SLIBFI) Awards 2019 and Bronze for the same deal at the regional Islamic Finance Forum of South Asia (IFFSA) Awards 2020. Seylan Bank was recognized for successfully financing a Diminishing Musharaka Facility to Timex Bukinda Hydro (U) Ltd as part of a syndicate facility.

The SLIBFI Awards, the premium industry awards for Islamic Finance in Sri Lanka, are presented in conjunction with KPMG, whose key role is to ensure an impartial evaluation process. An independent panel of judges of repute assist in the final adjudications, under the guidance of KPMG. The IFFSA Awards recognize the high achievers in the South Asian region for their efforts in Islamic Banking and Finance during 2019 with industry leading practitioners from Pakistan, Bangladesh, Maldives, India, and other South Asian Countries competing alongside Sri Lanka for accolades.

“Islamic banking is broadly adopted around the world and the preferred choice for some of our clients. Seylan Bank’s Islamic Banking Unit takes pride in being able to facilitate such an important deal for our client. Furthermore, this multiple award-winning deal has also placed Sri Lanka firmly in the global Islamic Finance map” said Ramesh Jayasekara, Chief Operating Officer, Seylan Bank.

The Timex Bukinda Hydro (U) Ltd project transaction has resulted in Sri Lanka understanding the proficiencies and capabilities of Islamic Banking and Financing which has a mere 20-year history in the country. It also portrays Sri Lanka’s own management expertise and engineering capabilities in establishing hydro power plants overseas, thereby putting Sri Lanka on the Global Islamic Banking map.

Speaking on the dual awards M Z Sameer Mohamed, Head- Islamic Banking Unit – Seylan Bank stated, “We are very humbled by the recognition this transaction has received from the wider Islamic Finance community. It has firmly placed Sri Lanka as a partner of choice for future cross border transactions via Sharia compliant platforms, and also created confidence in Foreign Investors and other leading Islamic Financial institutions to obtain more syndicate financing facilities in achieving their corporate goals, which as a result would promote Islamic Finance.”

Seylan Bank, the Bank with a Heart, operates with a vision to offer the ultimate banking experience to its valued customers through cutting-edge technology, innovative products, and best-in-class service. The Bank has a growing clientele of SMEs, Retail and Corporate Customers and has expanded its footprint with 173 branches across the country and an ATM network of 216 units. Seylan Bank has been endorsed as a financially stable organisation with performance excellence across the board by Fitch Ratings, with the bank’s national long-term rating revised upward, from ‘A-(lka)’ to ‘A (lka)’. The bank was ranked second among public listed companies for transparency in corporate reporting by Transparency Global. Seylan Bank has also been named the Most Popular Banking Service Provider in Sri Lanka in Customer Experience by LMD consecutively in 2019 and 2020. These achievements are a testament to Seylan Bank’s financial stability and unwavering dedication to ensure excellence across all endeavours.

Sri Lanka private healthcare leaders recently pledged an action plan with timelines to address the practical priorities of Sri Lanka’s healthcare sector while making it more viable for local and foreign investments.

The Association of Private Hospitals and Nursing Homes (APHNH) has committed to converting recommendations from its first Healthcare Leadership Summit into a trackable outcome document with defined actions, responsibilities, and timelines, marking a shift from discussion to implementation in sector reform efforts.

The summit held on March 9 at Waters Edge, Colombo, brought together hospital leaders, policymakers, regulators, insurers, and international experts to address practical priorities for Sri Lanka’s healthcare sector.

A key outcome of the summit was APHNH’s plan to consolidate recommendations into a single, trackable charter that will outline specific actions, assign responsibilities, establish timelines, and provide periodic progress updates.

“Our objective is to bring the right decision-makers into one room and focus on what can be implemented, not only what can be discussed, ” said Raveen Wickremesinghe, President of APHNH. “We are committed to taking the inputs from today and converting them into a clear, trackable set of actions that strengthens quality, transparency and public confidence, while supporting national health priorities. “

The summit featured insights from Dr. Hafeez Rahman Padiyath, Dr. Hamdani Anver, and Chandana L. Aluthgama on scaling quality and operational discipline. A keynote and fireside discussion with Dr. Paiboon Eksangsri, President of the Private Hospital Association of Thailand, explored lessons from Thailand’s private healthcare development and conditions for making Sri Lanka more competitive for healthcare investment.

By Sanath Nanayakkare

Business

Atlas SipSavi Naththal Poronduwa records positive public participation, benefiting 10,000 students

Atlas, Sri Lanka’s No. 1 learning brand, successfully concluded Atlas SipSavi Naththal Poronduwa, a national initiative that saw strong public participation in supporting children at risk of dropping out of school due to financial hardship. At a time when more than 22,000 Sri Lankan children leave school each year due to rising economic challenges, the initiative reinforced Atlas Sipsavi’s long-standing ‘No Child Left Behind’ promise by turning seasonal generosity into meaningful educational support.

The initiative reached 10,000 students, with beneficiary schools carefully selected to ensure support reached those most in need. The collected books were distributed to children at risk of dropping out, including those whose education had been disrupted by recent adverse weather, ensuring students had essential learning resources at the start of the new school term. Through its flagship Atlas SipSavi programme, the brand focused on improving access to education by providing essential learning tools, scholarships, and infrastructure to create better learning environments, bringing its purpose of ‘making learning fun’ to life in a meaningful way. As part of the initiative, the public was invited to donate schoolbooks, with each contribution matched one-for-one by Atlas. Donation boxes were placed at all Keells outlets island-wide and at Sarvodaya District Offices, making it easy for communities to take part.

Business

John Keells Logistics expands strategic engagement with CWIT through inter-terminal transport operations

John Keells Logistics (Pvt) Ltd (JKLL), one of Sri Lanka’s leading third-party logistics solutions providers, has successfully expanded its operational engagement with Colombo West International Terminal (Private) Limited (CWIT), through inter-terminal transport services within the Port of Colombo. This enhanced engagement further strengthens CWIT’s efforts to improve operational efficiency, reliability, and scalability across terminal activities.

Inter-terminal transport plays a critical role in modern port operations, requiring high levels of coordination, precision, and operational discipline. JKLL’s appointment for ITT operations reflects CWIT’s confidence in the company’s demonstrated capabilities in managing complex transport operations within a high-throughput port environment.

The ITT operations are underpinned by JKLL’s technology-enabled logistics framework, incorporating real-time fleet tracking, performance monitoring systems, and data-driven operational planning. These capabilities provide enhanced visibility and control over transport movements, while ensuring compliance with established safety, productivity, and service quality standards.

The awarding of this engagement to JKLL is a testament to the successful implementation of the Inter-Terminal Vehicle (ITV) operations undertaken by John Keells Logistics at CWIT during the previous year. The ITV assignment was executed through structured operating procedures and disciplined service delivery, contributing to improved cargo movement, operational coordination, and service continuity within the terminal. The performance outcomes of the ITV operations provided the basis for the subsequent expansion of the partnership into ITT services.

Showers or thundershowers will occur at several places in the Western, Sabaragamuwa, Central, North-western and Uva provinces and in Galle, Matara, Mannar and Anuradhapura districts after 2.00 pm.

Bahrain & Saudi Arabia Grands Prix to be cancelled

Pink Floyd guitar sold for record-breaking $14.6m

Promoting Local Industries is a key priority of the Government – PM

Crypto loopholes funnel Lankan funds abroad

SLCERT urges Lankans not to get gypped by internet scams in run-up to festive period

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

News5 days ago

News5 days agoRepatriation of Iranian naval personnel Sri Lanka’s call: Washington

-

Features5 days ago

Features5 days agoWinds of Change:Geopolitics at the crossroads of South and Southeast Asia

-

News4 days ago

News4 days agoProf. Dunusinghe warns Lanka at serious risk due to ME war

-

Sports3 days ago

Sports3 days agoRoyal start favourites in historic Battle of the Blues

-

Sports2 days ago

Sports2 days agoThe 147th Royal–Thomian and 175 Years of the School by the Sea

-

News2 days ago

News2 days agoHistoric address by BASL President at the Supreme Court of India

-

News3 days ago

News3 days agoCEBEU warns of operational disruptions amid uncertainty over CEB restructuring

-

Features7 days ago

Features7 days agoThe final voyage of the Iranian warship sunk by the US