Business

5G to accelerate digital economy development in Sri Lanka

As Sri Lanka sets to include the spectrum for 5G in the upcoming frequency auction, the island will embrace 5G technology in the near future. Huawei advocates for accelerating 5G in line with Digital Economy development objectives during the First National Digital Consortia, organized by Information and Communication Technology Agency (ICTA). The week-long event aimed at building ties between multinational organizations, local businesses, local government, and encouraged the leading technology giants to be part of Sri Lanka’s digital transformation.

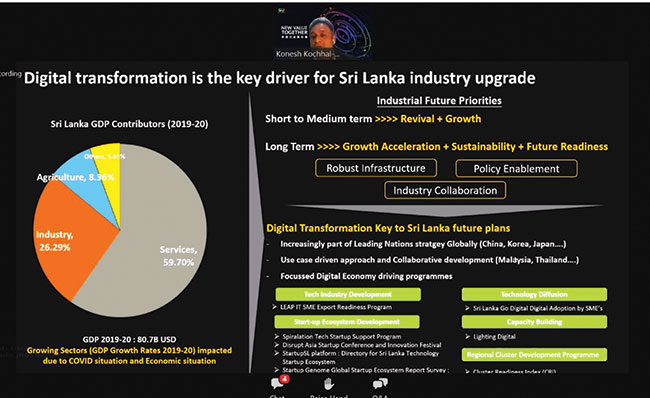

“Digital transformation is the key driver for the Sri Lanka industrial growth and higher productivity,” Huawei APAC Director of Industry Ecosystem Engagements, Konesh Kochhal highlighted that advancing Telecom and ICT technologies are key foundation enablers to achieve Digital Aspirations in Sri Lanka.

Whilst Sri Lanka has identified ‘Building a Technology-based society’ as a key national initiative in its National Policy Framework (NPF) named “Vistas of Prosperity and Splendour”, there are wider opportunities and room available in Sri Lanka for improvements even in more digitally mature sectors for digital transformation. A country needs to decode its National Strengths, prioritize digital developments, embark on vertical Industry digitalization, and leverage best practices through measurements, transparency, and collaborations. Kochhal highlighted that focused digital economy driving programmes such as Tech Industry development, Startup Ecosystem Development, Technology Diffusion, Capacity Building, and Regional Cluster Development defined in the ICTA’s Digital Economy Strategy are spot on and will be absolute essential for driving digital transformation of Sri Lanka.

Sri Lanka’s government has pledged to meet the Sustainability Development Goals of the United Nations. A digital economy with efficient digital infrastructure and skilled workforce will attract more investment and broaden trade relationships. Explaining on early 5G experience in several countries and the success of the digital economy, there have been studies showing that a 20% increase in ICT investments will lead to a 1% increase in GDP growth. In terms of investment efficiency, the ROI of ICT investments is 6.7 times higher than that of non-ICT investments. In addition, the global digital economy is growing 2.5 times faster than the global GDP.

In the past 10 years, the proportion of the digital economy in the global GDP has increased from 11% to 15%, according to experts. In the next 10 years, the proportion is expected to reach 24.3%, equivalent to $23 trillion US dollars in value. Thus, ICT technology investment and digital transformation will affect the entire economic and industry aspects. Nowadays, industries are experiencing digital transformation. More than 75% of the top 500 enterprises will transform the traditional business model into ICT digital service provider. Leading enterprises of various industries are already using digital or cloud technology, to innovate business & operating models, improve efficiency and experience, and benefit from digital dividends.

“The digital economy is characterized by fast growth, active innovation, and a wide impact, and it is becoming a key aspect in developing a new structure and mechanism for economic development. Currently, more than 170 countries have digital strategies” he said adding that “5G is not just a faster Internet connection for your smartphone, but that It is the foundation of tomorrow’s digital economy, powering everything from banks to hospitals to civil aviation and the management of cities. If 5G is going to support tomorrow’s complex digital systems, those systems must be made secure”.

Further elaborating on Sri Lanka’s present digital economy strategy, Kochhal highlighted that whilst ICTA’s Digital Economy Strategy includes utilizing existing programs and all relevant ecosystem partners to develop and implement an integrated Digital Economy transformation through higher operational efficiency, lower costs, and better services and outcomes for its citizens, there is still room for improvements even in more digitally mature sectors for digital transformation.

“Digitalization is fundamental to digital economy and it is important to develop infrastructure of telecommunications and ICT. Therefore encouraging the telecommunications and ICT sector development to expand along with inclusive growth will make Sri Lanka Digital. Technology investments could be adapted to address issues of national as well as regional importance and will also help Sri Lanka move up the technological ladder. Given current 4G penetration and experience in Sri Lanka, the immediate priority is to accelerate strengthening of the 4G layer both in terms of adoption, improved experience and ensure a robust foundation. As the local ecosystem gears up to accelerate all industry digitalization, people, industrial and enterprise digital demands will rise multi-fold in no time, we believe in order to address this 5G technology is essential to Sri Lanka” he said.

Sri Lanka has already emerged as the first South Asian nation to demonstrate a 5th generation mobile telephony in recent years. Earlier, Sri Lanka has been successful to become the country with the first operator in South Asia to start commercial operations of 4G-LTE services, after introducing 3G in 2006. Switching to 5G technology will encourage Sri Lankans to collaborate and create next-generation IoT and ICT innovations and serve the country’s digital footprint.

SLT‑MOBITEL Mobile, in collaboration with Fintelex (Pvt) Ltd, has launched ‘Yaya Agro’, an exclusive all‑in‑one smart agriculture app designed to empower Sri Lankan farmers with the tools they need to grow smarter, safer, and more sustainably.

Yaya Agro represents a new era of digital farming in Sri Lanka combining technology, expert knowledge, and community empowerment to provide farmers the confidence to make smarter decisions, improve productivity, and build a sustainable future.

Developed with support from GIZ and Hatch and validated by leading academic and professional institutions including the University of Colombo, Institute for Agrotechnology and Rural Sciences, and the Sri Lanka Red Cross Society, Yaya Agro combines agricultural expertise, real‑time weather updates, first aid support, and AI‑powered assistance into a single, easy‑to‑use platform.

The launch of Yaya Agro positions SLT‑MOBITEL as an innovative, inclusive, and collaborative technology leader. Partnering technology and academic institutions, the company extends its role outside the sector into agriculture, empowering farmers with AI‑driven tools, multilingual access, and market connectivity. The initiative also strengthens SLT‑MOBITEL’s image as a champion of digital empowerment and sustainable development in Sri Lanka.

Functioning as a comprehensive digital companion, Yaya Agro is positioned as a digital farming companion, bringing precision agriculture, real‑time support, and market access to the fingertips of every Sri Lankan farmer.

Whether managing a small home garden or a large commercial farm, the app equips farmers with vital insights to improve crop yield, reduce risks, and connect directly with buyers through the integrated online marketplace.

Yaya Agro offers farmers daily crop information with expert tips on management, pest control, and best practices, all validated by the University of Colombo. It provides accurate, location‑based weather forecasts to help plan farming activities more effectively. The app also delivers life‑saving first aid tutorials and safety information verified by the Sri Lanka Red Cross Society, ensuring farmers are prepared for emergencies. With the AI chatbot assistant, farmers can access instant, personalized advice around the clock, with smart notifications delivering timely alerts and reminders tailored to crop cycles.

To make learning inclusive and accessible, Yaya Agro is available in Sinhala, Tamil, and English, offering interactive educational content such as videos, voice guides, and infographics. The app also integrates an online marketplace, developed in partnership with GIZ and Hatch, enabling farmers to connect directly with buyers and expand their reach. (SLT‑MOBITEL )

Business

Kegalle sets up District Planning Committee to rein-in development spending under IMF-backed reforms

As Sri Lanka presses ahead with IMF-backed fiscal and governance reforms, the Kegalle District Planning Committee (DPC) was formally established yesterday as a standing sub-committee of the District Coordinating Committee (DCC), in a move aimed at tightening control over public investment, reducing duplication and strengthening monitoring at district level.

The committee was constituted under Home Affairs Circular No. 03/2025 issued by the Ministry of Public Administration, Provincial Councils and Local Government, and was inaugurated at the Kegalle District Secretariat auditorium under the leadership of Environment Minister and DCC Co-Chair Dr. Dhammika Patabendi and District Secretary H.M.J.M. Herath.

Addressing officials, Dr. Patabendi said the new structure directly responds to long-standing weaknesses in public investment management that have come under scrutiny during Sri Lanka’s engagement with the International Monetary Fund.

“Under the IMF programme, we cannot afford fragmented planning, overlapping projects or weak monitoring. This committee is about discipline—ensuring that limited public funds are allocated according to national priorities and deliver measurable outcomes,” Dr. Patabendi said.

He stressed that district-level planning must now align with national fiscal consolidation goals, with a stronger emphasis on value-for-money, results-based implementation and accountability.

The District Planning Committee will function as a permanent sub-committee of the DCC, chaired by the district’s Cabinet Minister, with the District Secretary serving as Secretary and the Director of Planning as Convener. Members include officials from district-level price and food committees and heads of government institutions or their nominees.

A central mandate of the committee is the preparation of an Annual Integrated District Development Plan, covering all funding sources—including foreign-funded and donor-supported projects—for approval by the District Coordinating Committee.

Officials said this would help rationalise project selection, prioritise urgent district needs and prevent the duplication of monitoring and evaluation systems, a key concern raised in public investment reviews under the IMF programme.

Dr. Patabendi noted that better coordination of state, private and non-state sector investments at district level would also support macro-level reform objectives by improving spending efficiency without increasing fiscal pressure.

“Fiscal adjustment does not mean stopping development. It means doing development better—through planning, coordination and proper evaluation,” he said.

The committee will oversee the operational rollout of DCC-approved projects, provide advisory support to implementing agencies, and monitor whether projects are delivered within approved timeframes and achieve stated targets.

Progress reports will be submitted to the Presidential Secretariat, Ministry of Public Administration, Ministry of Finance and the District Coordinating Committee, strengthening upward accountability.

At yesterday’s meeting, officials reviewed development proposals linked to the 2026 Budget, with focus on education, health, agriculture, infrastructure, industry, environment and tourism—sectors seen as critical for growth and social protection during the reform period.

Implementation challenges faced by projects carried out in 2025 across several Divisional Secretariat areas were also examined, with discussions centred on resolving bottlenecks early in 2026 and aligning future investments with the district’s five-year development plan.

Senior provincial and district officials, Members of Parliament from Kegalle, local authority heads and divisional secretaries attended the meeting.

Dr. Patabendi said the establishment of the District Planning Committee marked an important step towards embedding IMF-aligned public financial management reforms at the grassroots level, ensuring that development spending contributes to economic recovery while safeguarding fiscal sustainability.

By Ifham Nizam

Business

Allianz commits €200,000 for post flood recovery in Sri Lanka, part of €600,000 regional relief for Southeast Asia

Allianz SE (Headquartered in Munich, Germany) announced that it is donating €200,000 to support disaster relief efforts in Sri Lanka. In addition, Allianz SE is also extending its support to Thailand and Indonesia, contributing a further €400,000 to aid disaster relief across Southeast Asia. Torrential rainfalls have triggered severe flooding and landslides across Southeast Asia, leaving more than 1,100 people dead in a week of devastation and complicating rescue efforts for hundreds still missing. Allianz is deeply rooted with local entities in the three countries and serving millions of customers across Asia. By supporting the affected people and communities, Allianz acts on its promise to secure the future of its stakeholders in times of need.

Allianz SE will allocate €100,000 to the Sri Lanka Red Cross Society (SLRCS) to deliver immediate assistance to those most affected and €100,000 will also be provided for post-disaster support, implemented in collaboration with Allianz Insurance Lanka Limited and selected local partners, focusing on disaster prevention and climate resilience, helping communities rebuild and strengthen their preparedness against future events.

Renate Wagner, Member of the Board of Management of Allianz SE, responsible for Asia Pacific, Mergers & Acquisitions, People and Cultures says:

“At Allianz, we stand with the people and communities affected by the severe floods and landslides across Southeast Asia. Through immediate relief and long-term resilience support, we aim to help families recover, strengthen local communities, and better prepare for future climate-related events.”

Anusha Thavarajah, Regional Chief Executive Officer, Allianz Asia Pacific adds:

“Across Indonesia, Thailand and Sri Lanka, many families and communities are facing significant loss and disruption. In moments like these, Allianz stands alongside them. Asia Pacific is home to our people, our customers, and the communities we serve, and we remain deeply committed to the region. Our immediate focus is on providing relief where it is most needed, while also supporting communities to rebuild and strengthen resilience, so those most affected can move forward with confidence.”

Allianz is fully dedicated to Asia and its people. It represents a strategic growth region for Allianz Group, which already has established strong market positions throughout Southeast Asia. Besides Indonesia, Thailand and Sri Lanka, Allianz is present with various business segments in China, India, Malaysia and Singapore, among others.

BCB issues show cause notice to Nazmul Islam but Bangladesh players firm on boycott

From behind bars, Aung San Suu Kyi casts a long shadow over Myanmar

Senegal beat Egypt 1-0 in AFCON semifinal as Sadio Mane scores late

Trump says he’s been assured killings in Iran ‘stopped’

Let’s build a new Sri Lanka upholding harmony, mutual respect by protecting the religious and cultural rights of others- PM

Ambassador of the United States of America to Sri Lanka pays farewell call on PM

‘Dates have the highest sugar content to fight Coronavirus’

Sunday Island 27 December – Headlines

#SundayIsland 17th December – Headlines

Sunday Island – 28th March

Sunday Island Headlines – 21 March

Sunday Island – 21st February – Headlines

-

Business4 days ago

Business4 days agoDialog and UnionPay International Join Forces to Elevate Sri Lanka’s Digital Payment Landscape

-

News4 days ago

News4 days agoSajith: Ashoka Chakra replaces Dharmachakra in Buddhism textbook

-

Features4 days ago

Features4 days agoThe Paradox of Trump Power: Contested Authoritarian at Home, Uncontested Bully Abroad

-

Features4 days ago

Features4 days agoSubject:Whatever happened to (my) three million dollars?

-

News4 days ago

News4 days agoLevel I landslide early warnings issued to the Districts of Badulla, Kandy, Matale and Nuwara-Eliya extended

-

Business1 day ago

Business1 day agoNew policy framework for stock market deposits seen as a boon for companies

-

Opinion6 days ago

Opinion6 days agoThe minstrel monk and Rafiki, the old mandrill in The Lion King – II

-

News4 days ago

News4 days ago65 withdrawn cases re-filed by Govt, PM tells Parliament